June 8, 2026

Strategic resource management has evolved beyond traditional commodity frameworks as governments worldwide recognise the intersection between economic security and materials access. Supply chain vulnerabilities exposed through recent geopolitical tensions have fundamentally altered how policymakers evaluate domestic production capabilities versus import dependencies. The systematic classification of materials as strategically essential reflects this transformation, where economic continuity and national security considerations converge around specific mineral resources that demonstrate both supply vulnerability and industrial irreplaceability.

Modern economies depend increasingly on materials that combine monetary store-of-value characteristics with indispensable industrial applications. This dual-nature creates unique policy considerations as governments balance market mechanisms against strategic intervention requirements. When traditional precious metals evolve into critical manufacturing inputs for defence systems, renewable energy infrastructure, and advanced electronics, their classification transcends historical monetary frameworks to encompass broader security implications.

The silver critical mineral designation represents this analytical evolution, where a metal traditionally viewed through precious metals pricing dynamics now commands attention as an essential industrial input experiencing structural supply constraints. Understanding this transformation requires examining how regulatory frameworks evaluate material criticality, what policy mechanisms support domestic production capacity, and how these changes create new investment opportunities across the development pipeline.

Strategic Classification Criteria Transform Silver's Policy Status

Critical mineral designation operates through systematic evaluation frameworks that assess materials across multiple strategic dimensions. The Energy Act of 2020 established comprehensive criteria requiring materials to demonstrate economic essentiality to manufacturing capabilities, supply chain vulnerability through import dependence, and strategic importance to national security applications. Furthermore, the critical minerals executive order has reinforced this silver critical mineral designation, which qualified across all three evaluation criteria, joining an expanded list that reflects evolving technology requirements and strategic priorities.

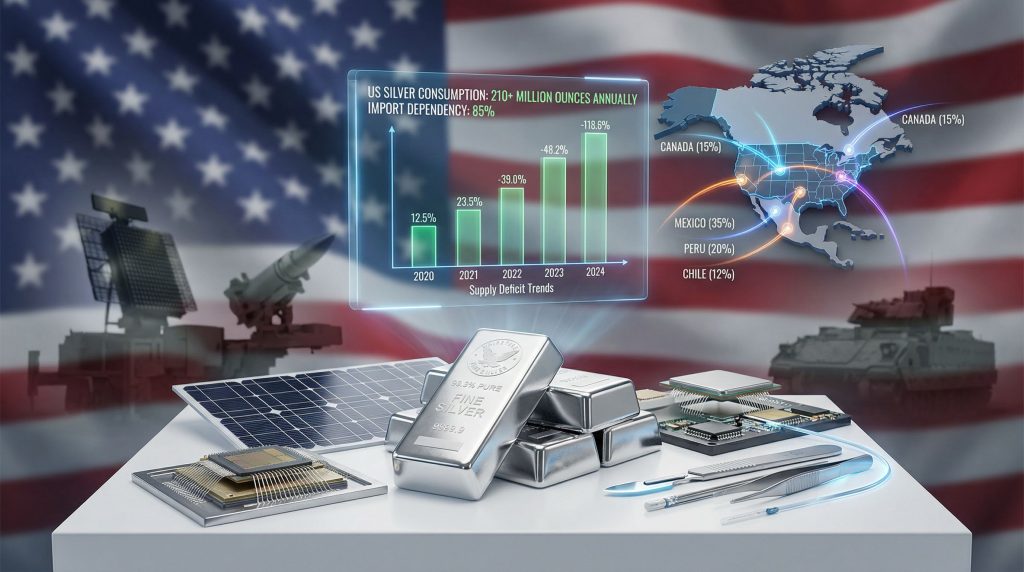

Economic Essentiality Assessment examines silver's role in manufacturing processes where substitution proves technically challenging or economically prohibitive. Industrial applications consume approximately 539 million ounces annually according to The Silver Institute's World Silver Survey 2024, representing 45% of total global demand. Solar photovoltaic manufacturing requires approximately 130-150 milligrams per cell, translating to 15-20 grams per standard residential panel, creating persistent demand that proves relatively inelastic to price fluctuations.

Supply Chain Vulnerability Analysis reveals America's significant import dependency for silver requirements. The U.S. Geological Survey reports that domestic production covers approximately 40% of consumption, creating 60% net import reliance that exposes strategic industries to potential supply disruptions. However, this dependency ratio places silver among materials requiring policy intervention to enhance supply chain resilience.

