May 22, 2026

The Economics of Underground Copper: Why Ownership Structure Defines National Wealth

Deep underground copper mining is one of the most capital-intensive industrial endeavours on earth. Unlike open-pit operations where ore can be accessed relatively quickly after permitting, underground shaft-sinking projects demand years of geological preparation, billions in upfront capital, and extraordinary engineering precision before a single tonne of copper reaches the surface. The Zambia stake in Mingomba copper mine reflects these enormous financial stakes, and for resource-rich African nations, the percentage points of equity held in these ventures can translate directly into generational fiscal outcomes.

It is within this context that the evolving ownership dynamic at Zambia's Mingomba copper project carries significance well beyond its headline numbers. The interplay between sovereign participation, foreign capital, and technological innovation at Mingomba reflects broader tensions reshaping how African nations approach their mineral endowments in the age of the energy transition.

When big ASX news breaks, our subscribers know first

Understanding the Zambia Stake in Mingomba Copper Mine

Zambia's current 20% equity position in the Mingomba project, held through state investment vehicle ZCCM Investments Holdings (ZCCM-IH), was established when U.S.-based KoBold Metals acquired its 80% controlling interest in late 2022. That transaction superseded a prior joint venture arrangement between EMR Capital and ZCCM-IH, bringing a technologically differentiated operator into what is already considered the most significant copper discovery in Zambia in recent decades.

The Mingomba deposit, also known as the Konkola West project, sits within Zambia's Copperbelt region, a geological formation that has produced copper for over a century and continues to host some of the world's highest-grade stratiform copper mineralisation. Stratiform deposits of this type, where copper mineralisation follows sedimentary rock layers across large horizontal extents, tend to offer favourable grade continuity and predictable mining geometry compared to intrusive or porphyry-hosted systems.

The current ownership picture is straightforward:

| Stakeholder | Current Equity | Proposed Equity | Role |

|---|---|---|---|

| KoBold Metals | 80% | 75% (if diluted) | Lead developer and operator |

| ZCCM-IH (Zambia) | 20% | 25% (proposed) | State equity participant |

| Status | Active | Under consideration | No formal negotiations disclosed |

The proposal to raise ZCCM-IH's stake to 25% was publicly signalled by ZCCM-IH chief executive Phesto Musonda at an inauguration ceremony held on April 28, 2026, with the announcement framed around the objective of increasing economic returns for Zambia. Critically, no formal negotiations between ZCCM-IH and KoBold Metals had been disclosed as of that date, placing the proposal firmly in the category of political signalling rather than advanced commercial dialogue.

Scale, Capital, and Production: What Mingomba Actually Represents

A Project Defined by Its Numbers

The Mingomba project's fundamental characteristics make it exceptional by any regional measure:

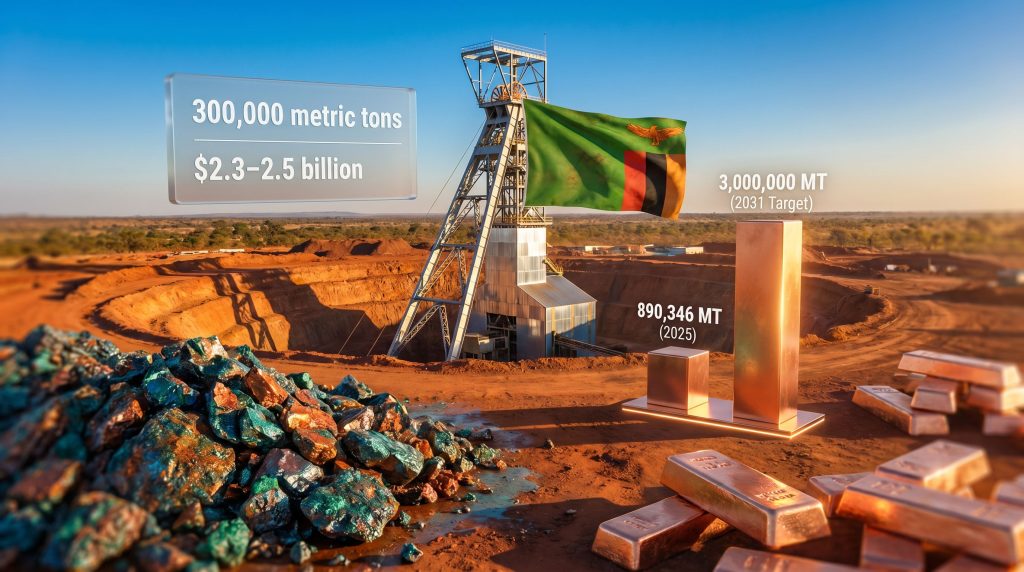

- Total capital investment estimate: $2.3 billion to $2.5 billion

- Annual copper concentrate production target: approximately 300,000 metric tons

- Expected production commencement: early 2030s

- Development trigger: shaft-sinking operations launched in late April 2025

To contextualise the capital commitment, $2.3 to $2.5 billion positions Mingomba among the most capital-intensive mining developments currently active across all of sub-Saharan Africa. For reference, the capital intensity per annual tonne of capacity at these estimates sits broadly in line with other recent large-scale underground copper projects globally, though deep shaft mines typically command premium development costs relative to open-pit or shallow underground equivalents. In addition, understanding the copper price growth drivers at play globally helps contextualise why commitments of this scale are being made now.

Shaft-Sinking: The Technical Gateway to Production

Shaft-sinking is often misunderstood outside specialist circles. It is the process of excavating vertical access shafts from surface to orebody depth, enabling mine ventilation, personnel access, ore hoisting, and materials transport. For deep Copperbelt deposits, shafts may extend hundreds to over a thousand metres below surface, requiring specialised ground support, concrete lining, and precision blasting techniques that distinguish this work from conventional civil construction.

The commencement of shaft-sinking at Mingomba in April 2025 was a genuine development milestone. Unlike earlier-stage activities such as drilling programmes or feasibility studies, shaft-sinking commits physical infrastructure and substantial capital. It is the point at which a project transitions from a paper asset to a physical mine under construction, and it was significant enough to attract the attendance of Zambian President Hakainde Hichilema at the inauguration ceremony.

Mingomba's Position in Zambia's National Output Ambition

Zambia produced approximately 890,346 metric tons of copper in 2025. The national target is 3 million metric tons per year by 2031, implying a 237% increase in output over six years. Mingomba's projected 300,000 metric tons per year would represent roughly 10% of the 2031 target and approximately 33% of the country's entire 2025 production.

| Metric | 2025 Baseline | 2031 Target | Growth Required |

|---|---|---|---|

| National copper output | ~890,346 metric tons | 3,000,000 metric tons | ~237% increase |

| Mingomba contribution | 0 (pre-production) | ~300,000 metric tons | ~10% of national target |

| Output gap (ex-Mingomba) | N/A | ~1,810,000 metric tons | Requires multiple additional projects |

Achieving the 2031 target will require Mingomba's successful and on-schedule delivery alongside parallel capacity expansions at existing operations and the advancement of multiple other development-stage projects across the Copperbelt. The ambition is substantial, and the execution complexity should not be underestimated.

KoBold Metals: AI-Driven Exploration Meets Underground Reality

What Makes KoBold Different

KoBold Metals is not a conventional mining company. Its foundational methodology applies machine learning algorithms and large-scale geological dataset analysis to identify high-probability mineral deposits that traditional exploration techniques might overlook or deprioritise. The company targets locations where subsurface mineralisation patterns can be inferred from geophysical, geochemical, and satellite datasets, then validates those predictions through targeted drilling.

This approach is theoretically powerful in regions like the Zambian Copperbelt, where decades of historical exploration data exist but may not have been fully integrated into predictive geological models. Furthermore, the ability to synthesise legacy data with modern remote sensing outputs could meaningfully reduce the exploration risk that typically consumes substantial capital before a project reaches the development decision stage.

KoBold counts prominent investors including Bill Gates and Jeff Bezos among its backers, reflecting confidence in both the technology platform and the long-term copper demand thesis underpinning it. However, the company remains privately held, which creates a structural transparency gap that is particularly consequential at Mingomba's development scale.

The Transparency Challenge

As a private entity, KoBold Metals is not subject to the continuous disclosure obligations that govern publicly listed mining companies on exchanges such as the ASX, TSX, or LSE. This means:

- No publicly available mineral resource or ore reserve statements compliant with international reporting standards (JORC, NI 43-101, or SAMREC)

- No bankable feasibility study accessible to external analysts or investors

- No detailed mine plan or production schedule disclosed to the market

- Limited visibility on the financing architecture underpinning the $2.3 to $2.5 billion capital commitment

Analytical Note: The absence of independently verified resource statements makes external assessment of Mingomba's production targets, capital cost estimates, and project timeline reliability difficult. Investors and analysts relying on publicly available information should treat forward-looking statements about Mingomba's output profile with appropriate caution until formal technical disclosures are made.

