June 9, 2026

The Second Profit Supercycle: How Geopolitical Fragmentation Is Reshaping Commodity Trading

History rarely repeats in commodity markets, but it frequently rhymes. The extraordinary profit surge recorded across major physical commodity trading houses in 2022 and 2023 was widely attributed to pandemic-era supply chain dislocations and the energy shock triggered by Russia's invasion of Ukraine. At the time, many analysts assumed those conditions were temporary. That assumption is now being tested.

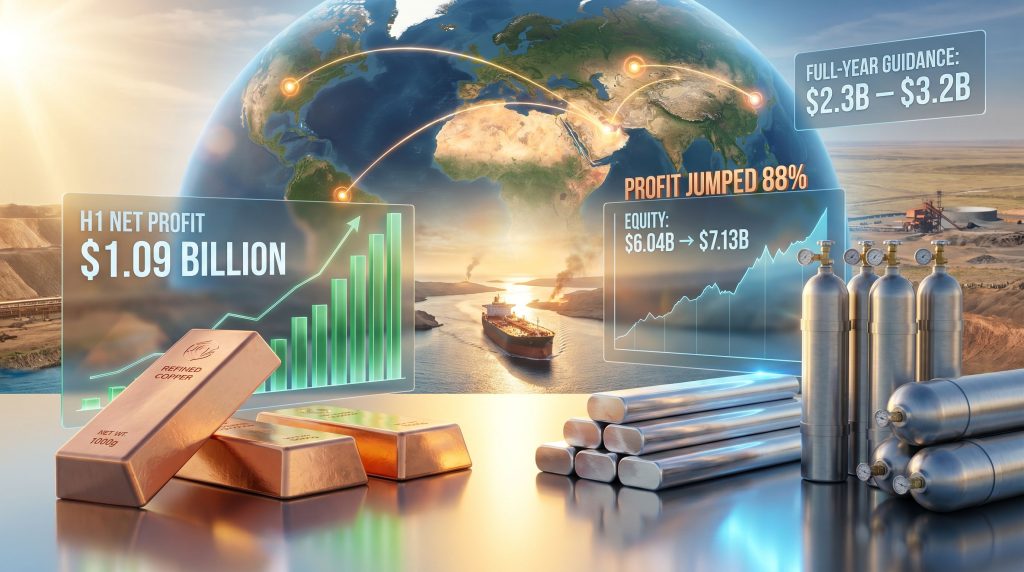

In the first half of the financial year ending March 2026, Mercuria first-half profit jumped 88% on commodity shocks, with the firm recording a net profit of $1.09 billion — representing the second-best first-half result in the company's two-decade history. The figure is not a product of a single market event. It reflects the compounding effect of simultaneous disruptions across oil, gas, metals, and power markets, a convergence that is becoming less of an anomaly and more of a defining feature of the current decade.

When big ASX news breaks, our subscribers know first

Understanding the Mechanics Behind Mercuria's First-Half Profit Jumping 88% on Commodity Shocks

Before examining the specific drivers, it is worth understanding how physical commodity trading houses generate profits in the first place, because the mechanism is fundamentally different from how financial traders or mining companies operate.

Physical commodity traders do not simply bet on price direction. Their profits emerge from a more nuanced set of activities:

- Location arbitrage: Buying a commodity in one region where it is priced lower and selling it in another where it commands a premium, with the difference covering logistics costs and generating margin.

- Temporal arbitrage: Purchasing commodities at spot prices and storing them for delivery at a higher future price, capturing the spread between prompt and forward markets.

- Quality and specification spreads: Managing differences in crude oil grades, metal purities, or gas specifications across counterparties and contracts.

- Financing and prepayment structures: Providing capital to producers in exchange for offtake rights at below-market prices, then selling into open markets at full price.

When supply routes are disrupted by conflict, sanctions, or infrastructure failure, the price differentials between regional markets widen dramatically. Commodity trading giants with established global logistics networks, pre-positioned inventory, and long-standing counterparty relationships are structurally positioned to capture these spreads at a scale unavailable to smaller participants.

The Commodity Shocks That Drove the Result

Mercuria's first-half performance was shaped by a cluster of distinct but overlapping market dislocations. Each created its own profit opportunity, and their simultaneous occurrence amplified the overall outcome.

