June 9, 2026

Africa's Uranium Moment: Why the Global Nuclear Revival Is Rewriting the Continent's Resource Map

For decades, nuclear energy operated in a kind of geopolitical purgatory. The promise of clean, reliable baseload power was perpetually overshadowed by the memory of Chernobyl and, more recently, the triple meltdown at Fukushima Daiichi in March 2011. That single event triggered a cascade of reactor shutdowns across Japan, a wave of policy reversals in Europe, and a uranium price collapse that froze development pipelines globally for the better part of a decade.

Fast forward to 2026, and the calculus has changed dramatically. Governments across Asia, Europe, and North America are treating nuclear energy not as a liability but as an indispensable tool for meeting decarbonisation targets without sacrificing grid reliability. More than 60 reactors are currently under construction worldwide, and long-term utility contracting cycles are drawing uranium demand projections sharply upward through the 2030s.

The structural gap between primary mine production and reactor fuel requirements is tightening in ways that have revived interest in uranium projects that were commercially unthinkable just a few years ago. Furthermore, uranium supply-demand volatility continues to shape how these projects are financed and prioritised globally.

Nowhere is this revival more consequential than in sub-Saharan Africa, where Tanzania's Mkuju River uranium project is now moving from years of dormancy into active development. What was once frozen by a global price collapse is now being thawed by a convergence of energy policy, geopolitics, and capital that few analysts predicted this rapidly.

When big ASX news breaks, our subscribers know first

The Mkuju River Uranium Project: Location, Scale, and What Makes It Distinctive

Where Is the Project Located and Why Does Geography Matter?

The Mkuju River uranium project sits within the Namtumbo District of Tanzania's Ruvuma Region in the country's far south. This remote corridor presents both opportunity and complexity. On one hand, the region hosts the Nyota uranium deposit, the project's primary resource and one of the more significant undeveloped uranium assets in sub-Saharan Africa.

On the other hand, the project operates in close proximity to the Selous Game Reserve, a UNESCO World Heritage Site recognised as one of Africa's largest protected wildlife ecosystems, which creates a layer of environmental scrutiny that accompanies every phase of development.

The logistical realities of operating in southern Tanzania are significant. Transportation infrastructure, power supply, and water management systems all require purpose-built solutions in a region that lacks the industrial corridor development found in more established mining jurisdictions. These are not insurmountable obstacles, but they are factors that materially shape the project's capital requirements and development timeline.

Core Project Parameters at a Glance

| Parameter | Detail |

|---|---|

| Project Location | Namtumbo District, Ruvuma Region, Tanzania |

| Primary Deposit | Nyota uranium deposit |

| Estimated Annual Production Capacity | Up to 3,000 tonnes of uranium per year |

| Total Project Valuation | Approximately USD $1 billion |

| Operating Entity | Mantra Tanzania Ltd. |

| Corporate Parent | Uranium One Group |

| Ultimate Controlling Entity | Rosatom State Atomic Energy Corporation (Russia) |

