June 9, 2026

The Industrial Policy Gap That Could Cost Southern Africa Its Battery Moment

The global transition to electric mobility is not simply a technological shift — it is a profound restructuring of industrial geography. South Africa auto incentives for battery materials are now at the centre of this restructuring, as nations that move early to align their mineral endowments with downstream manufacturing incentives will capture disproportionate value from a supply chain that analysts project will require over $400 billion in new investment before 2035. Those that delay risk becoming perpetual raw material exporters while value-added processing concentrates elsewhere.

South Africa sits at an unusual crossroads. It hosts world-class reserves of platinum group metals, manganese, iron ore, and increasingly identified deposits of lithium and graphite. However, its automotive industrial support framework has, until now, been anchored entirely in the internal combustion engine era. The proposed expansion of the country's primary automotive incentive mechanism to cover battery-critical minerals represents one of the most consequential industrial policy pivots in the region's recent history, and the implications extend well beyond South Africa's borders.

When big ASX news breaks, our subscribers know first

Understanding Why the Existing Framework Left Battery Materials Out

South Africa's automotive incentive architecture was constructed around a set of assumptions that made complete sense in the 1990s and early 2000s: vehicles would continue to run on combustion engines, and the materials required to build them — aluminium, steel, and platinum group metals — would remain the dominant inputs for decades.

The current programme supports the industry through customs duty rebates and refunds, production-linked incentives, investment support, and a volume-based allowance that rewards manufacturers for producing vehicles at scale within South Africa. These mechanisms were effective at their original purpose, helping grow the sector into a meaningful contributor to South Africa's industrial base.

The structural flaw emerged not from poor design but from a failure to anticipate the pace of electrification. Critical minerals central to EV battery manufacturing — including lithium, cobalt, graphite, copper, rare earth elements, and iron — were entirely absent from the qualifying materials list. This left battery component manufacturers and EV-oriented processors unable to access the programme's production-linked credits, creating a direct financial disincentive to locate battery supply chain operations in South Africa. Furthermore, the critical minerals demand growing from the energy transition made this gap increasingly costly.

"The proposed APDP2 amendments do not dismantle the existing incentive framework. They extend and recalibrate it, adding a battery-era layer to a structure that was already functioning effectively for conventional vehicles."

What the Proposed APDP2 Changes Actually Involve

The International Trade Administration Commission (ITAC) has released a government notice outlining proposed amendments to the Automotive Production and Development Programme, with a four-week public comment window open for stakeholder submissions.

The core changes operate across three dimensions:

1. Expanding the qualifying materials list to include lithium, cobalt, graphite, copper, rare earth elements, and iron, covering the primary inputs for both lithium-ion and lithium iron phosphate (LFP) battery chemistries.

2. Establishing a differentiated SVA rate of 50% for battery materials used in EV manufacturing, double the standard 25% rate applied to conventional qualifying inputs.

3. Extending regional sourcing eligibility beyond the Southern African Customs Union (SACU) to the full Southern African Development Community (SADC), dramatically broadening the geographic scope of qualifying supply chains.

The table below illustrates how the proposed changes compare to the existing programme structure:

| Programme Dimension | Current Framework | Proposed APDP2 Expansion |

|---|---|---|

| Standard materials covered | Aluminium, steel, PGMs | + Lithium, cobalt, graphite, copper, rare earths, iron |

| SVA rate for standard materials | 25% | 25% (unchanged) |

| SVA rate for EV battery materials | Not applicable | 50% |

| Regional sourcing eligibility | SACU only | Full SADC membership |

| Production credits for EV batteries | Not available | Enhanced credits for battery manufacturers |

The 50% SVA Rate: Why the Double Standard Matters for Investment Decisions

The Standard Value Added rate is not a minor accounting adjustment — it is the lever that determines how much of a manufacturer's input cost translates into claimable production incentive credits. Understanding this mechanism is essential for grasping why the proposed 50% rate for battery materials represents a material shift in the investment calculus.

