June 8, 2026

The Geological Backbone Behind West Africa's Gold Dominance

Few investment narratives in the global resources sector carry as much geological conviction as the West African gold story. Long before production statistics began reflecting the region's potential, the underlying rock formations were telling a different story altogether. The Birimian Supergroup, a sequence of volcanic and sedimentary rocks dating back approximately 2.1 to 2.2 billion years, spans a continuous arc across Ghana, Burkina Faso, Côte d'Ivoire, Senegal, Guinea, and Mali. These ancient greenstone belts host some of the most structurally complex and mineralogically rich gold systems found anywhere on earth, characterised by intersecting shear zones that created ideal pressure and temperature conditions for large-scale gold precipitation.

What makes these formations particularly attractive from an investment and development perspective is their versatility. The same geological province supports both shallow, bulk-tonnage open-pit operations and deeper, higher-grade underground targets, allowing producers to adapt extraction methodology as deposit economics evolve over the mine life. Discovery costs across West Africa have historically trended below comparable provinces in Nevada, Australia, and the Andes, reinforcing the region's appeal for exploration capital allocation.

The structural shift in West Africa's contribution to global gold supply over the past two decades is no longer speculative. The region has evolved from a secondary producing zone into a primary driver of supply growth, with major producers concentrating long-term capital commitments there precisely because the combination of geological endowment, operational expertise, and existing infrastructure creates compounding returns that are difficult to replicate in frontier regions.

When big ASX news breaks, our subscribers know first

What the Endeavour Mining West Africa Gold Growth Strategy Actually Means

An Organic-First Model in a Consolidating Industry

At a time when gold sector consolidation is engaged in one of its most aggressive cycles in recent memory, Endeavour Mining's approach stands out for its deliberate restraint. Rather than pursuing growth through acquisition premiums in a high gold price environment, the company has structured its entire expansion around a principle that CEO Ian Cockerill has articulated clearly: organic discovery through the drill bit remains both sufficient and superior to acquisition-led growth.

This is not simply a philosophical preference. It reflects a financial calculation. When elevated gold prices are factored in, acquisition targets command valuations that often bake in years of future cash flow, creating a structural disadvantage for acquirers that must immediately justify premium pricing. By contrast, organic exploration conducted on already-understood geology within an established operating footprint allows companies to discover resources at costs that bear little resemblance to what the same ounces would cost to acquire on the open market.

Endeavour's exploration target of a discovery cost below $40 per ounce illustrates the financial logic in concrete terms. That figure sits well below typical acquisition costs in the current pricing environment, making the organic pathway not just strategically preferable but arithmetically compelling.

The Four Strategic Pillars Driving Production to 1.5 Million Ounces

The Endeavour Mining West Africa gold growth strategy operates across four distinct but interconnected dimensions:

| Strategic Pillar | Description | Time Horizon |

|---|---|---|

| Portfolio Optimisation | Extend mine life and improve unit economics at cornerstone assets | Near-term (2025–2027) |

| Brownfield Expansion | Underground development and near-mine discoveries at existing operations | Medium-term (2026–2028) |

| Greenfield Development | Advance Assafo-Dibibango as a tier-one production driver | Medium-to-long-term (2027–2030) |

| Exploration Pipeline | Target 12–15 million ounces of new resources at under $40/oz discovery cost | Long-term (2026–2030) |

The internal logic connecting these pillars is what makes the strategy structurally resilient. Existing mines generate free cash flow that funds exploration. Exploration replenishes reserves and identifies new development candidates. New projects enter the pipeline and eventually begin contributing production. The cycle repeats without requiring external capital markets or M&A activity to sustain momentum.

Cost discipline reinforces each stage. With royalty-adjusted all-in sustaining costs positioned toward the lower end of annual guidance as of Q1 2026, the company retains a meaningful margin buffer even during periods of gold price softness, preserving the financial capacity to keep the exploration flywheel turning.