| Pilot Plant Commissioned | July 2025 |

| Main Plant Construction Commencement Target | Q1 2026 |

| Projected Full Commissioning | 2029 |

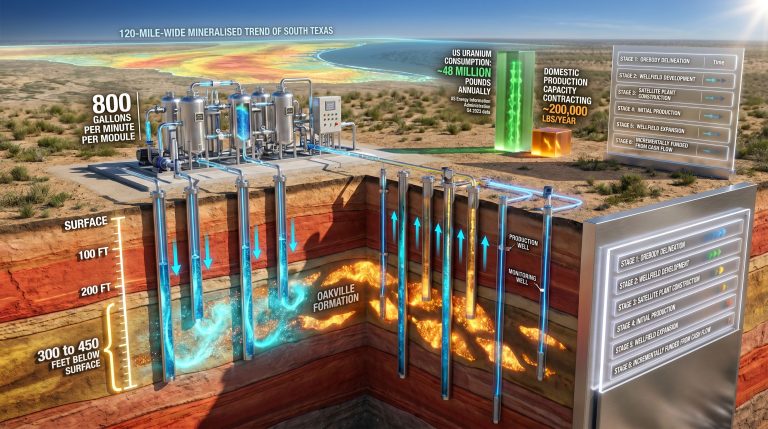

At its projected capacity of up to 3,000 tonnes of uranium per year, Mkuju River would represent a material addition to global uranium supply. For context, Namibia's Husab Mine, which is among Africa's largest operating uranium facilities, produces in the range of 5,000 tonnes annually. The Mkuju River project would therefore not be a marginal contributor but a production centre of comparable regional significance.

The Nyota Deposit: Technical Characteristics

The Nyota deposit forms the geological foundation of the entire project. Uranium mineralisation at Nyota is associated with sandstone-hosted roll-front style deposits, a deposit type that is amenable to conventional hydrometallurgical processing methods, including acid leaching circuits. This processing pathway was specifically validated during the pilot plant commissioning phase in July 2025.

Roll-front uranium deposits are generally well understood from a metallurgical standpoint, which reduces processing risk relative to more complex polymetallic or structurally hosted uranium styles. The pilot uranium processing plant launched in Tanzania generated site-specific performance data under actual ore conditions — a critical step that separates preliminary project studies from bankable engineering design.

The commissioning of a pilot processing plant is a pivotal de-risking milestone in uranium project development. It transforms laboratory-scale metallurgical assumptions into real-world processing parameters, providing the engineering certainty needed to finalise industrial plant design and attract project financing.

Who Controls the Mkuju River Project? Understanding the Rosatom–Uranium One Structure

The Corporate Hierarchy and Its Strategic Implications

The Mkuju River uranium project is operated by Mantra Tanzania Ltd., which functions as a subsidiary of Uranium One Group. Uranium One Group is itself ultimately controlled by Rosatom, Russia's state atomic energy corporation. This ownership structure is not incidental. It fundamentally shapes the project's capital access, risk tolerance, and strategic objectives in ways that distinguish it sharply from privately funded mining ventures.

Rosatom is one of the few entities globally that operates across the complete nuclear fuel cycle, from uranium mining and conversion through fuel fabrication, reactor construction, and even spent fuel management. Securing upstream uranium assets in Africa is therefore not simply a mining investment for Rosatom. It is a vertical integration strategy that strengthens Russia's capacity to deliver comprehensive nuclear fuel supply solutions to the growing number of nations building or planning nuclear power plants.

This distinction matters enormously for understanding the project's resilience to price volatility. A privately funded mining company with shareholders demanding near-term returns might have permanently abandoned Mkuju River during the post-Fukushima price trough. A state-backed entity with a 30-year strategic horizon and an institutional interest in the project's uranium output has entirely different threshold economics. In addition, understanding uranium market dynamics helps contextualise why state-backed operators behave so differently from privately listed mining companies.

Russia's Broader African Nuclear Strategy

Rosatom's engagement in Tanzania does not exist in isolation. Russia has actively pursued nuclear cooperation agreements across Africa, including reactor construction commitments in Egypt, South Africa, and several other nations. The logic is straightforward: as African governments increasingly pursue nuclear energy as part of their long-term electricity strategies, controlling both the reactor technology and the upstream fuel supply creates a powerful commercial and geopolitical position.

Tanzania's Mkuju River project therefore functions as one node within a larger strategic architecture. The uranium produced at the Nyota deposit could, in theory, feed into reactor fuel fabrication processes that serve both Russian domestic reactors and the growing portfolio of Rosatom-designed reactors being built or planned internationally.

What Caused a Decade-Long Freeze? The Fukushima Effect on Global Uranium Markets

How a Japanese Disaster Halted a Tanzanian Mining Project

The mechanism connecting Japan's 2011 Fukushima Daiichi nuclear accident to the suspension of a uranium project in southern Tanzania illustrates the extraordinary interconnectedness of global commodity markets. When the disaster triggered the shutdown of Japan's entire nuclear fleet, totalling approximately 50 reactors, the country's utilities immediately ceased purchasing uranium. Japan had been one of the world's largest uranium consumers, and its sudden withdrawal from the market removed a massive source of demand.

