May 22, 2026

Mali mining sector changes have become a defining characteristic of West Africa's evolving resource governance landscape, as the country implements comprehensive regulatory reforms that fundamentally alter the relationship between international operators and state authorities. This transformation exemplifies a broader continental shift toward enhanced state participation and domestic value capture mechanisms that prioritize national interests over traditional foreign investment models.

The regulatory evolution reflects growing confidence among African mineral-rich nations in asserting greater control over their natural resources. Furthermore, Mali's approach provides a template for other jurisdictions seeking to balance foreign investment attraction with meaningful domestic participation in extractive industries.

How Has Mali's 2023 Mining Code Transformed Resource Governance?

The 2023 mining code represents a fundamental restructuring of Mali's approach to resource extraction, establishing a multi-tiered ownership framework that prioritizes state participation and community involvement. Under the new regulatory structure, Mali automatically acquires a 10% equity stake in all new mining ventures without upfront capital requirements, providing direct representation on project boards and access to operational decision-making processes.

Beyond this baseline participation, the government maintains an additional 20% purchase option during the first two years of production, creating strategic flexibility to increase state ownership when projects demonstrate commercial viability. This staged acquisition model allows Mali to minimize early-stage investment risk while capitalizing on successful operations through equity participation rather than relying solely on traditional taxation mechanisms.

State Ownership Requirements Under the New Framework

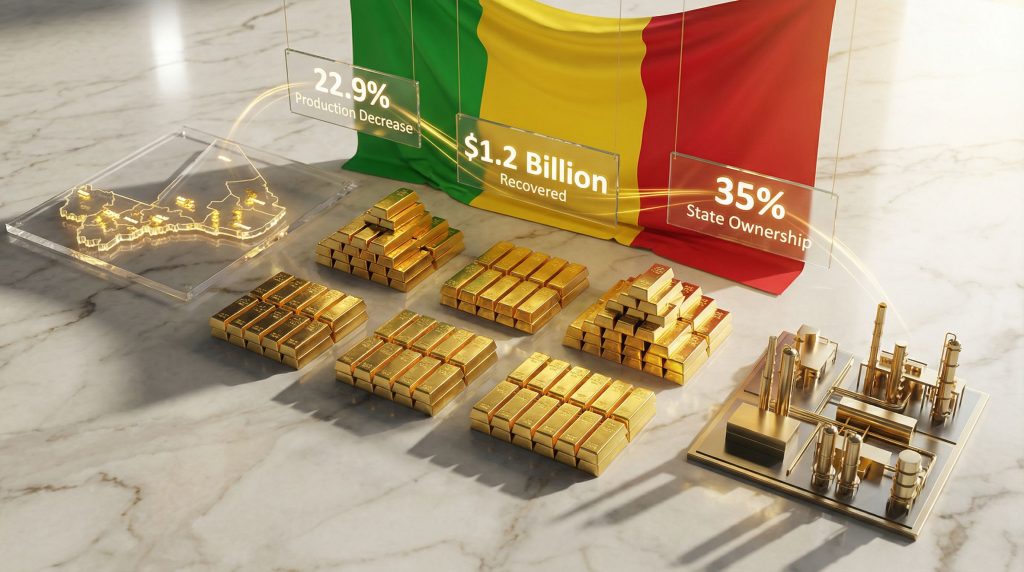

The ownership structure extends beyond direct government participation to include mandatory 5% local community allocations, bringing potential total domestic control to 35% under full implementation. This represents a dramatic shift from previous frameworks that typically granted foreign operators controlling stakes with minimal state participation requirements.

| Ownership Category | Percentage | Implementation Timeline |

|---|---|---|

| Automatic Government Stake | 10% | Immediate upon permit issuance |

| Government Purchase Option | 20% | Within first two years of production |

| Local Community Allocation | 5% | Concurrent with production commencement |

| Total Potential State Control | 35% | Full implementation by year two |

The regulatory framework introduces additional control mechanisms through permit transfer restrictions, requiring mandatory government approval for any ownership changes among existing operators. This prevents rapid equity reshuffling without state oversight and ensures Mali maintains visibility into foreign investment patterns affecting its strategic mineral resources.

Additionally, a tripartite governance model has emerged, with the presidency assuming direct oversight of key exploitation permits and contract negotiations. The industry evolution trends reflect this consolidation representing a significant departure from previous administrative structures where mining oversight was distributed across multiple agencies.

