May 23, 2026

The Hidden Materials Cost Powering the AI Economy

Most conversations about artificial intelligence centre on algorithms, model architectures, and the race between technology companies to deploy the most capable systems. Far less attention falls on the physical substrate that makes any of it possible. Before a single AI inference runs, before a training cluster processes one token, an enormous quantity of raw materials must be mined, refined, fabricated, and installed. Among those materials, copper sits at the centre of a supply challenge that the technology industry has been slow to recognise and that commodity markets are only beginning to price.

Understanding why AI growth in data centers driving copper demand is occurring at an unprecedented scale requires stepping back from the software narrative and engaging with the unglamorous physics of electricity delivery, thermal dissipation, and signal transmission. These are the domains where copper's unique properties make it functionally irreplaceable, and where the gap between what the AI buildout requires and what the mining industry can supply is widening at a pace that has serious implications for infrastructure timelines, commodity prices, and investment strategy.

When big ASX news breaks, our subscribers know first

Why Hyperscale AI Infrastructure Is Fundamentally Different From Anything Built Before

The data center industry has existed for decades, but the facilities being constructed today to support large-scale AI training and inference workloads bear only a superficial resemblance to their predecessors. A conventional enterprise data center might draw between 5 and 10 megawatts of power, enough to house general-purpose computing for a mid-sized organisation. The hyperscale campuses being commissioned by major technology operators regularly exceed 100 megawatts, with some next-generation facilities designed around 500 megawatts or more.

This is not a modest incremental increase. It represents a fundamental restructuring of what a computing facility actually is. At these power levels, the facility stops being primarily a building that houses servers and becomes, in practical engineering terms, a small power station attached to a computing complex. Every watt of power delivered to those server racks must travel through copper conductors from the grid connection point, through high-voltage switchgear, through transformer banks, through distribution panels, and ultimately to the rack-level power delivery hardware. The cumulative copper content across that delivery chain scales almost linearly with total power draw.

The Three Copper-Intensive Systems Inside Every AI Data Center

Copper's role in hyperscale AI infrastructure concentrates across three distinct functional domains, each of which compounds the total per-facility requirement:

-

Power delivery infrastructure: High-voltage cables, busbars, switchgear conductors, transformer windings, and low-voltage distribution systems collectively account for the largest share of copper content. At 100+ MW draw, the conductor cross-sections required are substantially larger than anything used in conventional facilities.

-

Thermal management systems: AI accelerator chips, particularly graphics processing units (GPUs) and custom AI chips, generate heat densities that legacy cooling architectures cannot manage. Liquid cooling loops, cold plates, and heat exchangers used in advanced thermal management systems rely heavily on copper tubing and heat exchange surfaces because copper's thermal conductivity of approximately 401 W/m·K outperforms aluminium by roughly 60%, making it the material of choice where space and efficiency constraints are most severe.

-

High-bandwidth network fabric: The interconnects linking thousands of GPUs within a training cluster require low-latency, high-throughput copper cabling at short distances. While fibre optic cable handles longer-distance runs, copper-based direct attach cables and twinaxial cabling dominate within-rack and top-of-rack connectivity where signal integrity and latency requirements are most demanding.

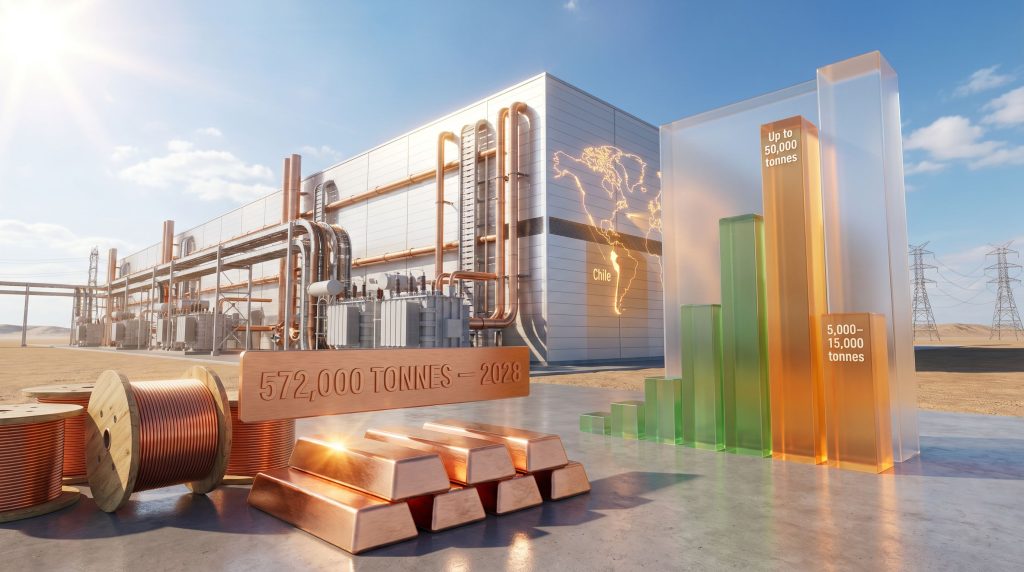

The combined effect of these three systems is a copper consumption profile that industry analysts estimate at up to 50,000 tonnes per hyperscale facility, compared to 5,000 to 15,000 tonnes for a conventional data center. This three-to-ten-fold intensity differential is the core arithmetic driving the demand surge. Furthermore, as BHP's analysis of AI and data centres highlights, this copper intensity is only expected to grow as AI workloads become more complex and power-hungry.