Other countries compounded the effect. Germany accelerated its nuclear exit, Switzerland announced a phase-out, and investor sentiment toward nuclear energy turned sharply negative globally. The uranium spot price, which had traded near $70 per pound in the pre-Fukushima period, began a prolonged collapse that eventually bottomed at approximately $18 per pound in 2016 and 2017.

At those price levels, the economics of developing a new uranium mine in remote southern Tanzania, with all the associated infrastructure requirements, were simply untenable. Mkuju River had completed exploration, defined its resource base, and secured the necessary regulatory approvals. It had done everything right from a technical development standpoint. However, commodity markets do not reward technical readiness when the underlying price signal is absent.

The 2017 Development Pause and the Art of Strategic Patience

A formal pause in active development activity was implemented in 2017, reflecting the commercial reality that advancing the project would destroy rather than create value at prevailing uranium prices. This type of strategic dormancy is a recognised option in the mining industry, particularly for assets with long mine lives and state-backed ownership structures that can absorb holding costs without the existential pressure facing publicly listed juniors.

The critical insight here is that Mkuju River did not lose its resource or its regulatory position during the dormancy period. The uranium remained in the ground. The approvals remained valid. What changed was simply the market context, and that context has now shifted decisively.

The Recovery Drivers: What Changed After 2020?

The uranium price recovery from its 2016–2017 trough has been driven by a combination of supply-side contractions and demand-side growth. Consequently, the uranium market deficit that has emerged creates compelling conditions for previously dormant projects to re-enter active development:

-

Supply discipline: Several major uranium producers curtailed output during the price trough, including significant production reductions from Cameco and Kazatomprom, tightening available supply.

-

Inventory drawdowns: Utilities that had been running down existing uranium stockpiles rather than contracting at spot prices gradually exhausted this buffer, returning to the market as active buyers.

-

Policy reversals: Countries including Japan, South Korea, and several European nations began reversing or moderating previous nuclear phase-out policies as the difficulty of replacing firm baseload power with intermittent renewables became apparent.

-

New demand centres: China's nuclear build programme has continued at pace, adding significant long-term uranium demand from a country with limited domestic uranium resources.

-

Small Modular Reactor programmes: The advancement of SMR technology in the United States, Canada, and the United Kingdom has created a new category of prospective uranium demand beyond conventional large-scale reactor builds.

Development Progress: Where Mkuju River Stands in Mid-2026

The Pilot Plant Milestone and What It Actually Proved

The commissioning of a pilot uranium processing facility in July 2025 by Tanzanian President Samia Suluhu Hassan was more than a ceremonial event. In the context of uranium project development, a successfully operating pilot plant signals that the project has crossed a critical technical threshold.

Specifically, the pilot facility was designed to accomplish two objectives. First, it validated the hydrometallurgical processing approach selected for the Nyota ore, confirming that the chosen chemistry and equipment configuration could reliably extract uranium at acceptable recoveries. Second, it generated the site-specific engineering data required to finalise the design of the full industrial complex. Without this data, an industrial plant design would rest on assumptions that could prove costly if wrong at scale.

Tanzania's Minister of Minerals, Anthony Mavunde, characterised the pilot plant activation as concrete evidence that the project had moved decisively beyond the planning stage, with visible operational activity already underway at the project site.

Infrastructure Tendering and Site Mobilisation

The commencement of competitive bidding for infrastructure development at the Mkuju River site represents the next concrete phase of advancement. Infrastructure packages typically encompass:

-

Haul roads and access infrastructure connecting the mine site to regional transport networks

-

Water management systems addressing both operational process water requirements and environmental compliance obligations

-

Power supply solutions capable of supporting continuous industrial operations

-

Tailings storage facilities designed to international safety and environmental standards

-

Worker accommodation and site services infrastructure

The fact that early-stage mining activities have already commenced within the existing regulatory framework, as confirmed by Minister Mavunde, indicates that the project is not merely advancing on paper but has tangible operational momentum on the ground.

