May 24, 2026

The Hidden Variable Most Gold Investors Keep Getting Wrong

Most financial commentary treats interest rates as a single, self-explanatory number. A rate goes up, gold goes down. A rate falls, gold rises. This shorthand has been repeated so many times across financial media that it has taken on the quality of settled fact. But this framing contains a critical flaw, one that has caused investors to misread gold's behaviour repeatedly across multiple economic cycles.

The variable being overlooked is not obscure or complex. It is simply the distinction between what rates appear to be and what they actually deliver in terms of purchasing power. Understanding this gap is the foundation of any serious analysis of real interest rates and gold.

When big ASX news breaks, our subscribers know first

Why Nominal Rates Tell Only Half the Story

The Fundamental Difference That Changes Everything

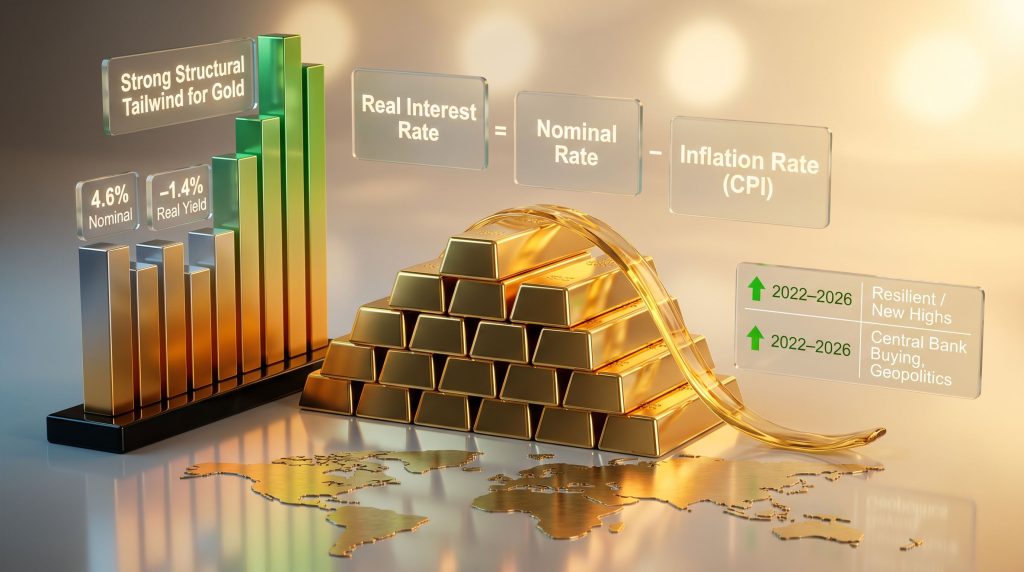

When a central bank announces an interest rate decision, the figure reported is a nominal rate. It is the headline number, the one quoted by news anchors and financial commentators. What it does not account for is inflation. A bond yielding 4.6% sounds attractive in isolation, but if prices across the economy are rising at 3.8% annually, the investor's actual gain in purchasing power is just 0.8%.

This is the real interest rate: the nominal yield minus the prevailing inflation rate. It is the economically meaningful figure because it measures what an investment actually returns after accounting for the erosion of purchasing power. Furthermore, understanding gold and bonds as distinct instruments with different responses to this dynamic is essential for any well-rounded portfolio approach.

The formula is straightforward:

Real Interest Rate = Nominal Rate minus CPI Inflation Rate

For gold investors, this distinction is not academic. It determines the genuine opportunity cost of holding a non-yielding asset. When real rates are high, fixed-income instruments offer meaningful compensation for the risk of holding them. When real rates are low or negative, that compensation shrinks or disappears entirely, and the comparative appeal of gold strengthens considerably.

How to Calculate Real Interest Rates: A Practical Walkthrough

-

Identify the current nominal yield on a benchmark instrument, such as the 10-year US Treasury bond.

-

Source the most recent annual Consumer Price Index (CPI) reading from the Bureau of Labor Statistics.

-

Subtract the CPI figure from the nominal yield to derive the real yield.

-

Interpret the result: a meaningfully positive real yield favours income-generating assets; a near-zero or negative real yield removes the primary competitive advantage bonds hold over gold.

