June 9, 2026

The Invisible Infrastructure That Determines Where Exploration Capital Flows

Long before a single drill rod turns in African soil, a far less visible competition is already underway. It takes place in licensing offices, regulatory frameworks, and policy chambers where the conditions that either attract or repel exploration capital are quietly being constructed or dismantled. The global energy transition has created an unprecedented demand signal for transition-critical minerals, and Africa sits atop some of the world's most significant deposits of those very materials. Yet geological endowment alone has never been sufficient to generate sustained investment flows. The real competition in 2026 is institutional, not geological.

Understanding why Africa mining investment conditions have become such a focal point for the global mining industry requires looking beyond the headline reserve figures and examining the structural mechanics of how exploration capital actually behaves.

When big ASX news breaks, our subscribers know first

Africa's Mineral Position in a Fragmenting World

The architecture of global supply chains has shifted materially over the past several years. Deglobalisation, strategic decoupling between major economies, and the acceleration of clean energy deployment have collectively elevated the status of mineral-rich jurisdictions in ways that would have seemed overstated a decade ago. Africa's position within this reconfigured landscape is genuinely significant.

The continent holds substantial shares of several minerals that sit at the core of the energy transition, with critical minerals demand intensifying across global markets:

- The Democratic Republic of Congo accounts for roughly 70% of global cobalt production, a material essential for lithium-ion battery cathodes (U.S. Geological Survey, 2024).

- South Africa and Gabon together produce the majority of the world's manganese, a critical input for battery manufacturing and steel production.

- Guinea holds approximately one quarter of the world's known bauxite reserves, making it the largest global supplier of the aluminium precursor.

- Tanzania and Mozambique host significant graphite deposits increasingly relevant to anode material supply chains.

- Zimbabwe has emerged as a notable lithium producer, with the Bikita and Arcadia deposits drawing significant international attention.

What has changed in 2026 is not the existence of these deposits but the intensity of international interest in securing access to them. Nations are actively competing for mineral partnerships, and the strategic calculus has shifted from Africa being viewed as a resource frontier to being recognised as an indispensable supply partner. The question, as articulated at the Junior Indaba conference held in Johannesburg in June 2026, is no longer whether Africa possesses the resources. The defining challenge is whether the institutional, regulatory, and infrastructure conditions exist to convert geological wealth into sustained investment.

What Investment Readiness Actually Requires

The Four Pillars of a Competitive Mining Jurisdiction

Industry practitioners consistently identify four interconnected conditions that determine whether a jurisdiction attracts or repels exploration capital: policy stability, regulatory efficiency, infrastructure adequacy, and social licence. Each of these operates as both an independent variable and a system component. Weakness in one pillar degrades the effectiveness of the others.

Exploration capital is inherently mobile and highly selective. Unlike production-stage financing, which is anchored to specific assets, early-stage exploration investment can be redirected to alternative jurisdictions within a single budget cycle. This asymmetry fundamentally changes the negotiating position between governments and investors at the exploration stage.

Junior mining companies are disproportionately sensitive to jurisdictional conditions compared with major mining houses. A major company with an established asset base, diversified revenue streams, and institutional relationships can absorb regulatory friction in ways that a junior explorer with limited capital and a single-project focus simply cannot. This distinction matters enormously for Africa's mining development strategy, because it is junior companies that historically drive the discovery phase of the mining cycle. Furthermore, junior exploration investment patterns suggest this gap in sensitivity is growing wider as capital becomes more selective.