The Roadmap to Full Production

The development sequence for the Mkuju River uranium project follows a structured four-phase pathway:

-

Phase 1 (Completed): Exploration campaigns, resource definition drilling, geological modelling, and procurement of all necessary regulatory approvals.

-

Phase 2 (Completed, July 2025): Pilot processing plant construction, commissioning, and technology validation against site-specific ore characteristics.

-

Phase 3 (Underway, 2026): Infrastructure tendering, contractor mobilisation, site preparation earthworks, and commencement of main industrial plant construction.

-

Phase 4 (Target, 2029): Full industrial-scale processing plant commissioning and commencement of commercial uranium production at nameplate capacity.

The St. Petersburg Forum Visit: Diplomatic Signal or Operational Catalyst?

What High-Level Engagement Actually Means for Project Advancement

President Samia Suluhu Hassan's attendance at the St. Petersburg International Economic Forum (SPIEF) in June 2026, where she participated in the plenary session alongside Russian President Vladimir Putin, carries significance beyond diplomatic optics. For a project of this scale, where the operating entity is a subsidiary of a Russian state corporation, sustained high-level political engagement between the two governments serves multiple practical functions.

It reinforces the bilateral commitment that underpins financing discussions. It signals to technical teams and contractors that the project has the sustained political backing needed to see through a multi-year construction programme. And it creates the kind of governmental momentum that accelerates the resolution of regulatory, logistical, and commercial bottlenecks that inevitably arise during major resource project development.

Minister Mavunde emphasised, ahead of the presidential visit, that bilateral discussions had strengthened both nations' resolve to advance the project, reaffirming that Tanzania's ambition to rank among Africa's leading uranium producers remained firmly on track.

Distinguishing Diplomatic Momentum from Operational Progress

A sophisticated reading of the project's status requires distinguishing between what diplomacy signals and what operational data confirms. The two are not equivalent:

| Indicator Type | Current Status |

|---|---|

| High-level diplomatic engagement | Confirmed (SPIEF, June 2026) |

| Pilot plant commissioned and operating | Confirmed (July 2025) |

| Infrastructure tendering commenced | Confirmed (early 2026) |

| Early-stage mining underway | Confirmed by Minister Mavunde |

| Main plant construction commenced | Targeted Q1 2026, active phase |

| Full commercial production | Targeted 2029, subject to execution |

The operational indicators align with the diplomatic narrative, which is a more reassuring picture than diplomatic signalling unsupported by on-the-ground progress. However, prudent analysis requires acknowledging that the path from construction commencement to full commissioning in 2029 remains subject to execution risk, global uranium price movements, and the practical challenges of building industrial infrastructure in a remote East African location.

The next major ASX story will hit our subscribers first

Environmental Complexity: The Selous Ecosystem and Tanzania's Regulatory Framework

A UNESCO World Heritage Site as a Neighbouring Stakeholder

The Selous Game Reserve occupies a unique position in global conservation. Covering approximately 54,000 square kilometres, it is one of the largest protected wildlife areas on Earth and holds UNESCO World Heritage designation recognising its outstanding universal ecological value. The Mkuju River project's location within the broader Selous ecosystem creates environmental management obligations that are substantially more demanding than those faced by uranium projects in less ecologically sensitive jurisdictions.

Key environmental considerations include:

-

Groundwater protection: The Ruvuma River catchment system connects the project site to broader hydrological networks that support wildlife and communities across a wide area. Any contamination pathway through groundwater would have consequences well beyond the immediate project boundary.

-

Wildlife corridor integrity: Industrial development in the project corridor must account for the movement patterns of wildlife species dependent on the broader Selous ecosystem, requiring careful infrastructure siting and operational management.

