June 9, 2026

The Hidden Mineral Wealth Sitting Inside Oil and Gas Wastewater

Every day, the global oil and gas industry generates a staggering volume of water it never wanted. Pulled to the surface alongside crude oil and natural gas, this produced water carries dissolved salts, trace metals, and in certain formations, meaningful concentrations of lithium. For decades, operators have treated this fluid as a costly disposal problem. That framing is changing rapidly, and the shift carries significant implications for how the world intends to supply the battery metals underpinning the energy transition.

Direct lithium extraction from wastewater sits at the intersection of two urgent industrial imperatives: managing the environmental burden of oilfield water production and closing a widening gap between lithium supply and the voracious appetite of the global battery industry. Understanding why this technology is gaining serious commercial traction requires looking first at the demand-side pressure that is making unconventional lithium sources increasingly attractive to investors and energy majors alike.

When big ASX news breaks, our subscribers know first

Why the Conventional Lithium Supply Chain Is Running Out of Time

Lithium demand is on course to roughly quadruple by 2035, driven by electric vehicle penetration, grid-scale battery storage, and the broader electrification of industrial processes. The arithmetic is unforgiving. A single gigafactory-scale battery plant can consume tens of thousands of tonnes of lithium carbonate equivalent annually, and dozens of such facilities are either under construction or in advanced planning globally.

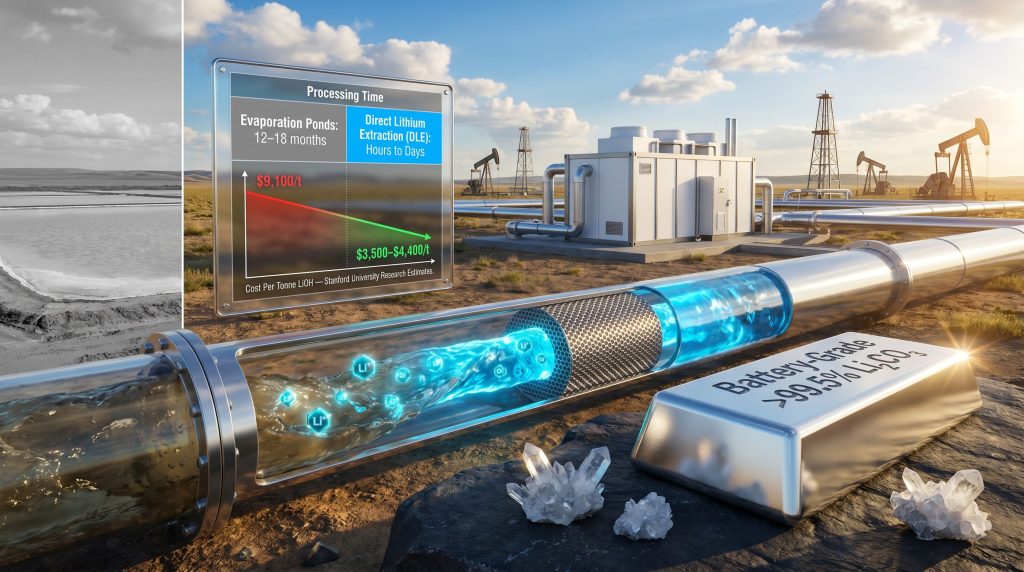

The supply-side response has been structurally inadequate. Hard rock lithium mines, which extract spodumene from pegmatite deposits, require five to ten years from discovery to first production under favourable conditions. Furthermore, conventional salar brine operations in South America's Lithium Triangle face water-rights disputes, indigenous consultation requirements, and the fundamental constraint that solar evaporation ponds need between twelve and eighteen months to concentrate lithium to recoverable grades. Neither pathway can be meaningfully accelerated to meet near-term shortfalls. The global lithium market outlook makes this structural inadequacy increasingly difficult to ignore.

This is the strategic logic that makes produced water compelling. The feedstock already exists. The water is already being lifted. The infrastructure to aggregate it is already in place. The question is purely whether the lithium concentration within that water is sufficient to justify extraction, and whether the technology can deliver battery-grade output at commercially viable cost.