Strategic Application Requirements demonstrate silver's irreplaceable properties across defence systems, semiconductor manufacturing, and critical infrastructure. The metal's superior electrical and thermal conductivity, combined with corrosion resistance, makes it essential for radar systems, missile guidance components, and electronic warfare equipment where reliability cannot accommodate substitute materials.

Primary Silver Supply Concentration Creates Geographic Vulnerabilities

Global silver production demonstrates concerning concentration patterns that justify strategic policy intervention. According to USGS data, Mexico produces 6,300 metric tons annually (approximately 202 million ounces), representing nearly 25% of world mine production. China contributes 3,600 metric tons whilst Peru adds 3,500 metric tons, creating a three-country concentration that supplies over 50% of global production.

Import Source Dependencies for the United States reveal additional concentration risks:

• Mexico: 41% of U.S. silver imports

• Canada: 31% of foreign sourcing

• Peru: 9% of import volumes

• Other sources: 19% distributed across multiple countries

This geographic distribution, whilst more diversified than some critical minerals, still creates potential chokepoints during regional instability or bilateral trade disputes. Silver's industrial applications in defence systems, semiconductor manufacturing, and renewable energy infrastructure make supply disruptions particularly problematic for strategic industries requiring operational continuity.

Processing Concentration Concerns compound raw material supply risks. China's significant role in global silver refining capacity creates additional dependency layers beyond mining operations. Raw silver concentrate requires sophisticated processing to achieve industrial-grade specifications, creating bottlenecks that extend beyond extraction activities into value-added manufacturing stages.

When big ASX news breaks, our subscribers know first

Industrial Applications Drive Critical Status Recognition

Silver critical mineral designation reflects the metal's irreplaceable role across multiple strategic sectors experiencing rapid growth. Unlike traditional precious metals valued primarily for monetary properties, silver's designation emphasises expanding industrial applications that demonstrate technical superiority over alternative materials.

Solar Photovoltaic Manufacturing Creates Structural Demand Growth

Solar energy deployment represents silver's largest and fastest-growing industrial application. The International Energy Agency's World Energy Outlook 2023 projects that solar PV capacity could triple by 2030 under current policies, driving sustained silver consumption growth. Each standard residential panel requires approximately 15-20 grams of silver for electrical connectivity, creating direct correlation between renewable energy expansion and silver demand.

Technological Efficiency Improvements in solar manufacturing have reduced silver content per panel through paste formulation advances and printing process optimisation. However, total sector demand continues growing as installation volumes expand faster than per-panel reduction rates. The Silver Institute reports solar photovoltaic applications consumed 161 million ounces in 2023, representing approximately 30% of industrial silver demand.

Thrifting Technology Limitations prevent unlimited silver content reduction without compromising panel efficiency and durability. In addition, silver's unique combination of electrical conductivity, thermal stability, and corrosion resistance makes it technically superior to alternatives like copper or aluminium for critical electrical connections where performance and reliability standards cannot accommodate substitution.

Semiconductor Manufacturing Drives Advanced Technology Demand

The CHIPS and Science Act of 2022 authorised approximately $52 billion to support domestic semiconductor research, development, and manufacturing. This massive investment in domestic production capacity creates additional strategic demand for silver used in advanced chip manufacturing where performance requirements exceed alternative materials' capabilities.

Electronics and Semiconductor Applications consumed approximately 70 million ounces of silver in 2023, including circuit boards, electrical contacts, and advanced packaging applications. Domestic semiconductor manufacturing expansion under CHIPS Act funding creates additional demand for reliable silver supplies that meet strict quality and security requirements.

5G Infrastructure Development and telecommunications advancement require silver's superior electrical properties for high-frequency applications where signal integrity proves critical. Advanced communication systems cannot accommodate performance compromises that substitute materials would introduce.

Defence Systems Integration Requires Domestic Supply Security

Military applications incorporate silver into radar systems, electronic warfare equipment, and guidance systems where reliability and performance specifications exceed civilian requirements. These applications require domestic sourcing to maintain operational security and supply chain integrity, making foreign dependency particularly problematic for defence procurement.

Classified Defence Consumption volumes remain undisclosed for security reasons, but the strategic importance of silver in defence electronics creates policy imperatives for domestic production capacity that extend beyond purely economic considerations. Consequently, this reinforces the broader defence materials strategy that prioritises supply chain security.

