May 22, 2026

Global supply chain dynamics have fundamentally shifted as nations grapple with unprecedented vulnerabilities in critical mineral dependencies. The intersection of geopolitical tensions and resource scarcity has created a complex web of relationships that extends far beyond traditional trade partnerships. Furthermore, modern economies increasingly recognize that control over essential materials translates directly into strategic leverage, forcing governments to recalibrate their diplomatic approaches while simultaneously pursuing alternative sourcing strategies. In this context, germany china rare earth talks have emerged as a crucial diplomatic initiative that could reshape European access to essential materials.

Current Diplomatic Developments in Germany-China Rare Earth Negotiations

Recent high-level engagement between German and Chinese officials marks a significant development in addressing European supply chain vulnerabilities. German Foreign Minister Johann Wadephul's December 8-9, 2025 diplomatic mission to Beijing represents the first substantial ministerial contact since Chancellor Friedrich Merz assumed office in May 2025, following a period of deteriorating bilateral relations.

The timing of these discussions proves particularly strategic, occurring against a backdrop of mounting pressure on European manufacturers who face potential production disruptions. Consequently, Wadephul's meetings with Commerce Minister Wang Wentao, Foreign Minister Wang Yi, and Vice President Han Zheng yielded what German officials describe as constructive progress toward resolving access issues.

General Licensing System Implementation

China's introduction of a general licensing framework for rare earth exports, effective December 1, 2025, represents a significant policy shift from previous restrictive measures. The system requires European companies to submit detailed applications demonstrating end-use purposes, with processing timelines reduced to 30-45 days from previous periods exceeding 90 days.

Key features of the licensing system include:

- Streamlined application processes for established trading relationships

- Priority processing for companies demonstrating no viable alternative sources

- Specific coverage of all 17 rare earth elements critical to European manufacturing

- Transparent criteria focusing on legitimate commercial applications

The Chinese Ministry of Commerce has indicated that applications from German companies will receive constructive consideration, with officials emphasizing their commitment to maintaining stable global supply chains rather than weaponizing resource access. Additionally, the mining industry innovation has played a crucial role in developing more efficient extraction and processing methods.

Bilateral Commitment Mechanisms

The diplomatic engagement has established preliminary frameworks for ongoing dialogue between the two nations. German officials report that Chinese counterparts have assured them of intentions to handle European requests constructively, with no deliberate attempts to burden German companies with additional complications.

This represents a notable shift from the tensions that emerged following Chancellor Merz's election, including Wadephul's canceled October 2025 visit to China and previous diplomatic friction over Taiwan policy. However, the current engagement suggests both nations recognize the mutual benefits of maintaining stable economic relationships despite broader geopolitical disagreements.

When big ASX news breaks, our subscribers know first

China's Rare Earth Export Controls Impact on European Manufacturing

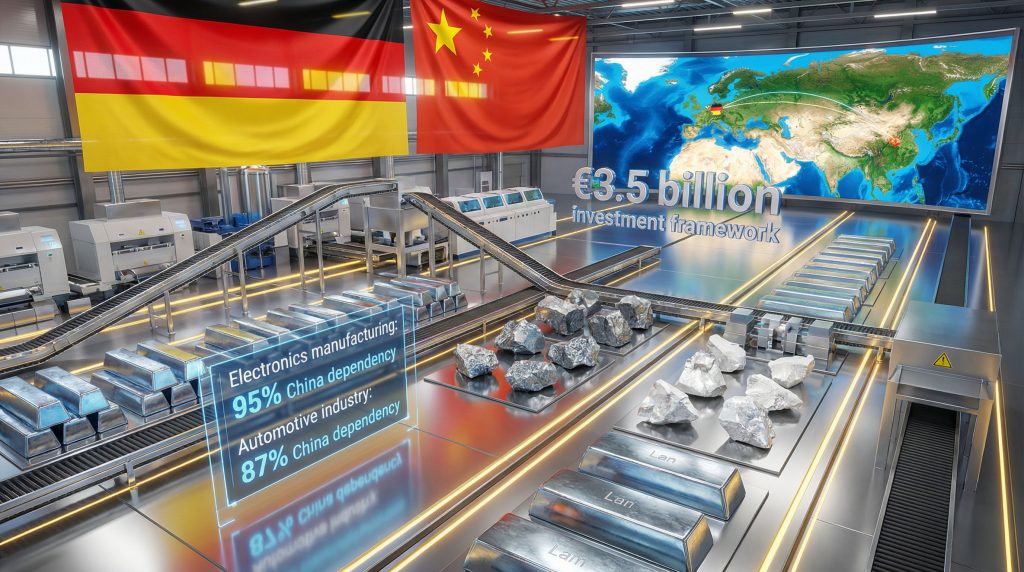

European industrial sectors face unprecedented vulnerability due to their overwhelming dependence on Chinese rare earth supplies. Current dependency levels across critical manufacturing sectors reveal the extent of this strategic exposure:

| Manufacturing Sector | China Dependency Rate | Critical Applications |

|---|---|---|

| Electronics Manufacturing | 93.5% | Semiconductors, displays, magnets |

| Automotive Industry | 85% | Electric vehicle motors, sensors |

| Defense Applications | 92% | Advanced weaponry, radar systems |

| Renewable Energy | 89% | Wind turbine generators, solar panels |

Manufacturing Disruption Scenarios

Supply chain analysts project that sustained restrictions on rare earth access could trigger cascading effects across European industrial capacity. The European Central Bank's latest financial stability review estimates potential economic losses of €17.5 billion in the first year of significant supply disruptions, with production delays extending 3-6 months across multiple sectors.