Under the existing framework, a manufacturer using R100 million worth of qualifying standard materials can count R25 million as locally added value toward production incentive thresholds. Under the proposed 50% SVA rate for EV battery materials, that same R100 million in qualifying inputs generates R50 million in recognised local value, doubling the incentive credit accessible to the manufacturer.

This matters because battery material processing is capital-intensive and technologically complex relative to conventional automotive component manufacturing. Achieving battery-grade lithium hydroxide, for example, requires purification to a minimum of 99.5% lithium hydroxide monohydrate content, with strict controls on impurities such as sodium, potassium, and calcium that can degrade battery performance. The processing infrastructure required to meet these specifications demands significantly higher upfront capital than conventional smelting or rolling operations.

The higher SVA rate directly addresses this capital intensity barrier by accelerating the recovery of investment through larger production incentive credits. For investors evaluating whether to establish battery-grade processing within the SADC region versus sourcing from established Asian refineries, this differential can shift project economics meaningfully. In addition, the broader battery metals investment landscape in 2025 makes these incentives particularly timely.

"When the recognised local value of an input doubles, the time required to recover capital through production incentives compresses significantly, which is often the critical variable in investment decisions for large-scale processing facilities."

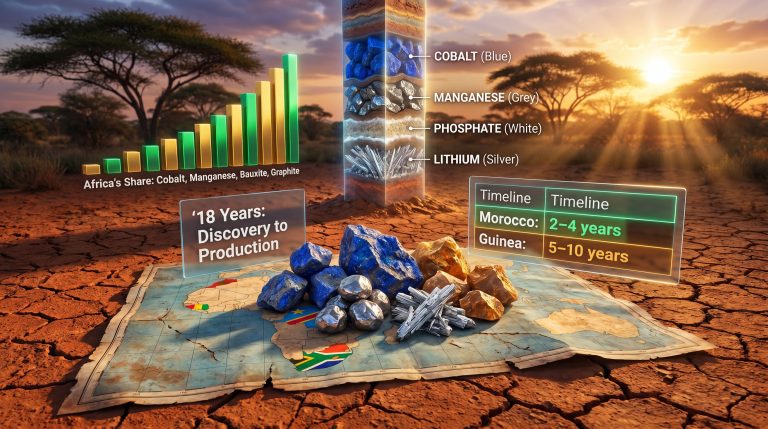

The Six Critical Minerals Now Entering the Qualifying List

The specific selection of materials proposed for inclusion covers both dominant and emerging battery chemistry pathways, which is a deliberate design choice rather than a coincidence.

-

Lithium: The foundational electrochemical element in all commercially dominant battery technologies. The ongoing lithium boom driven by battery storage expansion makes its inclusion particularly significant. Battery-grade lithium is typically processed either as lithium carbonate (Li2CO3) or lithium hydroxide monohydrate (LiOH·H2O), with hydroxide increasingly preferred for high-nickel cathode chemistries.

-

Cobalt: A stabilising element in nickel-manganese-cobalt (NMC) and nickel-cobalt-aluminium (NCA) cathode formulations. While the industry trend is toward lower-cobalt chemistries to reduce cost and supply chain concentration risk, cobalt remains essential in high-energy-density applications including aviation-adjacent EVs and premium passenger vehicles.

-

Graphite: The dominant anode material in current commercial lithium-ion batteries, with natural graphite typically requiring processing to spherical purified graphite (SPG) at 99.95%+ carbon purity for battery applications. Synthetic graphite is also used but is more energy-intensive to produce.

-

Copper: Essential for current collectors within battery cells, thermal management systems, motor windings, and high-voltage wiring throughout the vehicle. EV platforms require approximately 2.5 to 4 times the copper content of conventional ICE vehicles.

-

Rare Earth Elements: Critical for the permanent magnets used in EV traction motors, particularly neodymium-iron-boron (NdFeB) magnets. Consequently, securing rare earth supply chains has become a strategic priority for nations seeking EV manufacturing capability.

-

Iron: The inclusion of iron is strategically significant because it addresses the LFP battery chemistry that has gained dramatic global market share due to superior thermal stability, longer cycle life, and substantially lower cost compared to NMC alternatives.