Medical Device Manufacturing leverages silver's antimicrobial properties in surgical instruments, wound dressings, and implantable devices. The global medical silver market reached approximately $2.8 billion in 2023, with healthcare supply chain security emerging as a national priority following pandemic-era disruptions.

Market Structure Justifies Policy Intervention Logic

Silver markets demonstrate unique structural characteristics that distinguish them from typical commodities and justify government intervention through critical mineral frameworks. Traditional market mechanisms prove inadequate to address supply constraints created by the metal's unusual production profile and demand characteristics.

By-Product Production Creates Supply Inelasticity

Approximately 70-75% of silver production derives from base metal by-products where silver represents secondary economic value rather than the primary revenue driver. This production structure creates fundamental supply inelasticity that prevents traditional price signals from quickly incentivising increased output.

Supply Response Disconnection occurs when copper, zinc, or lead prices decline, causing primary metal operations to reduce production regardless of silver price levels. For instance, this creates scenarios where silver supply decreases even during periods of elevated silver prices, violating typical commodity market relationships between price and production incentives.

Primary Silver Mines represent only 25-30% of global production, limiting the sector's ability to respond to price signals through dedicated silver-focused operations. These pure-play operations cannot compensate for supply disruptions from the larger by-product segment that responds to different metal price dynamics.

Mine Development Constraints have limited new supply growth as extended permitting timelines, capital intensity requirements, and historically depressed prices discouraged exploration investment over the past decade. The Silver Institute reports that global silver markets have experienced supply deficits in recent years, with 2023 showing an estimated 184 million ounce deficit.

Physical Market Tightness Indicates Structural Imbalance

COMEX Silver Warehouse Stocks tracked by CME Group have declined significantly, indicating physical market tightness that reflects genuine supply constraints rather than speculative positioning. Traditional commodity markets typically see inventory rebuilding during price increases, making silver's continued tightness particularly notable for market analysts.

Above-Ground Silver Stocks face additional pressure from expanding industrial consumption that reduces available supplies for investment and monetary purposes. Unlike gold, which accumulates in central bank reserves and private hoarding, silver experiences continuous industrial consumption that permanently removes material from available stocks.

Recycling Contribution Limitations provide some supply augmentation but cannot fully offset primary production deficits. Secondary silver recovery from electronics and industrial applications requires sophisticated processing and proves economically viable only during elevated price periods.

Federal Support Mechanisms Create Investment Opportunities

Silver critical mineral designation unlocks comprehensive federal support frameworks designed to incentivise domestic production capacity and reduce strategic import dependencies. These mechanisms operate through multiple policy channels that fundamentally alter project economics for qualifying silver operations.

Defence Production Act Authorities Enable Direct Investment

The Department of Defence announced approximately $600 million in Defence Production Act Title III funding for critical minerals processing and production infrastructure through fiscal years 2022-2024. These authorities enable direct government investment in domestic silver mining and processing infrastructure through loan guarantees, purchase agreements, and rapid capacity expansion funding.

Project Eligibility Requirements for DPA support typically require domestic location, strategic value demonstration, and capability to meaningfully impact supply chain security. Projects demonstrating substantial production potential receive preferential consideration for major programme participation versus small-scale producers.

Coordinated Agency Support through the Federal Permitting Improvement Steering Council provides streamlined approval processes for covered infrastructure projects, including critical mineral developments. The FAST-41 permitting process enables coordination among federal agencies, though specific timelines for silver projects remain project-dependent.

Tax Incentive Structures Improve Project Economics

The Inflation Reduction Act provides Production Tax Credits and Investment Tax Credits for critical mineral extraction and processing facilities, with credits up to 30% of qualified expenditures. Section 45X manufacturing credits potentially benefit qualifying silver production operations, though specific eligibility criteria require regulatory guidance implementation.

Enhanced Depletion Allowances and accelerated depreciation schedules specifically targeting critical mineral operations improve project returns and competitive positioning versus international alternatives. However, these mechanisms compound over project lifespans, creating substantial value premiums for domestic assets.

Advanced Manufacturing Tax Credits under Section 45X provide production-based incentives for critical mineral processing, potentially benefiting silver refining and value-added manufacturing operations that support domestic supply chain integration.

Strategic Stockpiling Programmes Provide Demand Support

Government stockpiling initiatives create potential demand buffers that provide price floor mechanisms and long-term offtake security for domestic producers. Federal agencies can establish inventory targets that support market stability whilst reducing supply chain vulnerabilities, though specific silver stockpiling programmes require verification with recent government announcements.

