May 24, 2026

China pulls silver from global markets at unprecedented volumes, fundamentally reshaping precious metals dynamics through sustained industrial demand and retail investment convergence. The nation's extraordinary consumption of 790 tons during the first two months of 2026 demonstrates how policy deadlines intersect with investment psychology to create structural market shifts.

Furthermore, this silver market squeeze reflects deeper changes in global supply chains and regional pricing mechanisms. Understanding these macro forces requires examining how industrial policy deadlines interact with retail investor psychology, particularly when established price relationships between precious metals create substitution effects.

China's Strategic Position in Global Silver Markets

China pulls silver from global markets at volumes that demonstrate the nation's dominance in precious metals consumption. The country has established itself as the world's primary silver consumer, with import volumes reaching over 790 tons in just the first two months of 2026. This consumption represents a convergence of industrial manufacturing requirements and retail investment demand operating simultaneously.

The scale of Chinese silver consumption reflects deeper structural changes in both manufacturing capacity and investment behaviour patterns. January 2026 imports totalled 320 tons, followed by February's record-breaking 470 tons – the highest monthly import volume ever recorded for that specific month according to Chinese customs data.

These figures establish 2026 as reaching eight-year highs for two-month import periods. Market analysts note that declining inventories on Chinese exchanges create psychological effects that amplify perceived scarcity beyond actual supply constraints.

Exchange stockpiles have fallen consistently, contributing to market psychology that sustains import demand even as global supply conditions fluctuate. The consumption pattern distinguishes itself from previous demand cycles through its dual-driver mechanism.

Historical Context and Market Positioning

Chinese silver imports during early 2026 represent a significant departure from traditional seasonal patterns and multi-year averages. The 790-ton two-month total establishes China's position not merely as a large consumer, but as a market force capable of redirecting global supply flows.

This consumption capacity reflects China's industrial infrastructure concentration, particularly in solar manufacturing, where domestic production facilities process the majority of global solar panel manufacturing. Additionally, the gold-silver ratio analysis reveals how pricing relationships influence investor behaviour.

Exchange inventory depletion across Shanghai markets creates visible scarcity indicators that influence trader behaviour and pricing decisions. When combined with retail investment demand growth, these factors establish China as a price-setting market rather than a price-taking participant.

When big ASX news breaks, our subscribers know first

Analyzing the 790-Ton Import Surge Impact

The sheer volume of 790 tons over two months requires contextualising against global silver production and trade flows. This import volume represents a significant percentage of annual global mine production, concentrated into an abbreviated timeframe that strains existing logistics and financing infrastructure.

February's 470-ton record followed January's already substantial 320-ton figure, suggesting accelerating import velocity rather than steady monthly consumption. The progression indicates demand intensification driven by deadline-sensitive factors rather than gradual consumption growth.

Price volatility accompanied these import volumes, with silver prices surging approximately 70% in early 2026 before surrendering gains by late January. The rapid price correction following speculative buying waves demonstrates how quickly sentiment can shift in precious metals markets.

However, physical import demand sustained despite price volatility. Current market prices reflect this demand intensity, with silver trading near $69-70 per troy ounce as of March 2026, representing significant appreciation from historical averages.

Import Volume Breakdown Analysis

| Month | Import Volume | Percentage of Total | Market Context |

|---|---|---|---|

| January 2026 | 320 tons | 40.5% | Initial surge building |

| February 2026 | 470 tons | 59.5% | Record monthly high |

| Total | 790 tons | 100% | Eight-year high period |

The pricing level creates affordability constraints for some market participants while simultaneously attracting speculative interest from traders seeking volatility opportunities. Consequently, the import surge creates ripple effects throughout global supply chains, affecting everything from refinery processing schedules to transportation logistics.

Physical delivery requirements for 790 tons necessitate substantial coordination across multiple jurisdictions and regulatory frameworks. This coordinated effort highlights the complexity of modern precious metals markets.

