May 23, 2026

Global energy markets face their most significant vulnerability through the concentration of critical supply chains within strategic maritime chokepoints. These narrow waterways serve as essential arteries for international energy trade, yet their susceptibility to geopolitical disruption creates cascading risks throughout the global economy. Understanding how regional conflicts transform into worldwide supply constraints requires examining the complex interplay between maritime logistics, insurance markets, and diplomatic tensions that govern energy security, particularly regarding strait of hormuz lpg disruption.

Strategic Chokepoint Dependencies in Global Energy Trade

Geographic Vulnerabilities That Shape Energy Markets

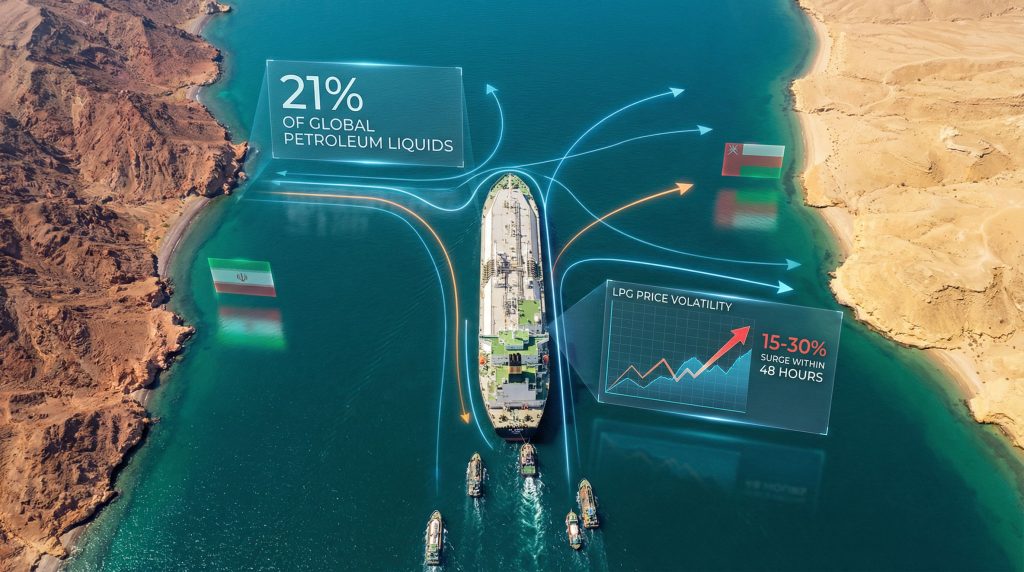

The world's energy infrastructure relies heavily on a handful of strategic waterways that handle disproportionate volumes of international petroleum trade. The Strait of Hormuz exemplifies this concentration risk, processing approximately 21% of global petroleum liquids daily through a passage measuring just 21 nautical miles at its narrowest point. This geographic bottleneck creates unique vulnerabilities that alternative routes cannot easily address due to economic and logistical constraints.

Unlike other major shipping lanes, the Persian Gulf region lacks viable alternative export routes for the six Gulf Cooperation Council nations that collectively control nearly half of OPEC's proven reserves. Furthermore, the Suez Canal handles roughly 12-13% of global seaborne trade but faces design limitations for LPG carrier transits, while the Panama Canal processes only 5-6% of global oil trade with significant time penalties for Asian-bound shipments.

Modern LPG carriers transiting these chokepoints typically carry 40,000-85,000 cubic meters of cargo, with larger vessels reaching 138,000 cubic meters capacity. During normal operations, transit times through strategic straits range from 6-12 hours, however, disruptions can immobilise dozens of vessels for extended periods, creating immediate supply constraints in consuming markets.

Insurance Market Dynamics During Supply Disruptions

Maritime insurance markets serve as the primary transmission mechanism through which geopolitical tensions convert into supply chain disruptions. War risk underwriting operates on accelerated timelines, with syndicate decisions occurring within 2-4 hours of initial incident classification. This rapid response creates immediate operational impacts for shipping companies and energy traders.

During conflict escalation, insurance premiums typically increase 200-400% above baseline rates, with war risk coverage becoming mandatory for strategic waterway transits. Consequently, the cost structure fundamentally alters shipping economics:

- Standard transit costs: $15,000-$30,000 per vessel passage

- War risk insurance during disruptions: $50,000-$150,000 per passage

- Potential loss exposure: $3-8 million per vessel including cargo value

- Vessel idle costs during delays: $25,000-$50,000 per day

Historical data from the 2019 Fujairah attacks demonstrates these dynamics in practice. Insurance premiums jumped from 0.5% to 3-4% of cargo value within 48 hours, while 15-20 vessels diverted from the region within 72 hours. Similarly, the 2022-2023 Red Sea escalation showed similar patterns, with transit volumes dropping 40-50% within one week as premiums rose 300-500%.