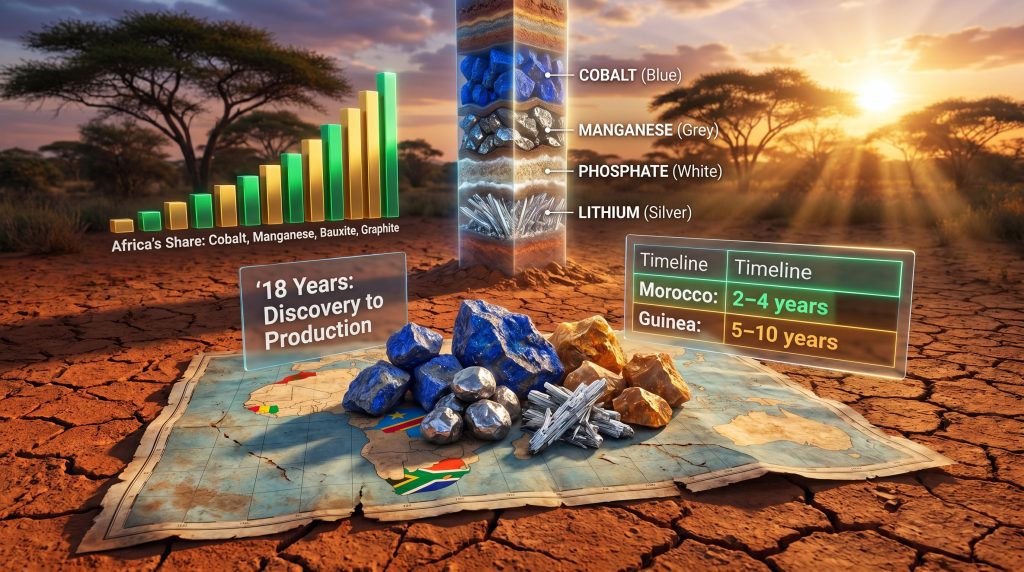

The 18-Year Timeline and Why Permitting Speed Is Disproportionately Important

One of the most underappreciated facts in mining investment analysis is the duration of the development cycle. The industry benchmark from initial discovery to first production spans approximately 18 years, a timeline that encompasses exploration, resource definition, feasibility studies, permitting, financing, construction, and commissioning. Within this sequence, mining permitting delays do not simply add time. They compound capital costs, erode investor confidence, and can render marginal projects economically unviable before a single tonne of ore is processed.

The following table illustrates estimated permitting timelines across key African jurisdictions, benchmarked against the broader competitive context:

| Jurisdiction | Estimated Permitting Timeline | Key Bottlenecks |

|---|---|---|

| South Africa | 3–7 years (variable) | Policy uncertainty, licensing backlogs |

| DRC | 4–8 years | Governance, contract stability |

| Morocco | 2–4 years | Relatively streamlined, stable |

| Guinea | 5–10 years | Infrastructure, political risk |

| Zimbabwe | 4–7 years | Regulatory reform in progress |

| Canada (benchmark) | 2–5 years | Environmental assessment, Indigenous consultation |

| Australia (benchmark) | 1–4 years | State-based systems, generally efficient |

The competitive implication is stark. When African permitting timelines extend to the upper bounds of these ranges, the total project development period can approach or exceed two decades. For junior explorers operating under capital constraints, that timeline is simply incompatible with the risk-return expectations of their investor base.

The Biggest Barriers Identified by Industry in 2026

Policy Certainty: The Primary Obstacle

At the Junior Indaba conference in June 2026, attendees participated in a live polling exercise asking what Africa lacks most when it comes to stimulating junior mining activity. The results were unambiguous. Policy certainty received the overwhelming majority of responses, outranking investment availability, collaboration frameworks, and project pipelines as the most critical missing ingredient.

This result carries important implications. Governments that assume exploration capital will flow if mineral endowment is sufficient are operating on a fundamentally flawed model. The polling data suggests that investors already understand Africa's geological case. What they are less confident about is the institutional environment in which they would be deploying capital.

Resource nationalism trends across parts of the continent have amplified this concern. Export restrictions, retroactive royalty adjustments, and mining code amendments introduced without adequate consultation have created a pattern of regulatory unpredictability that exploration-stage investors find particularly difficult to price. Unlike operating mines that generate cashflow and can absorb sudden cost increases, exploration projects generate no revenue during their development phase and are therefore acutely vulnerable to any deterioration in fiscal or regulatory conditions.