The simultaneous inclusion of materials relevant to both NMC and LFP chemistries signals a chemistry-agnostic policy approach — a deliberate hedge against the risk of concentrating industrial incentives on a single technology pathway that may not prevail in the long run.

Why the SADC Sourcing Requirement Is the Most Underappreciated Element of the Policy

The geographic boundary conditions attached to qualifying materials are arguably more strategically consequential than the SVA rate change itself, yet they have attracted comparatively little analytical attention.

By extending sourcing eligibility to the full SADC membership, the proposed amendments create an implicit architecture for a regional battery supply chain corridor rather than a purely domestic incentive. Consider the mineral distribution across SADC member states:

| Country | Primary Battery-Relevant Resources |

|---|---|

| South Africa | PGMs, manganese, vanadium, iron ore, emerging lithium |

| Democratic Republic of Congo | World's largest cobalt producer; major copper reserves |

| Zimbabwe | Significant lithium pegmatite deposits; active exploration |

| Zambia | Major copper belt; long-established production infrastructure |

| Mozambique | Graphite deposits; expanding critical mineral export base |

| Namibia | Rare earth projects; active lithium exploration activity |

| Botswana | Manganese; emerging battery mineral exploration |

The DRC alone produces approximately 70% of the world's cobalt. Zimbabwe has emerged as one of the most actively explored lithium jurisdictions outside of established producers. Furthermore, global cobalt production data underscores just how critical the DRC's participation in a SADC-wide supply chain would be for the framework's success.

By anchoring incentive eligibility to SADC sourcing, South Africa is effectively positioning the entire southern African mineral belt as the upstream foundation for a domestic EV manufacturing industry. This simultaneously creates economic rationale for those mineral-rich neighbours to develop processing capacity rather than exporting raw ores to Asian refineries.

This is a subtle but important distinction from comparable policies in other jurisdictions. Indonesia's downstream processing mandates, for instance, are explicitly domestic in scope, requiring processing within Indonesian territory. South Africa's approach creates a regional rather than purely national supply chain logic, which may prove more practically achievable given the geographic distribution of the minerals in question.

The next major ASX story will hit our subscribers first

Alignment With the South African Automotive Master Plan 2035

The proposed APDP2 amendments are explicitly positioned as an implementation mechanism for the South African Automotive Master Plan 2035 (SAAM 2035), which targets output of approximately 1.4 million vehicles per year by 2035, representing a substantial increase from current production levels.

Three pillars of SAAM 2035 are directly relevant to the battery materials expansion:

-

Volume growth: Achieving 1.4 million vehicles requires both scaling existing manufacturer operations and attracting new investment, including from EV-focused manufacturers for whom battery supply chain access is a primary location criterion.

-

Deepened localisation: SAAM 2035 measures localisation partly through SVA calculations — the same mechanism being enhanced by the proposed amendments. The 50% SVA rate for battery materials creates a direct financial incentive for vehicle assemblers to source battery inputs from within the SADC region rather than importing from established Asian supply chains.

-

Electric mobility transition: The plan explicitly identifies EV manufacturing capability as a structural priority, recognising that failure to develop this capability would leave South Africa's automotive sector increasingly misaligned with the direction of global demand.

Without the proposed APDP2 extension, SAAM 2035's EV ambitions would have lacked a concrete financial mechanism to attract battery supply chain investment. The amendments translate a policy aspiration into a bankable incentive structure.

Competitive Context: How South Africa Compares to Rival Jurisdictions

South Africa is not competing in a vacuum. Multiple resource-rich nations are actively constructing incentive frameworks to capture battery supply chain value, and the relative attractiveness of the proposed South Africa auto incentives for battery materials will be evaluated by investors against these alternatives.

