July 16, 2026

When the Engine of Global Demand Starts to Sputter

For most of the past two decades, the investment thesis for large-cap mining equities was elegantly simple: back the company with the most exposure to China, and watch commodity supercycle economics do the rest. That framework minted fortunes, reshaped balance sheets, and turned Australian iron ore into one of the most consequential export relationships in modern economic history.

However, commodity supercycles do not last forever, and the conditions that made China the world's most voracious consumer of raw materials are structurally shifting. For investors holding BHP Group (ASX: BHP) at current prices, the question is no longer whether the China boom has peaked. It is whether the market has correctly priced what comes next.

The short answer, according to multiple institutional valuation frameworks, is that it has not. The case for BHP overvalued due to China slowdown is increasingly difficult to dismiss when several independent analytical frameworks converge on the same conclusion.

When big ASX news breaks, our subscribers know first

China's Structural Role: More Than Just BHP's Biggest Customer

Understanding the BHP valuation debate requires understanding just how deeply China is embedded in global commodity markets, and by extension, in BHP's revenue architecture.

China consumes more than 50% of the world's steel and absorbs approximately 75% of seaborne iron ore trade, according to Rio Tinto. These are not marginal relationships. They represent a demand concentration so extreme that Chinese economic decisions function as de facto global pricing mechanisms for iron ore. Furthermore, the iron ore price decline of more than 30% in 2026 reflects just how rapidly this dynamic can shift.

The copper relationship is equally asymmetric. China accounts for less than 10% of its own mined copper supply but represents more than half of global refined copper demand, creating a structural import dependency that ties Chinese economic health directly to global copper price dynamics.

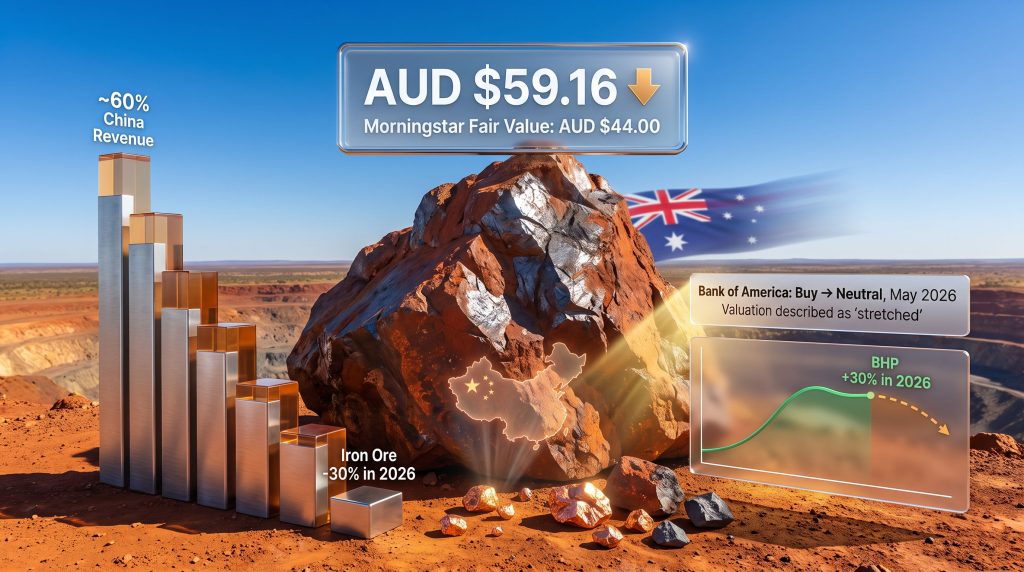

Against this backdrop, BHP's revenue geography tells its own story. China accounted for approximately 60% of BHP's total sales in fiscal year 2025, making it not merely the company's largest customer, but the central pillar around which BHP's entire earnings model is constructed.

What Multiple Valuation Frameworks Are Saying Right Now

BHP shares have risen more than 30% in 2026, driven by a combination of rising copper prices and the resolution of iron ore contract negotiations with China Mineral Resources Group (CMRG). At approximately AUD $59.16, the stock sits materially above what several independent valuation methodologies consider fair value.