Cadastral Systems: The Foundation That Cannot Be Substituted

A cadastral system in the mining context is a publicly accessible, legally recognised registry that maps mineral tenure rights, including claim boundaries, ownership details, and licensing status. Its function is to provide verifiable certainty about who holds which rights over which ground. Without a functional cadastral system, investors cannot confirm that the licences they are acquiring or exploring on are legally secure, free from competing claims, or accurately demarcated.

At the Junior Indaba, industry voices were clear on this point: while a modern cadastral system will not resolve every challenge facing Africa's exploration sector, it is impossible to build a globally competitive exploration industry without one. The absence of transparent, digitised land tenure administration creates an insurmountable obstacle at the earliest and most critical stage of the mining value chain.

Countries making meaningful progress on cadastral modernisation include Zambia, which has invested in digital mining cadastre platforms, and parts of francophone West Africa where donor-supported reform programmes have produced improvements in tenure transparency. The gap between leaders and laggards on this metric is widening, and it is increasingly reflected in exploration expenditure allocation decisions.

Infrastructure and Energy as Structural Constraints

Mining is among the most energy-intensive industrial activities in any economy. The consequences of unreliable power supply extend well beyond operational inconvenience. Load-shedding and grid instability force mining operations onto diesel-generated backup power, materially increasing operating costs and creating financial structures that reduce competitiveness against jurisdictions with stable power infrastructure.

South Africa's experience provides a cautionary case study. Despite possessing a mature legal framework, well-developed infrastructure relative to regional peers, and a sophisticated capital market with established mining finance expertise, the country's prolonged struggle with electricity supply instability has eroded its competitive positioning as a destination for new mining investment. The reputational and economic damage from energy insecurity compounds over time in ways that are difficult to reverse even when the immediate supply problem improves.

Transport infrastructure gaps compound these challenges. In many parts of Sub-Saharan Africa, inadequate rail corridors and port capacity mean that ore transport costs can represent a disproportionate share of total operating expenditure, transforming deposits that would be economically viable elsewhere into stranded assets.

Political and Governance Risk: Distinguishing the Types

It is analytically useful to distinguish between two categories of risk that are frequently conflated in discussions of African mining investment:

- Political risk encompasses regime change, armed conflict, expropriation, and the instability that follows abrupt transitions of power.

- Governance risk refers to corruption, bureaucratic unpredictability, selective enforcement of regulations, and the unreliability of contract enforcement through the judicial system.

Both matter, but they operate on different timescales and through different mechanisms. Political risk tends to be acute and episodic. Governance risk is typically chronic and cumulative. For long-duration mining investments, chronic governance risk often poses a greater practical challenge than episodic political disruption, because it erodes the day-to-day operational environment continuously rather than creating identifiable crisis points.

A third category deserves increasing attention: community-level social risk. Local opposition, land use disputes, and protest activity can halt mining operations independently of national political conditions. Securing what practitioners now describe as social licence is increasingly a commercial prerequisite rather than a discretionary corporate responsibility consideration. As the Atlantic Council notes, critical minerals investment must actively avoid repeating historical missteps in African mining that damaged community trust.

Country-Level Investment Conditions: A Comparative Framework

| Country | Mineral Strengths | Investment Climate Assessment | Key Risk Factors |

|---|---|---|---|

| South Africa | Gold, PGMs, coal, manganese | Mature legal framework, established mining finance | Power instability, policy uncertainty, licensing delays |

| Morocco | Phosphates, cobalt, silver | Stable politics, business-friendly regulatory environment | Limited mineral diversification beyond phosphates |

| DRC | Cobalt, copper, coltan | Enormous endowment, growing international interest | Governance, infrastructure deficits, contract risk |

| Guinea | Bauxite, iron ore, gold | World-scale reserves | Political volatility, infrastructure gaps |

| Zimbabwe | Lithium, platinum, chrome | Active reform agenda | Regulatory unpredictability, currency instability |

| Gabon | Manganese, iron ore | Established production base | Post-political transition uncertainty |

South Africa's Strategic Choice

South Africa occupies a paradoxical position in the African mining investment landscape. It possesses the most developed mining legal framework, the deepest capital market expertise, the strongest infrastructure base, and the longest institutional history of any mining jurisdiction on the continent. And yet, the country's competitive standing is under sustained pressure.