Procurement Preferences in government contracts may favour domestic silver suppliers for strategic applications, creating market access advantages that international competitors cannot replicate. Defence contractors and infrastructure developers benefit from preferential sourcing arrangements that enhance revenue predictability.

Geographic Positioning Maximises Policy Benefits

Not all silver projects qualify equally for critical mineral support mechanisms. Geographic location, ownership structure, and operational characteristics determine eligibility for various government programmes and incentive structures that create competitive advantages for strategically positioned assets.

Premier North American Jurisdictions Command Valuation Premiums

The Fraser Institute's Annual Survey of Mining Companies 2023 ranks Nevada 2nd globally in the Investment Attractiveness Index, providing regulatory certainty, established infrastructure, and favourable tax frameworks that support premium project valuations. Nevada accounts for approximately 75% of U.S. gold production and significant silver by-product output.

Idaho Silver Production ranks among top U.S. producing states with established mining culture, experienced workforce, and proven regulatory frameworks that accelerate project development timelines. The Silver Valley region hosts historic high-grade silver deposits with existing infrastructure that reduces capital requirements.

Texas Jurisdiction Benefits include 20% corporate tax rates and business-friendly regulatory environment that creates competitive advantages for qualifying projects. The state's location adjacent to established mining regions provides access to experienced service providers and supply chain networks.

Canadian Provincial Frameworks in British Columbia and Ontario offer additional North American exposure with established mining codes, environmental standards, and political stability that international investors prefer for long-term capital deployment.

Processing Integration Enhances Strategic Value

Domestic Processing Requirements for certain Defence Production Act projects and CHIPS Act funding require domestic processing and value-added manufacturing to qualify for maximum support. Concentrate export models may not qualify for strategic programmes designed to enhance domestic supply chain integration.

Value-Added Manufacturing capabilities that produce industrial-grade silver products domestically align with supply chain sovereignty objectives and qualify for enhanced support mechanisms versus raw material export strategies.

Refining Capacity Development addresses critical processing bottlenecks by reducing dependency on foreign refining services, creating additional margin opportunities and strategic value for integrated operations.

Investment Implications Across Development Stages

Silver critical mineral designation creates multiple investment thesis layers that extend beyond traditional precious metals analysis. Government support mechanisms fundamentally alter risk-return profiles for domestic silver projects whilst creating competitive advantages versus international alternatives.

Development Stage Projects Benefit from Enhanced Economics

Risk-Return Profile Improvements through tax incentives, loan guarantees, and accelerated depreciation schedules enhance internal rates of return and reduce capital requirements for qualifying operations. These benefits compound over project lifespans, creating substantial value premiums versus projects without government support eligibility.

Financing Access Enhancement via government loan guarantee programmes reduces project finance costs and expands available capital sources beyond traditional mining finance markets. The Department of Energy's Loan Programmes Office has authority to provide guarantees for critical mineral projects under Title XVII of the Energy Policy Act of 2005.

Permitting Timeline Acceleration through coordinated agency approval processes addresses historical development bottlenecks that have constrained project advancement. Predictable regulatory pathways reduce execution risk and enable more aggressive development schedules.

Operating Producers Gain Competitive Market Positioning

Offtake Security Benefits through government procurement preferences and strategic purchasing agreements provide revenue visibility that supports expansion planning and reduces market risk exposure. Federal demand creates price floor mechanisms that enhance cash flow predictability for strategic planning.

Market Access Advantages emerge as domestic producers gain preferential treatment in government procurement, infrastructure development, and strategic partnership opportunities. Critical mineral status creates competitive positioning that international suppliers cannot replicate.

Expansion Funding Support through various federal programmes enables capacity increases and productivity improvements that enhance operational leverage to commodity price movements whilst maintaining strategic supply chain positioning.

The next major ASX story will hit our subscribers first

Comparative Analysis Across Critical Mineral Classifications

Silver critical mineral designation occurs within a comprehensive framework that includes both traditional strategic materials and newly recognised industrial inputs. Understanding comparative policy treatment provides context for silver's positioning within broader resource security strategies.

Rare Earth Elements Receive Maximum Support Intensity

Rare earth elements demonstrate 74% import dependency with extreme Chinese supply dominance, creating the most comprehensive support frameworks due to acute vulnerability and limited alternative sources. Silver's 60% net import reliance creates similar strategic concerns whilst offering more diversified sourcing options.

