May 24, 2026

The Chokepoint That Controls the World's Energy Pulse

Global energy markets are built on a fragile geographic assumption: that roughly a dozen tankers can pass unimpeded through a narrow Persian Gulf corridor every single day. When that assumption holds, oil flows freely, prices remain anchored, and the industrial economies of Asia and Europe hum without interruption. When it breaks, the reverberations travel far beyond the strait itself, reshaping commodity benchmarks, trade finance systems, diplomatic calendars, and household energy bills simultaneously.

The Strait of Hormuz opening for commercial shipping has become one of the most consequential geopolitical questions of 2026. Understanding what that process actually involves, why it is taking longer than political announcements suggest, and what genuine normalisation looks like requires a closer examination of the mechanisms at work beneath the diplomatic headlines.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is Unlike Any Other Maritime Chokepoint

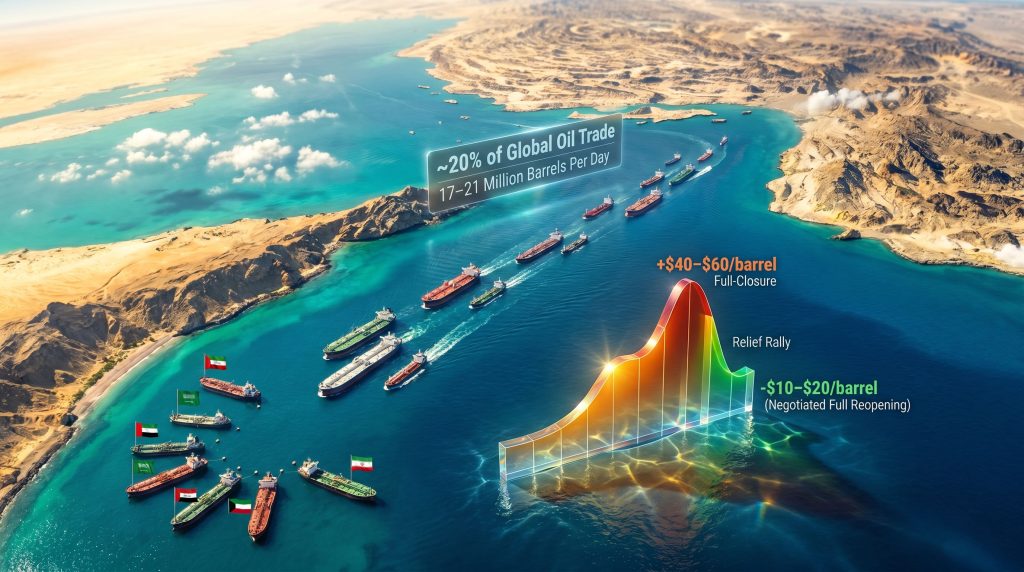

At its narrowest navigable point, the strait measures approximately 33 kilometres across — a distance a commercial jet covers in under two minutes. Yet this compressed geography facilitates the transit of roughly one-fifth of the world's total oil trade, equivalent to between 17 and 21 million barrels per day under normal operating conditions. No other single waterway comes close to this concentration of energy throughput.

What makes the strait structurally irreplaceable is the absence of credible alternatives at scale. Saudi Arabia operates the East-West Pipeline (Petroline), which can redirect some crude volumes to Red Sea export terminals, and the UAE operates the Abu Dhabi Crude Oil Pipeline with partial bypass capacity. However, neither infrastructure system can absorb the full volume of Hormuz traffic. Combined, they represent a partial pressure valve, not a substitute.

The other frequently cited alternatives involve rerouting tankers via the Cape of Good Hope. While technically viable, this adds approximately 10 to 15 additional transit days per round voyage for vessels serving Asian refiners, directly compressing effective fleet capacity and adding meaningful freight costs to every barrel delivered.