KoBold's Africa head, Mfikeyi Makayi, has indicated that the company can fund the current development phase independently while simultaneously engaging potential co-investors and strategic partners. This dual-track approach, advancing construction while exploring external financing options, is common in large-scale mining projects but adds a layer of uncertainty regarding the ultimate capital structure when full construction acceleration is required.

Comparing Zambia's Stake Ambition Against African Ownership Models

A Continent-Wide Perspective on State Participation

Resource nationalism in Africa exists on a spectrum, ranging from passive free-carry arrangements to majority state ownership. Zambia's proposed 25% ZCCM-IH stake sits at the moderate end of this spectrum, reflecting a deliberate calibration between revenue maximisation and investor confidence preservation. Furthermore, African mining finance trends suggest that this kind of incremental approach is becoming increasingly common across the continent.

| Country | State Entity | Typical Equity Range | Participation Model |

|---|---|---|---|

| Zambia | ZCCM-IH | 20% to 25% (proposed) | Passive to semi-active |

| Democratic Republic of Congo | Gécamines | 10% to 20% | Royalty and equity hybrid |

| Botswana | Debswana (50/50 joint venture) | 50% | Full partnership |

| Tanzania | STAMICO | 16% minimum | Mandatory free-carry |

| Ghana | Government | 10% | Free-carry model |

Zambia's incremental approach, seeking five additional percentage points rather than demanding majority control, is strategically calculated. It signals sovereign ambition without crossing the threshold that typically triggers investor reassessment of political risk and capital allocation priorities. The five percentage point increment may appear modest, but in the context of a project with $2.3 to $2.5 billion in total capital value, the long-term dividend and fiscal implications are material.

What Five Percent Actually Means Financially

The monetary significance of the proposed stake increase operates across multiple channels simultaneously:

- Equity dividends: A 25% stake versus 20% increases Zambia's proportional claim on distributable profits once Mingomba reaches production and recoups its capital investment

- Corporate income tax and royalties: These flows are independent of equity stake size and represent Zambia's most immediate fiscal capture mechanism during operational years

- Employment multipliers and local procurement: Both generate economic activity that is not captured in equity return calculations but contribute significantly to GDP and tax revenues

- Sovereign leverage: A larger equity position provides ZCCM-IH with greater board influence and information access, improving Zambia's ability to monitor project execution and enforce contractual obligations

Risks That Define the Negotiation Landscape

Why Timing and Sequencing Matter

The public announcement of Zambia's stake ambition at a project inauguration ceremony, rather than through a formal regulatory or commercial filing, deserves scrutiny. Making ownership aspirations public before negotiations commence serves a political purpose, demonstrating to domestic audiences that the government is actively pursuing maximum economic benefit from mineral assets. However, it also alerts KoBold Metals and potential co-investors to the state's intentions before a negotiating framework has been established, potentially affecting their assessment of the regulatory and commercial environment.

Key risks surrounding the proposed stake increase include:

- No formal negotiation framework: As of late April 2026, the proposal exists at the signalling stage only, with no disclosed timeline for advancing to commercial discussions

- KoBold's agreement required: Any equity restructuring must be negotiated with the operator, whose position on dilution or third-party introduction is not publicly known

- Construction timeline sensitivity: Equity renegotiations conducted during active shaft-sinking create potential for project delays if commercial disagreements stall decision-making

- Financing interdependencies: The structure of any co-investor arrangements KoBold is pursuing may complicate or constrain the mechanics of state stake increases

- Capex inflation risk: The $2.3 to $2.5 billion estimate is based on engineering assumptions that will be refined as shaft-sinking progresses, with cost overruns a historically common feature of deep underground mining projects

The Investor Confidence Equation

Zambia's investment climate has improved meaningfully under President Hichilema's administration, with mining fiscal terms stabilised and engagement with international capital markets deepened following the country's debt restructuring process. This positive trajectory creates a delicate balance: asserting greater resource ownership is a rational sovereign interest, but the manner in which that assertion is pursued will be observed closely by other operators and potential investors considering capital allocation to Zambian projects.