What Direct Lithium Extraction from Wastewater Actually Involves

Direct lithium extraction from wastewater refers to a family of technologies that isolate dissolved lithium ions from saline industrial fluids, principally oilfield produced water and geothermal brines, without relying on the slow, land-intensive process of solar evaporation. The defining characteristic of DLE is selectivity: the ability to target lithium specifically from a complex solution containing sodium, calcium, magnesium, potassium, and a range of other dissolved species.

Produced water arrives at surface separation facilities already mixed with hydrocarbons and suspended solids. Before any lithium recovery can occur, the fluid must be pre-treated to remove oil residues, particulates, and competing ions that would foul downstream extraction equipment. This pre-treatment step is often underappreciated in commercial assessments but represents a meaningful portion of both capital and operating expenditure.

The Critical Concentration Threshold

Not every produced water stream is a viable lithium feedstock. Commercial feasibility for direct lithium extraction from wastewater generally requires dissolved lithium concentrations of at least 50 mg/L. Below this threshold, the volume of fluid that must be processed per tonne of recovered lithium increases to a point where energy and capital costs make the operation economically marginal. This concentration floor means that brine characterisation and formation-level geochemical mapping are critical activities before any capital commitment is made.

The variability of lithium concentration across formations, and even across different wells within the same formation, is one of the most underappreciated technical challenges in the sector. Unlike a hard rock deposit where grade can be defined by drilling and assaying, a brine resource requires ongoing monitoring of fluid chemistry because concentrations can change over the production life of a field. These lithium supply challenges are compounded by the inherent inconsistency of produced water as a feedstock.

The Four Primary Extraction Technologies: How They Differ

The DLE technology landscape is not monolithic. Four distinct approaches are at various stages of commercial maturity, each with different performance profiles, cost structures, and suitability for different brine chemistries.

Ion Adsorption: The Current Commercial Leader

Ion adsorption is presently the most commercially deployed DLE method. The process works by passing brine over selective solid sorbents, typically materials based on aluminium, magnesium, or resin substrates, that physically bind lithium ions from solution. Once the sorbent material reaches its loading capacity, fresh water or a mild acidic solution is introduced to desorb the concentrated lithium, which is then collected for downstream refining. The sorbent is regenerated and the cycle repeats.

The first commercial lithium extraction plant in the United States, operated by Element3 in the Permian Basin and commissioned in February 2026, uses ion adsorption. A second facility operated by Gradiant in the Marcellus Shale region is anticipated to begin operations later in 2026. For a detailed overview of the fundamentals behind these approaches, the DLE fundamentals guide provides a useful technical grounding.

Solvent Extraction: Liquid-to-Liquid Selectivity

Solvent extraction takes a fundamentally different approach, operating as a liquid-to-liquid process rather than a liquid-to-solid one. Brine passes in contact with a specialised organic solvent containing selective extractant compounds that preferentially bind lithium over competing dissolved species. The loaded organic phase is then separated, scrubbed to remove co-extracted impurities, and stripped with an aqueous back-extraction solution to release concentrated lithium. The organic solvent is recirculated for reuse.

This method offers high throughput potential but requires careful management of the organic phase to prevent degradation and loss, and it introduces chemical handling and environmental compliance obligations that must be factored into project economics.

Ion Exchange and Membrane Technologies

Ion exchange operates on a chemically similar principle to adsorption but achieves selectivity through ionic charge-balancing reactions rather than physical surface adhesion. It performs well in high-salinity and chemically complex brines where adsorption materials may underperform.

Membrane technology represents the most nascent but potentially transformative pathway. Selective membranes can, in principle, achieve near-total lithium separation with lower energy inputs, reduced chemical consumption, and minimal land footprint. However, the challenge is that membranes capable of operating reliably at commercial scale in the harsh chemical environment of oilfield brines have not yet been demonstrated outside research settings.