Dedicated Funding Programmes for rare earth development exceed support available for other critical minerals due to the strategic importance of these materials for defence and advanced technology applications. Silver benefits from general critical mineral programmes rather than material-specific initiatives.

Copper's Concurrent Designation Demonstrates Electrification Focus

Copper's addition to the USGS critical minerals list in 2024 marks the first time this major industrial metal received critical designation, reflecting increased focus on electrification infrastructure requirements. Both copper and silver benefit from renewable energy deployment policies and infrastructure investment programmes.

Shared Policy Support for electrification metals creates synergistic opportunities for polymetallic projects containing both silver and copper, potentially qualifying for multiple support programmes and enhanced government interest.

Infrastructure Investment Alignment through various federal programmes supports both metals' roles in renewable energy systems, electric vehicle charging networks, and power grid modernisation initiatives.

Uranium's Strategic Classification Provides Defence-Focused Support

Uranium's critical mineral status emphasises defence and energy security priorities through specialised support mechanisms focused on nuclear fuel cycle security. Silver's defence applications provide similar strategic value propositions, though less specialised than nuclear-specific programmes.

National Security Implications create policy support that transcends purely economic considerations, providing stability and continuity across changing political administrations for materials deemed essential to defence capabilities.

Development Pipeline Demonstrates Exceptional Project Economics

The silver development sector features multiple advanced projects demonstrating high-grade characteristics, compelling economics, and accelerated development timelines that position them to capitalise on favourable market conditions and government support mechanisms.

High-Grade Resources Command Premium Valuations

Grade Quality Advantages distinguish premier silver projects from bulk tonnage operations through superior economics, reduced processing costs, and enhanced profitability that justify premium market multiples. High-grade deposits require lower capital intensity per ounce of production whilst generating superior cash flows.

Resource Growth Potential through systematic exploration provides upside optionality that enhances project value beyond current resource estimates. Companies demonstrating consistent discovery success command market premiums for exploration expertise and resource expansion capabilities.

Metallurgical Advantages in processing high-grade silver ores create operational efficiencies that improve project economics through higher recovery rates, reduced reagent consumption, and simplified flowsheet designs that lower operating costs.

Construction-Ready Projects Offer Near-Term Production Exposure

Engineering Completion eliminates typical development delays and enables immediate construction commencement following financing and permitting completion. Projects with completed feasibility studies and final engineering provide the highest probability of successful development execution.

Permit Advancement through established regulatory processes reduces development risk and provides timeline certainty for construction planning and financing arrangements. Permitted projects command valuation premiums reflecting reduced execution risk.

Infrastructure Advantages including existing site facilities, transportation access, and utility connections substantially reduce capital requirements and accelerate development schedules versus greenfield competitors requiring complete infrastructure development.

Operating Performance Validates Investment Thesis

Established silver producers demonstrate strong operational performance and cash generation capabilities that validate sector investment merits whilst executing growth strategies positioning them for substantial production increases over multi-year time horizons.

Record Financial Performance Supports Expansion Plans

Revenue Growth Acceleration driven by both production volume increases and favourable metal prices creates robust cash flow generation that funds organic growth initiatives without requiring external capital dilution.

Operating Leverage Benefits become apparent as fixed cost structures spread across increased production volumes, improving margins and cash flow per ounce whilst maintaining operational efficiency standards.

Free Cash Flow Generation provides internal funding for exploration programmes, capacity expansions, and acquisition opportunities that enhance long-term production profiles and resource bases.

Production Growth Strategies Target Multi-Asset Portfolios

Satellite Deposit Development utilises existing infrastructure and processing facilities to add production from nearby resources, creating capital-efficient growth that leverages established operational capabilities.

Mill Capacity Expansions increase throughput capabilities to handle growing ore reserves whilst improving operational efficiency through economies of scale and processing optimisation.

Aggressive Exploration Programmes focus on expanding existing resources and discovering new deposits within established mining districts, providing organic growth opportunities that utilise existing infrastructure and expertise.

2026 Catalyst Timeline Creates Systematic Value Recognition

The silver sector approaches 2026 with multiple technical and economic catalysts concentrated across the development pipeline, providing systematic de-risking opportunities and valuation re-rating potential as projects advance through critical development milestones.