The Zambia stake in Mingomba copper mine negotiation, when it formally commences, will function as a reference case for how Zambia manages the tension between developmental participation and investor relationship management. Consequently, the outcome will resonate well beyond this single project.

The next major ASX story will hit our subscribers first

Copper's Structural Role in Zambia's Economic Future

Copper is not merely an export commodity for Zambia. At approximately 17% of GDP in 2024, the metal is woven into the fundamental architecture of the national economy in ways that few single commodities are for any country. Revenue from copper finances public services, services government debt, and anchors foreign exchange reserves.

The global structural case for copper demand growth is well established. Electric vehicle powertrains require three to four times more copper than internal combustion engine equivalents. Grid-scale battery storage systems, solar photovoltaic installations, and offshore wind infrastructure all represent copper-intensive applications expanding rapidly as the energy transition accelerates. Analysts across major commodity research houses project sustained copper demand growth through the 2030s, with a looming copper supply crunch potentially widening the gap between demand and available production capacity.

Zambia's geological position within this demand narrative is genuinely advantageous. The Copperbelt hosts some of the world's highest-grade copper deposits, with mineralisation characteristics that support competitive cash costs once production infrastructure is established. Securing maximum economic benefit from flagship projects like Mingomba is not simply a political aspiration; it is a rational economic imperative for a country whose fiscal trajectory depends on copper sector performance. For context, a major copper project comparison reveals just how competitively positioned Zambia's assets are on the global stage.

Key Milestones to Watch

For investors and analysts tracking the Zambia stake in Mingomba copper mine developments, the following indicators will be most informative:

- Formal announcement of equity renegotiation discussions between ZCCM-IH and KoBold Metals

- Release of a mineral resource statement, technical study, or bankable feasibility study by KoBold

- Identification and public announcement of co-investment or project financing partners

- Quarterly progress reporting on shaft-sinking advancement and construction metrics

- Annual Zambian national copper production figures against the 3 million tonne 2031 benchmark

- Any revisions to the $2.3 to $2.5 billion capital estimate as engineering advances

The broader African mining investment community will be watching these developments with considerable interest. Mingomba's trajectory, from exploration discovery through equity negotiation to production ramp, offers a real-time case study in how resource-rich African nations can pursue sovereign economic ambitions while maintaining the investor relationships necessary to fund development at scale. In addition, those evaluating copper investment strategies will find Mingomba's progress a compelling indicator of what sovereign-backed projects can achieve.

Frequently Asked Questions: Zambia's Stake in the Mingomba Copper Mine

What percentage does Zambia currently own in the Mingomba copper mine?

Zambia holds a 20% equity stake in the Mingomba copper project through ZCCM Investments Holdings. The remaining 80% is controlled by KoBold Metals as the lead operator and developer.

Has the proposed 25% stake increase been formally agreed?

No. As of April 2026, ZCCM-IH's chief executive publicly indicated the intention to raise Zambia's stake to 25%, but no formal negotiations with KoBold Metals had been announced. The proposal remains at the signalling stage.

What is KoBold Metals and why is it developing Mingomba?

KoBold Metals is a U.S.-based mineral exploration company that applies artificial intelligence and geological data modelling to identify high-probability mineral deposits. Backed by prominent investors including Bill Gates and Jeff Bezos, KoBold acquired its 80% controlling interest in Mingomba in late 2022, bringing both capital and a technologically differentiated exploration methodology to the project.

When will Mingomba begin producing copper?

Based on current development timelines communicated by KoBold's Africa leadership, copper production from Mingomba is expected to commence in the early 2030s, following the completion of shaft-sinking operations and full mine construction.

How much will it cost to develop the Mingomba mine?

Total capital investment is estimated at between $2.3 billion and $2.5 billion, positioning Mingomba as one of the largest single mining capital commitments currently active in sub-Saharan Africa.

How significant is Mingomba to Zambia's production targets?

Zambia aims to increase national copper output from approximately 890,346 metric tons in 2025 to 3 million metric tons per year by 2031. Mingomba's projected annual output of 300,000 metric tons would contribute roughly 10% of that national target and represents approximately a third of the country's entire current copper production capacity.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements regarding production timelines, capital costs, and equity negotiations are subject to material uncertainty. Independent verification of technical claims should be sought before making investment decisions.

Want to Track the Next Major Copper Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's discoveries page, then start your 14-day free trial to position yourself ahead of the market.