June 5, 2026

When Multiple Commodities Fall Together, the ASX Has Nowhere to Hide

There is a particular kind of market session that exposes the structural fault lines running beneath Australia's benchmark equity index. It is not a session defined by a single commodity moving lower or one heavyweight stock dragging its sector down. It is the session where iron ore, copper, and lithium all retreat simultaneously, removing every available offset and leaving the ASX materials sector with no internal hedge against the selling pressure. Friday, 5 June 2026 was precisely that kind of session.

Understanding why lower iron ore, copper and lithium prices turned the ASX red on Friday requires more than reading the closing numbers. It demands a clear-eyed look at how Australia's index is constructed, how commodity pricing flows through to equity valuations in real time, and why the ASX remains uniquely exposed to these cycles in ways that most comparable global benchmarks are not.

When big ASX news breaks, our subscribers know first

The Architecture of ASX Vulnerability: Why Commodities Control the Index

The ASX 200 is not a diversified benchmark in the way the S&P 500 or even the FTSE 100 might be characterised. Materials and energy stocks command a disproportionate share of its total market capitalisation, meaning that when bulk and battery commodity prices move in concert, the resulting impact on the index is amplified well beyond what a sector-level weighting might suggest on paper. The ASX commodity pressure this creates is well documented and continues to shape investor behaviour.

This concentration dynamic operates through several reinforcing channels:

- Direct valuation impact: Mining company share prices are continuously re-rated as commodity spot and futures prices move, with fund managers adjusting revenue and earnings forecasts in near real time

- Sentiment transmission: A broad-based commodity selloff shifts risk appetite across the entire index, not just among resources stocks, as portfolio managers reduce exposure to cyclical assets generally

- Currency feedback: A weaker commodity price environment tends to soften the Australian dollar, which then creates secondary effects across import-exposed sectors and consumer confidence metrics

- Index weighting mechanics: BHP alone represents a significant fraction of the ASX 200's total weight, meaning a single-stock decline of even 2% registers as a meaningful drag on the headline index number

The SGX iron ore futures contract, traded on the Singapore Exchange, functions as the real-time pricing compass for Australian mining valuations. It references 62% Fe iron ore delivered to China and is updated continuously during Asian trading hours, making it the most operationally relevant benchmark for the companies, analysts, and fund managers who collectively determine where BHP, Fortescue, and Rio Tinto's share prices should trade on any given day.

