May 21, 2026

The Metal That Powers Quantum Computing Has No U.S. Mine — Until Now

The global race to secure quantum-age minerals is quietly exposing a supply chain blind spot that has received far less attention than lithium, cobalt, or rare earths. While policymakers debate domestic lithium production and rare earth processing capacity, a smaller but arguably more strategically acute vulnerability has been hiding in plain sight: the United States produces zero rubidium domestically. Not a small amount. Zero.

That structural gap matters because rubidium is not a niche laboratory curiosity. It sits at the functional core of atomic clocks, quantum computing systems, GPS-denied military navigation, and positron emission tomography (PET) scanners used in medical imaging. The U.S. National Institute of Standards and Technology relies on rubidium frequency standards for timekeeping infrastructure accurate to within ±2 × 10⁻¹¹ seconds, a precision that underpins synchronisation across telecommunications, financial markets, and defence networks.

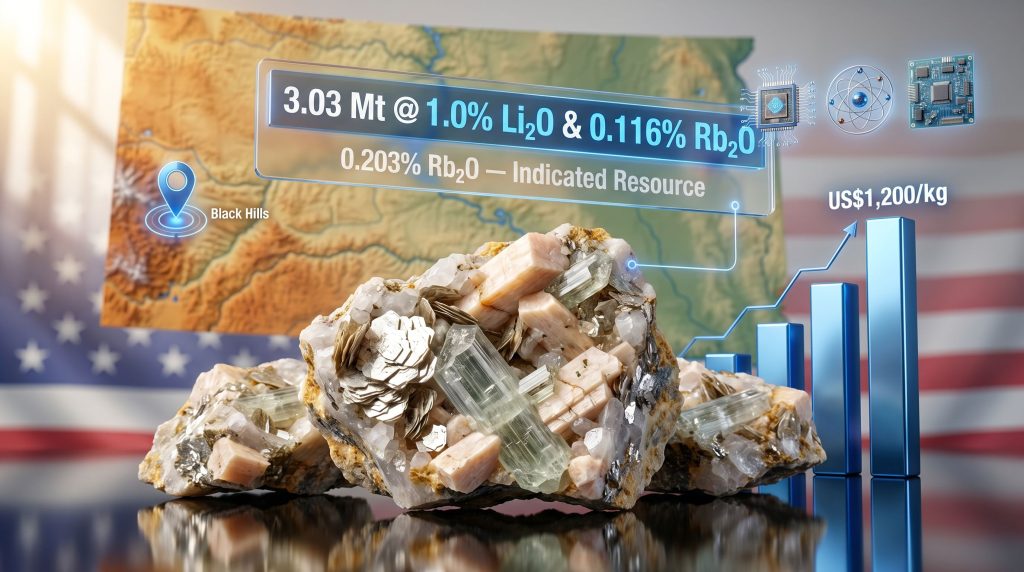

Against this backdrop, a JORC 2012-compliant Mineral Resource Estimate released in late April 2026 for the Iris Metals Beecher rubidium deposit in South Dakota's Black Hills has drawn significant attention from critical minerals analysts and supply chain strategists. The numbers are meaningful. The context is more so.

When big ASX news breaks, our subscribers know first

Why Rubidium Sits in a Different Risk Category to Lithium or Cobalt

Most investors and analysts approach critical mineral supply risk through the lens of volume. Lithium and cobalt are measured in hundreds of thousands of tonnes annually; their supply chains are large, heavily scrutinised, and increasingly subject to domestic development programmes. Rubidium, however, is different in almost every respect.

Global rubidium supply is measured in tonnes per year rather than thousands of tonnes. The metal occurs as a trace element in lepidolite, pollucite, zinnwaldite, and most significantly for the Beecher project context, within potassium feldspar and muscovite in Lithium-Caesium-Tantalum (LCT) pegmatite systems. Because it rarely forms discrete ore minerals of its own, it has historically been treated as an incidental by-product or simply ignored during resource estimation.

That indifference has created a paradox. Rubidium is formally classified as a critical mineral by the U.S. Department of the Interior (Final List of Critical Minerals, 2024), the country imports 100% of its supply according to the U.S. Geological Survey Mineral Commodity Summaries 2024, yet almost no U.S. pegmatite project has ever bothered to formally measure and report its rubidium content under a recognised resource standard.

