June 29, 2026

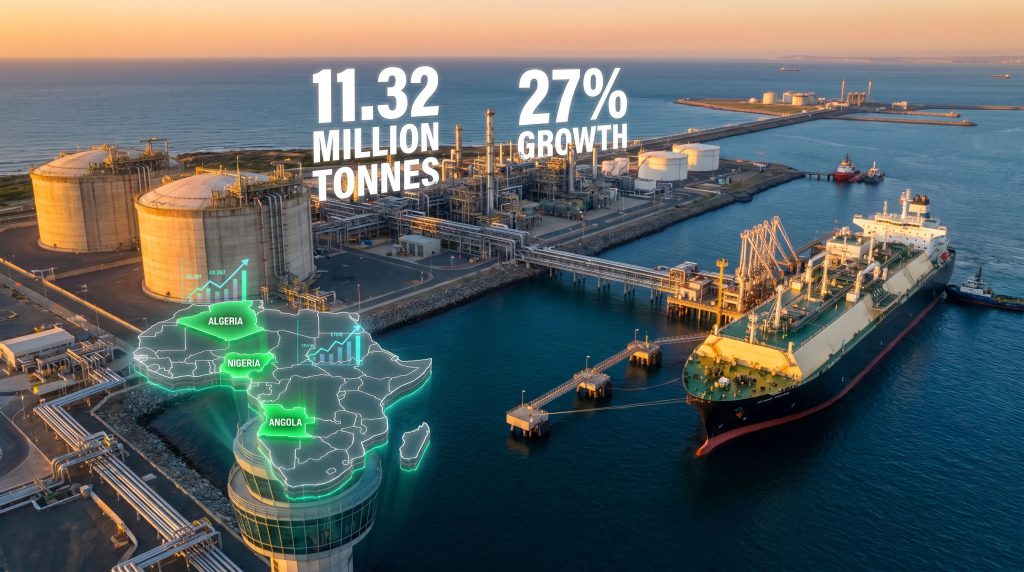

Africa's LNG exports rise dramatically as global energy markets face unprecedented disruption from geopolitical tensions and supply chain vulnerabilities. The continent's liquefied natural gas sector demonstrates remarkable resilience, achieving 11.32 million tonnes in Q1 2026—a substantial 27% year-over-year increase that positions African producers as essential components of international energy security infrastructure. This transformation reflects broader shifts in global energy architecture, where traditional supply dependencies give way to diversified sourcing strategies prioritising security over pure cost optimisation.

Continental Market Dynamics Reshape Global LNG Architecture

Africa's strategic position in global energy markets strengthens considerably as European and Asian buyers confront supply chain vulnerabilities that expose decades of concentrated sourcing dependencies. The continental export architecture reveals concentrated production among five leading nations controlling 88% of total African LNG volumes. Nigeria commands the largest market share with 4.99 million tonnes, followed by Algeria's 2.04 million tonnes, Angola's 1.25 million tonnes, Mozambique's 914,000 tonnes, and Equatorial Guinea's 735,000 tonnes.

Furthermore, market volatility indicators suggest individual country-specific factors rather than continental-wide constraints drive performance variations. Export changes range from -8% to +1,574% among major producers, reflecting diverse project development phases, maintenance scheduling, and infrastructure commissioning timelines. Nigeria's 45% growth contrasts sharply with Algeria's 8% decline, illustrating how facility-specific operational considerations override macro-level sector trends.

The sector achieved 9.96% of global LNG trade, marking a significant shift from historical market positions where African suppliers functioned primarily as secondary or swing producers. This performance demonstrates the continent's capacity to absorb displaced demand from traditional suppliers while maintaining competitive cost structures.

When big ASX news breaks, our subscribers know first

Infrastructure Modernisation Accelerates Production Capacity

Continental LNG infrastructure undergoes comprehensive transformation through three primary mechanisms: advanced liquefaction technology deployment, floating LNG system installation, and cross-border partnership development. These modernisation initiatives enable African producers to capitalise on global supply disruptions while positioning for sustained market expansion beyond immediate geopolitical opportunities.

Algeria's Strategic Infrastructure Investment

The Arzew gas liquefaction complex represents Africa's most significant capacity expansion initiative, with SOMIZ and Sinopec collaboration targeting doubled production capacity through 2027. The project exemplifies international technology transfer patterns where Chinese engineering expertise combines with African resource endowments to enhance competitive positioning. Current maintenance activities temporarily reduced Q1 2026 output by 8%, but systematic infrastructure improvements promise substantial medium-term capacity additions.