Quantifying the Demand Surge: What the Forecasts Actually Show

Translating per-facility copper intensity into aggregate market impact requires understanding the pace of hyperscale construction. In 2024 alone, primary US data center markets had 6.3 gigawatts of capacity under active development, a record figure that reflected the acceleration in AI infrastructure investment following the widespread commercialisation of large language models.

Goldman Sachs research projects that data center power demand will increase by 165% by 2030, a trajectory that would push US data centers from approximately 5% of national electricity consumption today to around 14% within the same timeframe. This power growth translates directly into copper demand through the delivery infrastructure described above. The critical minerals demand implications of this trajectory are profound and extend well beyond copper alone.

The aggregate demand picture that emerges from these construction rates points to a significant and sustained new demand category for copper markets:

| Timeframe | Projected AI Data Center Copper Demand | Key Driver |

|---|---|---|

| Peak Year (2028) | ~572,000 tonnes | Concentrated hyperscale buildout |

| Annual Average (2028-2038) | ~400,000 tonnes per year | Sustained expansion and refresh cycles |

| Long-Term (2050) | ~3,000,000 tonnes per year | Six-fold growth from 2025 baseline |

These projections, if realised, would elevate data centers from roughly 1% of global copper consumption today to as much as 7% by 2050, making the sector one of the largest single end-use categories in global copper markets, comparable in scale to entire national industrial economies.

The Campus Multiplier Effect Most Analysts Miss

A detail that aggregate demand figures tend to obscure is the copper requirement that extends beyond the facility boundary. Each new hyperscale campus requires dedicated grid interconnection infrastructure, including new electrical substations, high-voltage transmission line upgrades, and in many cases entirely new grid segments to deliver the required power reliably. This upstream infrastructure carries its own substantial copper content, and it falls outside the facility construction budget while still drawing on the same constrained supply pool.

When this campus-level multiplier is factored in, the effective copper demand per hyperscale project is meaningfully higher than facility-level estimates alone suggest. This is one reason why regional copper supply bottlenecks can emerge even when global headline figures appear manageable. Consequently, understanding the copper supply crunch becomes essential for anyone planning large-scale AI infrastructure deployment.

The Supply Side: Why the Mining Industry Cannot Respond Quickly

Copper demand from AI infrastructure is growing at a pace measured in quarters. Copper supply, however, responds at a pace measured in decades. This asymmetry is the structural core of the copper-AI supply challenge, and it deserves careful analysis.

New copper mine development from initial discovery to first production typically requires 10 to 20 years, encompassing exploration drilling, resource estimation, feasibility studies, environmental permitting, community consultation processes, financing, and construction. The permitting phase alone routinely extends beyond five years in major producing jurisdictions, including Chile and Peru, which together account for the largest share of global copper reserves and production capacity.

The supply challenge is further compounded by several structural headwinds affecting existing mines:

-

Declining ore grades: The average copper ore grade in Chilean mines has fallen significantly over recent decades as higher-grade surface deposits have been depleted. Miners are processing more rock per tonne of copper produced, increasing both costs and energy intensity.

-

Water scarcity in key producing regions: Chile's Atacama region, which hosts some of the world's most significant copper deposits, faces acute water constraints that limit processing throughput and require expensive desalination infrastructure. Peru faces similar pressures in its high-altitude mining districts.

-

Community and social licence challenges: Indigenous land rights, water access disputes, and environmental concerns have delayed or blocked several significant copper projects across Latin America, introducing a category of risk that geological and financial models historically underweighted.

-

Underinvestment during low-price cycles: Years of suppressed copper prices in the 2010s led to reduced exploration budgets and deferred development decisions, creating a pipeline gap that is now manifesting as constrained supply growth precisely when demand is accelerating.

BHP, one of the world's largest copper producers, has projected that global copper demand will rise 72% by 2050, with AI infrastructure identified as a primary structural driver alongside electric vehicles and renewable energy. The company's long-range analysis suggests data center copper consumption alone could grow six-fold over that period. The future of copper mining will therefore depend heavily on how quickly the industry can respond to these intersecting pressures.

The result is a projected supply deficit that some analysts estimate could reach 6 million tonnes annually by 2035 if demand continues accelerating without a corresponding expansion in mine supply. This figure has significant implications for both commodity pricing and the pace at which AI infrastructure can physically be built.