The table below summarises key institutional and quantitative assessments:

| Institution / Model | Fair Value Estimate | Implied Premium at ~AUD $59 | Primary Risk Flagged |

|---|---|---|---|

| Morningstar (equity research) | AUD $44.00 | ~33% above fair value | China demand softening; iron ore structural decline |

| Simply Wall St | AUD $55.50 | ~12% above fair value | Copper reliance and China slowdown |

| DCF Intrinsic Model (Yahoo Finance) | ~AUD $31-32 | ~46% above intrinsic value | Cash flow compression on China exposure |

| Bank of America | Downgrade: Buy to Neutral (May 2026) | Valuation described as stretched | Negative China credit impulse; 6-8 month earnings lag |

The convergence of these independent frameworks around a single conclusion is analytically significant. When discounted cash flow models, qualitative equity research, and institutional analyst upgrades all arrive at a similar diagnosis, the divergence between their consensus and the market price warrants serious investor attention.

The Morningstar No-Moat Classification Explained

Morningstar's equity research team assigns BHP a no-moat rating, a designation that carries specific analytical weight within their framework. A moat, in Morningstar's terminology, refers to a durable structural competitive advantage that enables a company to generate returns above its cost of capital across a full business cycle.

For commodity producers like BHP, this classification reflects an unavoidable economic reality: iron ore is iron ore. BHP cannot charge a premium for its product relative to a competitor's chemically equivalent output. As a price taker in global commodity markets, BHP's profitability is entirely determined by external forces, primarily the intersection of Chinese demand and global supply dynamics.

Morningstar's AUD $44.00 fair value estimate reflects this structural reality. At a current market price of approximately AUD $59, the implied overvaluation sits at roughly 33% above Morningstar's intrinsic assessment.

It is worth noting that BHP's low-cost asset base and geographic proximity to Asian markets do provide a modest freight cost advantage over producers in Africa and South America. However, operational resilience does not equate to a structural competitive moat in the technical sense Morningstar applies.

The Iron Ore Problem: Structural Reset, Not a Cyclical Dip

The most consequential risk embedded in BHP's current valuation is not a temporary demand shortfall. It is the possibility that China's property sector contraction represents a permanent recalibration of the demand ceiling for iron ore. Consequently, the China steel demand outlook has fundamentally altered the investment case for BHP at current prices.

China's property and infrastructure sectors together account for approximately 60% of domestic steel demand, according to Rio Tinto's own estimates. Iron ore feeds directly into that demand chain as the primary steelmaking raw material. When construction activity contracts, the transmission mechanism to iron ore pricing is rapid and direct.

Furthermore, China has reduced its official GDP growth target to a range of 4% to 5% in 2026, down from approximately 5% in 2025 and representing the lowest official target since 1991.

Why Beijing's Traditional Stimulus Response Is Losing Traction

China's historical playbook during economic slowdowns has been to accelerate commodity-intensive infrastructure investment. This approach generated powerful demand bounces in 2009, 2016, and again following the COVID-19 disruptions. Infrastructure investment in the first quarter of 2026 rose 9% year-on-year, consistent with this pattern, but growth momentum visibly decelerated through April and May.

The structural problem is that this playbook is subject to diminishing returns. Two compounding forces are reducing its effectiveness:

- Returns on new infrastructure investment in China are declining as the most economically productive projects are completed

- Central government policy has explicitly committed to reorienting growth toward domestic consumption rather than investment-driven expansion

The practical implication for BHP investors is a ratchet effect, where each successive infrastructure stimulus cycle generates less incremental iron ore demand than the preceding one. Demand peaks are becoming progressively lower, and trough floors are not recovering to prior cycle levels.

Investors extrapolating China's historical stimulus response onto current market conditions may be applying a framework that has fundamentally changed. The infrastructure lever is not broken, but its commodity demand multiplier has substantially diminished.

The Credit Impulse: A Leading Indicator BHP Investors Cannot Ignore

Bank of America's May 2026 downgrade from Buy to Neutral cited a specific macroeconomic signal as central to its revised assessment: China's credit impulse had turned negative on a year-over-year basis.