Commodity Shock Summary:

| Commodity | Disruption Event | Trading Opportunity |

|---|---|---|

| Crude Oil and Brent | Hormuz Crisis, Iran-US-Israel conflict | Supply route disruption, price volatility |

| Aluminum | Middle East conflict affecting regional production | Regional price dislocations |

| LNG | Hormuz closure risk | Supply rerouting, storage arbitrage |

| Copper | US tariff-driven import arbitrage | Cross-regional price spread capture |

| Natural Gas and Power | January 2026 extreme cold event | Spot price spikes, storage premiums |

The Hormuz Crisis and Its Ripple Effects

The conflict involving the United States, Israel, and Iran introduced significant uncertainty into oil and gas markets. The Strait of Hormuz handles roughly 20% of global oil trade and approximately 17% of global LNG trade, making it one of the most strategically sensitive chokepoints in the world. Even the perception of a potential closure is sufficient to widen price spreads, incentivise alternative routing, and trigger storage accumulation by end users.

It is notable that Mercuria's first-half reporting period only captured approximately one month of volatility directly attributable to the conflict. The full earnings impact of sustained Hormuz uncertainty would likely be reflected in subsequent reporting periods. This is partly why CEO Marco Dunand's guidance at an April 2026 conference pointed toward returns at the upper end of the firm's historic 25% to 50% return-on-equity range, implying full-year profits of between $2.3 billion and $3.2 billion.

Aluminum and Middle East Production Exposure

Less widely discussed than oil, but equally significant for commodity traders, is the Middle East's growing role as an aluminium producer. Countries such as the UAE and Bahrain operate large smelting operations reliant on cheap natural gas feedstock. Conflict-related uncertainty affecting energy supply to these facilities, or disrupting shipping routes through the Gulf, creates regional aluminium price dislocations that traders can exploit through arbitrage between Middle Eastern, European, and Asian markets.

Furthermore, the broader geopolitical metals landscape continues to evolve rapidly, adding structural complexity to what were once relatively predictable supply chains.

The US Copper Arbitrage

The tariff environment in the United States created a compelling and recurring arbitrage opportunity in copper throughout the first half of 2026. The US copper tariff impact has been particularly significant, as when the US copper price trades at a sustained premium to the London Metal Exchange benchmark, traders are incentivised to physically move copper inventories toward US delivery points.

This cross-regional spread capture has been described by market participants as one of the most consistently profitable metals trading plays of recent years, benefiting firms with the physical logistics infrastructure to execute it efficiently.

January's Gas and Power Freeze

Extreme cold events in January 2026 created sharp, short-duration spikes in natural gas and electricity prices across multiple markets. While these events are relatively brief, they are highly profitable for traders holding storage capacity or flexible supply positions. The ability to sell gas from storage into a tight winter spot market at multiples of the acquisition cost represents exactly the type of asymmetric payoff that physical commodity trading is structured to capture.

Mercuria's Financial Position: A Closer Look at the Numbers

The headline profit figure tells only part of the story. The broader balance sheet dynamics reveal a company in active expansion mode.

Key Financial Metrics (H1 Financial Year to March 2026):

| Financial Metric | Value | Context |

|---|---|---|

| H1 Net Profit | $1.09 billion | Second-best first-half result in company history |

| Group Equity (March 2026) | $7.13 billion | Up from $6.04 billion at end of September 2025 |

| Advances and Loans | $5.09 billion | 75% increase during the first half |

| H1 Taxation | $226 million | Reflects significant underlying profitability |

| Projected Annual ROE | Upper end of 25-50% range | Per CEO guidance at April 2026 conference |

| Implied Full-Year Profit Range | $2.3B to $3.2B | Based on CEO equity return guidance |

The 75% increase in advances and loans to $5.09 billion is among the most revealing data points in the entire result. This growth does not reflect passive balance sheet expansion. It represents deliberate capital deployment into prepayment structures and financing arrangements that give Mercuria preferential offtake rights over physical commodity flows.

The decision to withhold dividends during this period, departing from the distribution-heavy approach taken after the 2022–2023 profit cycle, signals a strategic preference for compounding the equity base rather than returning capital. With equity growing from $6.04 billion to $7.13 billion in just six months, the reinvestment thesis appears to be gaining traction internally.

Prepayment Financing: The Hidden Engine of Modern Commodity Trading

One of the least understood but most structurally important aspects of Mercuria's business model is its use of prepayment financing as a growth mechanism. The $1.2 billion commitment to help finance the buyout of a copper mining company in Kazakhstan is a textbook example of how large trading houses convert capital into privileged commodity access.