This is the structural anomaly that makes the Iris Metals Beecher rubidium deposit genuinely novel. It is not simply a lithium project with rubidium mentioned in passing. It is reported as one of the first U.S. mineral resource estimates to formally quantify rubidium under JORC 2012 standards, creating a verifiable, investment-grade framework for assessing the metal's value within the deposit.

"The absence of formal rubidium quantification across most U.S. pegmatite projects does not reflect geological scarcity. It reflects historical indifference to a metal that was not considered commercially relevant. That calculus is now changing rapidly."

Understanding the Beecher Project: Geology, Location, and Land Position

Black Hills Pegmatites: An Established but Underexplored Metallogenic Province

The Black Hills region of western South Dakota has been recognised for its pegmatite mineralisation for over a century. Historical mining records from the USGS and South Dakota Geological Survey document significant pegmatite extraction activity in the region dating back to the early-to-mid twentieth century, with feldspar, mica, and beryllium among the historically extracted commodities.

LCT pegmatites, the geological family to which the Beecher deposits belong, form during the final crystallisation stages of granitic magmas. As a magma cools, lithophile elements concentrate progressively in the residual melt. By the time crystallisation is near-complete, this residual fluid is extraordinarily enriched in lithium, caesium, tantalum, rubidium, and related incompatible elements. The result is a coarse-grained rock with commodity concentrations that can be orders of magnitude above crustal averages.

Crucially for the Beecher story, rubidium's geochemical behaviour is closely analogous to potassium. Because rubidium ions are similar in size and charge to potassium ions, rubidium substitutes readily into potassium-bearing minerals during crystallisation. In a mature LCT pegmatite, this means potassium feldspar and muscovite become the primary rubidium host phases, and their abundance within a pegmatite body directly predicts rubidium enrichment potential. This is not speculative geology; it is a well-documented principle in pegmatite geochemistry.

The Beecher Project itself sits approximately 7 km from the township of Custer, South Dakota, across a total footprint of 50.88 hectares of private patented mining claims, supplemented by surrounding Bureau of Land Management federal claims. The patented claim status is operationally significant because it provides greater land tenure security and permitting flexibility compared to unpatented federal mineral claims.

The Three-Deposit Architecture: Longview, Black Diamond, and Beecher Lode

How Do the Three Deposits Compare?

The resource base at Beecher is distributed across three distinct LCT pegmatite bodies, each with individual structural characteristics that contribute differently to the overall resource profile. Understanding the mineral deposit tiers of each body is essential to evaluating the project's full potential.

| Deposit | Strike Length | Width (max) | Primary Characteristics |

|---|---|---|---|

| Longview | 520 metres | Not individually reported | Largest deposit; primary rubidium concentration zone; hosts shallow high-grade rubidium |

| Black Diamond | 650 metres | 115 metres | Widest deposit; southern zones carry elevated rubidium grades |

| Beecher Lode | Smaller scale | Not individually reported | Third LCT pegmatite; contributes to multi-deposit resource base |

The combined strike length across all three deposits approaches 2 kilometres, providing meaningful lateral extent and suggesting that the current resource footprint retains genuine expansion potential through step-out drilling. Geologically, the consistency of LCT-type mineralisation across three separate pegmatite bodies within a defined district indicates a shared magmatic-hydrothermal source, rather than isolated occurrences, which improves geological confidence in resource continuity.

It is also worth noting that LCT pegmatites often carry prospective concentrations of tantalum and beryllium alongside their primary lithium-rubidium assemblages. Both metals are separately designated as critical mineral uses are well-established across defence and advanced manufacturing sectors. This raises the theoretical possibility of a multi-commodity resource base at Beecher beyond lithium and rubidium alone, though this remains exploratory at this stage.