Where Multiple Demand Vectors Collide

The AI data center buildout does not exist in a commodity vacuum. It is arriving simultaneously with two other major structural copper demand drivers, each of which would be historically significant on its own:

| Demand Driver | Nature of Demand | Copper Intensity |

|---|---|---|

| AI Hyperscale Data Centers | Concentrated, rapid deployment | Up to 50,000 tonnes per facility |

| Electric Vehicles and Grid Storage | Distributed, multi-decade adoption | ~80-100 kg per battery EV vs ~20 kg in ICE vehicle |

| Renewable Energy Infrastructure | Established and expanding | Solar, wind, and grid interconnection |

| Traditional Construction and Industry | Dominant but gradually declining in relative share | Broad-based industrial demand |

The convergence of these demand vectors into a single constrained supply pool, before new large-scale mining capacity can be commissioned, creates conditions for a prolonged supply-demand imbalance. This is not a cyclical tightening of the kind commodity markets have absorbed before. It is a structural realignment driven by simultaneous technology transitions across multiple major economic sectors, all of which have copper as a critical enabling material.

For investors, this multi-vector demand convergence represents one of the more durable commodity theses of the current decade. Unlike demand spikes driven by a single end-use market, the breadth of drivers means demand resilience is maintained even if one sector moderates.

Price Dynamics Across Different Time Horizons

The price implications of AI-driven copper demand unfold differently depending on the timeframe under consideration. In addition, the copper price drivers operating across these different horizons are distinct in character and should be analysed separately.

Near-term (2025 to 2028): The rapid pace of hyperscale construction is creating concentrated procurement demand in specific regional markets. This manifests as spot price volatility and increasing competition among large technology operators for copper delivery commitments, particularly for high-specification cable and conductor products that require longer lead times.

Medium-term (2028 to 2035): As the supply deficit widens and peak AI infrastructure demand coincides with constrained mine supply growth, the conditions for a structural price floor elevation emerge. Copper prices in this window are likely to be supported by fundamental demand rather than speculative positioning. According to S&P Global's research on copper in the age of AI, this medium-term tightening could be more severe than most current market models anticipate.

Long-term (2035 to 2050): Data centers growing to represent approximately 7% of global copper consumption would constitute a permanent demand category of major significance. In combination with the energy transition's copper intensity, this would sustain a premium pricing environment well above the historical averages that informed many existing offtake agreements and mining project economics.

It is important to note that commodity price forecasts carry inherent uncertainty. These projections reflect analyst consensus based on current demand trajectories and should not be treated as guaranteed outcomes. Supply-side responses, technological substitution, and macroeconomic variables could materially alter these dynamics.

The next major ASX story will hit our subscribers first

Strategic Implications Across the Value Chain

For Technology Operators and Infrastructure Developers

Copper procurement strategy is transitioning from a procurement function to a strategic capability. Hyperscale operators who secure long-term supply agreements, develop direct relationships with copper producers, or invest in supply chain visibility are building a competitive advantage that will matter increasingly as the buildout intensifies. The technology companies most exposed to copper supply constraints are those with the most aggressive data center expansion programmes.

For Mining and Metals Investors

The AI infrastructure thesis for copper is structurally distinct from cyclical industrial demand arguments. It is driven by technology adoption timelines that are relatively insensitive to economic cycles, because AI infrastructure investment is now considered mission-critical by the operators deploying it. Furthermore, copper investment strategies that prioritise projects with near-term production potential in stable, well-permitted jurisdictions carry elevated value in this environment. The premium attached to production certainty and jurisdictional reliability has rarely been higher.

For Policymakers

Copper supply security has quietly become a technology infrastructure policy question. The ability of a nation to build and operate AI data centers at competitive scale depends, in part, on reliable access to copper at reasonable cost. This creates alignment between critical minerals policy, energy infrastructure investment, and technology competitiveness strategy that has not historically been recognised in policy frameworks.

Key Takeaways: The Copper-AI Nexus

-

AI hyperscale data centers consume up to 50,000 tonnes of copper per facility, three to ten times the copper content of conventional data centers.

-

Copper demand from AI infrastructure is forecast to peak at approximately 572,000 tonnes in 2028 and average around 400,000 tonnes annually over the following decade.

-

The global copper supply deficit could reach 6 million tonnes by 2035 if AI growth in data centers driving copper demand continues accelerating at current rates without corresponding mine supply growth.

-

BHP projects data center copper consumption will grow six-fold by 2050, elevating the sector from roughly 1% to approximately 7% of global copper use.

-

The simultaneous convergence of AI infrastructure, electric vehicle adoption, and renewable energy buildout creates multi-vector demand pressure on a supply base that responds in decades, not quarters.

-

Copper has transitioned from a predominantly industrial commodity into a critical enabler of the digital and clean energy economy, with pricing and supply security implications that extend well beyond traditional commodity market frameworks.

This article contains forward-looking statements, demand projections, and market forecasts sourced from publicly available industry research. These projections involve assumptions that may not be realised. Nothing in this article constitutes financial or investment advice. Readers should conduct their own due diligence before making any investment decisions.

Want to Position Yourself Ahead of the Next Major Copper Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including copper plays positioned to benefit from the accelerating AI infrastructure buildout — instantly transforming complex geological data into actionable insights for investors of all experience levels. Explore historic examples of exceptional discovery returns and begin your 14-day free trial at Discovery Alert to secure your market-leading advantage before the broader market catches on.