Redox-Couple Electrodialysis: A Cost-Disruptive Research Pathway

Research from Stanford University has described a redox-couple electrodialysis approach with potentially transformative economics. Estimated production costs for this method fall in the range of $3,500 to $4,400 per tonne of lithium hydroxide, compared to approximately $9,100 per tonne for dominant conventional brine evaporation methods. Critically, the technique has been reported to consume less than 10% of the electricity required by current brine extraction processes, while achieving near-100% lithium selectivity.

These figures remain research-stage estimates and have not yet been validated at commercial scale. Investors and industry observers should, consequently, treat them as indicative of a theoretical cost floor rather than a confirmed commercial benchmark.

The following table summarises the comparative performance of key DLE approaches alongside conventional evaporation:

| Technology | Processing Time | Land Footprint | Est. Cost per Tonne (LiOH) | Lithium Selectivity |

|---|---|---|---|---|

| Evaporation Ponds | 12–18 months | Extensive | ~$9,100 | Low to moderate |

| Ion Adsorption | Hours to days | Minimal | Variable | High |

| Solvent Extraction | Hours to days | Minimal | Variable | High |

| Ion Exchange | Hours to days | Minimal | Variable | High |

| Membrane Technology | Hours to days | Minimal | TBD (development stage) | Potentially near-100% |

| Redox-Couple Electrodialysis | Hours to days | Minimal | $3,500–$4,400 (research est.) | ~100% |

Where the Largest Opportunities Are Located

The Permian Basin: Volume That Redefines Scale

The Permian Basin in west Texas and southeast New Mexico generates approximately 22 million barrels of produced water every single day. The sheer volume makes it the most frequently cited DLE target in North America, and for good reason. At that flow rate, even modest lithium concentrations in the brine translate into enormous theoretical recovery potential. Infrastructure co-location is another advantage: produced water gathering systems, pipelines, and disposal wells are already in place, reducing the greenfield capital required to establish a DLE operation.

The chief operating officer of Lithium Harvest, Paw Juul, has characterised the scale of the Permian opportunity as effectively boundless, though he has been clear that large-scale capital deployment remains the principal obstacle to realising it. This is a candid acknowledgement that resource abundance does not automatically translate into commercial production.

The Marcellus Shale: A Northeastern Supply Solution

Theoretical modelling of the Marcellus Shale's produced water volumes and lithium concentrations suggests that full recovery from this single formation could satisfy between 38 and 40 per cent of total US lithium demand. That figure demands context: it represents a theoretical maximum under idealised assumptions about concentration uniformity and recovery efficiency. Nevertheless, even a fraction of that potential would constitute a meaningful domestic supply contribution. The Gradiant facility currently under commissioning in the Marcellus Shale region represents the first commercial test of whether that potential can be realised.

The Smackover Formation: Attracting Major Energy Capital

The Smackover Formation, spanning parts of Arkansas, Texas, and Louisiana, has emerged as one of the most actively contested DLE provinces in the United States. Equinor holds a 45% equity stake across two of Standard Lithium's DLE projects in this formation. Chevron made leasehold acquisitions in northeast Texas and southwest Arkansas during 2025. The entry of supermajors into this formation signals that institutional capital is beginning to view produced-water lithium as a credible strategic asset rather than a speculative exploration play.

Geothermal Brines and South American Salars

Occidental Petroleum and a subsidiary of Berkshire Hathaway formed a joint venture in June 2024 to pursue battery-grade lithium extraction from geothermal brine extraction operations in California's Salton Sea region. Geothermal brines differ chemically from oilfield produced water in important ways: they are typically hotter, often more concentrated, and carry different impurity profiles that require tailored process design.

In South America, Rio Tinto is advancing multiple DLE projects across Argentine salar assets, while Codelco and SQM have structured a joint venture to develop the Salar de Atacama through 2060. These partnerships represent an attempt to retrofit DLE efficiency gains into existing brine infrastructure rather than building entirely new supply chains. Recovering lithium from brines at this scale requires a fundamentally different engineering approach than conventional evaporation-based methods.