Beyond crude oil, the strait carries a substantial share of Qatar's LNG export volumes, making it a critical node in global gas markets as well. Disruptions to global LNG supply do not just affect oil-dependent economies; they tighten gas supply into markets that increasingly rely on LNG as a bridge fuel.

| Traffic Category | Normal Conditions |

|---|---|

| Share of global oil trade | ~20% |

| Daily crude throughput | 17-21 million barrels |

| Primary exporters using the strait | Saudi Arabia, Iraq, Kuwait, UAE, Iran |

| LNG exposure | Significant share of Qatari exports |

| Alternative bypass capacity | Partial only (pipelines); full rerouting adds 10-15 days via Cape |

How the 2026 Shipping Disruption Unfolded

The current disruption to Strait of Hormuz commercial shipping did not emerge from a single event. It developed along a sequence of military and diplomatic escalations that began intensifying from 28 February 2026, when coordinated U.S. and Israeli strikes on Iranian positions triggered a retaliatory posture from Tehran that directly threatened commercial vessels transiting the waterway.

The downstream effects on tanker traffic were almost immediate. S&P Global data from early March 2026 indicated that vessel movements through the strait's primary shipping lanes had declined by an estimated 40% to 50% from pre-conflict levels. Ships clustered near the waterway entrance rather than attempting transit, a phenomenon maritime logistics professionals describe as anchorage bunching, where tonnage accumulates at threshold points rather than proceeding through elevated-risk corridors.

The IMF's PortWatch platform classified the Strait of Hormuz as an active major trade disruption event, placing it alongside the Red Sea crisis as a simultaneous pressure point on global maritime supply chains. The oil market disruptions caused by two critical chokepoints experiencing disruption simultaneously represented an unusual and severe stress test for global commodity logistics.

Key timeline of the 2026 Hormuz disruption:

-

28 February 2026: U.S.-Israel strikes on Iranian positions trigger retaliatory threats; commercial tanker traffic begins declining sharply.

-

Early March 2026: S&P Global data records tanker traffic down approximately 40%-50%; anchorage bunching observed at strait entry points.

-

8 April 2026: A fragile ceasefire is declared, but shipping disruptions continue; the gap between political agreement and operational normalcy becomes apparent.

-

Mid-May 2026: Iran announces the strait is open along a "coordinated route," introducing a routing mandate rather than restoring unrestricted international navigation.

-

24 May 2026: U.S. Secretary of State Marco Rubio, speaking after meeting with Indian External Affairs Minister S. Jaishankar, confirms that significant progress has been achieved in negotiations over the preceding 48 hours, and signals that a formal announcement from President Trump may be imminent.

The Critical Distinction Between "Open" and "Fully Normalised"

One of the most consequential misunderstandings in public discourse around the Strait of Hormuz involves treating government declarations of openness as operationally equivalent to genuine shipping normalisation. They are not, and the difference matters enormously to the commercial operators, insurers, and cargo owners who drive actual vessel movements.

When Iran announced the strait was open along a coordinated route, this introduced a routing mandate: ships could transit, but only via pre-approved corridors rather than under the standard freedom of navigation principles embedded in customary international law. From a commercial risk perspective, a routing mandate signals residual sovereign interference with international maritime passage, which underwriters treat as a risk flag regardless of the stated openness.

According to Al Jazeera's analysis, the timeline for the strait becoming genuinely safe for commercial shipping remains uncertain, further illustrating the gap between political declarations and operational reality.

| Status | Operational Reality | Insurance Implication |

|---|---|---|

| Announced Open | Government declaration only | Reduces legal ambiguity; does not eliminate physical risk |

| Coordinated Route Open | Transit via designated corridor only | Routing flexibility limited; underwriters remain cautious |

| Fully Normalised | Unrestricted transit under international law | War risk premiums revert toward baseline |

| Suspended/Closed | Active interdiction or threat environment | Near-total halt; extreme risk surcharges applied |

During active conflict periods, war risk insurance surcharges applied to Hormuz-transiting vessels have historically multiplied by 10 to 20 times their baseline levels. These surcharges are not symbolic; they are embedded directly into the economics of every voyage. When insurance costs rise to this degree, charterers either absorb the additional freight cost, pass it forward to end buyers, or simply avoid the routing altogether.

Industry Insight: Lloyd's of London and the major Protection and Indemnity (P&I) clubs maintain independent risk classification systems for maritime conflict zones. A government's announcement that a waterway is open does not trigger an automatic reclassification. Underwriters require a sustained period of incident-free transits, verified de-escalation of military postures, and formal diplomatic resolution before downgrading elevated risk designations.