Permit Transfer and Control Mechanisms

Strategic mineral prioritization under the new code emphasizes lithium and uranium development alongside traditional gold operations, reflecting Mali's recognition of critical minerals strategy growing importance in global supply chains. The government has implemented a three-permit maximum per district limitation, though specific enforcement mechanisms and geographical definitions remain subject to ongoing regulatory clarification.

Local content requirements mandate both hiring and procurement preferences for domestic suppliers, creating non-equity value capture mechanisms that complement direct ownership participation. These provisions require operators to demonstrate measurable contributions to local economic development beyond traditional tax and royalty payments.

The appointment of Hilaire Bebian Diarra, formerly a Barrick executive who transitioned to government service during the Loulo-Gounkoto complex negotiations, exemplifies the knowledge transfer occurring between private operators and state administration. This institutional knowledge integration may accelerate policy implementation while raising questions about potential regulatory capture dynamics.

When big ASX news breaks, our subscribers know first

What Impact Did Regulatory Changes Have on Gold Production?

Mali mining sector changes experienced significant disruption during the regulatory transition period, with industrial output declining 22.9% from a 2023 peak of 66.48 tons to approximately 42.2 tons in 2025. This production decrease directly correlates with operational disruptions at major mining facilities as the government enforced new ownership and compliance requirements.

Production Statistics and Decline Analysis

The Loulo-Gounkoto complex, Mali's largest industrial gold operation, became the focal point of regulatory enforcement when government authorities assumed operational control in June 2025. Following a complete production halt, limited operations resumed in July 2025, generating only 5.5 tons of output during the initial restart phase.

| Time Period | Production Status | Monthly Output | Cumulative Impact |

|---|---|---|---|

| January-May 2025 | Normal Operations | ~5.5 tons/month | 27.5 tons |

| June 2025 | Government Takeover | 0 tons | Production halt |

| July 2025 | Limited Restart | 5.5 tons | Reduced capacity |

| August-December 2025 | Gradual Recovery | Variable | ~9.2 tons estimated |

The production disruption methodology reveals that forced operational cessation, even for relatively brief periods, generates disproportionate impacts on annual output due to gold mining's capital-intensive nature and continuous processing requirements. Equipment ramp-up procedures, processing pipeline restoration, and ore development work resumption typically require several months for full capacity restoration.

Operational Disruptions and Recovery Timeline

Industrial gold mining operations depend on uninterrupted processing cycles to maintain economic efficiency. The June 2025 operational suspension at Loulo-Gounkoto disrupted established production rhythms, requiring extensive coordination between government administrators and technical personnel to restore functionality.

Recovery patterns suggest that production restoration follows predictable technical constraints rather than political considerations. Mining equipment requires systematic reactivation procedures, ore stockpile management must be reestablished, and safety protocols demand comprehensive inspection before full-rate operations can resume.

However, the government's willingness to accept temporary production losses in pursuit of regulatory compliance demonstrates that policy enforcement took priority over immediate revenue generation. This strategic calculation implies confidence that long-term governance improvements would offset short-term production disruptions through enhanced gold production insights.

Important Note: Mining production figures should be verified against official Ministry of Mines publications, as preliminary data may be subject to revision based on final processing and quality assessments.

How Much Revenue Has Mali Recovered Through Mining Audits?

Mali's comprehensive mining sector audit generated $1.2 billion (761 billion CFA francs) in recovered arrears, representing one of the most significant revenue recovery efforts in recent West African mining history. This substantial figure reflects cumulative historical tax and royalty obligations that had remained unpaid under previous regulatory frameworks.

Financial Recovery Breakdown

The December 2025 government announcement of the $1.2 billion recovery represents successful enforcement of the 2023 mining code's compliance requirements. However, this figure encompasses multiple years of accumulated obligations rather than annualized ongoing revenue, making it essential to distinguish between one-time historical recovery and sustainable future income streams.

Key Financial Recovery Components:

- Historical tax obligations previously unpaid or disputed

- Mining royalty payments calculated under revised assessment methodologies

- Penalties and interest charges for late or incomplete payments

- Compliance fees associated with permit maintenance and renewal

- Infrastructure development contributions required under new regulations

Sector-wide audit methodology employed both internal government assessors and external verification processes to ensure comprehensive coverage of major operators. The systematic approach examined multiple years of operational history, focusing particularly on periods when regulatory oversight may have been insufficient or enforcement inconsistent.

