June 9, 2026

When Supply Chains Break: The Hidden Architecture of African Mining's Chemical Dependency

Most investors tracking African mining equities focus on commodity prices, ore grades, and operational costs. Far fewer consider the upstream chemical infrastructure that makes extraction physically possible in the first place. Explosives and fertilisers are not glamorous industries, yet they sit at the absolute foundation of the SADC region's mining and agricultural output. When geopolitical shocks strike the global chemical supply chain, the companies that have quietly built resilient procurement architectures do not merely survive — they gain structural competitive advantages that can take years to replicate.

The Omnia special dividend Iran disruption story is really two stories running in parallel: one about a company that made the right supply chain decisions before the crisis hit, and another about what the Middle East conflict has permanently changed in the way African industrial operators think about procurement geography and chemical input security.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz as a Chemical Chokepoint, Not Just an Oil Corridor

Public discourse around the Strait of Hormuz almost exclusively frames it as an energy security issue. The waterway's role as a critical transit corridor for crude oil is well understood. However, what receives far less attention is its function as the primary shipping lane for a significant share of globally traded nitrogen-based chemicals, particularly ammonia.

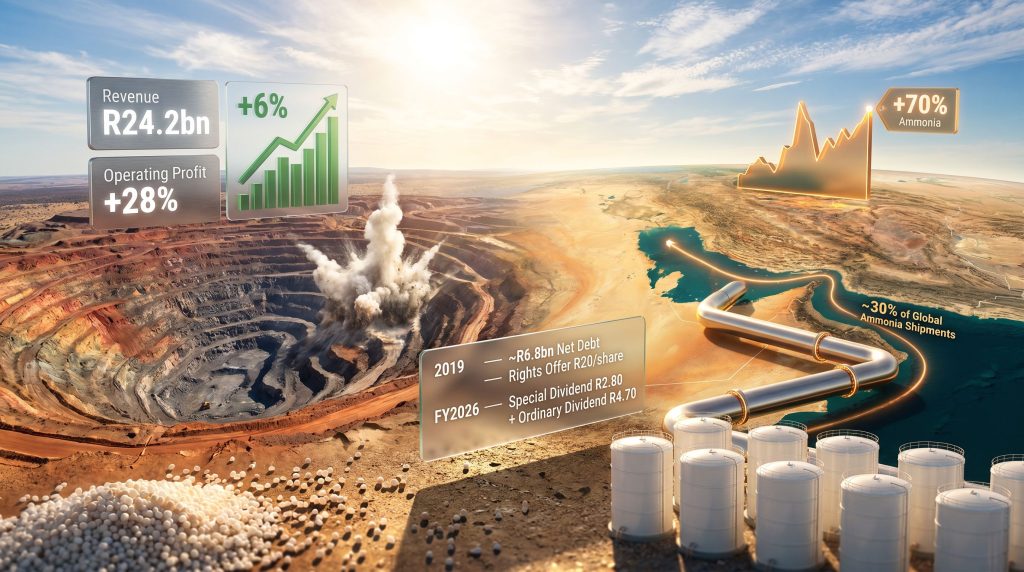

Approximately 30% of all ammonia traded internationally moves through this narrow passage between Iran and Oman. For industries that depend on ammonia as a feedstock — including explosives manufacturers who use it to produce ammonium nitrate, and fertiliser producers who convert it into urea and downstream nitrate compounds — any sustained interruption to this corridor has consequences that extend well beyond energy markets.

In the African context, this dependency is especially acute. The continent's industrial chemical manufacturing base is limited, which means the majority of nitrogen-based inputs must be imported. Sasol produces approximately 400,000 tonnes of ammonia annually within South Africa, providing a partial domestic buffer, but this volume is insufficient to cover the full requirements of major agricultural and mining chemical consumers operating across the SADC region.

The structural import dependency is therefore not a temporary condition — it is a feature of the African chemicals landscape that geopolitical events can exploit. Furthermore, mining geopolitics increasingly shapes how companies across the continent approach procurement resilience, adding another layer of complexity to already challenging supply chains.

Omnia's FY2026 Results: Decoding the Financial Signal

The financial year ended 31 March 2026 captures only one month of active Iran conflict disruption, yet the results reveal how the preceding years of operational restructuring set the platform for an exceptional performance. According to Business Report, the headline figures tell a compelling story of financial transformation.

| Metric | FY2026 Result | Change vs Prior Period |

|---|---|---|

| Revenue | R24.2 billion | +6% |

| Operating Profit | R2.17 billion | +28% |

| Headline Earnings Per Share | 849 cents | +21% |

| Ordinary Dividend Per Share | 470 cents | Up from R4.00 |

| Special Dividend Per Share | 280 cents | First special dividend declared |

The most analytically significant number in this table is not the headline revenue figure. It is the relationship between the 6% revenue increase and the 28% operating profit expansion — a ratio that implies operating profit grew at more than four times the pace of the top line. This kind of operating leverage does not emerge from a single good year. It reflects accumulated margin improvement from years of cost discipline, procurement optimisation, and strategic product mix management across both the agriculture and mining divisions.

