May 24, 2026

What Drives Brazil's Mining Industry Growth in the Current Economic Climate?

Global commodity markets underwent significant restructuring throughout 2025, creating unique opportunities for resource-rich economies positioned to capitalise on shifting demand patterns. Brazil's mining sector exemplified this dynamic, leveraging both traditional bulk commodity strengths and emerging strategic mineral opportunities to achieve substantial revenue expansion. The growth in Brazilian mineral industry reflects broader macroeconomic forces reshaping how extractive industries contribute to national economic performance.

Macroeconomic Foundations Supporting Sectoral Expansion

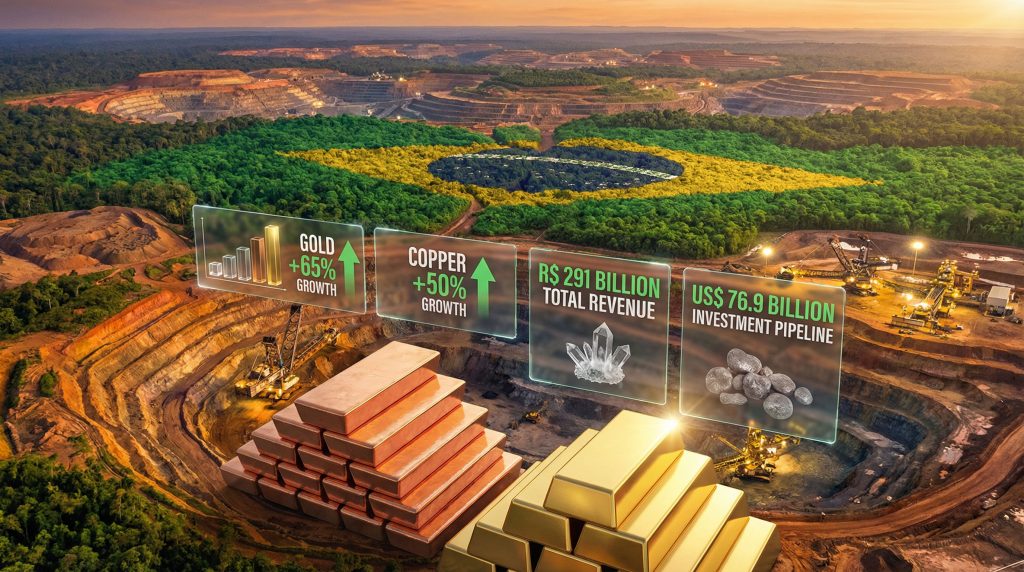

Brazil's mining industry demonstrated remarkable resilience in 2025, generating R$ 298.8 billion in total revenue, representing a robust 10% growth compared to the previous year. This expansion occurred against a backdrop of complex global economic conditions, highlighting the sector's fundamental importance to Brazil's economic stability.

The mining sector's contribution to Brazil's export portfolio reached US$ 35.81 billion in 2025, accounting for approximately 10% of the country's total export revenue of US$ 348.7 billion. This substantial foreign exchange generation provides critical support for Brazil's trade balance and currency stability, particularly during periods of global economic uncertainty.

The sector's performance reflects several underlying macroeconomic advantages. Brazil's established mining infrastructure, developed over decades of resource extraction, enables efficient production scaling without proportional increases in capital expenditure. Additionally, the country's geographic position provides strategic access to both Atlantic and Pacific shipping routes, facilitating cost-effective commodity exports to diverse global markets.

Currency dynamics also played a favourable role in export competitiveness. While specific exchange rate impacts require detailed analysis, the relationship between domestic revenue growth (+10%) and export value performance suggests that Brazilian producers effectively managed currency volatility to maintain market position.

Global Commodity Demand Patterns Reshaping Brazilian Production

Energy transition requirements fundamentally altered global mineral demand structures throughout 2025. Critical minerals essential for renewable energy infrastructure, electric vehicle manufacturing, and grid modernisation created new growth vectors for Brazilian producers specialising in copper, lithium, and related materials.

Traditional bulk commodity markets, particularly iron ore, faced different dynamics. Despite maintaining dominant market positions, iron ore trends demonstrated pricing pressures that required volume optimisation strategies to preserve revenue levels. This divergence between traditional and strategic mineral performance illustrates the ongoing transformation of global commodity demand.

Geopolitical factors further supported Brazilian mineral exports as international buyers sought supply chain diversification away from geographically concentrated sources. Brazil's political stability and established trade relationships positioned the country advantageously for long-term supply contracts across multiple commodity categories.