State Infrastructure Development Initiatives

Revenue recovery has enabled significant infrastructure investments, most notably the development of West Africa's first state-owned gold refinery in partnership with Russian industrial consortium Yadran. The facility is designed with 200 tons annual processing capacity, representing a strategic shift toward domestic value-added processing rather than raw ore export.

This refinery development exemplifies import substitution strategies designed to capture additional value from Mali's mineral resources. By processing gold domestically rather than exporting unrefined ore, Mali aims to generate employment opportunities in higher-skilled technical operations while reducing dependence on foreign processing facilities.

Consequently, the Russian partnership arrangement provides technical expertise and equipment supply while maintaining Malian operational control, reflecting the government's preference for technology transfer agreements that build domestic capacity rather than creating new forms of foreign dependence.

What Are the Long-Term Implications for International Mining Investment?

Mali mining sector changes create a new risk-return framework for international mining investment that prioritizes partnership models over traditional concession structures. Foreign operators must now navigate more complex approval processes while accepting reduced ownership stakes and enhanced government oversight.

Risk Assessment for Foreign Mining Companies

Critical Compliance Requirements: All new mining ventures must accommodate 10% automatic state participation, prepare for potential additional 20% government acquisition, and implement measurable local content programs from project inception.

Investment decision frameworks must incorporate extended negotiation timelines, enhanced due diligence requirements, and ongoing compliance monitoring costs that were previously minimal under older regulatory structures. The consolidation of mining oversight under presidential authority means that political relationships and government stability assessments become increasingly important factors in project evaluation.

Due Diligence Checklist for New Entrants:

- Political Risk Assessment: Evaluate long-term government stability and policy continuity

- Ownership Structure Planning: Design equity frameworks accommodating state participation requirements

- Local Content Strategy: Develop comprehensive hiring and procurement plans for domestic suppliers

- Compliance Cost Estimation: Budget for enhanced regulatory oversight and reporting requirements

- Partnership Evaluation: Assess potential joint venture arrangements with Malian entities

Contract renegotiation precedents established through the Barrick dispute resolution create templates for future operator-government negotiations. These precedents suggest that established operators may face retroactive application of new requirements, while new entrants can plan for current regulations from project inception.

Strategic Mineral Diversification Beyond Gold

Mali's focus on lithium and uranium development reflects recognition that traditional gold mining, while economically important, provides limited strategic advantage in evolving global supply chains. Critical minerals offer potential for enhanced geopolitical leverage and industrial development beyond simple commodity export.

Strategic Mineral Development Priorities:

- Lithium: Battery industry supply chain integration opportunities

- Uranium: Nuclear energy sector participation and strategic resource control

- Rare Earth Elements: Technology industry supply chain diversification

- Copper: Infrastructure development and industrial expansion support

Export dependency reduction strategies emphasise domestic processing capacity development and regional value chain integration rather than continued reliance on raw material exports to developed economies. This approach requires substantial infrastructure investment but offers potential for higher-value economic participation through effective mining investments strategies.

How Does Mali's Approach Compare to Other African Mining Jurisdictions?

Mali's 35% potential state ownership requirement positions it among the more assertive African jurisdictions in terms of resource nationalism, though several regional neighbours have implemented similar frameworks with varying degrees of success.

Regional Regulatory Benchmarking

| Country | State Ownership % | Local Content Requirements | Revenue Sharing Model |

|---|---|---|---|

| Mali | 10-35% | Mandatory hiring/procurement | Equity + taxation |

| Ghana | 10% | Local supplier preferences | Traditional taxation |

| Burkina Faso | 10-20% | Employment quotas | Royalties + profit sharing |

| Guinea | 15% | Training requirements | Variable taxation |

| Niger | 10% | Local partnership mandates | Fixed royalty rates |

Regional investment climate rankings reflect the ongoing tension between resource control objectives and foreign investment attraction. Mali's approach represents a middle path between complete state ownership (as seen in some socialist-oriented jurisdictions) and minimal government participation (traditional liberal frameworks).

Furthermore, recent developments across the continent demonstrate that Mali's president tightens direct control over key mining sector operations, reflecting broader continental trends toward enhanced state oversight.

Economic Dependence and Diversification Challenges

Mali's 80%+ export dependency on gold sector revenues creates significant economic vulnerability that the new mining code attempts to address through enhanced state participation and domestic processing requirements. This level of mineral export dependence exceeds most global benchmarks for economic sustainability.