Q1 2026 Performance: Reading the Signals Beyond the Headline Numbers

Record Free Cash Flow and What It Reveals

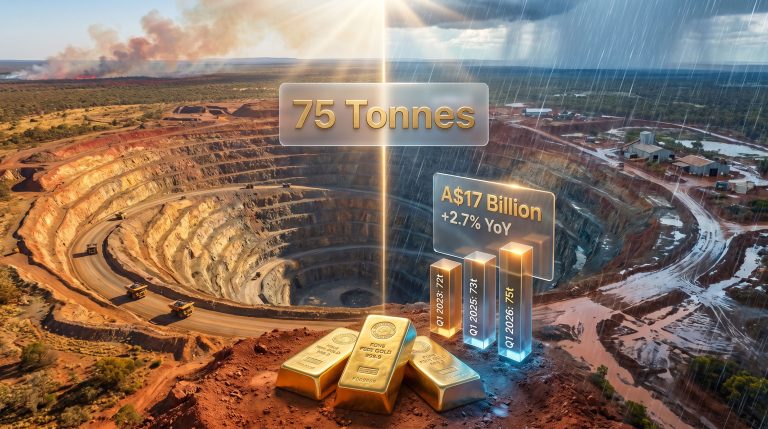

Endeavour's Q1 2026 results delivered 282,000 ounces of gold production, representing approximately 26% of the low end of full-year guidance. On its own, that production figure tells a partial story. The more instructive signal came from the financial conversion rate: the combination of stable costs and elevated gold prices produced record free cash flow for the quarter.

What matters here is not simply that gold prices were high. Multiple producers operate in similar pricing environments without achieving equivalent financial outcomes. The distinguishing variable is operational consistency. As Cockerill confirmed in his June 2026 interview with Ecofin Agency, every mine in the portfolio performed in line with or slightly ahead of internal expectations, a statement that speaks to operational maturity across a geographically diverse set of assets.

Production is expected to progressively improve through the second half of 2026, with the first quarter positioning the company well within its full-year guidance range.

Why Cost Structure Is the Underappreciated Competitive Advantage

In gold mining, two producers can operate adjacent deposits with similar grades and achieve dramatically different financial outcomes depending on their cost structures. The royalty-adjusted all-in sustaining cost metric used by Endeavour provides a more conservative and accurate picture of true operating economics than headline AISC figures that exclude royalties.

For investors, this matters because royalty payments are non-discretionary and often linked to gold price escalators, meaning they rise as prices increase. A company reporting AISC without royalty adjustments can appear more competitive than it actually is during bull markets. Endeavour's use of the royalty-adjusted metric signals a commitment to transparent financial reporting that facilitates genuine peer comparison.

The compounding effect of maintaining low-cost production across a multi-year price cycle is significant. Each dollar saved on operating costs at current gold prices translates directly into free cash flow available for exploration, debt reduction, or shareholder returns, amplifying the impact of every efficiency improvement across the entire asset base.

The Asset Portfolio: Five Mines Building Toward a Singular Ambition

| Asset | Country | Key Development Focus | Strategic Role |

|---|---|---|---|

| Sabodala-Massawa | Senegal | Underground expansion | Reserve extension and grade improvement |

| Houndé | Burkina Faso | Near-pit brownfield discovery | Low-cost reserve replacement |

| Ity | Côte d'Ivoire | Near-mine exploration | Mine life extension |

| Lafigué | Côte d'Ivoire | Ramp-up and optimisation | Portfolio scale and diversification |

| Assafo-Dibibango | Côte d'Ivoire | Greenfield development | Primary long-term growth driver |

You can explore Endeavour's full portfolio to understand how each asset contributes to the group's long-term production ambitions.

Sabodala-Massawa: Underground Depth as the Next Value Layer

Sabodala-Massawa in Senegal represents one of the more technically interesting development stories within the portfolio. The asset already operates as a large-scale producer, but the underground expansion programme introduces a different economic dynamic. Underground mining at established open-pit operations typically accesses higher-grade ore that was either too deep for economic open-pit extraction or was bypassed in earlier mine planning.

When the orebody geometry is favourable, the transition to underground operations can meaningfully improve average head grade and extend mine life simultaneously, improving the unit economics of the overall asset.

Houndé and Ity: The Brownfield Discovery Premium

A near-pit discovery at Houndé carries disproportionate economic value relative to its resource size. New mineralisation identified adjacent to or beneath an existing pit can often be processed through existing infrastructure with minimal incremental capital, effectively adding production at a cost structure far below what a standalone greenfield development would require. The same logic applies to near-mine prospects identified at Ity, where existing heap leach and carbon-in-leach processing infrastructure provides a ready-made pathway for incorporating new ore sources.

This brownfield discovery dynamic is one of the least appreciated drivers of value in established mining operations. Market participants tend to focus on headline resource additions, but the infrastructure-adjusted value of a tonne of ore that can be processed without new capital is materially higher than a tonne requiring fresh processing capacity.