Agriculture Division: The Profit Engine Behind the Numbers

The majority of profit growth in FY2026 originated in Omnia's agriculture segment. This is worth examining carefully because it runs counter to the intuitive assumption that a chemicals company exposed to a major input price spike would see margin compression. Instead, the agriculture division demonstrated that when input cost inflation is paired with genuine pricing power and a captive customer base dependent on seasonal crop cycles, the ability to pass through cost increases is structurally embedded in the business model.

African farmers cannot defer fertiliser applications indefinitely. Planting windows are biological constraints, not financial ones, and this inelasticity of demand gives companies like Omnia significant leverage when negotiating price increases with agricultural distributors and end users.

Mining Division: Resilience With Pockets of Pressure

The mining segment, which contributes approximately half of Omnia's total profit, delivered a flat performance relative to the prior period. The headline flatness, however, conceals some important underlying dynamics. Volumes in South Africa's mining operations increased on the back of stronger demand from iron ore and platinum sector customers, contract extensions, and organic growth from existing relationships.

Consequently, what compressed margins was a currency-related headwind in Zambia. The Zambian Kwacha strengthened significantly during the period, creating translation losses that eroded the rand-equivalent value of earnings generated in the copper belt. Zambia copper production is growing, but the financial reporting of that growth through a strengthening local currency can paradoxically suppress reported profitability — a dynamic that underscores how currency risk can overshadow otherwise strong operational results.

Additional offsets came from a downturn in the diamond market, volatility in the coal sector, and the operational disruption caused by above-average rainfall, which reduces blast frequencies at open-cut and surface mining operations.

How Omnia Avoided the Force Majeure Trap

One of the most strategically revealing aspects of the FY2026 reporting period is what did not happen to Omnia. While several of its competitors and chemical suppliers formally declared force majeure in response to the Iran conflict's impact on supply chains, Omnia maintained uninterrupted operations throughout the disruption period.

The mechanism behind this resilience was not luck. According to company commentary at the results presentation, Omnia had already established alternative procurement channels outside the conflict zone before supply conditions deteriorated meaningfully. Simultaneously, the company managed blended inventory positions that provided a buffer against spot market volatility during the period when Hormuz-routed supplies became uncertain.

The ability to blend existing stock with material sourced from alternative origins is a technically straightforward but operationally demanding capability. It requires pre-established relationships with non-Middle Eastern ammonia producers, active logistics management across multiple shipping corridors, and sufficient working capital to hold inventory through periods of elevated spot pricing.

The competitive implication of this is significant. When suppliers and competitors declare force majeure, their customers face supply shortages. Those customers must find alternative sources urgently, often at premium pricing. Companies that can honour existing supply commitments in that environment do not simply retain their customer base — they typically expand it, as distressed buyers seek reliability over price. This dynamic is likely to be visible in Omnia's FY2027 volume data as market share consolidation becomes measurable.

Ammonia at +70%: Understanding the Price Shock Mechanics

The magnitude of the ammonia price movement since the Iran conflict began is worth contextualising carefully for investors unfamiliar with nitrogen chemical markets. As reported by Mining MX, the Omnia special dividend Iran disruption narrative has drawn considerable attention from analysts tracking the knock-on effects across the broader chemicals sector.

| Chemical Input | Price Movement at Conflict Onset | Current Level vs Pre-War Baseline |

|---|---|---|

| Ammonia | +70% at peak | Approximately +50% above pre-conflict levels |

| Urea-derived nitrates | Elevated and sustained | Ongoing upward pressure |

| Oil-linked chemical inputs | Significant increase | Highly volatile |

Ammonia pricing is notoriously responsive to geopolitical and logistical shocks because the commodity has high transport specificity — it requires pressurised or refrigerated handling — and a relatively concentrated export market geography. Unlike many bulk commodities where alternative supply routes are easily substituted, ammonia shipping requires specialised vessels, and rerouting around a blockaded strait adds meaningful freight cost and delivery time.

The critical question for mining sector analysts is whether a sustained 50% premium on ammonia inputs translates into demand destruction for explosives. The industry evidence strongly suggests it does not, for several interconnected reasons:

- Explosives costs represent a small fraction of total mining operating expenditure, typically in the range of single-digit percentages of total blasting costs

- The metals driving current mining activity — including copper, platinum group metals, and iron ore — are experiencing structurally elevated demand from green economy applications and AI infrastructure energy requirements

- Mine operators cannot reduce blast frequency without directly impairing ore production volumes, which creates an immediate revenue consequence that dwarfs any explosives cost saving

- The economics of mine closure and restart are extremely unfavourable, meaning operators absorb input cost increases rather than curtail production

This demand inelasticity is what makes the Omnia business model particularly robust during input cost inflation cycles. Furthermore, the pass-through pricing mechanism functions because customers have no viable substitution option, a dynamic that aligns closely with broader critical minerals demand trends shaping the global resources sector in 2025 and beyond.