The table below demonstrates how the same nominal yield produces dramatically different real returns depending on the inflation environment:

| Nominal 10-Yr Treasury Yield | CPI Inflation Rate | Real Interest Rate | Implication for Gold |

|---|---|---|---|

| 4.6% | 2.0% | +2.6% | Moderate headwind for gold |

| 4.6% | 3.8% | +0.8% | Minimal opportunity cost; gold competitive |

| 4.6% | 5.0% | -0.4% | Negative real yield; gold highly attractive |

| 4.6% | 6.0% | -1.4% | Strong structural tailwind for gold |

As the table illustrates, the current environment of approximately 4.6% nominal yields and 3.8% CPI produces a real return of just 0.8% on a 10-year Treasury. That is not a compelling reason to abandon gold for fixed income, particularly when the inflation trajectory remains uncertain.

The CPI Problem: Why Official Inflation May Be Understating the True Cost of Living

There is a layer of complexity beneath even the real rate calculation that most mainstream commentary ignores entirely. The Consumer Price Index as currently measured may not accurately reflect the true rate of purchasing power erosion experienced by households. According to research on gold, real interest rates and the US dollar index, the relationship between these variables is more nuanced than headline figures suggest.

The US government revised its CPI measurement methodology during the 1990s, with changes that have been documented to produce systematically lower inflation readings compared to the pre-revision formula. Analysts applying the older methodology to current data have argued that true price inflation could be running at roughly double the official figure. If that assessment has any validity, then with official CPI at 3.8%, the true inflation environment may be closer to 6% or higher.

If real inflation is materially higher than official CPI suggests, then the real interest rate on a 10-year Treasury is not +0.8% as the headline calculation implies. It could be deeply negative. And a deeply negative real yield is among the most structurally powerful environments for gold appreciation that history has recorded.

This is not a fringe position. It is a methodological observation that has been discussed within monetary economics for decades, and it has significant implications for how investors should interpret any real rate calculation that relies on official CPI data.

What History Tells Us About Real Interest Rates and Gold Prices

The Long-Run Inverse Relationship Across Multiple Cycles

The negative correlation between real interest rates and gold is one of the better-documented relationships in commodity markets. Across multiple decades and distinct economic regimes, falling real yields have consistently corresponded with rising gold prices, while rising real yields have tended to suppress gold's appeal. Historically, gold as a safe haven has demonstrated its most compelling performance precisely during these periods of compressed or negative real yields.

The clearest historical example remains the 1970s stagflation era. With oil shocks driving inflation well above nominal interest rates, real yields plunged deep into negative territory. The result was one of gold's most powerful bull markets on record. By the late 1970s, gold had appreciated by multiples from its earlier levels as investors fled the purchasing power destruction embedded in the bond market.

The 2008 to 2011 period provided a more recent confirmation. As the Federal Reserve slashed rates to near zero and launched quantitative easing programmes, real yields collapsed. Gold responded by surging from approximately $800 per ounce in late 2008 to above $1,900 per ounce by mid-2011, a gain of over 130% in roughly three years. Furthermore, gold in recessions has repeatedly demonstrated this pattern of outperformance during periods of monetary expansion.

Conversely, the 2013 to 2018 period saw real yields rise as the Fed began tapering its asset purchases and eventually hiking rates. Gold entered a multi-year bear market and consolidation phase, reinforcing the inverse relationship.

Has the Correlation Weakened Since 2022?

The post-2022 period has introduced a genuine puzzle for analysts who rely primarily on the real rate framework. Despite the most aggressive rate-hiking cycle in decades, with real yields climbing to multi-decade highs, gold did not follow the historically expected playbook. Instead, it showed remarkable resilience and, in numerous periods, continued setting new price records.

Several structural forces have been identified as co-drivers that appear to be partially overriding the traditional rate sensitivity:

- Central bank gold accumulation has reached volumes not seen in decades, with purchases by emerging market institutions creating sustained, price-inelastic demand

- Geopolitical instability across multiple theatres has elevated gold's safe-haven premium independently of yield dynamics

- Active de-dollarisation among sovereign reserve managers has increased structural demand for gold as a neutral reserve asset with no counterparty risk

- Persistent above-target inflation has maintained gold's store-of-value appeal even as nominal yields rose

- Investor diversification away from traditional fixed income has added a portfolio construction dimension to gold demand

The weakening of the gold-real rate correlation does not invalidate the relationship. It signals that gold's price formation has become a multi-variable function where real rates remain a critical input but now share the stage with structural demand forces that were less prominent in prior cycles.