Dissecting the Updated JORC 2012 Mineral Resource Estimate

Total Resource, Grades, and Classification

The updated Mineral Resource Estimate for the Iris Metals Beecher rubidium deposit, reported in late April 2026 and prepared under JORC 2012 standards, establishes the following headline parameters:

- Total resource: 3.03 million tonnes

- Average lithium grade: 1.0% Li₂O (approximately 0.47% Li metal)

- Average rubidium grade: 0.116% Rb₂O (approximately 0.108% Rb metal)

- Cut-off grade: 0.5% Li₂O

- Classification: Indicated and Inferred categories

JORC 2012 compliance is the standard adopted by the Australian Securities Exchange and recognised by international capital markets as a robust framework for resource reporting. The classification of resources into Indicated and Inferred categories reflects geological confidence levels. For project financing, study work, and economic assessment purposes, Indicated resources carry substantially more weight.

The High-Grade Rubidium Zone: Where Economics Concentrate

Within the broader resource, a high-grade rubidium zone sits entirely within the Indicated category, providing a higher-confidence subset with materially stronger economic characteristics:

- Indicated high-grade zone: 1.04 million tonnes at 0.203% Rb₂O

- In-situ rubidium oxide content: approximately 2,100 tonnes

- Metal equivalent: approximately 1,960 tonnes of rubidium metal

The grade premium within this zone is substantial. At 0.203% Rb₂O, the high-grade zone is approximately 75% above the whole-of-resource average of 0.116% Rb₂O. In the context of a by-product recovery model, this concentration matters enormously: processing costs are largely fixed per tonne of ore treated, so higher grades translate directly into greater rubidium mass recovery per unit of operating expenditure.

"With rubidium trading at approximately US$1,200 to US$1,244 per kilogram, the roughly 1,960 tonnes of contained rubidium metal within the high-grade Indicated zone represents a significant in-situ value figure, even before recovery rates are applied. This is not a valuation, and investors should note that in-situ value is not equivalent to recoverable economic value."

Drilling Intensity and Resource Confidence

The resource estimate was built on a substantial two-year drilling campaign spanning 2023 to 2024:

- 117 drill holes in total (67 diamond drill holes and 50 reverse circulation holes)

- Approximately 15,000 metres of total drilling

- 45 intersections exceeding 2 metres at grades greater than 0.20% Rb₂O confirmed during rubidium screening

The combination of diamond drilling and reverse circulation drilling reflects a systematic approach to resource definition. The confirmation of 45 high-grade rubidium intercepts across this programme suggests that enrichment is laterally and vertically consistent rather than confined to isolated pockets.

Selected high-grade drill intercepts from the programme include:

| Drill Hole | Intercept Width | Average Grade (Rb₂O) | Depth to Top | Notable Sub-Interval |

|---|---|---|---|---|

| BDD-23-005 | 10.5 m | 0.41% | 136.9 m | 5.8 m at 0.50% Rb₂O |

| BDD-23-007 | 23.2 m | 0.29% | 80.0 m | 5.5 m at 0.48% Rb₂O |

| Longview Zone | 53.3 m | 0.20% | 17.0 m | Shallow, from near surface |

The Longview Zone intercept is particularly noteworthy from a development perspective. A 53.3-metre intersection grading 0.20% Rb₂O beginning at only 17 metres depth implies a low strip ratio for open-cut extraction scenarios, which reduces pre-production capital requirements and shortens the path to early cash flow.

Why Most Rubidium Resources Go Unmeasured — And Why Beecher Is Different

A critical piece of context that rarely appears in mainstream mining coverage is the systematic underreporting of rubidium in pegmatite resource estimates. The industry norm, driven by historical price weakness and limited end-use visibility, has been to either omit rubidium assaying entirely or to note its presence without formal quantification.

The consequence is a paradox: rubidium may be present at economically meaningful grades in dozens of lithium pegmatite projects across the United States and elsewhere, but no formal resource estimate exists to support its valuation. This means there is no established comparable dataset against which to benchmark any single project's rubidium endowment, making first-mover quantification both technically challenging and strategically valuable.

Iris Metals made a deliberate decision to commission formal rubidium assaying and to report the results within a JORC 2012-compliant framework. This is not a trivial undertaking. Rubidium assaying requires inductively coupled plasma mass spectrometry (ICP-MS) or similar analytical techniques capable of detecting the element at low concentrations. Furthermore, the decision to absorb these costs reflects a strategic judgement that rubidium's critical mineral status creates a real commercial opportunity that justifies the additional technical rigour.