Industrial Manufacturing vs. Investment Demand Dynamics

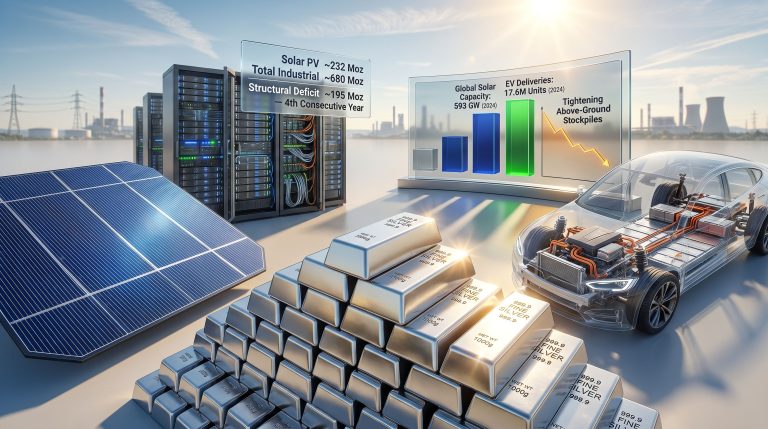

Two distinct consumption channels drive china pulls silver from global markets, each operating under different economic incentives and timeline pressures. The solar manufacturing sector consumes approximately 20% of annual global silver supply, with Chinese facilities representing the overwhelming majority of this industrial consumption.

Export tax rebate removal deadline of April 1, 2026 creates artificial urgency for solar manufacturers to accelerate production and secure silver supplies before policy changes affect export economics. This front-loading behaviour concentrates normal annual consumption into compressed timeframes, distorting typical seasonal demand patterns.

Manufacturing acceleration driven by rebate deadline approaches creates temporary demand spikes that exceed underlying consumption requirements. Solar panel production lines operate at maximum capacity to maximise output before tax policy changes affect export profitability calculations.

Meanwhile, the broader gold market analysis reveals how precious metals pricing affects industrial consumption patterns across different sectors.

Retail Investment Substitution Effects

Simultaneously, retail investment demand emerges from gold price accessibility challenges as gold trades around $5,000 per troy ounce compared to silver's $70 level. This pricing differential creates a gold-to-silver ratio of approximately 71:1, making silver relatively attractive for retail investors seeking precious metals exposure.

Physical investment bars ranging from 20 grams to 1 kilogram have become common products in Shenzhen's Shuibei market, the centre of China's retail bullion trade. Consumer psychology increasingly views gold as inaccessible, creating substitution demand that redirects retail precious metals investment toward silver.

Dealer inventory expansion demonstrates this shift, with Shuibei market stockpiles tripling to approximately 300 tons in recent months. This inventory accumulation reflects both increased retail demand and dealers' financial preference for silver's lower absolute price per unit.

For instance, this preference reduces financing requirements compared to gold inventory. Market researchers identify a fundamental shift in retail investor psychology, where consumers increasingly perceive gold as inaccessible due to price levels.

"Silver has become a functionally substitutable precious metals investment vehicle as gold pricing pushes beyond retail accessibility thresholds," according to market analysts studying consumer behaviour patterns.

Manufacturing Timeline Pressures

The April 1 rebate deadline creates measurable urgency for solar manufacturers to secure silver supplies and complete production runs before export tax advantages disappear. This policy timeline compression explains why import volumes accelerated from January's 320 tons to February's 470-ton record.

Solar industry front-loading strategies involve securing months of raw material supplies in advance of production deadlines. Silver's role in solar cell manufacturing makes it a critical input that cannot be substituted, creating inelastic demand during policy transition periods.

Manufacturing capacity utilisation rates approach maximum levels as facilities attempt to complete production runs before rebate removal. This operational intensity explains sustained silver consumption despite price volatility that might otherwise moderate demand.

Hong Kong's Role as Precious Metals Gateway

Hong Kong serves as the critical arbitrage gateway enabling profitable silver flows from London markets to Chinese consumers. The territory's traditional role as a precious metals trading hub has evolved into a congestion point where demand exceeds available pipeline capacity.

Premium structures have inverted traditional relationships, with Hong Kong silver bars commanding premiums of up to $8 per troy ounce above London benchmark prices. This represents a structural reversal from historical patterns where Hong Kong typically traded at discounts to London markets.