-

Tailings containment: Uranium processing generates radioactive tailings that require engineered long-term containment. The design and ongoing monitoring of tailings storage facilities in close proximity to a World Heritage ecosystem carries heightened scrutiny.

Comparing Environmental Challenges Across African Uranium Operations

| Operation | Country | Primary Environmental Challenge | Management Approach |

|---|---|---|---|

| Mkuju River (Nyota) | Tanzania | Proximity to Selous UNESCO ecosystem | EIA compliance, buffer zone management, catchment protection |

| Husab Mine | Namibia | Acute water scarcity in arid environment | Desalination infrastructure, water recycling systems |

| Rössing Mine | Namibia | Long-duration tailings management | Engineered tailings storage, long-term monitoring programmes |

| Somair/Cominak | Niger | Community impacts, dust management | Resettlement frameworks, dust suppression infrastructure |

Tanzania's regulatory framework for uranium mining, established under the Mining Act and associated environmental legislation, requires comprehensive Environmental Impact Assessment prior to major project phases, with ongoing monitoring obligations that persist throughout the operational life of the project.

Economic Significance: What Full Production Would Mean for Tanzania

Quantifying the Development Impact

At full operational capacity, the Mkuju River uranium project is expected to generate several categories of economic benefit for Tanzania:

-

Direct employment: Construction phase workforce requirements are typically substantial for projects of this scale, with operational phase employment providing longer-term job creation in a region with limited alternative industrial employment.

-

Export revenue: Annual production of up to 3,000 tonnes of uranium at market prices would represent a meaningful contribution to Tanzania's export earnings, with the magnitude depending on prevailing uranium spot and contract prices at the time of production.

-

Infrastructure catalysis: The investment required to build haul roads, power supply, and water management systems for the mining operation creates infrastructure that can serve broader regional development purposes beyond the project's direct footprint.

-

Fiscal revenues: Royalties, taxes, and other government levies associated with large-scale extractive operations contribute to national revenue streams over the project's multi-decade operational life.

Tanzania's Potential Position Among African Uranium Producers

The current African uranium production landscape is dominated by Namibia, where the Husab Mine (controlled by China General Nuclear Power Group) and the historic Rössing Mine (controlled by China National Nuclear Corporation) together account for the majority of continental output. Niger was historically a significant producer but has faced serious disruption following political instability.

At projected Mkuju River capacity, Tanzania could realistically position itself as the third-largest uranium-producing nation in Africa, a significant leap for a country that currently has no commercial uranium production. This ranking would carry both economic and geopolitical weight, establishing Tanzania as a credible participant in global nuclear fuel supply discussions. For further context, Kazakhstan's uranium dominance illustrates how state-backed control of uranium supply can translate into substantial geopolitical leverage.

The concentration of African uranium production in Namibia, combined with Niger's political disruption, creates a structural opening for new producing nations. Tanzania's Mkuju River project arrives at a moment when supply chain diversification has become a priority consideration for utilities and fuel buyers globally.

How Mkuju River Compares to African Peer Projects

The African Uranium Development Pipeline

| Project | Country | Status | Est. Annual Capacity | Key Investor |

|---|---|---|---|---|

| Mkuju River (Nyota) | Tanzania | Construction phase (2026) | Up to 3,000 t/yr | Rosatom / Uranium One |

| Husab Mine | Namibia | Operating | ~5,000 t/yr | CGN (China) |

| Rössing Mine | Namibia | Operating | ~2,000 t/yr | CNNC (China) |

| Letlhakane | Botswana | Development stage | TBC | A-Cap Energy |

| Falea | Mali | Exploration stage | TBC | Various |

What Sets Mkuju River Apart Structurally

Several characteristics distinguish the Mkuju River uranium project from its African peers in ways that are relevant to understanding its development trajectory.

State-backed capital certainty: Unlike privately funded junior mining companies, which are exposed to equity market conditions and investor sentiment cycles, Uranium One Group's integration within Rosatom's corporate structure provides access to patient capital that is not subject to the same short-term return pressures. This is a structural advantage during extended market downturns, as the project's decade-long dormancy without permanent abandonment demonstrates.