Liquefaction technology advancements focus on thermal efficiency optimisation, compression train enhancement, and auxiliary system performance improvements. The partnership structure indicates broader Chinese energy infrastructure investment strategies across African markets, providing capital mobilisation and technical capabilities that domestic resources alone cannot achieve within competitive timeframes.

Floating LNG Technology Deployment

Congo's 98% export growth to 273,000 tonnes demonstrates floating LNG technology's strategic advantages in monetising remote gas reserves. FLNG systems eliminate complex onshore infrastructure requirements while reducing development timelines and capital expenditures compared to traditional facilities. This technology proves particularly valuable for nations lacking established pipeline networks or deepwater port capabilities.

FLNG deployment enables faster production ramp-up cycles and enhanced operational flexibility during demand fluctuations. The modular system approach supports scalable capacity additions as market conditions justify additional investment, providing superior risk management compared to large-scale fixed infrastructure projects with extended development horizons.

Cross-Border Development Models

The Grand Tortue Ahmeyim project exemplifies innovative cross-border cooperation frameworks that optimise resource development efficiency while reducing individual country risk exposure. Mauritania and Senegal's joint venture with BP and Kosmos Energy achieved commercial production in 2025, generating 703,000 tonnes during Q1 2026 compared to just 42,000 tonnes in the previous year.

This 1,574% growth trajectory illustrates how shared infrastructure investments accelerate commercialisation timelines while distributing development costs across multiple stakeholders. The subsea infrastructure model connecting offshore reserves to centralised processing facilities provides a template for similar projects across maritime boundary regions throughout West and Central Africa.

Regional Production Leaders Drive Continental Growth

What Makes Nigeria Africa's LNG Powerhouse?

Nigeria's position as continental LNG leader reflects convergence of established infrastructure, substantial reserve endowments, and strategic geographic advantages. The nation's proven gas reserves exceeding 200 trillion cubic feet provide multi-decade supply security that enables long-term buyer confidence and project financing structures. Current production represents less than 1% of total reserves, indicating enormous expansion potential under favourable market conditions.

The 45% year-over-year growth suggests either previously underutilised capacity activation or successful debottlenecking initiatives that enhanced facility throughput rates. Nigeria's Atlantic coast positioning enables direct shipping routes to European regasification terminals within 7-10 days compared to 25-30 days from Asian suppliers, providing crucial competitive advantages during supply chain disruption periods.

Established buyer relationships dating to 1990s commissioning phases create institutional knowledge and contractual frameworks that facilitate rapid volume scaling during market opportunities. The combination of technical reliability, geographic proximity, and relationship maturity positions Nigerian LNG as preferred alternative sourcing for European utilities facing Middle Eastern supply uncertainties.

Angola: Steady Growth Through Operational Excellence

Angola's 30% export increase to 1.25 million tonnes reflects consistent operational performance and market responsiveness. The nation's LNG sector benefits from integrated oil and gas development models where associated gas monetisation improves overall project economics while reducing environmental impact through flaring elimination.

However, technical infrastructure investments focus on production optimisation and export facility efficiency improvements. Angola's position within the West African corridor provides logistical advantages for both European and Asian market access, while established international partnerships facilitate technology transfer and capital mobilisation for expansion projects.

Mozambique: Managing Security Challenges

Despite regional security concerns, Mozambique maintained 914,000 tonnes of Q1 2026 exports, representing only a 3% decline from previous year levels. The nation's ultra-deepwater gas reserves constitute some of Africa's largest undeveloped resources, with potential to transform regional supply architecture once infrastructure development accelerates.

International energy companies continue project development despite operational challenges, reflecting confidence in long-term resource value and market positioning. The geographic location provides direct access to high-growth Asian markets while maintaining flexibility for European supply arrangements through established shipping routes.

Geopolitical Supply Chain Restructuring Creates African Opportunities

Middle Eastern conflicts fundamentally altered global energy flows by damaging regional oil and gas infrastructure while elevating maritime security risks through critical shipping chokepoints. The Strait of Hormuz, historically enabling 21% of global petroleum trade flows, faces elevated transit risk premiums that compel buyers to accelerate diversification initiatives regardless of potentially higher delivered costs from alternative suppliers.

European energy security strategies prioritise supply source diversification following lessons from previous pipeline dependency experiences. African LNG suppliers benefit from reduced buyer resistance to premium pricing when security of supply considerations outweigh pure cost optimisation. This strategic buyer behaviour shift creates sustainable competitive advantages for reliable African producers beyond immediate crisis periods.

Maritime Security Risk Management

Shipping route alterations force European and Asian buyers to reassess delivered cost calculations when traditional supply sources face elevated insurance premiums and extended transit times. African producers along Atlantic coastlines avoid Red Sea and Persian Gulf transit risks, providing inherent logistical advantages during regional instability periods.