The Special Dividend as a Balance Sheet Narrative

For investors who have followed Omnia across multiple business cycles, the declaration of a R2.80 per share special dividend carries a meaning that extends well beyond the cash return itself.

| Period | Financial Position | Capital Action |

|---|---|---|

| 2019 | Approximately R6.8 billion net debt | R20 per share rights offer to raise equity capital |

| FY2026 | Strong cash generation, restructured balance sheet | R2.80 special dividend plus R4.70 ordinary dividend |

In 2019, the company was in a deeply stressed financial position, carrying debt levels that required a dilutive capital raise at a time when management described the circumstances as particularly challenging. Seven years later, the same company is returning surplus capital to shareholders through a special dividend, having already declared an ordinary dividend of R4.70 per share, up from R4.00 in the prior year.

This trajectory represents one of the more complete balance sheet rehabilitation stories in South African industrial company history. Special dividends in capital-intensive industrial businesses are a high-conviction signal precisely because they imply that management is confident the elevated cash generation is not a one-cycle phenomenon. Companies do not typically distribute special dividends when they believe the following year will see cash flow deteriorate sharply.

The next major ASX story will hit our subscribers first

SADC Mining's Non-Negotiable Demand for Explosives

The broader sector-level implication of Omnia's FY2026 performance is what it reveals about the structural character of explosives demand across southern African mining operations.

The company's own framing of its operational priorities is instructive. The view expressed by management is that ensuring uninterrupted supply to mining customers is a primary obligation, not merely a commercial one, because the consequences of supply failure extend to national economic output. Copper extraction in Zambia, iron ore demand trends in South Africa, and platinum group metal mining on the Bushveld Complex are all industries that cannot simply pause blasting operations for weeks while supply chain disruptions resolve themselves.

This framing elevates Omnia's role from a chemical distributor to something closer to critical industrial infrastructure. That positioning has implications for how the company negotiates with customers, how it manages inventory risk, and how it should be valued by investors who understand the non-discretionary nature of its demand base.

Forward Scenarios: Three Pathways for the Iran Disruption

The FY2027 trajectory for Omnia's explosives and fertiliser businesses will be shaped significantly by how the geopolitical situation in the Persian Gulf evolves. Three plausible scenarios frame the range of outcomes, and commodity price impacts will play a pivotal role in determining which trajectory materialises for the broader sector.

Scenario 1: Rapid De-escalation

The Strait of Hormuz returns to full commercial operation. Ammonia prices normalise toward pre-conflict levels over a period of months. Omnia's pass-through pricing advantage narrows, but volume growth accelerates as market conditions stabilise and competitor relationships with customers, damaged by force majeure declarations, take time to repair.

Scenario 2: Prolonged Disruption

Force majeure conditions persist among competing suppliers for an extended period. Omnia consolidates market share through demonstrated supply reliability. Elevated input pricing sustains margin expansion, whilst the company's diversified procurement architecture becomes a recognised and increasingly valued competitive differentiator.

Scenario 3: Escalation and Structural Re-routing

Extended naval disruption forces a permanent restructuring of global ammonia trade geography, with new export corridors through alternative regions gaining commercial scale. Omnia's early investment in non-Hormuz supply relationships positions it to benefit from the emerging trade architecture rather than being caught in a transition period.

In all three scenarios, the company's underlying demand base remains intact. The variable is margin profile and the speed of market share consolidation — not the fundamental need for explosives across African mining operations. The Omnia special dividend Iran disruption episode has, in many respects, crystallised precisely why supply chain resilience commands a premium in the current operating environment.

Key Takeaways for Investors and Industry Observers

- Supply chain diversification has a measurable financial value that only becomes fully visible when geopolitical shocks materialise and competitors are forced to declare force majeure

- The relationship between revenue growth and operating profit growth in FY2026 reveals the depth of operational leverage embedded in Omnia's restructured cost base

- Explosives demand is largely price inelastic relative to moderate input cost increases, particularly when end-market metal prices are supported by green economy and AI infrastructure investment cycles

- Currency dynamics in resource-producing African nations, particularly the strengthening Zambian Kwacha, can create reporting headwinds even when underlying operational performance is strong

- The declaration of a special dividend against the backdrop of the 2019 debt crisis represents a fundamental transformation in the company's financial character, not a cyclical aberration

- The Iran conflict has accelerated a broader reassessment of chemical supply chain geography across the African industrial sector, with lasting implications for how operators structure procurement relationships

This article is for informational purposes only and does not constitute financial advice. Past performance of any company or asset class referenced is not indicative of future results. Investors should conduct their own due diligence and consult qualified financial advisers before making investment decisions. Scenario analysis and forward-looking statements are speculative by nature and subject to significant uncertainty.

Want to Identify the Next Major ASX Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex mineral data into clear, actionable insights for both short-term traders and long-term investors — explore historic discoveries and their exceptional returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.