When big ASX news breaks, our subscribers know first

How Are Regional Mining Hubs Contributing to National Growth Patterns?

Brazil's mining industry exhibits pronounced regional concentration, with three states accounting for the overwhelming majority of national production value. This geographic clustering reflects both geological endowment and historical infrastructure development patterns that continue to shape industry expansion.

Minas Gerais Economic Dominance Analysis

Minas Gerais maintained its position as Brazil's mining powerhouse, generating R$ 119 billion in revenue during 2025, representing 40% of the nation's total mineral industry output. This concentration reflects the state's exceptional geological diversity, encompassing iron ore deposits, gold reserves, and various industrial minerals.

The state's infrastructure advantages compound its natural resource endowment. Decades of mining development created integrated transportation networks, specialised labour forces, and supporting service industries that reduce operational costs for mining companies. Furthermore, rail connections to major ports, established power generation capacity, and proximity to steel production facilities create operational synergies unavailable in less developed mining regions.

| Regional Contribution | 2025 Revenue | National Share |

|---|---|---|

| Minas Gerais | R$ 119 billion | 40% |

| Pará | R$ 103 billion | 34% |

| Bahia | R$ 13 billion | 4% |

| Other States | R$ 63.8 billion | 22% |

Employment concentration in Minas Gerais creates significant economic multiplier effects. Mining operations require extensive supply chains, from specialised equipment manufacturers to environmental consulting services, generating indirect employment opportunities across multiple sectors. Consequently, municipal governments in mining regions benefit substantially from increased tax revenues, enabling infrastructure improvements and public service expansion.

Pará's Strategic Position in Northern Development

Pará contributed R$ 103 billion to Brazil's mineral revenue in 2025, representing 34% of national output. This substantial contribution positions Pará as the second-largest mining hub, with distinct advantages in logistics and resource accessibility.

The state's geographic position provides strategic access to international shipping routes through the Amazon River system and Atlantic ports. Moreover, large-scale mining operations, particularly those focused on iron ore and bauxite, benefit from established export infrastructure capable of handling substantial cargo volumes efficiently.

Pará's mining development intersects with complex environmental and social considerations. The state contains significant indigenous territories and protected environmental areas, requiring sophisticated stakeholder engagement and environmental management protocols. However, successfully balancing resource extraction with environmental protection and indigenous rights represents both a challenge and an opportunity for sustainable mining expansion.

The region's development trajectory depends heavily on continued infrastructure investment. Transportation corridor improvements, port facility expansion, and power generation capacity additions enable production scaling while maintaining competitive operational costs.

Emerging Regional Players and Market Diversification

Bahia's mining sector contributed R$ 13 billion in 2025, representing 4% of national output. While significantly smaller than Minas Gerais and Pará, Bahia demonstrates the potential for geographic diversification within Brazil's mining industry.

Regional specialisation patterns are emerging as different states focus on their comparative geological advantages. For instance, Bahia's mineral portfolio includes copper, gold, and various industrial minerals, providing diversification benefits during periods of commodity price volatility.

Secondary mining states collectively contributed approximately R$ 63.8 billion (22% of national output), indicating substantial mining activity beyond the three primary producing regions. This geographic distribution reduces concentration risks and provides opportunities for balanced national development.

Which Commodity Categories Are Driving Revenue Growth?

Commodity performance diverged significantly throughout 2025, with traditional bulk commodities facing pricing pressures while strategic minerals experienced exceptional growth. This performance variation reflects fundamental shifts in global demand patterns and provides insights into future industry trajectories.

Iron Ore Market Leadership Despite Price Pressures

Iron ore maintained its position as Brazil's leading mineral commodity, generating R$ 152.2 billion in revenue during 2025. However, this leadership came with challenges, as revenue declined 2.2% compared to 2024 despite increased production volumes.

The commodity's export performance illustrates the complexity of global iron ore markets. Brazilian iron ore exports reached 416 million tonnes in 2025, representing a 7% increase in physical volume, while export values totalled US$ 28.9 billion, declining 3% from the previous year. This divergence indicates an estimated 8.6% reduction in average international pricing.

| Iron Ore Metrics | 2025 Performance | Year-over-Year Change |

|---|---|---|

| Revenue (R$ billion) | 152.2 | -2.2% |

| Export Volume (million tonnes) | 416 | +7% |

| Export Value (US$ billion) | 28.9 | -3% |

| Implied Price Impact | N/A | -8.6% |

This price-volume relationship reflects producer strategies during challenging market conditions. Companies increased production volumes to maintain revenue levels and cover fixed operational costs, even as international prices declined. This approach demonstrates the industry's operational flexibility and commitment to market share preservation.