This approach may establish a template for how future U.S. pegmatite projects approach resource reporting, particularly as rubidium's critical mineral designation increases scrutiny of supply chain exposure across the defence and technology sectors.

The next major ASX story will hit our subscribers first

Processing Pathways: What Metallurgical Testwork Reveals

Conventional Methods, Unconventional Opportunity

One of the technical risks most often cited in critical mineral project assessments is metallurgical complexity. Novel or refractory mineralogy can demand processing circuits that are expensive to build and difficult to operate, inflating capital and operating cost estimates and increasing project risk profiles. However, initial metallurgical testwork at Beecher has not triggered these concerns.

The mineralisation has been confirmed as amenable to two well-established processing approaches:

-

Dense Media Separation (DMS): A gravity-based technique that separates minerals by density using a heavy liquid or slurry medium. DMS is widely used in spodumene extraction globally and is considered a low-capital, operationally straightforward pre-concentration method. It is particularly effective at removing waste gangue minerals before downstream processing, reducing energy consumption and reagent costs.

-

Flotation: A surface chemistry-based concentration method that uses air bubbles and reagents to selectively attach to target minerals and float them to the surface of a slurry. Flotation is the industry standard for spodumene concentration and is well-understood at commercial scales.

Testwork achieved lithium recoveries of up to 80%, producing SC6 spodumene concentrate that meets the quality thresholds required by lithium chemical conversion facilities. SC6 is the standard commercial benchmark for hard-rock lithium projects globally.

Rubidium Recovery as a By-Product Stream

The rubidium recovery pathway is currently under active technical assessment as a by-product of the primary lithium processing circuit. This is a critical distinction: rubidium does not need its own standalone processing infrastructure to contribute to project economics. In addition, if rubidium can be selectively concentrated within existing flotation or DMS circuits, the incremental capital cost of capturing it may be modest relative to the revenue it generates.

The step-by-step economic logic for this by-product credit model follows a clear framework:

- Establish primary lithium processing economics based on testwork results and SC6 concentrate pricing.

- Quantify rubidium in-situ tonnage within the ore stream to be processed.

- Apply rubidium recovery rate assumptions derived from ongoing testwork.

- Multiply recovered rubidium mass by the prevailing market price (approximately US$1,200 to US$1,244 per kilogram at the time of reporting).

- Apply the resulting by-product revenue credit against lithium processing operating costs.

- Assess the net effect on project-level economics, cut-off grade sensitivity, and margin profiles.

Importantly, rubidium is not currently incorporated into the cut-off grade calculation used to define the resource boundary. This means its economic contribution is entirely additive upside that has not yet been credited in the formal resource model. As testwork progresses and recovery rates are better defined, integrating rubidium by-product economics into project-level financial modelling could materially alter the economic picture. Furthermore, advances in lithium extraction technologies may also influence how the overall processing circuit is optimised over time.

The U.S. Critical Minerals Policy Context: What Designation Actually Means

Rubidium's formal inclusion on the U.S. Department of the Interior's critical minerals list in 2024 is a regulatory fact, not a project-specific advantage. The designation applies to the metal itself, not to any individual project. What it does do, however, is alter the broader procurement and policy environment in ways that affect the commercial calculus for any domestically located rubidium resource.

Critical mineral designation under U.S. federal frameworks can influence:

- Federal procurement priorities for defence and technology applications that require rubidium

- Loan guarantee eligibility thresholds under the U.S. Department of Energy's Loan Programmes Office

- Strategic stockpile considerations managed through federal agencies

- Industry incentive frameworks that may apply to qualifying domestic producers

These are structural policy conditions. Whether and how any individual project accesses these mechanisms depends on project-specific applications and assessments that have not been publicly confirmed for Beecher at this stage. Investors should evaluate these as background conditions, not guaranteed project-level benefits.

Iris Metals' Broader U.S. Portfolio and What Comes Next at Beecher

The Beecher project does not exist in isolation within Iris Metals' asset portfolio. The company holds U.S.-focused critical mineral assets including the Tin Mountain project (also rubidium-lithium bearing, also located in the Black Hills region) and the Finley Basin tungsten project. This geographic concentration within a single mineralogically prospective jurisdiction reflects a deliberate strategy of building district-scale exposure rather than spreading capital across unrelated asset types.