The Multi-Mineral Dimension: Beyond Lithium Alone

One of the most underappreciated aspects of produced water processing is that lithium is rarely the only commercially interesting constituent. Depending on formation geology and fluid chemistry, brines can carry recoverable concentrations of magnesium, vanadium, strontium, gold, and copper. Treating produced water as a polymetallic resource rather than a single-mineral target fundamentally changes the project economics.

When lithium recovery is the sole revenue stream, the economics must bear the full weight of pre-treatment, extraction, and refining costs. However, when those same costs can be allocated across multiple co-produced minerals, the per-unit economics of each individual product improve. This portfolio logic is gaining traction among project developers and is increasingly viewed as a prerequisite for long-term commercial sustainability rather than an optional enhancement.

Water recovery represents a third potential revenue pillar. In water-scarce basins like the Permian, treated produced water has agricultural and industrial reuse value. Regulatory frameworks in several US states are evolving to accommodate produced water reuse, creating an additional economic incentive for operators to invest in processing infrastructure that would simultaneously enable lithium recovery.

The next major ASX story will hit our subscribers first

The Step-by-Step Process: How an Oilfield DLE Operation Works

For those unfamiliar with the operational mechanics, the following sequence describes how produced water moves from wellhead to lithium product:

- Produced water collection – Fluids from multiple wellheads and separation facilities are aggregated into centralised gathering systems.

- Pre-treatment and filtration – Residual hydrocarbons are skimmed, suspended solids are filtered, and competing ions are partially removed to protect downstream extraction equipment.

- Selective lithium extraction – Depending on the chosen technology, brine passes over solid sorbents, through organic solvent contactors, or across selective membranes to isolate Li+ ions.

- Desorption and concentration – Lithium is stripped from the loaded extraction medium and concentrated into a purified intermediate solution.

- Downstream refining – The concentrated lithium solution is processed into battery-grade lithium carbonate (Li2CO3) or lithium hydroxide monohydrate (LiOH·H2O), typically requiring purity above 99.5% with tight controls on sodium, potassium, calcium, magnesium, and sulphate impurities.

- Water and residual management – The stripped brine and process water are treated for disposal, injection, or reuse depending on applicable regulatory requirements.

LibertyStream's delivery of its first commercial tonne of lithium carbonate to a US customer in June 2026 represents a milestone demonstrating that this full process chain is now operational at commercial scale in at least one US oilfield context.

Technical and Regulatory Barriers That Remain

The Scale-Up Problem

Direct lithium extraction DLE technology is not a standardised, off-the-shelf solution that can be dropped into any produced water stream and immediately generate battery-grade output. Every brine has a unique chemical fingerprint, and extraction systems must be designed around that specific chemistry. What works optimally for a high-lithium Smackover brine may perform poorly on a Permian Basin fluid with different salinity, temperature, and competing ion concentrations. Pilot testing and brine characterisation are therefore essential de-risking steps before any material capital commitment, adding time and cost to project development timelines.

Regulatory Landscape

US federal and state-level regulations governing produced water management, chemical use, and water disposal or reuse vary significantly across jurisdictions. In some states, produced water is classified as a waste product subject to strict disposal requirements, which complicates efforts to commercially valorise it. In others, regulatory frameworks are actively being updated to accommodate beneficial reuse. Navigating this patchwork is a non-trivial compliance burden for operators, particularly those seeking to operate across multiple basins simultaneously.

Reagent Supply Chains

Selective sorbents, ion exchange resins, and organic solvent extractants are specialised materials with concentrated global supply chains. At commercial scale, ensuring the reliable supply and regeneration of these materials introduces dependencies that project developers must account for in both risk assessments and procurement strategies. Research published in Nature Reviews Earth and Environment has highlighted how these upstream material constraints represent a critical but often overlooked bottleneck for scaling DLE globally.