Junior Indaba chairperson Bernard Swanepoel framed this tension directly at the June 2026 event, stating that South Africa faces a choice between continuing to debate its challenges and actively restoring its global competitiveness. He noted that investors have options, that exploration capital is mobile and selective, and that good intentions alone are insufficient. Competitiveness, measured in practical operational and regulatory terms, is what ultimately determines where capital flows. (Mining Weekly, Junior Indaba, June 9, 2026)

The reform levers available to South Africa are well understood within the industry. They include cadastral modernisation, licensing process redesign, energy policy reform, and the introduction of incentive structures specifically designed to attract junior exploration companies. The constraint is not analytical. It is political will and implementation capacity.

The Junior Mining Imperative: Why Early-Stage Exploration Cannot Be Taken for Granted

Historical Discovery Patterns and Their Implications

The historical record of mineral discovery is unambiguous: major deposits are overwhelmingly identified by junior companies and individual explorers, not by mining majors. Large companies acquire and develop deposits, but they typically do not find them. This division of labour reflects the different risk tolerances, capital structures, and operational models of the two categories.

Junior explorers operate closest to the geological frontier. They take on the highest technical and financial risk at the stage when the probability of success is lowest and the potential upside is greatest. This is precisely the activity that the current critical minerals supercycle makes most valuable. Without a functioning junior exploration sector, the pipeline of future mines does not get built.

What distinguishes environments that support junior exploration from those that do not comes down to a specific set of conditions:

- Transparent and predictable licensing processes that allow permit applications to be processed within commercially viable timeframes.

- Low-cost access to cadastral data and exploration permit systems that do not impose prohibitive administrative burdens on small-capitalisation companies.

- Collaborative frameworks that connect governments, capital providers, and explorers in a structured dialogue about what is working and what is not.

- Political risk insurance and blended finance mechanisms that help reduce early-stage capital exposure in jurisdictions where institutional risk is elevated.

The next major ASX story will hit our subscribers first

The Policy Architecture Required to Unlock Investment

A Four-Stage Reform Roadmap

Industry consensus, reflected in discussions at forums including the Junior Indaba, points toward a sequenced policy reform architecture for African mining jurisdictions seeking to improve their investment conditions:

- Foundational reforms: Implement or modernise cadastral systems, reduce and standardise permitting timelines, establish transparent and stable royalty frameworks, and ensure that mining codes are not subject to retroactive amendment.

- Infrastructure enablement: Address energy supply reliability, develop transport corridors that connect mineralised zones to export infrastructure, and increase port capacity in key commodity export nodes.

- Value chain development: Create incentive structures for in-country processing and beneficiation, establish technology transfer frameworks with international partners, and build the industrial base required for downstream value addition.

- Ecosystem building: Develop local capital markets capable of financing junior exploration, invest in technical skills development, and establish community benefit-sharing frameworks that build durable social licence. In addition, exploring capital raising options designed specifically for junior miners can support this final stage significantly.

This sequencing matters. Attempting value chain development before foundational regulatory and infrastructure conditions are in place tends to produce outcomes that are economically uncompetitive and operationally fragile.

Regulatory Transparency as a Competitive Differentiator

A counterintuitive finding from jurisdictional competitiveness research is that tax rates and royalty levels are not the primary determinants of exploration investment allocation decisions. Predictability and transparency consistently rank higher than cost minimisation in investor preference surveys. An investor can model a known tax burden into a project's economics. An investor cannot reliably model regulatory uncertainty.