Iron ore's cyclical nature remains tied to global steel demand, particularly from major consuming countries. Production cost advantages in Brazilian operations, including high-grade ore quality and established infrastructure, provide competitive advantages during pricing downturns.

Gold and Copper: The New Growth Champions

Strategic minerals experienced remarkable growth throughout 2025, with gold and copper leading sectoral expansion through distinct demand drivers.

Gold revenue reached R$ 39 billion in 2025, representing exceptional 65% growth compared to 2024. This performance reflects multiple market forces converging to support gold demand. Furthermore, global economic uncertainty drove safe-haven asset demand, while central bank purchasing patterns provided institutional support for the gold price forecast trends.

Economic consultant Luciana Mourão from AMIG Brasil emphasised gold's strategic importance during uncertain market conditions, noting that the precious metal tends to consolidate as a protection asset during periods of global market volatility. This fundamental demand characteristic provides structural support for sustained gold production expansion.

Copper achieved R$ 30 billion in revenue during 2025, representing remarkable 50% growth year-over-year. The commodity's performance reflects long-term structural demand tied to energy transition requirements. Copper's essential role in electrification infrastructure, from renewable energy installations to electric vehicle manufacturing, creates sustained demand growth independent of traditional economic cycles.

Salobo Metals S.A., Vale's subsidiary responsible for Brazil's largest copper deposit, contributed 7% of the entire mining sector's revenue from copper production alone. This concentration demonstrates both the scale of major copper operations and the potential for continued expansion as demand fundamentals strengthen.

Mourão highlighted copper's strategic character in the energy transition, noting its essential role in electrification, electric vehicle production, cable manufacturing, and technological equipment. This broad-based demand provides multiple growth vectors for Brazilian copper producers.

The performance divergence between gold (+65%) and copper (+50%) reflects different demand drivers: gold responding to macroeconomic uncertainty and monetary policy, while copper benefits from infrastructure investment and technological transformation trends.

What Investment Patterns Indicate Future Growth Potential?

Investment allocation patterns across Brazil's mining sector provide critical insights into future growth trajectories and strategic priorities. Capital deployment decisions reflect both immediate operational requirements and long-term market positioning strategies.

Capital Allocation Trends Across Mining Segments

Mining companies demonstrated increased investment focus on strategic minerals and critical materials throughout 2025. This reallocation reflects anticipated demand growth for commodities essential to energy transition and technological advancement, aligning with the broader critical minerals strategy emerging globally.

Foreign direct investment patterns indicate international confidence in Brazil's mining potential. Moreover, major multinational corporations continued expanding operations, while domestic companies pursued partnerships to access advanced technologies and global distribution networks.

The relationship between investment and production capacity suggests that sustained capital deployment will be necessary to meet growing international demand, particularly for strategic minerals. However, infrastructure bottlenecks in some regions require coordinated investment between private companies and government agencies to enable efficient production scaling.

Technology and Sustainability Investment Drivers

Operational efficiency improvements through technology adoption represent a significant investment category across Brazilian mining operations. The mining technology advances encompass automation systems, digital monitoring platforms, and data analytics tools that enable production optimisation while reducing operational costs.

Environmental compliance requirements drive substantial capital allocation toward sustainable mining practices. Water management systems, tailings safety improvements, and carbon emission reduction initiatives require ongoing investment to meet regulatory standards and international sustainability expectations.

Companies increasingly integrate Environmental, Social, and Governance (ESG) considerations into capital allocation decisions. This approach reflects both regulatory requirements and market expectations from international investors and customers prioritising sustainable supply chains.

How Does Employment Growth Reflect Industry Expansion?

Employment trends provide reliable indicators of mining industry expansion and regional economic development. Job creation patterns reflect both direct operational requirements and broader economic multiplier effects throughout mining regions.

Direct Employment Creation Metrics

Brazil's mining sector created 9,554 formal employment positions during 2025, bringing total formal sector employment to 291,000 positions by year-end. This job creation occurred despite commodity price volatility, indicating sustained operational expansion across mining companies.

The diversity of mining operations contributes to employment distribution patterns. Approximately 8,000 mining entrepreneurs paid Compensation for Mineral Extraction (CFEM) during 2025, demonstrating a market structure encompassing both large multinational operations and smaller independent producers.