| Policy Dimension | South Africa (Proposed) | Indonesia | Chile | DRC |

|---|---|---|---|---|

| Battery mineral incentive mechanism | 50% SVA rate for EV inputs | Domestic processing mandates | Lithium royalty and tax regime | Limited formal industrial framework |

| Regional sourcing eligibility | SADC-wide | Domestic only | Domestic and Mercosur | Minimal |

| EV production target | ~1.4M vehicles/yr by 2035 | Growing assembly base | Limited vehicle assembly | Negligible |

| Mineral diversity | High: PGMs, Li, Co, graphite, RE, iron | Nickel-dominant | Lithium-dominant | Cobalt and copper-dominant |

South Africa's competitive differentiation lies in mineral diversity rather than depth in any single commodity. This breadth provides resilience against the kind of technology concentration risk that affects more narrowly endowed jurisdictions, but it also requires a more complex policy architecture to incentivise development across multiple materials simultaneously.

The chemistry-agnostic design of the proposed amendments — covering both NMC-relevant and LFP-relevant materials — reflects this strategic reality.

What the Public Comment Period Means for Industry Stakeholders

The four-week public comment window opened by ITAC represents a genuine opportunity to shape the final policy design. Based on the proposed framework, the stakeholder groups with the most direct material interest include:

- Battery mineral miners and processors operating in South Africa or anywhere within the SADC region, who stand to benefit from increased downstream demand for their output.

- EV battery manufacturers evaluating southern Africa as an investment destination, for whom the incentive economics will directly influence site selection decisions.

- Vehicle assemblers currently participating in APDP2 who are planning transitions toward electric model lines and need clarity on how battery input sourcing will interact with their existing incentive structures.

- Foreign investors conducting feasibility assessments for battery processing facilities, who require certainty on the SVA calculation methodology and qualifying criteria before committing capital.

Key questions that the comment process should probe include whether the 50% SVA rate is calibrated at the right level to drive investment relative to competing jurisdictions, how hybrid battery derivatives are defined within the qualifying materials categories, and what transition arrangements will apply to existing APDP2 participants as they shift toward EV production.

"The public comment period is not a procedural formality. It is the mechanism through which the technical details that determine real-world investment economics get resolved, and those with the most to gain or lose should engage substantively."

The Broader Significance for African Industrial Development

Stepping back from the specific mechanics of the APDP2 proposal, the policy represents a meaningful attempt to address one of the most persistent structural weaknesses in African industrial development: the gap between resource endowment and downstream value capture.

Africa holds an extraordinary share of the world's battery-critical minerals. The DRC's cobalt dominance is well documented. Southern Africa's combined lithium, graphite, manganese, and rare earth resources represent a geological endowment that few other regions can match. Yet historically, the vast majority of value creation from these resources has occurred outside the continent — in Chinese refining facilities, South Korean battery plants, and German automotive factories.

South Africa auto incentives for battery materials, however incrementally, move the incentive architecture toward a model where regional mineral extraction, regional processing, and regional manufacturing are financially connected rather than operating in isolation. Whether it succeeds will depend substantially on the implementation details that emerge from the current consultation process and the subsequent regulatory design.

What is clear is that the window for positioning southern Africa within the emerging global battery supply chain is not indefinitely open. Supply chain architectures, once established, tend toward consolidation around established nodes. The policy decisions made in the next two to three years will likely determine whether southern Africa becomes a genuine participant in the battery-era industrial economy or remains a supplier of unprocessed inputs to value chains anchored elsewhere. Consequently, analysts tracking the broader EV battery manufacturing sector have noted that southern Africa's window of opportunity is narrowing as competing jurisdictions accelerate their own frameworks.

This article is intended for informational purposes only and does not constitute financial or investment advice. Readers should conduct their own due diligence before making any investment decisions. Policy proposals are subject to change following public consultation processes.

Want to Capitalise on the Next Major Battery Minerals Discovery Before the Market Does?

As southern Africa's industrial policy begins aligning mineral endowments with downstream battery manufacturing incentives, the race to identify high-potential ASX-listed critical mineral opportunities is accelerating — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries hit the ASX, turning complex data across lithium, cobalt, graphite, copper, and rare earths into actionable insights for investors at every level. Start your 14-day free trial today and explore how historic mineral discoveries have generated extraordinary returns to understand what early positioning can mean for your portfolio.