Assafo-Dibibango: Why This Development Asset Changes the Company's Trajectory

The Numbers That Define a Tier-One Asset

Assafo-Dibibango carries a production profile that places it among the most significant new gold developments currently advancing in West Africa. At 320,000 ounces per year for the first eight years of operation, at first-quartile all-in sustaining costs, the asset would rank among the region's top-producing individual mines upon commissioning.

First-quartile cost positioning is a specific and meaningful designation. It means the asset is expected to sit within the lowest 25% of the global cost curve for gold production, providing substantial insulation against gold price cycles and delivering above-average margins through a range of pricing environments. When that cost profile is combined with 320,000 ounces of annual throughput, the financial contribution to Endeavour's group metrics becomes transformative.

Assafo-Dibibango was identified through Endeavour's own exploration programme rather than acquired, meaning the discovery cost reflects the economic advantage of organic exploration over acquisition premiums.

What 320,000 Ounces at First-Quartile Costs Does to the Group Profile

The practical impact of bringing Assafo-Dibibango into production by 2030 extends beyond adding raw volume. When a large, low-cost asset enters a portfolio, it dilutes the group's average cost per ounce downward, improving overall margins even without changes to existing operations. For investors analysing Endeavour's long-term valuation, this dilutive cost effect on the group AISC represents a significant and often undermodelled source of future earnings improvement.

Exploration Strategy 2026–2030: Building the Production Pipeline Beyond the Current Decade

Targeting 12–15 Million Ounces at Under $40 Per Ounce

The five-year exploration programme announced in December 2025 targets the discovery of 12 to 15 million ounces of new gold resources between 2026 and 2030 at a discovery cost below $40 per ounce. The scale of this ambition requires some contextualisation. Replacing production depletion across a portfolio producing over one million ounces annually already demands discovery of millions of new ounces every five years.

The exploration programme is designed not merely to replace what is mined, but to add meaningful net resource growth that supports production beyond 2030. A robust gold exploration strategy of this kind requires both the land position and operational infrastructure to execute at scale, which Endeavour has already assembled across its West African footprint.

| Exploration Metric | Target |

|---|---|

| New resources targeted (2026–2030) | 12–15 million ounces |

| Discovery cost target | Less than $40 per ounce |

| New greenfield deposits targeted | 2–3 standalone deposits |

| Exploration timeframe | 2026–2030 |

| Primary method | Brownfield drilling combined with greenfield targeting |

The JV Model as a Low-Risk Optionality Tool

Endeavour's selective use of joint ventures, illustrated by the East Star Resources partnership in Kazakhstan, reflects a sophisticated approach to building exploration optionality without concentrating capital risk. A JV structure allows a company to gain exposure to prospective geological provinces at a fraction of the cost of direct ownership, while limiting downside if exploration disappoints.

For a company already deploying substantial capital across its West African portfolio, this approach to international exploration diversification is capital-efficient and strategically coherent. It also signals a management team comfortable with the distinction between core and non-core capital deployment, a discipline that is not universally practised in the mid-tier gold sector.

The next major ASX story will hit our subscribers first

Economic Contribution: The Quantitative Foundation of Social Licence

$2.8 Billion in 2025 Across Three Pillars

Endeavour contributed USD 2.8 billion to its West African host economies in 2025, representing a 27% increase year-on-year and exceeding 72% of total revenues reinvested locally. This figure disaggregates across three categories:

- Local economic integration: $1.6 billion in procurement, with 86% directed to host-country suppliers, alongside $309 million in salaries and benefits paid to a workforce that is 95% nationally employed

- Public revenue contribution: $919 million delivered to host governments through taxes, royalties, and dividends

- Financial system support: $69 million repaid to domestic financial institutions

The five-year cumulative figure of over $12 billion contributed to host economies between 2021 and 2025 provides the most striking framing. That total is approximately seven times the amount returned to shareholders over the same period, fundamentally repositioning how the company's value distribution model should be understood. This is not a company extracting value from West Africa and redistributing it elsewhere.

Navigating Fiscal Evolution With Proactive Engagement

West Africa's fiscal frameworks for mining operate on broadly consistent terms across WAEMU member states, providing a degree of cross-border regulatory coherence that is uncommon in other mining-intensive regions. These frameworks typically undergo revision on approximately ten-year cycles, with the natural direction of change being incremental increases in government revenue participation, particularly during periods of elevated commodity prices.