In a prepayment deal, the trading house provides upfront capital to a producer or acquirer in exchange for the right to purchase future output at agreed pricing terms, typically at a discount to market. The structure benefits producers who need financing and cannot or prefer not to access traditional debt markets. It benefits the trading house by securing a long-term, below-market commodity supply that can be sold into higher-priced markets.

This model is increasingly common across the sector for several reasons:

- Banking sector retreat: Regulatory changes since 2015 have reduced the willingness of large banks to provide commodity-backed lending, creating a financing gap that trading houses have stepped in to fill.

- Geopolitical complexity: In regions such as Kazakhstan, Venezuela, and parts of Africa, securing commodity access requires relationship capital and risk tolerance that banks are unwilling to provide.

- Vertical integration benefits: Owning or financing upstream assets gives trading houses better market intelligence, earlier access to commodity flows, and reduced reliance on open-market procurement.

Mercuria's acquisition of an oil refinery and petrol station network in Argentina, combined with bulk commodity purchase agreements in Venezuela, reflects this same logic applied across different geographies and commodity types.

Mercuria vs. Trafigura: Sector-Wide Profit Dynamics

Mercuria's result does not exist in isolation. Trafigura Group, one of its closest direct competitors in scale and business model, reported profits exceeding $4 billion for its own first half to March 2026. The comparison is instructive.

| Trading House | H1 2026 Profit | Primary Profit Drivers |

|---|---|---|

| Mercuria | $1.09 billion | Hormuz crisis, copper arbitrage, gas freeze |

| Trafigura | Over $4 billion | Hormuz crisis, oil volumes, metals |

Trafigura's significantly larger absolute result reflects differences in overall scale, commodity mix, and the proportion of its business exposed to crude oil volumes. Both results, however, confirm a shared underlying dynamic: the commodity trading sector is experiencing its second major profit supercycle within four years.

Moreover, the drivers this time are rooted in geopolitical fragmentation rather than pandemic-era demand shocks, and commodity market volatility appears set to remain a defining feature of the operating environment for the foreseeable future.

The distinction matters for anyone trying to assess the durability of these profits. Pandemic dislocations were, by definition, temporary. Geopolitical fragmentation, by contrast, appears to be a multi-year structural condition with no clear resolution timeline.

The next major ASX story will hit our subscribers first

What Separates Top-Tier Commodity Traders From Mid-Tier Competitors?

The 2026 profit environment has been highly lucrative, but the benefits are not evenly distributed across the trading industry. Several factors determine whether a firm can fully capture the value created by commodity market dislocations:

- Global logistics infrastructure: The ability to physically reroute commodity flows at short notice requires owned or contracted shipping, storage, and port access across multiple continents.

- Balance sheet strength: Prepayment deals, storage accumulation, and arbitrage positions all require significant upfront capital. Firms with larger equity bases can take larger positions.

- Counterparty network depth: In disrupted markets, the ability to transact quickly depends on pre-established relationships with producers, refiners, utilities, and governments.

- Information asymmetry: Physical traders with boots on the ground in producing regions often have access to supply and logistics intelligence before it is reflected in market prices.

Mid-tier trading firms without these structural advantages may participate in some of the same markets but are typically unable to capture the compounding benefits that firms like Mercuria and Trafigura extract from simultaneous multi-commodity disruptions.

The Broader Implication: Supply Chain Fragility as a Permanent Feature

Perhaps the most significant takeaway from Mercuria first-half profit jumping 88% on commodity shocks is what it reveals about the structural condition of global commodity supply chains. The fact that a single six-month period can generate nearly $1.1 billion in net profit from supply disruptions across five distinct commodity classes simultaneously suggests that the world's resource supply architecture is operating with far less redundancy than it did a decade ago.

Consequently, the impact of tariffs on supply chains compounds these existing vulnerabilities, creating further dislocation that well-capitalised physical traders are structured to exploit. The combination of geopolitical conflict, trade tariff escalation, climate-driven weather events, and chronic underinvestment in commodity infrastructure creates a persistent backdrop against which large traders are structurally advantaged.

Each new disruption is an opportunity. In a world where disruptions are becoming more frequent rather than less, the business model that Mercuria and its peers have refined over decades is arguably more relevant now than at any point in the industry's history.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forward-looking statements, including profit guidance and return-on-equity projections, involve inherent uncertainty. Readers should conduct independent research before making any investment decisions.

Want To Profit From The Next Major Commodity Discovery Before The Market Reacts?

As geopolitical fragmentation continues to reshape global commodity markets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly turning complex commodity data into actionable investment opportunities — explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.