Regional Market Vulnerabilities and Response Mechanisms

Asian energy markets demonstrate the highest vulnerability to strait of hormuz lpg disruption due to supply concentration and limited storage infrastructure. Approximately 60-65% of Asian LPG imports originate from Persian Gulf producers, creating direct exposure to transit disruptions. Moreover, alternative sourcing from the United States, Russia, or Australia requires 20-45 day transit times compared to 15-20 days from Gulf suppliers.

Receiving terminal infrastructure in major Asian markets operates at 70-85% capacity utilisation during normal periods, limiting inventory buffers available during supply interruptions. This constraint amplifies price volatility when supply disruptions occur, as terminals cannot easily absorb extended delivery delays without affecting end-user supplies.

For instance, the following table illustrates comparative supply route analysis:

| Supply Route | Transit Time | Cost Premium | Capacity Constraints |

|---|---|---|---|

| Persian Gulf → Asia | 15-20 days | Baseline | High volume, single chokepoint |

| US Gulf → Asia via Panama | 25-30 days | +$100-200k fuel | Canal size limitations |

| Russian Arctic (seasonal) | 35-40 days | Variable | Weather dependent |

| African suppliers via Suez | 30-35 days | +15-25% | Limited production capacity |

When big ASX news breaks, our subscribers know first

Market Response Patterns and Price Discovery Mechanisms

Immediate Price Volatility During Transit Disruptions

LPG markets exhibit predictable price response patterns when strategic waterway disruptions occur. Historical analysis shows Asian LPG spot prices typically surge 8-15% within the first week of conflict escalation, with intraday volatility increasing substantially when markets reopen following weekend geopolitical events.

During the 2019 Fujairah incident, Asian LPG propane prices increased from $310 per metric ton to $335-345 per metric ton within 48 hours, representing a $25-35 per metric ton premium. European markets showed smaller but significant increases due to greater supply diversification and higher baseline storage levels.

Price discovery mechanisms during disruptions follow established patterns. Firstly, immediate futures market repricing occurs within hours of incident reports. Subsequently, spot market premium emergence develops as buyers compete for available cargoes. Additionally, regional price differential expansion occurs between constrained and alternative supply sources. Finally, storage draw activation occurs by governments and major consumers.

The baseline LPG pricing structure across major markets reflects these vulnerability differentials:

- Asian LPG (CFR basis): $250-400 per metric ton

- European LPG: $300-450 per metric ton (5-15% premium to Asia)

- US Gulf LPG (FOB): $200-300 per metric ton

Industrial Response Protocols and Demand Management

Refiners and major industrial consumers maintain established protocols for managing supply disruptions through production adjustments and alternative sourcing activation. Indian refiners, as major LPG consumers, have demonstrated systematic responses during previous Middle East supply interruptions by increasing domestic production capacity utilisation and activating emergency supply agreements.

Industrial demand management follows priority allocation hierarchies during severe disruptions. Essential residential cooking fuel maintains highest priority, while critical industrial processes receive secondary allocation. Furthermore, power generation backup systems are activated as needed, and non-essential commercial applications face potential restrictions.

"Strategic storage reserves serve as the primary buffer against short-term supply disruptions, but their effectiveness depends on advance preparation and coordinated release protocols."

Large petrochemical complexes typically maintain 15-30 day inventory buffers for critical feedstocks. However, extended disruptions require production curtailments or alternative feedstock substitution. The economic threshold for activating emergency production protocols occurs when procurement costs exceed 150-200% of historical averages for sustained periods.

Long-term Strategic Infrastructure and Energy Security

Alternative Route Development and Investment Requirements

Reducing strategic chokepoint dependencies requires substantial infrastructure investments in alternative routing capacity and regional storage systems. Pipeline development economics often compete unfavourably with maritime transport due to the high capital requirements and geopolitical risks associated with cross-border infrastructure projects.

The most viable diversification strategies focus on several key areas. Strategic storage facility expansion in major consuming regions represents a critical component. Additionally, regional supply hub development helps reduce single-source dependencies. Furthermore, alternative production capacity in geographically diverse locations provides essential resilience. Finally, enhanced maritime route flexibility through vessel size optimisation offers operational advantages.