What the US-Iran Negotiations Are Actually Trying to Resolve

The diplomatic framework attempting to resolve the Hormuz crisis involves two non-negotiable priorities from Washington's position. These are not peripheral issues to be traded off against each other; they are presented by U.S. officials as parallel requirements for any workable agreement.

The first priority is Iran's nuclear programme. U.S. Secretary of State Marco Rubio reiterated publicly that Iran must permanently forgo the development or possession of nuclear weapons capability. This is the foundational U.S. red line in any negotiated framework, and it has remained consistent regardless of tactical diplomatic progress on other fronts.

The second priority is guaranteed, unrestricted access to the Strait of Hormuz. The U.S. position frames the strait as an international waterway under customary international law, within which no sovereign nation holds the legal authority to impose tolls, enforce routing mandates, or threaten commercial vessels. Rubio characterised Iranian threats against commercial shipping as a violation of international law under any applicable legal framework.

Furthermore, the U.S. position, as reported by PTI on 24 May 2026, specifically stipulates that any agreement must result in a completely open strait without tolls, not merely a partially accessible or conditionally routed corridor. The geopolitical trade tensions surrounding this negotiation extend well beyond the strait itself, with implications for broader regional stability.

Pakistan has emerged as a critical diplomatic intermediary. Islamabad hosted the first direct U.S.-Iran talks since 1979 in the preceding month, and Pakistani Prime Minister Shehbaz Sharif indicated his government was preparing to host a subsequent negotiation round. Pakistan's Army Chief held direct talks with senior Iranian leadership in Tehran as recently as late May 2026.

Beyond Pakistan, U.S. President Trump held direct phone consultations with leaders from Saudi Arabia, Qatar, Turkey, Egypt, the UAE, Jordan, Bahrain, and Pakistan on the Saturday preceding Rubio's 24 May press conference. This multilateral engagement reflects the reality that Gulf states have their own acute stake in Hormuz normalisation; for nations like Saudi Arabia, Kuwait, and the UAE, the strait is not merely a global energy issue but the primary exit route for their own crude exports.

India's Energy Security Equation and the Hormuz Exposure Problem

India's position in the Hormuz crisis illustrates a structural vulnerability that extends well beyond the current conflict cycle. As one of the world's largest crude oil importers, India routes a substantial share of its energy supply through the strait under normal conditions. Every day of disruption translates into real cost increases, supply uncertainty, and pressure on foreign exchange reserves used to finance energy imports.

Indian External Affairs Minister S. Jaishankar, speaking after his meeting with Rubio on 24 May 2026, articulated India's dual concern: ensuring safe and unimpeded maritime commerce, and ensuring that global energy prices remain accessible for sustained economic growth. These are not merely diplomatic talking points; they reflect the direct exposure of India's manufacturing sector and consumer economy to Persian Gulf supply conditions.

India's strategic response has been to accelerate a supply diversification programme that was already underway before the current crisis. Jaishankar noted a very significant uptick in India's energy imports from the United States, framing this as a deliberate rebalancing rather than an emergency measure. The underlying policy logic is straightforward: multi-vector energy sourcing reduces the leverage any single geographic corridor holds over India's economic stability.

This approach aligns with a broader principle that energy markets must remain free from distortion or constraint, and that maintaining competitive global energy pricing is a prerequisite for sustained world economic growth, not merely a benefit for importing nations.

The next major ASX story will hit our subscribers first

The Economic Stakes of a Prolonged Closure

The scale of potential economic disruption from a sustained Hormuz closure is difficult to overstate. A 40% to 50% reduction in strait throughput removes the equivalent of approximately 7 to 10 million barrels per day from accessible global oil supply, a shock comparable in magnitude to the 1973 Arab oil embargo.