Formal sector employment data from Novo Caged (Brazil's employment registration system) provides reliable tracking of documented positions with labour protections and benefits. This distinction between formal and informal employment ensures accurate assessment of industry job quality and worker protection levels.

Employment growth patterns correlate with regional production concentration. Consequently, Minas Gerais, Pará, and Bahia likely account for the majority of new job creation, reflecting their dominant positions in national mineral production.

Skills requirements in modern mining operations increasingly emphasise technical expertise, safety protocols, and environmental management capabilities. This evolution creates opportunities for workforce development programmes and specialised training initiatives.

Indirect Economic Multiplier Effects

Mining employment generates substantial indirect job creation throughout regional economies. Supply chain requirements, from specialised equipment maintenance to environmental consulting services, create employment opportunities beyond direct mining operations.

Service sector development in mining regions reflects increased local economic activity. For instance, transportation services, hospitality businesses, and retail establishments benefit from the presence of well-compensated mining workforces.

Long-term demographic impacts include population stabilisation in historically rural regions and infrastructure development supporting community growth. Educational facilities, healthcare services, and municipal infrastructure improvements often accompany major mining developments.

The economic multiplier effect varies by mining operation type and regional characteristics. Large-scale operations typically generate greater indirect employment per direct position, while smaller operations may provide more localised economic benefits.

What Role Does Export Performance Play in Growth Sustainability?

Export performance represents a critical component of Brazil's mining sector sustainability, providing foreign exchange earnings and supporting national trade balance objectives. International market positioning determines long-term growth potential and economic stability.

Trade Balance Contribution Analysis

Brazil's mineral exports (excluding petroleum) totalled US$ 35.81 billion in 2025, representing approximately 10% of the country's total export revenue of US$ 348.7 billion. This substantial contribution demonstrates mining's strategic importance to national foreign exchange generation.

The extractive industry, including petroleum and gas, accounted for 23.7% of total Brazilian exports (US$ 80.4 billion). When petroleum is excluded, mineral exports still represent a significant portion of national export performance, highlighting the sector's fundamental importance to trade balance sustainability.

Iron ore exports dominated mineral trade performance, generating US$ 28.9 billion from 416 million tonnes of exports. The 7% increase in export volumes despite 3% decline in export values demonstrates Brazilian producers' commitment to market share maintenance during challenging pricing conditions.

Trade surplus generation from mineral exports supports Brazilian currency stability and provides foreign exchange reserves for national economic management. This contribution becomes particularly valuable during periods of global economic uncertainty or commodity price volatility.

International Market Positioning Strategies

Brazilian mining companies increasingly pursue market diversification strategies to reduce dependency on single geographic regions or customer concentrations. This approach provides stability during regional economic downturns or geopolitical disruptions.

Asian markets represent critical growth opportunities for Brazilian mineral exports, particularly as infrastructure development and manufacturing expansion continue across emerging economies. Furthermore, long-term supply relationships with major consumers provide revenue predictability and operational planning advantages.

European Union critical mineral requirements create opportunities for Brazilian producers specialising in strategic materials essential to renewable energy and automotive electrification. These partnerships often involve premium pricing for reliable, sustainably produced commodities.

Infrastructure investment requirements for export capacity expansion include port facility improvements, transportation network development, and logistics optimisation. Coordinated public and private investment enables efficient commodity movement from production sites to international markets.

The next major ASX story will hit our subscribers first

Which Regulatory and Policy Factors Shape Growth Trajectories?

Regulatory frameworks and policy environments significantly influence mining sector growth patterns and investment decisions. Understanding these factors provides insights into future development trajectories and potential challenges.

CFEM Revenue Distribution and Municipal Development

Brazil's mining sector generated R$ 7.9 billion in Compensation for Mineral Extraction (CFEM) payments during 2025, distributed across 2,840 municipalities nationwide. This revenue distribution mechanism ensures that local communities benefit directly from mineral extraction activities.

CFEM represents a percentage-based royalty system that scales with mining production and commodity prices. Higher commodity values and increased production volumes automatically generate greater compensation for affected municipalities, creating alignment between mining success and local community benefits.

Municipal governments utilise CFEM revenues for infrastructure development, education programmes, healthcare facilities, and environmental projects. This funding mechanism enables mining regions to address population growth and infrastructure demands associated with mining development.

Revenue transparency and accountability measures ensure effective utilisation of CFEM funds for community development. Regular reporting requirements and public disclosure mechanisms enable citizens and oversight agencies to monitor fund allocation and project outcomes.