Japan's post-Fukushima energy diversification strategy provides a relevant framework for reducing import dependencies while maintaining economic competitiveness. The approach emphasises portfolio diversification across supply sources, transit routes, and storage infrastructure rather than complete self-sufficiency.

Risk Management Frameworks for Energy Security

Effective energy security planning treats supply disruptions as operational certainties rather than exceptional risks. This approach requires systematic preparation across multiple dimensions including diplomatic coordination, emergency logistics protocols, and market stabilisation mechanisms.

Key risk indicators for energy traders include various warning signs. Vessel clustering patterns in strategic waterways indicate potential bottlenecks. Similarly, insurance premium spikes above historical norms suggest elevated risk assessment. Moreover, naval activity increases in critical transit zones provide early warnings. Additionally, diplomatic communication deterioration between regional powers signals potential disruptions.

Early warning systems rely on multi-source intelligence gathering including satellite imagery of vessel traffic, insurance market signals, and diplomatic communications monitoring. The integration of these information sources enables predictive risk assessment rather than reactive crisis management, addressing critical minerals energy security concerns proactively.

Economic Impact Assessment and Vulnerability Modelling

The cascading effects of strategic waterway disruptions extend far beyond immediate energy price increases to encompass broader economic impacts including currency stability, trade balance adjustments, and industrial production constraints. Energy-import-dependent economies face disproportionate vulnerabilities during extended supply interruptions, potentially exacerbating oil market volatility across global markets.

GDP impact modelling suggests that a 30-day complete closure of a major energy transit chokepoint could reduce global economic growth by 0.3-0.7 percentage points annually, with concentrated impacts in Asian and European markets. The economic vulnerability index varies significantly by country based on import dependency ratios and strategic storage availability.

Currency stability implications emerge through increased energy import costs that pressure current account balances. Countries with limited foreign exchange reserves face particular challenges during extended periods of elevated energy prices combined with supply uncertainty, compounding energy export challenges.

"Energy chokepoint disruptions typically accelerate energy transition investments by 18-24 months as governments prioritise supply security over cost optimisation."

The next major ASX story will hit our subscribers first

Future Energy Trade Pattern Evolution

Technology Innovation and Distribution System Transformation

Strategic waterway vulnerabilities are driving innovation in energy storage, distribution technologies, and alternative supply chain architectures. Advanced storage systems, including underground salt cavern facilities and floating storage units, provide enhanced flexibility for managing supply disruptions.

Technological developments in modular LNG production and distributed storage systems enable greater geographic diversification of both supply sources and storage capacity. These innovations reduce dependence on large-scale centralised infrastructure that creates single points of failure during geopolitical disruptions.

The integration of renewable energy sources with strategic storage systems provides additional resilience against fossil fuel supply disruptions, supporting renewable energy integration initiatives across multiple sectors. However, the transition timeline extends across multiple decades for complete energy security transformation.

Regional Supply Agreement Restructuring

Energy trade relationships are evolving toward greater diversification and flexibility as consuming nations seek to reduce strategic chokepoint dependencies. Bilateral supply agreements increasingly incorporate force majeure clauses optimised for geopolitical disruptions and alternative sourcing mechanisms.

The restructuring emphasises several key elements. Multi-source supply contracts replace single-supplier relationships. Additionally, flexible delivery terms accommodate alternative routing during disruptions. Furthermore, emergency logistics coordination protocols between suppliers and consumers enhance resilience. Finally, shared strategic storage arrangements among allied nations provide collective security benefits.

These agreements reflect recognition that energy security requires treating supply disruptions as operational realities requiring systematic preparation rather than exceptional circumstances addressed through crisis management. In addition, the approach acknowledges trade war impacts on global supply chains and the need for comprehensive contingency planning.

According to the Indian Express, the Strait of Hormuz's strategic importance extends beyond immediate energy supplies to encompass broader geopolitical implications for regional stability and international maritime law.

Furthermore, analysis from S&P Global demonstrates how tanker traffic disruptions in strategic waterways create immediate market responses across global energy trading platforms.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and historical patterns. Energy market dynamics involve substantial uncertainties including geopolitical developments, technological changes, and regulatory modifications that may materially affect actual outcomes. Readers should conduct independent research and consult qualified advisors before making investment or policy decisions based on this information.

Ready to Navigate Resource Market Volatilities?

Discovery Alert's proprietary Discovery IQ model delivers real-time insights on significant ASX mineral discoveries, transforming complex market data into actionable trading opportunities during periods of global supply chain uncertainty. Discover how historic mineral discoveries have generated substantial returns by exploring Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of volatile energy and resource markets.