Large silver bars traded by banks specifically attract these premium prices, distinguishing institutional trading channels from smaller retail investment bars flowing through different distribution networks. The premium structure compensates traders for logistics costs, financing expenses, and scarcity value during high-demand periods.

Furthermore, understanding these market dynamics becomes easier with access to comprehensive exchange traded commodities guide resources that explain trading mechanisms.

Arbitrage Opportunity Mechanics

Profitable arbitrage opportunities emerge when Hong Kong premiums exceed the total costs of transportation, insurance, financing, and handling required to redirect silver from London to Chinese markets. The $8 per ounce premium provides sufficient economic incentive to justify complex logistics and regulatory compliance requirements.

Physical delivery logistics infrastructure requires coordination across multiple jurisdictions, banking relationships, and transportation systems. Hong Kong's established precious metals trading infrastructure facilitates these complex transactions during periods of intense demand.

Premium softening indicators suggest market dynamics may be normalising as solar demand moderates approaching the April rebate deadline. However, underlying investment demand may sustain arbitrage opportunities even as industrial consumption patterns shift.

Traditional Discount-to-Premium Reversal

The structural shift from traditional Hong Kong discounts to substantial premiums reflects fundamental changes in global silver supply and demand relationships. Historical discount patterns typically reflected Hong Kong's role as a redistribution hub rather than a final consumption destination.

Current premium levels indicate Hong Kong has evolved into a supply constraint bottleneck where available silver quantities cannot satisfy Chinese demand at traditional pricing relationships. This transformation demonstrates how regional demand intensity can overwhelm established trading patterns.

Banking product specifications for large silver bars involve standardised weights, purity requirements, and certification standards that distinguish institutional trading from retail investment products. These specifications ensure fungibility across global trading networks while maintaining quality standards.

Global Supply Response and Market Rebalancing

London markets demonstrate remarkable resilience despite Chinese demand pressure, supported by record silver inflows following historic squeeze conditions in previous years. These inflows provide the physical metal necessary to satisfy arbitrage demand without disrupting core London trading operations.

Exchange-traded fund (ETF) liquidations have released more than 1,900 tons of silver in 2026, freeing previously held metal for physical market absorption. These institutional selling flows offset Chinese import demand at the global level, preventing widespread supply disruptions.

Borrowing cost normalisation reflects improved supply availability, with silver lease rates moderating from extreme levels experienced during previous squeeze periods. Nevertheless, longer-dated leases remain expensive due to market volatility and precautionary positioning against future supply constraints.

According to Bloomberg's analysis, this demand surge represents a fundamental shift in global precious metals trading patterns that could persist beyond immediate policy deadlines.

Exchange Inventory Analysis

Visible inventories across major global exchanges continue declining or remain well below long-term averages, suggesting underlying tightness persists despite improved London supply conditions. Exchange stockpiles from New York to Shanghai reflect ongoing consumption that exceeds new supply additions.

Shanghai Futures Exchange inventory depletion creates psychological effects that influence trader behaviour and pricing decisions. When market participants observe declining visible inventories, they adjust their positioning and risk management strategies accordingly.

Global exchange inventory comparison reveals regional disparities in available stockpiles, with some markets experiencing more acute shortages than others. These disparities create arbitrage opportunities and explain premium variations across different trading centres.

Supply Chain Rebalancing Indicators

London inflow records demonstrate how global supply chains adapt to regional demand imbalances through price incentives and logistics coordination. Record inflows provide the physical foundation necessary to maintain market stability during demand surges.

ETF liquidation trends reflect institutional investor repositioning as market conditions evolve. When ETF holdings decline by substantial volumes, the released metal becomes available for physical delivery to end users.

Market maker liquidity provision faces challenges during volatile periods, requiring careful risk management and financing coordination. Professional trading firms must balance profit opportunities against potential supply disruptions.

Investment Strategy and Market Psychology Considerations

Retail investor behaviour patterns demonstrate preference for following rising price trends rather than purchasing during market declines. This momentum-based psychology sustains demand even after speculative buying waves subside, creating persistent upward pressure on imports.

Gold-to-silver ratio investment decisions influence asset allocation choices as the 71:1 ratio makes silver appear relatively attractive compared to historical relationships. Investors seeking precious metals exposure calculate per-ounce affordability differences when making purchase decisions.