This insight has practical implications for African policymakers. Jurisdictions that prioritise regulatory clarity and consistency, even at relatively higher fiscal rates, tend to attract more sustained exploration investment than those that offer low initial rates but generate uncertainty through frequent amendments, opaque administrative processes, or inconsistent enforcement. Furthermore, progressing to a definitive feasibility study becomes considerably more straightforward in jurisdictions where the regulatory environment is transparent and stable.

Frequently Asked Questions: Africa Mining Investment Conditions

What is the biggest challenge for mining investment in Africa?

Policy certainty consistently ranks as the primary barrier to investment, as confirmed by industry polling at the 2026 Junior Indaba. Regulatory inefficiency, infrastructure gaps, and political or governance risk follow in the assessment of most industry practitioners.

Which African country offers the most favourable mining investment conditions in 2026?

South Africa and Morocco are generally considered the most structurally stable, though each carries distinct limitations. South Africa offers a mature legal and institutional framework but is constrained by energy instability and licensing delays. Morocco offers political stability and a business-friendly environment but has limited mineral diversification. The optimal jurisdiction depends on the investor's target mineral and risk tolerance.

Why is the junior mining sector so important to Africa's critical minerals strategy?

Junior companies historically drive the discovery phase of the mining cycle. Without active junior exploration, the pipeline of future mines cannot be developed. The current critical minerals supercycle creates an outsized opportunity for junior explorers in Africa, but only if the conditions that support early-stage exploration are in place.

What is a cadastral system and why does it matter?

A cadastral system is a formal, publicly accessible registry of mineral tenure rights. It maps claim boundaries, ownership details, and licensing status. Without a functional cadastral system, investors cannot verify that the rights they are acquiring are legally secure, making exploration capital allocation extremely high-risk.

What reforms would most improve Africa's mining investment conditions?

The highest-priority reforms, as identified by industry consensus, are cadastral modernisation, permitting timeline reduction, stable and transparent royalty frameworks, and investment in energy infrastructure. These foundational conditions must precede more ambitious value chain and beneficiation objectives.

Converting Geological Advantage Into Investment Reality

The argument for Africa's mineral significance has effectively been won. The continent's endowment in cobalt, manganese, bauxite, lithium, graphite, and platinum group metals positions it as a structurally important supplier for the technologies underpinning the global energy transition. That case does not need to be made again.

What requires urgent attention is the gap between geological potential and institutional performance. Every year of policy inaction or regulatory inefficiency represents exploration capital that flows to other jurisdictions. Australia, Canada, and parts of Latin America continue to attract substantial shares of global exploration spending not because they have superior mineral endowments but because they have built the conditions that make deploying capital predictable and legally secure.

Bernard Swanepoel's framing at the Junior Indaba captured the essential dynamic: mining is ultimately a business of faith, patience, and perseverance, and it occasionally demands that participants move well outside their comfort zones. However, faith, patience, and perseverance cannot substitute for the foundational conditions that allow Africa mining investment conditions to support rational capital deployment. (Mining Weekly, Junior Indaba, June 9, 2026)

The opportunity cost of delay is not abstract. It is measured in undiscovered deposits, unbuilt mines, and economic development foregone. Africa's mineral endowment is a generational asset. The institutional window to capture its full value within the current critical minerals supercycle is defined, finite, and narrowing. The continent's governments, regulators, and industry participants collectively hold the conditions for success. Whether those conditions are built with sufficient urgency remains the open question that 2026 has yet to answer. For a broader perspective on why Africa's mining sector represents a compelling long-term investment strategy, the case ultimately rests on closing this gap between endowment and execution.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Mining investment involves significant risks including geological, regulatory, political, and financial uncertainties. Readers should seek independent professional advice before making any investment decisions. Forecasts and projections referenced in this article are subject to material uncertainty.

For further coverage of Africa's evolving mining investment landscape and junior mining sector developments, visit Mining Weekly, which provides ongoing reporting on the Junior Indaba conference series and related industry developments.

Want to Track the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex geological and commodity data into actionable investment insights for both short-term traders and long-term investors — explore historic discoveries and their returns to understand the potential, then begin your 14-day free trial to position yourself ahead of the market.