For the Beecher project specifically, the near-term development milestones most relevant to analysts and investors include:

- A maiden standalone rubidium Mineral Resource Estimate targeted for delivery in the near term, which would separate rubidium into its own resource classification framework independent of the lithium cut-off grade

- An expanded lithium MRE incorporating additional drilling data accumulated since the current estimate was completed

- A demonstration mining programme designed to test operational concepts and generate early data for feasibility-level studies

- Direct Shipping Ore (DSO) sales as a potential early revenue mechanism, leveraging the project's existing permit status to generate cash flow ahead of full processing infrastructure commissioning

Frequently Asked Questions: Iris Metals Beecher Rubidium Deposit

What is the total size of the Beecher Project mineral resource?

The updated JORC 2012-compliant Mineral Resource Estimate for the Beecher Project totals 3.03 million tonnes, grading 1.0% Li₂O and 0.116% Rb₂O, reported above a 0.5% Li₂O cut-off grade.

How much rubidium oxide is contained within the high-grade zone?

The Indicated resource high-grade rubidium zone contains 1.04 million tonnes at 0.203% Rb₂O, representing approximately 2,100 tonnes of in-situ rubidium oxide, equivalent to roughly 1,960 tonnes of rubidium metal.

Why is rubidium considered a critical mineral in the United States?

The U.S. government formally designated rubidium as a critical mineral due to its applications in quantum computing, atomic clocks, defence electronics, and specialty glass manufacturing, combined with the country's complete dependence on imported supply. (U.S. Department of the Interior, Final List of Critical Minerals, 2024.)

What processing methods have been tested at Beecher?

Metallurgical testwork has confirmed amenability to both Dense Media Separation (DMS) and flotation processing. Lithium recoveries of up to 80% have been achieved, producing SC6 spodumene concentrate. Rubidium recovery as a by-product stream is currently under active technical assessment.

What makes Beecher unique among U.S. mineral resource estimates?

The Iris Metals Beecher rubidium deposit is reported as one of the first U.S. mineral resource estimates to formally quantify and report a rubidium component under JORC 2012 standards. This distinction carries both technical and strategic significance given the country's complete import dependency for this metal, and may set a precedent for how other U.S. pegmatite projects approach rubidium reporting going forward.

The Bigger Picture: Why This Deposit Matters Beyond the Drill Results

Supply chain analysis rarely makes headlines until a shortage forces the issue. Rubidium has not yet reached that inflection point, but the structural conditions that precede critical supply events are clearly assembling: zero domestic production, 100% import dependency, accelerating demand from quantum and defence technology sectors, and a formal critical mineral designation that signals policy awareness of the problem.

Against that backdrop, a formally quantified, JORC 2012-compliant rubidium resource on U.S. soil, supported by 15,000 metres of drilling, conventional processing confirmations, and a high-grade Indicated zone, represents something genuinely new in the U.S. critical minerals landscape.

The key takeaways for anyone tracking this space can be summarised as follows:

- Supply chain imperative: A formally quantified domestic rubidium resource addresses a genuine and documented strategic vulnerability in U.S. supply chains.

- Resource quality: High-grade drill intersections and a substantial Indicated resource category provide a credible technical foundation that reduces geological risk.

- Processing viability: Confirmed amenability to conventional DMS and flotation methods materially reduces technical risk compared to projects requiring novel processing approaches.

- Multi-commodity optionality: By-product rubidium economics could materially enhance project-level returns without requiring standalone infrastructure investment.

- Benchmark potential: The Iris Metals Beecher rubidium deposit's formal rubidium quantification may establish the template against which future U.S. pegmatite projects are evaluated and compared.

This article is for informational purposes only and does not constitute financial or investment advice. All forward-looking statements, forecasts, and speculative observations involve uncertainty and should not be relied upon as predictions of future outcomes. Readers should conduct their own due diligence and consult a licensed financial adviser before making any investment decisions.

Want to Stay Ahead of the Next Major Critical Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including critical minerals like rubidium, lithium, and rare earths — so subscribers can identify actionable opportunities ahead of the broader market. Explore how historic discoveries have generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin a 14-day free trial today to secure a genuine market-leading edge.