Gold's Behaviour Across Different Real Rate Environments

| Period | Real Rate Direction | Gold Price Trend | Dominant Driver |

|---|---|---|---|

| 1970s | Deeply negative | Strong bull market | Inflation, dollar weakness |

| 2008 to 2011 | Falling to negative | Major bull run | QE, financial crisis response |

| 2013 to 2018 | Rising | Bear market/consolidation | Fed tightening cycle |

| 2020 to 2022 | Negative then rising | Rise then correction | Pandemic stimulus, then rate hikes |

| 2022 to 2026 | Elevated but under pressure | Resilient/new highs | Central bank buying, geopolitics |

The Central Bank Policy Dilemma: Can High Rates Actually Be Sustained?

The Debt Constraint That Changes the Calculation

The mainstream assumption that central banks can maintain elevated interest rates indefinitely deserves serious scrutiny. There is a structural fiscal constraint that complicates this picture considerably.

When government debt levels are high and rising, the cost of servicing that debt escalates sharply as interest rates increase. US government borrowing costs have been climbing sharply in the current environment. As debt servicing consumes an ever-larger share of government revenue, the political and economic pressure to reduce rates or expand the money supply intensifies in ways that can override the inflation-fighting mandate.

This dynamic creates what analysts describe as a structural ceiling on how long or how high rates can realistically remain. The Federal Reserve is already exhibiting signs of this tension, with evidence suggesting that asset purchase activity has resumed in ways that function similarly to quantitative easing, even without being formally labelled as such. When a central bank begins suppressing long-end yields through balance sheet operations, it is effectively acting as a covert real rate suppressor, keeping real yields lower than a free market would otherwise produce.

Three Times the Fed Has Chosen Stimulus Over Inflation Control

History provides a consistent pattern when weighing how central banks behave when financial stability comes under threat. Across three major episodes, the response has been remarkably uniform:

-

The dot-com bust (2000 to 2002): Emergency rate cuts and liquidity injections were deployed as the equity market collapsed and recession risk mounted.

-

The 2008 Global Financial Crisis: Rates were slashed to near zero and quantitative easing was introduced on a scale previously unprecedented in peacetime, prioritising financial system rescue over price stability.

-

The 2020 pandemic shock: Rates were cut to zero within weeks of the crisis emerging, and the Fed's balance sheet expanded to levels that would have been unthinkable a decade earlier.

In each case, the inflation-fighting mandate was subordinated to economic rescue objectives. The pattern is not coincidental. It reflects a structural reality: the consequences of allowing a debt-laden financial system to implode are immediate and politically catastrophic, while the consequences of entrenched inflation are diffuse and slower-moving.

Central banks face a genuine structural dilemma. Sustaining high rates long enough to genuinely defeat inflation risks triggering a debt-driven financial crisis. Prioritising financial stability risks entrenching above-target inflation. The historical record consistently shows which choice tends to win, and gold has been a beneficiary of that pattern each time.

How Quantitative Easing Suppresses Real Yields Even When Rates Appear High

A nuance that escapes most mainstream commentary is the mechanism by which central bank asset purchases depress real yields even during periods when policy rates appear elevated. When a central bank purchases government bonds at scale, it artificially suppresses long-end yields below where market forces would otherwise place them. This keeps the nominal yield lower than it would naturally be, which in turn keeps the calculated real yield lower as well.

Simultaneously, the money created through these purchases can stoke inflation expectations, creating a compounding dynamic: lower nominal yields and higher expected inflation both push real yields downward. For gold, this represents a structurally supportive environment regardless of what the headline policy rate appears to say. Central bank gold buying behaviour during these periods further reinforces this structural support.

The Multi-Driver Framework for Gold in 2026

Central Bank Demand as a Price Floor

One of the most significant structural shifts in the gold market over the past several years has been the scale of central bank accumulation. Purchases by sovereign institutions, predominantly from emerging market economies seeking to reduce dependence on US dollar reserves, have added a layer of demand that is largely insensitive to interest rate dynamics.

This institutional buying creates a de facto price floor in the gold market. Unlike speculative demand, which can reverse quickly in response to changing yield conditions, central bank accumulation is driven by long-term reserve management objectives that do not recalibrate based on quarterly rate movements.

Geopolitical Risk as an Independent Variable

Geopolitical instability, including energy market disruptions, military conflicts, and trade fragmentation, elevates gold's safe-haven premium in ways that operate entirely outside the interest rate framework. Oil price shocks, in particular, carry a secondary effect: they feed through to consumer price inflation, which in turn compresses real yields, creating a compounding tailwind for gold that works through both the safe-haven channel and the real rate channel simultaneously.

De-Dollarisation and the Monetary Architecture Shift

The long-term trend of sovereign reserve managers reducing USD-denominated holdings represents perhaps the most structurally durable demand driver for gold that exists today. Gold in the monetary system has taken on renewed relevance as central banks navigate a fragmenting geopolitical order and seek assets with no counterparty risk.