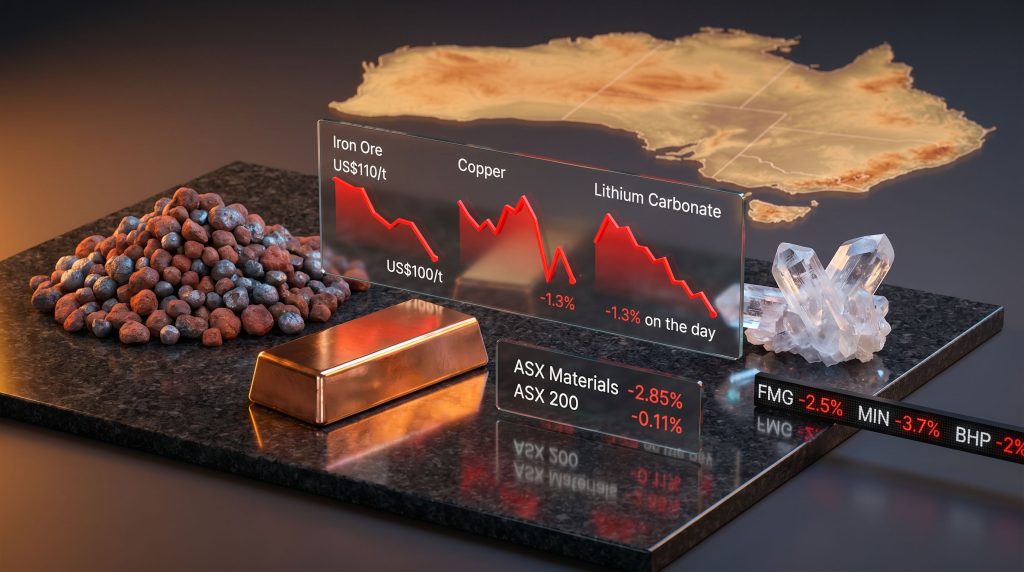

Iron Ore's Retreat From US$110/t: What the Numbers Actually Mean

The trajectory of SGX iron ore futures in the weeks leading into Friday's session tells a nuanced story. Prices had climbed from well below US$90 per tonne twelve months prior to levels approaching US$110/t, representing a substantial cyclical recovery that had broadly re-rated the earnings outlooks of Australia's major iron ore producers. The pullback to approximately US$100 to US$103 per tonne therefore registers as a meaningful retracement from the recovery high, even if the absolute price level still represents a significant improvement on where the market sat a year ago. Understanding iron ore price trends helps contextualise these movements within the broader demand cycle.

| Timeframe | SGX Iron Ore Futures | Contextual Significance |

|---|---|---|

| ~12 months prior | Below US$90/t | Cyclical trough |

| Recovery peak | ~US$110/t | Multi-month high |

| Friday session range | ~US$100–US$103/t | Pullback from peak |

| Latest benchmark (June 3) | US$103.71/t | Soft but stabilising |

The US$100 per tonne level carries particular weight in the way market participants think about iron ore pricing. It functions simultaneously as a psychological round number and a technical support level that separates comfortable margin territory for most Australian producers from the zone where project economics start to compress meaningfully. When futures hover near this threshold, capital allocation decisions, feasibility assessments, and dividend sustainability all come under heightened scrutiny from analysts and institutional investors.

What is less commonly understood is how the quality differential embedded in iron ore pricing interacts with these headline numbers. The SGX benchmark references 62% Fe fines, but Australian producers often export ore at varying grade profiles. High-grade ore above 65% Fe commands a premium over the benchmark, while lower-grade material trades at a discount. When headline futures compress toward the US$100/t level, the effective received price for producers shipping sub-benchmark grade material can fall considerably below that figure, making the margin impact more severe than the headline number implies for certain operators.

BHP, Fortescue, and MinRes: Three Different Exposures to the Same Storm

BHP: The Copper Hedge That Only Partially Offsets Iron Ore Weakness

BHP's Friday decline of more than -2% arrived in the context of a stock that had only two trading sessions earlier reached a record high approaching A$65 per share, driven substantially by copper's sustained strength. The pullback left BHP still trading above A$60 per share, a valuation threshold the company had only recently broken through, but the speed of the reversal underscored how quickly commodity repricing can erode equity gains in the mining sector.

The analytical complexity in BHP's case stems from its dual commodity identity. As both a dominant iron ore exporter and an increasingly important copper producer, BHP's share price is effectively a blended function of two commodity cycles that do not always move in the same direction. On Friday, they did move in the same direction, with copper futures declining approximately -1.3% on the session. However, copper's broader trend remains constructive, having gained close to +5% over the preceding month and touching record highs on multiple occasions in recent trading history. The ongoing copper supply crunch underpins this longer-term constructive outlook despite short-term volatility.

Investors who treat BHP as a simple iron ore proxy are systematically miscalculating its earnings sensitivity. The company's growing copper division means that sustained copper strength can significantly offset iron ore weakness over a full reporting period, even when both commodities decline in a single session.

This distinction matters for portfolio construction. Short-term traders react to daily commodity moves; longer-term investors should be modelling BHP's earnings through both commodity cycles independently, recognising that the company's diversification provides a structural earnings buffer that pure-play operators cannot access.

Fortescue: Pure-Play Exposure Leaves No Margin for Commodity Error

Fortescue's -2.5% decline during Friday's late morning session reflects the amplified sensitivity that pure-play operators carry relative to diversified miners. As a producer overwhelmingly dependent on iron ore revenues, Fortescue's equity value is essentially a leveraged instrument on SGX futures. When those futures decline, Fortescue's implied earnings fall in near-direct proportion, and its share price adjusts accordingly with limited offsetting factors.