The credit impulse measures the rate of change in new credit creation relative to GDP. When negative, it indicates credit contraction, which historically precedes softening in industrial commodity demand by approximately 6 to 8 months. This lag structure means the earnings pressure implied by a negative credit impulse in early 2026 had not yet fully manifested in BHP's reported financials at the time of the downgrade.

Copper: A Strategic Pivot With Its Own China Exposure

The BHP strategic pivot toward copper represents a deliberate and well-capitalised response to iron ore's structural vulnerability. The acquisition of OZ Minerals in fiscal 2023 and the purchase of a 50% stake in the Vicuna copper joint venture in fiscal 2025 represent the clearest expression of this strategic shift.

The copper bull case is genuinely compelling over a multi-decade horizon. Electric vehicles, utility-scale renewable energy systems, grid modernisation programmes, and data centre infrastructure all require substantially more copper per unit of economic output than the fossil-fuel and analogue systems they replace.

Where the Copper Thesis Intersects With China Risk

The complication is that copper market trends reveal demand geography that is almost as China-concentrated as iron ore's. China accounts for more than 50% of global refined copper demand. Critically, JPMorgan estimates that building and construction activities alone account for approximately 30% of China's total copper consumption, through wiring, plumbing systems, and electrical infrastructure embedded in new development.

A sustained Chinese property contraction therefore creates a direct headwind to copper demand even as electrification trends provide a partial structural offset. Copper is unambiguously the superior long-term commodity when compared to iron ore, but it is not immune to the same Chinese economic deceleration that is weighing on BHP's broader earnings profile.

What BHP Gets Right: Operational Strengths the Bears Underweight

A balanced analysis requires acknowledging what BHP's sceptics may be discounting. The Australia iron ore advantage is most visible in BHP's Western Australia Iron Ore (WAIO) operations, which rank among the lowest-cost iron ore production systems globally.

Several additional operational strengths deserve recognition:

- BHP's balance sheet management philosophy prioritises financial resilience through commodity cycles, maintaining lower leverage than many mining peers

- The Jansen potash project in Saskatchewan, Canada, provides growth optionality linked to global agricultural demand, which is structurally independent of China's industrial cycle

- Geographic concentration of assets in Australia provides sovereign risk predictability that African or South American-weighted peers cannot replicate

- Modest WAIO volume expansion targets above 290 million metric tonnes per year are positioned as incremental rather than capital-intensive growth

These characteristics explain why BHP commands a premium to smaller, higher-cost commodity producers. The question is not whether BHP deserves a premium, but whether the premium currently embedded in the AUD $59 share price is proportionate to these operational advantages.

The next major ASX story will hit our subscribers first

How to Evaluate BHP's Risk-Reward at Current Prices

Investors assessing BHP in this environment should apply a structured analytical framework rather than relying on narrative momentum from the 2026 share price rally.

Step 1: Distinguish structural from cyclical demand softening

Determine whether iron ore demand is experiencing a temporary cyclical trough or a permanent demand ceiling reduction. The property sector evidence points toward the latter.

Step 2: Stress-test earnings across commodity price scenarios

Model BHP's earnings at iron ore spot prices of USD $80, $90, and $100 per tonne. Separately assess copper's earnings contribution at current prices and at a 15% to 20% price correction to understand the earnings sensitivity range.

Step 3: Apply a China concentration risk premium to the discount rate

A revenue concentration of approximately 60% in a single customer economy warrants a higher risk premium than institutional models typically assign to diversified industrials. Morningstar and Bank of America appear to embed this risk in their fair value assessments.

Step 4: Compare BHP against direct peers on standardised metrics

Evaluate BHP relative to Rio Tinto (ASX: RIO) and South32 (ASX: S32) on enterprise value to EBITDA multiples, price-to-fair-value ratios, and forward dividend yield.

Step 5: Monitor China-specific leading indicators continuously

- China's monthly credit impulse versus prior year

- Chinese steel mill capacity utilisation rates

- Iron ore port inventory levels at major Chinese import terminals

- CMRG pricing negotiation outcomes as a forward compression signal

The CMRG Dynamic: A Structural Compression Mechanism

The resolution of iron ore contract negotiations between BHP and China Mineral Resources Group contributed meaningfully to the 2026 share price rally. Reports indicated China had lifted a ban on certain BHP iron ore products, narrowing product-specific price discounts following engagement with BHP's incoming leadership.