The automotive sector faces particularly acute risks, with electric vehicle production heavily dependent on neodymium and dysprosium for permanent magnets. Furthermore, current stockpile levels across major European manufacturers average only 45-60 days of production capacity, insufficient to weather extended supply interruptions. This vulnerability directly relates to critical minerals energy security concerns across the continent.

Electronics Production Bottlenecks

European electronics manufacturers have identified critical vulnerabilities in their rare earth supply chains, particularly for smartphone production and industrial equipment manufacturing. Companies report that current inventory management practices, optimized for just-in-time delivery, leave minimal buffer capacity for supply disruptions.

"Manufacturing executives across Europe report heightened concerns about supply chain stability, with many companies accelerating contingency planning and exploring alternative sourcing arrangements despite higher costs and longer lead times."

The semiconductor industry faces additional challenges, as rare earth elements are essential for:

- Phosphor production for LED displays

- Magnetic storage device manufacturing

- High-performance computing components

- Advanced sensor technologies

Industry analysis suggests that a 6-month supply disruption could reduce European electronics output by 15-20%, with recovery periods extending 12-18 months due to complex supply chain interdependencies.

Strategic Alternatives European Nations Are Pursuing

The European Union has committed €3.2 billion through 2027 to reduce critical mineral dependencies, representing the most ambitious supply chain diversification initiative in the bloc's history. This comprehensive strategy encompasses multiple approaches to achieving greater resource security.

EU Critical Minerals Diversification Framework

The diversification strategy targets 30-40% reduction in Chinese rare earth dependency by 2030 through a combination of alternative sourcing partnerships, domestic processing capacity development, and technological innovation programs. The Australian critical minerals reserve represents one of the most promising alternatives to Chinese supplies. Key initiatives include:

Strategic Partnerships:

- €750 million EU-Australia critical minerals agreement beginning Q1 2026

- Canadian rare earth processing joint ventures worth €650 million

- African mining development projects totaling €1.2 billion over four years

Domestic Capacity Building:

- €580 million recycling infrastructure investment program

- €900 million research and development initiative for substitute materials

- Strategic stockpile establishment across member nations

In addition, the European CRM facility initiative aims to enhance domestic processing capabilities.

Technology Innovation Pathways

European research institutions are pursuing breakthrough technologies to reduce rare earth consumption through improved recycling methods and alternative materials development. Current programs focus on:

-

Advanced Recycling Technologies

- Hydrometallurgical processing improvements

- Magnetic separation enhancement techniques

- Urban mining from electronic waste streams

-

Substitute Material Development

- Iron-based permanent magnet research

- Ceramic superconductor applications

- Nanomaterial alternatives for electronic components

-

Efficiency Optimization

- Reduced rare earth content in manufacturing processes

- Improved product lifecycle management

- Enhanced material recovery systems

The European Commission projects these combined efforts could achieve 8% domestic rare earth recovery capacity by 2026, with substitute materials contributing an additional 12% reduction in import requirements by 2030.

Geopolitical Tensions Influence on Rare Earth Trade Relations

The evolving relationship between Germany and China reflects broader shifts in global power dynamics, with rare earth access serving as both a diplomatic tool and a strategic vulnerability. Chancellor Merz's administration has adopted a noticeably tougher stance toward Beijing compared to previous governments, emphasizing economic security alongside traditional trade relationships.

Diplomatic Balancing Challenges

German-Chinese trade volumes decreased 12.3% in the first half of 2025, reflecting growing economic tensions that extend beyond rare earth access. The relationship has been strained by disagreements over:

- Taiwan Strait security concerns and Chinese military activities

- Ukraine conflict resolution and German expectations for Chinese influence on Russia

- Technology transfer restrictions and market access limitations

- Human rights issues and democratic governance principles

Despite these challenges, both nations recognize the economic costs of complete decoupling, leading to the current diplomatic engagement focused on managing tensions while maintaining essential trade relationships. According to reports from German diplomatic sources, the recent discussions have shown measurable progress.

Strategic Competition Framework

The US-China technological rivalry has created additional complications for European rare earth strategy, as American export controls and sanctions create secondary effects on global supply chains. European External Action Service reports indicate a 15% decrease in high-tech trade discussions between the EU and China since mid-2025 geopolitical incidents. These US‑China trade impacts have created ripple effects across global supply chains.