The mining sector provides employment for approximately 10% of Mali's population when including direct operations, supply chain activities, and artisanal mining participation. This employment concentration makes mining policy changes particularly sensitive from both economic and political perspectives.

GDP contribution analysis reveals that mining represents Mali's primary source of foreign currency earnings and government revenue, making successful regulatory implementation essential for broader economic stability. However, this dependence also creates pressure to balance enforcement with continued investment attraction.

What Does the Future Hold for Mali's Mining Sector?

Production recovery projections suggest that Mali's gold output could return to pre-disruption levels by 2027, assuming successful implementation of the new regulatory framework and continued operator compliance with enhanced requirements.

Production Recovery Projections

Short-term forecasts through 2026-2027 indicate gradual capacity restoration as operators adapt to new compliance requirements and operational structures. The Loulo-Gounkoto complex recovery timeline provides a template for sector-wide production normalisation patterns that align with broader gold market resurgence expectations.

Recovery Scenarios:

Optimistic Pathway (70% probability):

- 2026: 55-60 tons annual production

- 2027: 65-70 tons (approaching 2023 peak levels)

- 2028+: Potential expansion beyond historical peaks with new development

Baseline Scenario (20% probability):

- 2026: 45-50 tons annual production

- 2027: 55-60 tons (gradual recovery)

- 2028+: Stabilisation at 60-65 tons annually

Pessimistic Outcome (10% probability):

- Continued regulatory disputes limiting recovery

- Production stabilising below 50 tons annually

- Additional foreign operator departures

Infrastructure investment requirements for production optimisation include transportation network improvements, processing facility upgrades, and technical training programmes to support domestic capacity building objectives.

Geopolitical Considerations and Market Access

International sanctions and diplomatic tensions may affect Mali's market access options, potentially requiring alternative export routes and trading relationships. The Russian partnership for gold refinery development exemplifies this reorientation toward non-traditional international economic relationships.

Regional integration opportunities through Economic Community of West African States (ECOWAS) mechanisms could provide alternative market access channels. However, political tensions within the regional organisation may limit immediate opportunities for enhanced cooperation.

Alternative export route development becomes increasingly important as Mali seeks to reduce dependence on specific transportation corridors that may be subject to external political pressures or economic sanctions.

The next major ASX story will hit our subscribers first

Key Takeaways for Stakeholders

Mali mining sector changes represent a comprehensive shift toward enhanced state control and domestic value capture that will likely influence regulatory approaches across West Africa's mineral-rich jurisdictions.

Investment Decision Framework

Risk-Return Analysis Considerations:

- Higher Entry Costs: Enhanced compliance requirements and state participation reduce operator control

- Extended Negotiation Timelines: Government oversight consolidation may accelerate or complicate approval processes

- Operational Flexibility: State board representation affects decision-making autonomy

- Revenue Sharing: Equity participation supplements traditional taxation mechanisms

- Political Stability: Centralised oversight creates both opportunities and vulnerabilities

Compliance cost estimation must incorporate legal advisory services, ongoing regulatory reporting requirements, local content programme implementation, and potential dispute resolution procedures that were previously minimal considerations.

Policy Evolution Indicators

Monitoring mechanisms for future regulatory changes should focus on presidential decree patterns, mining ministry enforcement actions, and international arbitration proceedings that may signal policy direction shifts.

Critical Success Factors for New Mining Ventures:

- Early engagement with government stakeholders during project development phases

- Comprehensive local content strategies exceeding minimum requirements

- Technology transfer commitments supporting domestic capacity building

- Environmental and social governance programmes aligned with community development objectives

- Flexible financial structures accommodating potential state equity participation

Stakeholder engagement processes increasingly require direct coordination with presidential authorities rather than traditional ministry-level negotiations, reflecting the governance centralisation under current political leadership.

In addition, long-term sector sustainability metrics will depend on successful balance between enhanced state participation and continued attraction of international technical expertise and capital investment necessary for complex mining operations.

Disclaimer: This analysis is based on available public information and should not be considered investment advice. Mining sector regulations in Mali continue to evolve, and potential investors should seek current legal and regulatory guidance before making investment decisions.

Want to Capitalise on ASX Mineral Discovery Opportunities?

Whilst Mali's mining sector demonstrates the transformative impact of major resource discoveries on national economies, Australian investors can access similar opportunities through Discovery Alert's proprietary Discovery IQ model, which instantly identifies significant mineral discoveries across ASX-listed companies. Start your 30-day free trial today to position yourself ahead of major ASX discoveries before they reshape market valuations.