However, investors should be cautious about interpreting this development as a durable positive. CMRG's role as a centralised state-backed price negotiator represents a structural mechanism designed to compress BHP's realised prices over time. A single negotiation resolution does not alter the fundamental architecture of that buyer-seller relationship. BHP's share price performance has already demonstrated how swiftly China-linked earnings deterioration can flow through to market valuations.

Frequently Asked Questions: BHP Valuation and China Exposure

Is BHP currently overvalued?

Based on institutional valuation frameworks, BHP's current share price of approximately AUD $59 trades at a premium ranging from 12% above Simply Wall St's estimate to more than 33% above Morningstar's AUD $44 fair value. The primary driver of these assessments is the company's heavy revenue dependency on China at a point where the case for BHP overvalued due to China slowdown is supported by multiple independent analytical sources.

What is China's credit impulse and why does it matter?

China's credit impulse measures the rate of change in new credit creation as a proportion of GDP. A negative reading signals contracting economic stimulus, which historically precedes softening in industrial commodity demand by approximately 6 to 8 months. Bank of America explicitly cited a negative year-on-year credit impulse as a forward warning for BHP's near-term earnings when it downgraded the stock to Neutral in May 2026.

Does BHP's copper exposure offset iron ore risk?

Copper provides a growing and strategically important earnings contribution, and BHP has committed substantial capital to expanding its copper portfolio. However, China accounts for more than 50% of global refined copper demand, and building and construction activities represent roughly 30% of that Chinese copper consumption. Copper is a superior long-term commodity, but it is not structurally insulated from Chinese near-term demand softening.

What is the Morningstar fair value for BHP?

Morningstar's equity research team holds a fair value estimate of AUD $44.00 per share for BHP, paired with a no-moat rating. At approximately AUD $59, the stock trades roughly 33% above this intrinsic assessment.

Key Takeaways for Investors Assessing BHP Overvaluation Risk

- Revenue concentration is the foundational risk: Approximately 60% of BHP's revenue flows from a single customer economy undergoing a structural demand transition

- Iron ore faces a demand ceiling reset, not a cyclical correction: China's property sector is experiencing a permanent recalibration of activity levels, not a temporary softening

- Stimulus effectiveness is diminishing: Each successive Chinese infrastructure investment cycle is generating lower incremental commodity demand than historical precedents would suggest

- Copper is better but not insulated: Electrification demand tailwinds are real, but insufficient to fully offset near-term construction-related copper demand losses in China

- Institutional consensus is consistently pointing to overvaluation: Morningstar, Bank of America, and multiple quantitative models all indicate material premium pricing relative to intrinsic value estimates

- The no-moat classification has practical investment consequences: Without pricing power, BHP's earnings trajectory is entirely determined by forces outside management's control

BHP remains one of the highest-quality operators in global mining, with low-cost assets, disciplined capital management, and genuine strategic optionality through copper and potash. However, at current market pricing, the argument that BHP is overvalued due to China slowdown is supported by a breadth of institutional analysis that investors should not dismiss lightly. The 30%-plus 2026 rally deserves sceptical scrutiny against the structural demand headwinds that multiple valuation frameworks continue to flag.

This article is intended for informational purposes only and does not constitute financial advice. Investors should conduct their own due diligence and consider seeking independent professional advice before making investment decisions. All valuation estimates referenced are drawn from publicly available institutional research and are subject to change. Past share price performance is not indicative of future returns.

Readers seeking independent equity research coverage of ASX-listed resource companies, including BHP, can access Morningstar Australia's research platform at morningstar.com.au.

Want to Identify ASX Mineral Discoveries Before the Broader Market Does?

While large-cap miners like BHP navigate structural demand headwinds from China, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries across more than 30 commodities — turning complex data into actionable investment opportunities. Explore how historic discoveries have generated substantial market returns and begin your 14-day free trial today to position yourself ahead of the market.