Rather than treating this dynamic as a threat, Endeavour's stated approach is to engage proactively with governments at multiple levels, ensuring that any fiscal evolution remains economically sustainable for both the state and the operator. A government that captures more revenue from a profitable mine continues to benefit from that mine's ongoing operation. One that imposes terms that compromise operator economics risks the cessation of investment entirely.

The M&A Question: Why Organic Growth Is Both Sufficient and Preferable

The Financial Logic of Staying Disciplined

The current consolidation wave reshaping the global gold sector is driven by senior producers seeking to replace depleting reserve bases in an environment where organic discovery has become increasingly difficult at scale. For companies without established exploration platforms in proven geological provinces, acquisition becomes the path of least resistance.

Endeavour's position is structurally different. With a large West African land package, established operational expertise across five producing mines, and a brownfield discovery pipeline actively delivering results, the company faces no reserve replacement crisis that would justify paying acquisition premiums. Cockerill has been direct on this point: the Endeavour Mining West Africa gold growth strategy's pathway to 1.5 million ounces per year by 2030 does not require M&A activity to succeed.

The criteria framework Endeavour would apply to any potential transaction reflects genuine capital discipline:

- Strategic fit with the existing West African operational footprint

- Risk profile compatible with proven operating expertise

- Financial returns that clear disciplined internal hurdle rates

- A clear value creation pathway that organic development could not achieve more efficiently

Furthermore, investors evaluating gold mining stocks in the mid-tier space will recognise that this kind of disciplined M&A framework is relatively rare and warrants a premium in portfolio consideration.

The Consolidation Irony

There is an underappreciated irony in Endeavour's position within the current consolidation cycle. A company with an organically built, low-cost portfolio, a major development project advancing toward production, and a five-year exploration programme targeting 12 to 15 million new ounces may be more attractive as a consolidation target than as an acquirer.

The very qualities that make the organic strategy compelling for management also make the asset base compelling for senior producers seeking exactly the kind of long-life, low-cost production Endeavour has assembled.

Mali and the Kalana Decision: Capital Discipline in Practice

Kalana in Mali occupies a specific and instructive position in understanding how Endeavour's capital allocation framework operates in practice. The asset is an early-stage development project that sits outside the core portfolio. After evaluating multiple structural options, the company concluded that transitioning Kalana to a joint venture with a dedicated local partner represents the optimal path forward. This structure ensures the project receives focused development attention without competing with core assets for capital.

The decision reflects a principle that is straightforward to articulate but harder to execute: when an asset does not meet the return profile of the core portfolio, the right answer is structured partnership rather than forced development or outright disposal. Throughout the transition process, Endeavour has maintained continuous dialogue with Malian authorities, working toward an orderly outcome that preserves value for all stakeholders.

West Africa's Gold Future: Growth Conditions and Structural Potential

What a 1.5 Million Ounce Regional Leader Looks Like by 2030

The pathway from Endeavour's current production base to 1.5 million ounces per year by 2030 runs primarily through Assafo-Dibibango's contribution and progressive brownfield expansion across existing operations. That trajectory, if achieved, would cement the company's position as West Africa's leading gold producer by a significant margin. According to Endeavour's published strategy, this ambition is underpinned by a disciplined capital allocation framework that prioritises long-term value over short-term production volume.

The broader regional picture reinforces the opportunity. West Africa's Birimian belts remain significantly underexplored relative to comparable gold provinces globally, suggesting that the current wave of discovery activity is a beginning rather than a maturation. Infrastructure built to support existing operations reduces the capital intensity of future developments, creating a positive feedback loop between current investment and future exploration value.

Completing a definitive feasibility study on key development assets will be a critical milestone in converting this structural potential into investable certainty. The conditions required for this potential to be realised include:

- Mutual fiscal stability, with governments respecting existing investment frameworks whilst operators deliver on economic contribution commitments

- Continued investment in local workforce development and supply chain localisation, deepening the host-economy integration that underpins social licence

- Transparent engagement frameworks that align producer, government, and community interests across the full mine life cycle

Disclaimer: This article contains forward-looking statements and projections regarding production targets, exploration outcomes, and financial performance. These projections are based on current plans and assumptions and are subject to material risks including gold price volatility, geopolitical and security conditions, regulatory changes, exploration outcomes, and operational factors. Readers should not rely on these projections as predictions of future performance. Past financial results do not guarantee future outcomes.

Want to Track the Next Major West African Gold Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological data into actionable investment insights — explore historic discovery returns to understand the magnitude of opportunities these moments can create, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.