The Cape of Good Hope route alternative adds 10-15 days to Asian-bound shipments while increasing fuel consumption and charter rates. However, African suppliers' geographic positioning enables competitive delivered pricing even when accounting for these additional costs, particularly when traditional suppliers face security-related shipping premiums.

Consequently, natural gas price trends reflect this fundamental market restructuring, where security premiums become permanent features of global energy pricing rather than temporary crisis adjustments.

Buyer Relationship Evolution

Long-term supply contract negotiations increasingly incorporate security of supply provisions that value source diversification beyond pure price considerations. African producers leverage this buyer preference shift to negotiate improved contract terms and volume commitments that provide revenue stability for infrastructure investment planning.

European utilities demonstrate willingness to pay security premiums for reliable African supply sources, creating sustainable competitive advantages that extend beyond immediate geopolitical crisis periods. Furthermore, US natural gas forecasts indicate sustained volatility that makes diversified sourcing increasingly attractive to major buyers.

Technology Innovation Enhances Competitive Positioning

African LNG producers adopt advanced liquefaction technologies that improve operational efficiency while reducing production costs per unit. These technological improvements enable competitive positioning against established suppliers while supporting expansion into previously uneconomic reserve locations through enhanced project returns.

Liquefaction Efficiency Improvements

Modern liquefaction facilities incorporate advanced heat exchanger designs, optimised compression systems, and enhanced process control technologies that reduce energy consumption while increasing throughput capacity. The Arzew complex modernisation demonstrates how retrofit applications can achieve capacity doubling through technological upgrades rather than complete facility replacement.

Energy consumption optimisation remains critical for competitive positioning, as liquefaction typically consumes 8-12% of total gas input. Efficiency improvements directly translate to increased export volumes from identical feed gas quantities while reducing operational costs and environmental impact profiles.

Modular Development Strategies

Floating LNG systems enable modular capacity additions that match market demand growth while minimising upfront capital requirements. This approach proves particularly valuable for African producers seeking to optimise investment timing and risk management during volatile market conditions.

Modular systems support phased development strategies where initial capacity establishes market presence and operational experience before committing to large-scale expansion projects. This incremental approach reduces project risks while maintaining expansion optionality as market conditions evolve.

Market Fundamentals Support Long-Term Growth Trajectory

Global LNG demand projections indicate sustained growth driven by Asian economic expansion, European energy transition requirements, and coal-to-gas switching policies across emerging markets. These fundamental demand drivers create structural market opportunities for African producers beyond immediate supply disruption benefits.

Asian Market Expansion

Asian LNG demand growth reflects economic development patterns, urbanisation acceleration, and environmental policy implementation across the region's largest economies. China and India's continued industrial expansion requires reliable energy supplies that complement domestic production capabilities and renewable energy development.

African LNG suppliers benefit from geographic flexibility enabling both European and Asian market access depending on price differentials and contractual opportunities. This dual-market positioning provides revenue optimisation capabilities and reduces dependence on single regional demand patterns.

In addition, successful energy transition challenges in developed economies create templates for emerging markets to follow similar decarbonisation pathways utilising natural gas as a bridge fuel.

European Energy Security Imperatives

European buyers prioritise supply source diversification following previous pipeline dependency experiences and current geopolitical uncertainties. Natural gas functions as a bridge fuel supporting renewable energy integration while maintaining grid stability during intermittent generation periods.

African suppliers align with European energy security strategies by providing reliable alternatives to traditional pipeline supplies while maintaining competitive pricing structures. Long-term supply agreements increasingly incorporate African sources as strategic components of diversified energy portfolios rather than emergency alternatives.

The next major ASX story will hit our subscribers first

Investment Capital Mobilisation Accelerates Development

African LNG projects attract substantial international investment exceeding $60 billion in committed capital across continental development initiatives. Investment flows prioritise proven technologies, established partnerships, and strategic geographic positioning that support long-term market access and competitive sustainability.

Capital Allocation Patterns

Investment priorities focus on floating LNG technology deployment for remote reserve monetisation, pipeline infrastructure connecting landlocked gas fields, and port facility development supporting larger vessel operations. These infrastructure categories provide scalable capacity additions while improving operational flexibility and cost competitiveness.

International financing structures incorporate development bank participation, export credit agency support, and private equity investment that distribute project risks while optimising capital costs. Multi-source financing approaches enable larger project scales and shorter development timelines compared to single-source funding constraints.

Risk-Return Assessment

African LNG investments offer attractive returns reflecting resource quality, market positioning advantages, and infrastructure development potential. However, investment decisions require comprehensive risk assessment covering political stability, regulatory framework evolution, and security consideration variations across producing regions.