Political stability premium: Tanzania's relative political stability compared to uranium-producing peers in the Sahel region, where Niger's production disruption illustrates the consequences of political instability for resource projects, represents a meaningful risk reduction factor for long-term project financing and offtake negotiations.

Processing technology validation: The completion of pilot plant testing at Nyota before full construction commencement reduces metallurgical risk to a degree that distinguishes Mkuju River from projects still in pre-feasibility stages. Furthermore, spot versus term pricing dynamics will play a decisive role in determining the commercial returns the project ultimately achieves once production commences.

Frequently Asked Questions About the Mkuju River Uranium Project

What is the Mkuju River uranium project?

The Mkuju River uranium project is a large-scale uranium mining and processing development located in Tanzania's Ruvuma Region, centred on the Nyota uranium deposit. It is operated by Mantra Tanzania Ltd., a subsidiary of Uranium One Group, which is ultimately controlled by Rosatom, Russia's state nuclear energy corporation. The project is valued at approximately USD $1 billion and targets annual production of up to 3,000 tonnes of uranium.

When Will the Project Reach Full Commercial Production?

The main processing plant was targeted to commence construction in early 2026, with full industrial-scale commissioning projected for 2029. These timelines are subject to construction progress, financing arrangements, and regulatory compliance milestones.

Why Was the Project Dormant for More Than a Decade?

The collapse in global uranium prices following Japan's 2011 Fukushima nuclear disaster rendered the project commercially unviable despite completed exploration and secured regulatory approvals. A formal development pause was implemented in 2017 when spot prices had fallen to economically untenable levels. The subsequent recovery in uranium demand and pricing created the conditions for the project's revival.

What Are the Main Environmental Concerns?

The project's proximity to the Selous Game Reserve, a UNESCO World Heritage Site, creates obligations around groundwater protection, wildlife corridor management, and tailings containment that require rigorous Environmental Impact Assessment compliance and ongoing monitoring under Tanzania's Mining Act regulatory framework.

What Would Full Production Mean for Tanzania's Economy?

At full capacity, the project is expected to generate thousands of direct and indirect jobs, substantial export revenue, and catalyse infrastructure development across the Ruvuma region. Tanzania could potentially rank among Africa's top three uranium-producing nations, significantly elevating its profile in global nuclear fuel supply discussions.

Key Takeaways: Reading the Mkuju River Uranium Project in 2026

The Mkuju River uranium project's current trajectory reflects something more complex than a simple mining revival story. It sits at the intersection of three converging forces: a global uranium market shifting from oversupply to structural deficit, a geopolitical environment in which state-backed resource investment in Africa is intensifying, and a domestic policy context in Tanzania that is increasingly oriented toward extracting value from the country's natural resource endowment.

For investors and energy analysts tracking the uranium supply chain, the project's 2029 commissioning target should be understood as a conditional milestone rather than a guaranteed outcome. The operational indicators as of mid-2026 are genuinely encouraging: the pilot plant has been commissioned, infrastructure tendering is underway, early mining activity is confirmed, and diplomatic engagement at the highest levels has reinforced bilateral commitment to advancement.

The variables that could still alter the timeline include global uranium price volatility, the practical challenges of large-scale construction in a remote East African location, environmental compliance requirements related to the Selous ecosystem, and the financing and contractual arrangements that underpin the main plant construction programme.

What is clear is that the decade-long window when Mkuju River was simply a permitted but dormant asset has closed. The project is in active development, and its progression toward production will increasingly draw scrutiny from utility fuel buyers, environmental monitors, and geopolitical analysts tracking the evolving landscape of African critical mineral supply.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements regarding production timelines, capacity projections, and economic impacts are based on currently available information and subject to material risks and uncertainties. Readers should conduct independent research before making investment decisions related to uranium markets or associated companies.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex resource data into clear, actionable opportunities for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.