This dynamic forces European nations to navigate between:

- Maintaining alliance coordination with the United States

- Preserving essential economic relationships with China

- Developing independent strategic capabilities

- Managing domestic political pressures for greater autonomy

Furthermore, German officials have emphasised the importance of fair trade practices in their ongoing discussions with Beijing.

Long-Term Implications for Global Rare Earth Markets

Market analysts project three primary scenarios for rare earth supply chain evolution over the next decade, each carrying distinct implications for pricing, investment, and geopolitical relationships. The outcome of ongoing germany china rare earth talks will significantly influence which scenario ultimately unfolds.

Market Restructuring Scenarios

Scenario 1: Successful Cooperation Model

Under sustained Germany-China diplomatic engagement, rare earth prices could stabilise with a 5-10% decrease from current levels by 2027, according to World Bank commodity projections. This outcome requires continued Chinese cooperation and European acceptance of managed dependency relationships.

Scenario 2: Accelerated European Independence

Successful implementation of EU diversification strategies could reduce Chinese market share from current 85% to approximately 50% by 2030. This transition would likely maintain higher pricing levels but provide greater supply security for European manufacturers.

Scenario 3: Fragmented Global Supply Chains

Continued geopolitical tensions could lead to parallel supply systems serving different geopolitical blocs, potentially increasing overall costs by 25-35% while reducing efficiency gains from global integration.

Investment Opportunities Assessment

Non-Chinese rare earth mining projects have attracted $4.2 billion in investment during 2025, representing a 40% increase from previous years. Key investment themes include:

- Processing Technology Development: Advanced separation and purification methods

- Alternative Material Research: Substitute compounds and recycling innovations

- Strategic Infrastructure: Transportation, storage, and distribution networks

- Geopolitical Hedging: Projects in politically stable jurisdictions

S&P Global Commodity Insights projects continued strong investor interest in diversified rare earth assets, with particular focus on projects offering strategic value beyond pure financial returns.

Strategic Recommendations for Stakeholders

For European Manufacturers

Immediate action items for companies dependent on rare earth inputs include:

- Licensing Applications: Submit comprehensive applications under China's general licensing system while terms remain favourable

- Supply Chain Mapping: Conduct detailed audits of rare earth dependencies across all product lines and supplier relationships

- Strategic Partnerships: Establish relationships with alternative suppliers in Australia, Canada, and Africa

- Inventory Management: Increase strategic stockpiles to 90-120 days of production capacity

- Technology Investment: Develop internal recycling capabilities and explore substitute materials

For Investment Community

Portfolio strategy considerations should encompass:

- Diversified Exposure: Balance Chinese supply chain investments with alternative source development projects

- Technology Innovation: Focus on companies developing recycling, substitute materials, and efficiency improvements

- Infrastructure Development: Consider long-term investments in processing facilities and transportation networks

- Geopolitical Risk Management: Evaluate political stability and regulatory environments across potential investment jurisdictions

For Policy Makers

Government strategy frameworks should prioritise:

- Diplomatic Engagement: Maintain constructive dialogue with China while pursuing diversification objectives

- Strategic Investment: Accelerate funding for alternative supply chain development and domestic processing capacity

- Regulatory Coordination: Align export controls and trade policies with allied nations to maximise leverage

- Innovation Support: Enhance research and development programmes for rare earth alternatives and recycling technologies

The next major ASX story will hit our subscribers first

Navigating the Critical Minerals Transition

The germany china rare earth talks illuminate the complex challenges facing nations as they attempt to balance economic interdependence with strategic autonomy. While diplomatic progress offers hope for near-term supply stability, the underlying vulnerabilities revealed by this episode demonstrate the urgent need for comprehensive supply chain transformation.

European stakeholders must recognise that current diplomatic success, while encouraging, represents only a temporary solution to deeper structural challenges. The path forward requires sustained commitment to diversification strategies, technological innovation, and diplomatic engagement that acknowledges both the realities of current dependencies and the imperatives of future security.

The transition away from overwhelming reliance on single-source supply chains will prove costly and time-consuming, but the alternative risks of supply weaponisation and geopolitical manipulation present even greater long-term challenges. Success will require coordinated efforts across industry, government, and international partnerships, with clear recognition that energy security and economic prosperity increasingly depend on control over critical mineral resources.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and policy developments. Actual outcomes may vary significantly due to changing geopolitical circumstances, technological developments, and market dynamics. Investors and stakeholders should conduct independent research and consider multiple scenarios when making strategic decisions.

Are You Positioning Yourself for Critical Minerals Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical minerals essential to global supply chains, empowering subscribers to identify actionable opportunities ahead of the broader market. Visit Discovery Alert's dedicated discoveries page to understand why major mineral discoveries can generate substantial returns and begin your 30-day free trial today to position yourself ahead of the market.