Country-specific risk profiles influence project structuring, insurance requirements, and expected return thresholds. Established producers with operational track records command improved financing terms compared to emerging exporters requiring additional risk premiums and enhanced security provisions.

For instance, US-China trade war strategies demonstrate how geopolitical tensions influence investment patterns and partnership structures across international energy projects.

Energy Transition Implications and Strategic Positioning

Natural gas positioning as a transitional fuel during global decarbonisation efforts supports sustained African LNG demand through medium-term energy system evolution. International climate commitments recognise gas-fired generation's role in replacing coal capacity while renewable infrastructure scales to meet growing electricity demand.

Bridge Fuel Market Dynamics

European decarbonisation strategies increasingly rely on natural gas to provide dispatchable generation capacity supporting renewable energy integration. Grid stability requirements during variable wind and solar production create sustained demand for flexible gas-fired power generation capabilities.

African LNG suppliers benefit from this transition role by providing cleaner alternatives to coal and oil-fired generation while supporting renewable energy development through complementary grid services. This positioning creates sustained market demand extending beyond immediate supply disruption opportunities.

Consequently, renewable energy solutions complement rather than compete with natural gas infrastructure during transition periods, creating synergistic development opportunities.

How Do Domestic Energy Requirements Affect Export Strategies?

African producers must balance export revenue optimisation with domestic energy development requirements as economic growth accelerates energy consumption. Strategic planning involves optimising gas utilisation between export markets and domestic power generation to support industrial development and electrification objectives.

Domestic market development can provide demand stability and economic diversification benefits while reducing export dependency. However, international market pricing typically exceeds domestic prices, creating opportunity cost considerations in resource allocation decisions.

Regional Infrastructure Development and Connectivity

West African corridor development enables coordinated infrastructure investments that reduce individual country costs while accelerating regional gas monetisation. Shared pipeline networks, port facilities, and processing capabilities optimise continental resource development efficiency while improving market access for smaller producers.

Pipeline Network Integration

Cross-border pipeline development connects previously isolated gas fields to export facilities, enabling reserve monetisation that would otherwise remain stranded due to insufficient individual project economics. Regional network effects reduce transportation costs while providing operational flexibility during maintenance or capacity constraints.

Integrated pipeline systems support multiple producer access to shared export facilities, optimising infrastructure utilisation while reducing per-unit development costs. This cooperative approach proves particularly valuable for smaller reserves that cannot justify standalone export infrastructure investment.

Port Infrastructure Enhancement

Expanded port capabilities accommodate larger LNG carriers and improved loading efficiency, reducing shipping costs while increasing operational flexibility. Enhanced storage capacity provides operational buffers during demand fluctuations while enabling more efficient vessel scheduling and route optimisation.

Port infrastructure investments support multiple users and cargo types, improving project economics through diversified revenue streams. Integrated facility development enables economies of scale that individual country investments cannot achieve within competitive timeframes.

Future Market Positioning and Growth Sustainability

Africa's LNG exports rise continues positioning the continent for sustained expansion through infrastructure investment continuity, technological advancement adoption, and strategic market positioning that capitalises on global energy security concerns while maintaining competitive cost structures. Success depends on balancing export optimisation with domestic energy development requirements.

Long-term growth sustainability requires addressing security challenges, optimising operational efficiency, and maintaining competitive positioning relative to emerging suppliers and alternative energy sources. Continental coordination and shared infrastructure development provide strategic advantages for sustained market expansion.

Moreover, the sector's evolution reflects broader global energy market transformations where African producers increasingly function as reliable suppliers capable of meeting growing international demand while supporting continental economic development objectives. Strategic planning and infrastructure investment continuity determine long-term competitive sustainability and market positioning effectiveness.

According to Africa's LNG export potential analysis, the continent possesses sufficient reserves and strategic advantages to maintain competitive positioning through evolving market cycles while supporting domestic energy transition requirements.

Furthermore, recent data from African energy market developments confirms sustained growth momentum across multiple production hubs, reinforcing the continent's emergence as a reliable alternative to traditional LNG suppliers facing ongoing geopolitical and operational challenges.

This analysis represents independent research and should not be considered investment advice. Market projections involve inherent uncertainties, and actual results may differ materially from expectations discussed above.

Looking to Capitalise on Africa's Energy Transformation?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across the ASX, helping subscribers identify actionable investment opportunities in the rapidly evolving energy and resources sector. With Africa's LNG exports demonstrating remarkable 27% growth and global energy markets undergoing fundamental shifts, positioning yourself ahead of major discoveries in Australia's mining sector could provide the market edge needed during these transformative times.