Gold cannot be frozen by a foreign government, carries no counterparty risk, and is not subject to sanctions. These characteristics make it uniquely attractive to reserve managers operating in an increasingly multipolar world. This demand is price-inelastic in a way that purely financial demand is not, and it will not reverse simply because real yields in the United States move higher by 50 basis points.

Common Misconceptions About Gold and Interest Rates

| Misconception | The More Complete Picture |

|---|---|

| Higher rates are always bad for gold | Only if real rates rise meaningfully; nominal increases absorbed by inflation are neutral or positive for gold |

| Gold has no yield so bonds always win in rate-rising cycles | The relevant comparison is real yield; near-zero or negative real yields eliminate bonds' competitive advantage |

| The Fed can sustain high rates indefinitely | Debt sustainability constraints and historical crisis responses suggest otherwise |

| The gold-real rate relationship is reliable and linear | The relationship has weakened since 2022 as structural demand forces have become dominant co-drivers |

| CPI accurately reflects the opportunity cost of holding gold | Measurement methodology revisions may systematically understate true inflation |

The next major ASX story will hit our subscribers first

A Framework for Evaluating Gold's Attractiveness Against Real Yields

For investors attempting to navigate this landscape, a structured analytical approach is more useful than any single metric. The following five-step process provides a foundation:

-

Identify the nominal yield on the benchmark 10-year government bond and note whether it is rising, falling, or stable.

-

Assess prevailing CPI and consider whether methodological limitations may cause it to understate the true inflation environment.

-

Calculate the real yield and evaluate whether it genuinely compensates for inflation risk and the opportunity cost of not holding income-generating assets.

-

Layer in structural factors, including central bank demand trends, geopolitical risk levels, fiscal sustainability concerns, and de-dollarisation momentum.

-

Apply historical context, identifying which prior macro regime most closely resembles the current environment and examining how gold performed in that analogue.

No single variable determines gold's direction. However, real interest rates and gold remain inseparably linked as analytical concepts, and understanding them accurately requires looking beyond the nominal figures that dominate financial media coverage. For a deeper examination of how these dynamics play out across yield environments, long-term trends in gold versus real yields provide a valuable empirical reference point.

Frequently Asked Questions: Real Interest Rates and Gold

What is the relationship between real interest rates and gold prices?

Gold has historically exhibited a negative correlation with real interest rates. When inflation-adjusted yields on safe assets fall to low or negative levels, the opportunity cost of holding gold diminishes substantially. Conversely, meaningfully positive real yields make income-generating assets more competitive relative to gold.

Why do real rates matter more than nominal rates for gold?

Nominal rates do not account for purchasing power erosion. A 4.6% bond yield in a 3.8% inflation environment delivers just 0.8% in real terms. Gold's appeal as a store of value is evaluated against this real return, not the nominal headline figure.

Has the gold-real rate relationship changed in recent years?

Yes. Since approximately 2022, the historically reliable inverse correlation has become less consistent. Central bank accumulation, geopolitical risk premiums, and de-dollarisation trends have emerged as significant co-drivers that support gold demand independently of the rate environment.

Can the Federal Reserve realistically maintain high interest rates long-term?

Fiscal sustainability constraints create a structural ceiling on how long elevated rates can be maintained. The historical pattern across multiple crisis episodes suggests that when financial stability comes under pressure, central banks have consistently prioritised economic rescue over inflation control.

What happens to gold if real interest rates turn negative?

Negative real yields, where inflation exceeds the nominal bond yield, have historically been among the most powerful environments for gold appreciation. When holding government bonds guarantees a loss in purchasing power, the structural case for gold as an alternative store of value becomes highly compelling.

How does CPI measurement affect the real rate calculation?

If official CPI understates actual price inflation due to methodological revisions implemented in the 1990s, then the true real interest rate is lower than the published figure implies. This means gold's structural attractiveness may be greater than a surface-level calculation would indicate. The LBMA's analysis of gold, real interest rates and the dollar provides further institutional perspective on this relationship.

Disclaimer: This article is intended for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. Forecasts, historical analogues, and analytical frameworks discussed herein involve inherent uncertainty. Investors should conduct their own due diligence and consult a qualified financial adviser before making investment decisions. Gold prices and interest rates can move in unexpected ways, and past performance is not indicative of future results.

Want to Know Which ASX Gold and Mineral Discoveries Are Worth Acting On Right Now?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, cutting through complex data to surface actionable opportunities the moment they are announced — explore historic discovery returns to understand the potential, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.