Financing and storage considerations affect dealer inventory strategies and retail investor participation. Silver's lower per-unit cost reduces financing pressure on dealers while requiring more physical storage space compared to equivalent gold values.

Additionally, investors interested in precious metals fundamentals can benefit from gold safe-haven insights that provide broader context for portfolio allocation decisions.

Market Timing and Cyclical Analysis

Speculative vs. fundamental demand differentiation requires analysing whether import surges reflect temporary trading activity or sustained consumption changes. The combination of industrial deadline pressures and investment substitution suggests both factors operate simultaneously.

Seasonal demand fluctuations typically follow predictable patterns, but policy deadlines and investment trends can override seasonal factors. The April rebate deadline creates artificial seasonality that may not repeat in subsequent years.

Risk management considerations involve assessing whether current demand levels represent sustainable trends or temporary dislocations. Investors must evaluate both upside potential and downside risks in volatile precious metals environments.

Investment Psychology Factors

Momentum-based trading behaviour contributes to sustained demand as retail investors tend to purchase during rising price environments rather than seeking value during declines. This psychological pattern extends demand cycles beyond fundamental drivers.

Accessibility perception changes regarding gold create substitution effects that redirect investment flows toward silver. Consumer psychology increasingly views gold as beyond reach, making silver an acceptable alternative for precious metals portfolio allocation.

Dealer financing preferences for silver inventory reflect practical economic considerations about working capital requirements and storage costs. These operational factors influence market structure and product availability.

The next major ASX story will hit our subscribers first

Future Market Trajectory and Structural Changes

Demand sustainability assessment requires evaluating whether current consumption levels reflect permanent structural changes or temporary policy-driven acceleration. The convergence of industrial deadline pressures with investment substitution effects creates complex forecasting challenges.

Solar industry growth trajectory will continue influencing silver consumption as manufacturing capacity expands globally. However, the concentration of production facilities in China means domestic consumption patterns significantly impact global silver markets.

Chinese economic policy influence extends beyond specific rebate deadlines to broader industrial development strategies and currency management decisions. Policy makers' approaches to export competitiveness and domestic consumption affect silver import requirements.

Market observers note through recent research that these developments may establish new baseline consumption levels that persist beyond immediate policy catalysts.

Supply Response Development

Mining production capacity constraints limit how quickly global supply can respond to sustained demand increases. Silver mining operations require substantial lead times to develop new capacity, creating supply inelasticity during demand surges.

Recycling and secondary supply potential offers some capacity expansion, but recycled silver requires collection, processing, and refinement infrastructure that takes time to develop. Secondary supply provides more flexibility than primary mining but faces its own limitations.

Strategic reserve policy implications may emerge if governments view silver supply security as strategically important. Industrial applications in renewable energy and electronics create national security considerations that could influence policy responses.

Long-term Market Structure Evolution

Regional premium normalisation depends on whether Chinese demand moderates or remains elevated beyond immediate policy deadlines. Sustained high consumption could establish permanently higher regional pricing structures.

Global trading hub rebalancing may occur as market participants adapt to changed demand patterns and supply flows. Hong Kong's evolution from discount hub to premium market demonstrates how regional roles can shift during structural changes.

Investment product innovation could emerge to address accessibility concerns and financing challenges associated with physical precious metals ownership. Market participants may develop new products to serve evolving investor preferences and operational requirements.

Disclaimer: This analysis contains forward-looking statements and market assessments that involve uncertainties and assumptions. Precious metals markets exhibit significant volatility, and actual outcomes may differ substantially from projections. Investors should conduct their own due diligence and consider consulting financial advisors before making investment decisions. Past performance does not guarantee future results, and commodity investments carry inherent risks including price volatility, storage costs, and market liquidity considerations.

Looking to Capitalise on Precious Metals Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant precious metals discoveries across the ASX, transforming complex mineral data into actionable trading opportunities ahead of market movements. Understanding the investment potential of historic discoveries becomes clearer by exploring Discovery Alert's dedicated discoveries page, which showcases exceptional returns from major finds, whilst beginning your 14-day free trial today positions you to identify the next breakthrough before the broader market responds.