First Quarter Resource and Technical Updates

Updated Mineral Resource Estimates incorporating 2023-2024 drilling programmes will demonstrate resource growth and grade improvements from high-grade discoveries, providing quantified metrics for comparing assets against peer companies and establishing updated project economics.

Technical Reports with Preliminary Economic Assessments enable comparative analysis through standardised metrics including net present value, internal rate of return, and payback calculations that facilitate institutional investment analysis and project ranking methodologies.

Reserve Estimate Releases qualify companies to publish formal production guidance under regulatory standards, providing revenue forecasting capabilities that support advanced-stage project financing and strategic partnership discussions.

Mid-Year Development Advancement Milestones

Construction Commencements following completed engineering eliminate typical development delays and provide immediate progress toward production startup, creating visible advancement that supports continued market interest and institutional participation.

Aggressive Drilling Programmes targeting 20,000-36,000 metres demonstrate systematic resource expansion efforts designed to grow existing deposits whilst testing exploration targets that provide additional upside potential beyond current development plans.

Metallurgical Test Work Completion de-risks processing strategies through demonstrated recovery rates and flowsheet optimisation, providing technical validation that supports project financing and reduces development execution risk.

Third Quarter Operational Milestones

Facility Commissioning including paste backfill plants and processing expansions enables throughput increases and operational efficiency improvements that translate directly into production growth and enhanced cash flow generation.

JORC-Compliant Resource Conversions through systematic drilling campaigns provide international reporting standard compliance that expands potential investor base and facilitates institutional participation from global mining funds.

Production Rate Increases from capacity expansions and operational optimisation create visible operational leverage that demonstrates management execution capabilities whilst providing enhanced commodity price exposure through increased production volumes.

Strategic Investment Framework for Critical Mineral Exposure

The convergence of structural supply deficits, expanding industrial applications, and comprehensive government support mechanisms creates a compelling investment framework that extends beyond traditional precious metals characteristics. Moreover, the critical minerals strategy has evolved to address growing supply chain vulnerabilities whilst recognising silver's dual role as both monetary asset and strategic industrial input.

Multi-Layered Value Proposition

Supply Security Premium emerges as domestic projects command valuation benefits through reduced regulatory risk, enhanced financing access, and government support eligibility that justify premium multiples versus international competitors facing potential silver tariffs impacts.

Industrial Demand Growth Acceleration through renewable energy deployment, semiconductor manufacturing expansion, and defence spending increases creates structural consumption growth independent of monetary policy cycles, providing demand stability during economic uncertainty.

Policy Support Optionality provides downside protection through government intervention mechanisms whilst maintaining upside exposure to commodity price appreciation, creating asymmetric risk profiles that distinguish critical mineral investments from traditional commodity exposure.

Institutional Validation through growing participation demonstrates recognition of sector investment merits, with institutional ownership percentages rising organically through open-market purchases and oversubscribed capital raises attracting established mining-focused investment managers.

Development Stage Risk-Return Optimisation

Resource Growth Leverage in exploration and development-stage companies typically provides greater sensitivity to metal price movements than producing companies with fixed cost structures, creating enhanced upside participation during favourable commodity cycles.

Government Support Access for domestic projects provides additional optionality through potential financing assistance, permitting acceleration, and procurement preferences that reduce development risk whilst enhancing project economics through multiple policy channels.

Discovery Economics Validation by companies demonstrating low-cost resource addition rates generates meaningful leverage in rising price environments, with efficient exploration programmes creating substantial resource bases at compelling per-ounce discovery costs.

Technical De-Risking Progress through systematic advancement of metallurgical testing, engineering studies, and permitting processes creates visible milestone achievement that supports continued institutional interest and reduces execution uncertainty.

The convergence of structural supply deficits, expanding industrial applications, and comprehensive government support mechanisms creates a compelling investment framework for silver assets positioned to benefit from this evolving policy landscape. Furthermore, understanding the broader context of silver supply challenges reinforces the strategic importance of domestic production capabilities. Projects demonstrating domestic production capabilities, processing integration, and strategic end-market exposure offer optimal positioning for investors seeking leveraged exposure to both precious metals appreciation and strategic resource policy support.

Want to Capitalise on Critical Mineral Policy Changes?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, particularly those positioned to benefit from evolving strategic resource policies and government support mechanisms. Access real-time insights into exploration breakthroughs and resource development announcements, including silver and other critical mineral opportunities that could reshape supply chain security whilst delivering substantial returns to early investors.