The geographic distribution of CFEM payments reflects mining activity concentration patterns. Consequently, municipalities in Minas Gerais, Pará, and Bahia likely receive the largest individual payments, while smaller mining operations contribute to a broader distribution network.

Environmental and Social Governance Evolution

Environmental licensing processes continue evolving to balance development objectives with environmental protection requirements. Streamlined procedures for low-impact operations, combined with enhanced scrutiny for major projects, create predictable regulatory frameworks.

Indigenous community consultation protocols ensure that traditional territories receive appropriate consideration during mining development planning. These requirements often result in benefit-sharing agreements and employment opportunities for indigenous communities, as highlighted in recent Brazilian mining industry research.

Tailings safety regulations implemented following historical incidents require ongoing compliance investments and operational modifications. Enhanced monitoring systems, improved dam design standards, and emergency response protocols represent mandatory safety improvements.

Climate change adaptation strategies become increasingly important for mining operations exposed to weather-related risks. Water management systems, extreme weather preparedness, and carbon emission reduction commitments influence operational planning and capital allocation.

What Strategic Scenarios Could Impact Future Growth?

Forward-looking analysis requires consideration of multiple potential scenarios that could significantly influence Brazil's mining sector development. These scenarios help stakeholders prepare for various market conditions and policy environments.

Optimistic Growth Scenario (2026-2030)

Sustained commodity demand growth, particularly for strategic minerals, could drive exceptional sectoral expansion. Energy transition acceleration, infrastructure investment programmes, and technological advancement requirements would support premium pricing for critical materials within the broader mining industry evolution.

Infrastructure investment acceleration, including transportation network improvements and port facility expansion, could enable significant production scaling without proportional cost increases. Coordinated public and private investment might resolve current bottlenecks limiting efficient market access.

Technology adoption across mining operations could reduce production costs by 20-25%, improving competitive positioning and profit margins. Automation systems, predictive maintenance programmes, and operational optimisation tools would enhance productivity while reducing environmental impacts.

Export market diversification could reduce volatility exposure while capturing premium pricing opportunities in specialised market segments. Furthermore, long-term supply agreements with technology manufacturers and renewable energy companies would provide revenue predictability.

Conservative Growth Scenario Considerations

Global economic deceleration could reduce commodity demand across multiple categories, particularly those tied to infrastructure development and manufacturing expansion. Trade tensions or geopolitical disruptions might affect export market access and pricing stability.

Environmental regulatory tightening could increase compliance costs and development timelines for new mining projects. Enhanced environmental protection requirements, while beneficial for long-term sustainability, might impact short-term profitability and expansion plans.

Infrastructure development delays could limit production expansion capabilities in key mining regions. Transportation bottlenecks, port capacity constraints, and power generation limitations might prevent efficient scaling of mining operations.

Currency appreciation could reduce export competitiveness for Brazilian mineral products in international markets. Strong domestic economic performance, while positive overall, might create challenges for export-dependent mining operations.

Risk Mitigation Strategies for Sustained Growth

Portfolio diversification across commodity categories reduces exposure to single-commodity price volatility. Companies maintaining production capabilities across bulk commodities and strategic minerals achieve greater revenue stability during market cycles.

Vertical integration opportunities in processing and refining enable value capture beyond raw material extraction. Downstream development creates domestic job opportunities while reducing dependency on international commodity price fluctuations.

Strategic partnerships with international technology companies, infrastructure developers, and end-user manufacturers provide market access and technical expertise. These relationships often include long-term supply commitments and premium pricing arrangements.

Technology investment for operational efficiency improvements enables cost reduction and productivity enhancement independent of commodity price performance. Digital systems, automation platforms, and data analytics tools provide sustainable competitive advantages.

The growth in Brazilian mineral industry demonstrates remarkable resilience and strategic positioning for future expansion. Through effective resource utilisation, technological advancement, and strategic market positioning, Brazil's mining sector continues establishing itself as a critical component of global commodity supply chains while supporting domestic economic development objectives.

Disclaimer: This analysis contains forward-looking projections and market assessments that involve inherent uncertainties. Commodity markets, regulatory environments, and economic conditions may differ significantly from scenarios presented. Readers should consult multiple sources and consider professional advice for investment or business decisions related to Brazil's mining sector.

Ready to Capitalise on the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers instant alerts on significant ASX mineral discoveries, helping investors identify actionable opportunities ahead of the broader market. See how historic discoveries can generate substantial returns and begin your 14-day free trial today to position yourself ahead of market movements.