Historical patterns demonstrate that even credible escalation threats produce significant price volatility in Brent crude and WTI benchmarks, with intraday spikes of 5% to 15% observed during previous Hormuz tension episodes. Consequently, a full closure scenario carries far more severe implications, as the crude oil market overview for 2025 already highlighted the fragility of supply-side fundamentals heading into this period.

| Disruption Scenario | Estimated Oil Price Impact | Estimated Global GDP Effect |

|---|---|---|

| Partial closure (40-50% reduction, 1-3 months) | +$15 to +$30/barrel | -0.3% to -0.5% |

| Full closure (1 month) | +$40 to +$60/barrel | -0.8% to -1.2% |

| Prolonged full closure (3+ months) | +$60 to +$100+/barrel | -1.5% to -2.5% |

| Negotiated full reopening | -$10 to -$20/barrel relief | Positive stabilisation |

Note: These figures represent indicative analytical estimates based on historical disruption precedents and should not be treated as precise forecasts. Actual market outcomes will depend on OPEC+ responses, strategic reserve releases, and the pace of diplomatic resolution.

The secondary effects on trade finance are frequently underappreciated. Letters of credit and commodity financing instruments tied to Hormuz-routed cargo face elevated counterparty risk during disruption periods, creating knock-on friction in the banking systems that underpin global commodity trade. The oil price shock dynamics already observed in 2025 have, in addition, pre-conditioned shipowners operating very large crude carriers (VLCCs) to face fleet deployment dilemmas that reduce effective global tanker capacity independent of the physical closure itself.

What Full Normalisation Actually Requires

A genuine and durable Strait of Hormuz opening for commercial shipping involves resolving a layered set of interdependent conditions, none of which can substitute for the others:

-

A verified nuclear framework agreement with credible international monitoring mechanisms acceptable to both the U.S. and the relevant treaty bodies.

-

Formal Iranian commitment to unrestricted international navigation, explicitly removing any routing mandate, toll structure, or threat posture toward commercial vessels.

-

Military posture de-escalation from all parties, reducing U.S. and allied naval presence in the Persian Gulf to levels consistent with normal freedom of navigation operations.

-

War risk insurance reclassification by Lloyd's of London and the major P&I clubs, triggered only after a sustained period of verified incident-free transits, not by government announcement alone.

-

A regional security framework that durably reduces the probability of future closure threats, providing the forward visibility that commercial operators and long-term energy contracts require.

Until all five conditions are met, the gap between political announcements and operational shipping normalcy will persist. Safety4Sea has confirmed Iran's declaration that the strait is completely open; however, experienced maritime operators know that an outline framework and a fully functioning international shipping lane are separated by a significant distance, measured not in kilometres but in verified de-escalation benchmarks.

Structural Takeaway: The 2026 Hormuz disruption has accelerated energy diversification strategies that will outlast the immediate crisis. India's expanded U.S. energy import programme, Gulf states' investment in bypass infrastructure, and broader supply chain resilience investments represent lasting structural shifts in global energy trade architecture, regardless of when the strait fully normalises.

Frequently Asked Questions

What share of global oil trade passes through the Strait of Hormuz?

Under normal conditions, approximately 20% of global oil trade transits the strait daily, representing 17 to 21 million barrels, making it the world's single most critical oil chokepoint.

When did the current Hormuz shipping disruption begin?

Disruptions escalated sharply from 28 February 2026, following military strikes that triggered Iranian retaliatory actions targeting commercial shipping in the waterway.

Is the Strait of Hormuz open for commercial shipping now?

As of late May 2026, the situation remains unresolved. Iran announced openness along a coordinated routing corridor, but maritime risk assessors and live vessel tracking data indicate the corridor has not yet returned to full, unrestricted international transit standards.

What are the main sticking points in U.S.-Iran negotiations?

The two primary issues are Iran's nuclear programme, specifically the permanent prevention of Iranian nuclear weapons capability, and the restoration of fully unrestricted, toll-free commercial access to the Strait of Hormuz under international maritime law.

Which economies face the greatest exposure to Hormuz disruptions?

India, China, Japan, South Korea, and several European economies represent the highest-exposure energy importers. Gulf exporters including Saudi Arabia, Kuwait, the UAE, and Iraq are also severely affected, as the strait is their primary crude export corridor.

Want to Know Which ASX Commodities Stand to Gain From Hormuz Disruptions?

Global energy shocks like the Strait of Hormuz crisis routinely reshape commodity markets and create significant opportunities in ASX-listed resource stocks — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment a significant mineral or energy discovery is announced on the ASX, ensuring subscribers can act ahead of the broader market. Explore historic discoveries and their returns to understand the scale of opportunity, and begin your 14-day free trial today to secure a genuine market-leading advantage.