Three Scenarios for DLE Adoption Through 2035

| Scenario | Key Assumptions | Probable Outcome |

|---|---|---|

| Accelerated Adoption | Sustained elevated lithium prices; capital available; regulatory clarity improves | DLE from produced water supplies 10–15% of US lithium by 2035 |

| Moderate Growth | Technology matures but capital constraints persist; brine variability limits rollout | DLE becomes a meaningful supplementary source, not a primary one |

| Stalled Development | Lithium prices fall; capital dries up; scale-up failures damage investor confidence | DLE remains confined to a small number of niche commercial operations |

"The difference between the accelerated and stalled scenarios is not primarily technological. The core variables are lithium price sustainability, the cost of capital, and whether early commercial operations demonstrate the reliability and purity consistency that battery manufacturers require before signing long-term offtake agreements."

Frequently Asked Questions

What Distinguishes Direct Lithium Extraction from Conventional Brine Processing?

Conventional brine operations in salars pump lithium-rich groundwater into large evaporation ponds, where sunlight and wind slowly concentrate the brine over twelve to eighteen months before chemical precipitation isolates the lithium. DLE replaces that slow physical process with chemical or physical selectivity that achieves the same separation in hours to days, on a fraction of the land area, without dependence on arid climate conditions.

Does Every Produced Water Stream Contain Enough Lithium to Be Worth Processing?

No. Lithium concentrations in produced water vary enormously by formation and even by well. Concentrations below approximately 50 mg/L generally make recovery uneconomic under current cost structures. Thorough brine characterisation before capital commitment is essential, and each project requires a tailored process design rather than a generic solution.

What Purity Standard Does Battery-Grade Lithium Require?

Battery manufacturers typically specify lithium carbonate or lithium hydroxide at purity levels exceeding 99.5%, with strict limits on contaminants including sodium, potassium, calcium, magnesium, and sulphate. Achieving this specification from complex oilfield brines is one of the most technically demanding aspects of the entire process chain.

Which US Formations Offer the Most Near-Term Commercial Potential?

The Permian Basin, with its approximately 22 million barrels of daily produced water, and the Marcellus Shale, with theoretical recovery potential representing 38–40% of US lithium demand, represent the two most significant near-term targets. The Smackover Formation is attracting major energy company capital and is viewed as an emerging tier-one DLE province.

Are There Minerals Other Than Lithium Recoverable from Produced Water?

Yes. Depending on formation chemistry, brines can contain commercially recoverable concentrations of magnesium, vanadium, strontium, gold, and copper. Multi-mineral recovery from produced water is increasingly viewed as the pathway to sustainable long-term project economics rather than a secondary consideration.

What Would Unlock the Full Potential of Wastewater Lithium Recovery

Several conditions would need to converge to shift direct lithium extraction from wastewater from a promising emerging sector to a foundational pillar of domestic lithium supply:

- Standardisation of DLE module designs for the most common produced water chemistries, reducing engineering costs and project timelines

- Advances in membrane technology that lower energy and chemical consumption to levels that improve overall cost competitiveness

- Integration of multi-mineral recovery frameworks that allow project economics to be underwritten by a basket of co-products rather than lithium price alone

- Demonstrated consistency in battery-grade output quality across multiple commercial operations over multi-year timeframes, building the track record that offtake purchasers require

- Regulatory harmonisation across key US producing states to reduce the compliance complexity facing operators seeking to scale across basins

The convergence of energy company infrastructure expertise, mining company process knowledge, and dedicated DLE technology developer innovation is accelerating the sector's development trajectory. Whether that trajectory is fast enough to make a material contribution to the fourfold demand increase projected by 2035 depends on how quickly capital, technology, and regulatory clarity align.

Disclaimer: This article contains forward-looking statements, scenario projections, and cost estimates sourced from research literature and industry reports. These figures are indicative rather than guaranteed and should not be construed as financial advice. Readers considering investment decisions related to lithium, direct lithium extraction technology, or energy transition minerals should conduct independent due diligence and seek qualified professional advice.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including battery metals critical to the energy transition — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.