There is an additional layer of complexity specific to Fortescue's ore characteristics. The company has historically exported iron ore with a lower Fe grade than BHP or Rio Tinto, meaning it has at times traded at a discount to the 62% Fe benchmark. In a softer price environment, lower-grade material faces proportionally greater pricing pressure as Chinese steel mills, which are the primary buyers, prioritise blend efficiency and reduce the premiums they pay for higher-grade input, while simultaneously widening discounts on lower-grade supply.

MinRes: The Compounding Effect of Dual-Commodity Weakness

Mineral Resources suffered the steepest decline of the major materials names on Friday, falling -3.7%. The explanation lies in its simultaneous exposure to both iron ore and lithium, meaning it absorbed negative pricing signals from two separate commodity markets within the same trading session. Lithium recorded a -1.3% decline on the day, compounding the pressure already arriving from iron ore's retreat.

MinRes's situation illustrates a portfolio risk concept that is often underappreciated: correlated commodity exposure within a single company. When a producer's revenue streams span multiple commodities, investors instinctively assume diversification benefits. However, when those commodities are both linked to Chinese industrial demand and global risk sentiment, they can decline together under the same macro conditions, eliminating the diversification premium and amplifying the downside. The commodity price impact on dual-exposed operators like MinRes is consequently more severe than most investors anticipate.

Lithium's Protracted Correction: Separating Cycle From Structure

The lithium sector's Friday weakness did not occur in isolation. It arrived as the latest episode in a prolonged price correction that has challenged the economic viability of high-cost producers and forced a reassessment of expansion plans across the industry. Pilbara Minerals, Liontown Resources, and Elevra Lithium were among the ASX names recording session losses, with MinRes's dual exposure making it particularly vulnerable. Furthermore, the broader lithium market downturn continues to weigh heavily on sector sentiment as oversupply conditions persist.

The core tension in lithium markets is between competing structural narratives:

- The long-run demand thesis: Electric vehicle adoption, grid-scale battery storage deployment, and expanding consumer electronics production collectively underpin a multi-decade demand growth trajectory that most analysts consider structurally intact

- The near-term oversupply reality: Aggressive capacity additions from Australian hard-rock spodumene operations, expanded South American brine projects in Chile and Argentina, and substantial growth in Chinese lithium refinery capacity have collectively overwhelmed current demand, pushing prices into territory that renders many projects marginal or sub-economic

- The battery chemistry wildcard: The accelerating adoption of lithium iron phosphate (LFP) battery chemistry, which uses less lithium per kilowatt-hour than nickel-manganese-cobalt (NMC) alternatives, has moderated near-term demand growth estimates and added uncertainty to volume forecasts

| Recovery Trigger | Plausibility | Estimated Timeline |

|---|---|---|

| Sustained EV demand acceleration in China | Moderate to High | 12 to 24 months |

| High-cost producer supply curtailments | Moderate | 6 to 18 months |

| Grid storage demand surge | Moderate | 18 to 36 months |

| New battery chemistry driving lithium intensity increase | Low to Moderate | 24 to 48 months |

| Geopolitical supply disruption | Low | Unpredictable |

A sustained sub-US$10 per kilogram lithium carbonate equivalent environment creates existential pressure for producers operating above the cost curve. The irony is that sufficiently low prices are ultimately self-correcting: they force capacity out of the market, reduce investment in new projects, and eventually tighten the supply-demand balance enough to support price recovery. However, this correction cycle can take considerably longer to resolve than initial optimism suggests, as noted by analysts tracking the sector.

Macro Overlays: Geopolitical Risk and the ASX's Second-Tier Perception Problem

The commodity pricing story on Friday cannot be fully understood without accounting for the broader macro environment shaping how global capital is allocated toward Australian equities. The ongoing geopolitical instability linked to the Iran conflict has contributed to a risk-off disposition among international investors that tends to favour more liquid, more diversified benchmarks over commodity-concentrated indices like the ASX.

This dynamic manifests as a persistent discount on ASX valuations relative to comparable markets. When global capital moves defensively, Australia's resource-heavy index is not the natural destination, regardless of the underlying quality of the companies listed on it. The absence of a meaningful safe-haven tailwind from gold, which also faced pricing pressure during the session, removed what might otherwise have partially cushioned the materials sector's decline.

Commonwealth Bank's -0.75% decline on Friday serves as a useful illustration of how commodity-sector weakness transmits beyond materials stocks. The financial sector's indirect exposure to resources runs through corporate lending books, project finance facilities, and the broader wealth effect that commodities exert on consumer confidence in a mining-dependent economy. When materials fall sharply, the sentiment contagion rarely stays contained within the sector. This pattern is consistent with how the materials sector sell-off has historically cast a shadow well beyond mining stocks alone.

The next major ASX story will hit our subscribers first

Reading the Signal: How to Assess Multi-Commodity Selloff Days

Not all commodity selloff sessions carry equal analytical weight. A single-day decline of -1% to -3% across iron ore, copper, and lithium sits well within the normal range of daily price volatility and does not in isolation constitute evidence of a structural trend reversal. The more productive analytical question is whether Friday's moves represent a continuation of established downtrends or temporary pullbacks within broader recovery phases.

| Indicator | Current Reading | Key Threshold to Watch |

|---|---|---|

| SGX Iron Ore Futures | ~US$100–US$105/t | Sustained hold above US$100/t |

| Copper Monthly Trend | +5% over 30 days | Sustaining above recent record levels |

| Lithium Carbonate Price | Soft, -1.3% on Friday | Evidence of supply curtailment |

| ASX Materials Sector (Weekly) | -2.85% | Stabilisation vs. further deterioration |

| BHP Share Price Level | Above A$60/sh | A$60 as key technical support |

For investors managing longer time horizons, multi-commodity selloff days can present entry-point considerations rather than exit signals, provided the underlying assets are assessed on their structural merits rather than short-term price momentum. The distinction that matters most in this kind of environment is between low-cost, long-life asset operators — who can sustain profitability through extended periods of price weakness — and high-cost, capital-intensive producers who entered the cycle during the price boom and now face margin compression that threatens their operational and financial sustainability.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Commodity prices, share prices, and market conditions referenced are subject to change. Readers should conduct their own research and seek guidance from a qualified financial adviser before making investment decisions.

The Structural Demand Case Remains the Long-Term Anchor

Whatever the near-term price signals suggest, the structural demand thesis underpinning Australia's three most consequential export commodities has not fundamentally changed. Iron ore's long-run demand profile is tied to urbanisation trajectories in developing economies that remain decades from completion. Copper's structural deficit narrative is grounded in the electrification requirements of the global energy transition, a process that is accelerating rather than decelerating. Lithium's demand story, while currently obscured by oversupply conditions, rests on a battery storage growth curve that is still in its early innings relative to the ultimate scale of the EV and grid storage markets.

Friday's session, viewed through this longer lens, looks less like a structural inflection and more like a routine episode of cyclical volatility in markets that have always moved in waves. The conditions that produced lower iron ore, copper and lithium prices turning the ASX red on Friday are not novel; they are a recurring feature of how commodity-driven indices behave across the cycle. The ASX's deep sensitivity to commodity cycles is simultaneously its greatest source of long-term return potential and its most persistent source of short-term pain. For investors who can hold that duality in mind, days like Friday are not warnings to exit. They are reminders that the price of accessing Australia's world-class resource base comes with an inherent requirement to tolerate the cycle.

For ongoing coverage of ASX materials, mining, and commodity market developments, readers can explore The Market Online at themarketonline.com.au.

Want to Know When the Next Major ASX Mineral Discovery Hits the Market?

When commodity cycles create volatility across the ASX, the most compelling opportunities often emerge from significant new mineral discoveries rather than macro-driven price swings. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment high-potential ASX mineral discoveries are announced, transforming complex geological and commodity data into actionable insights for investors at every experience level — begin a 14-day free trial today and explore historic discoveries that have generated exceptional market returns to understand just how transformative early positioning can be.