July 10, 2026

The Structural Forces Behind Canada's Enduring Mining Dominance in Latin America's Most Contested Jurisdiction

Few investment relationships in the global mining landscape carry the depth, complexity, and strategic weight of the Canada-Mexico corridor. While headlines frequently focus on political friction and regulatory reform, the underlying architecture of this relationship reflects decades of accumulated capital, geological alignment, and institutional familiarity that cannot be easily displaced. Understanding why Canada mining leadership in Mexico has persisted through multiple cycles of political change requires moving beyond event-driven analysis toward a structural assessment of what makes this partnership function and where its vulnerabilities genuinely lie.

When big ASX news breaks, our subscribers know first

Why Mexico Consistently Attracts Canadian Mining Capital

Mexico occupies a position unlike any other jurisdiction in Latin America for Canadian mining investors. Its geological endowment spans several of the world's most prolific mineral belts, including the Sierra Madre Occidental, which hosts some of the highest-grade silver and gold deposits on the planet. This mountain range, stretching through Sonora, Chihuahua, Sinaloa, and Durango, has been the backbone of Mexican precious metals production for centuries, and Canadian junior and mid-tier miners have leveraged its potential more aggressively than any other foreign cohort.

Beyond geology, the structural case for Mexican investment rests on several converging factors:

- Geographic proximity reduces logistics costs for equipment, personnel, and concentrate shipments compared to South American jurisdictions

- Operating cost advantages remain significant, with all-in sustaining costs at established Mexican underground operations typically lower than comparable assets in West Africa or Central Asia

- The USMCA trade framework creates a degree of bilateral investment predictability not present in jurisdictions outside the North American trading bloc

- An experienced, technically skilled mining workforce has been cultivated across Mexico's key mining states over generations, reducing the human capital deficit that plagues frontier jurisdictions

- Established processing infrastructure in states like Zacatecas and Durango means capital-efficient pathways to production exist for exploration-stage discoveries

Mexico's commodity profile adds further appeal. The country is one of the world's foremost silver producers, consistently ranking first or second globally by output volume. It is also a meaningful gold, copper, zinc, and lead producer, offering Canadian operators a diverse menu of deposit types across a single jurisdiction with a unified legal and fiscal framework.

Quantifying the Scale of Canada's Presence in Mexican Mining

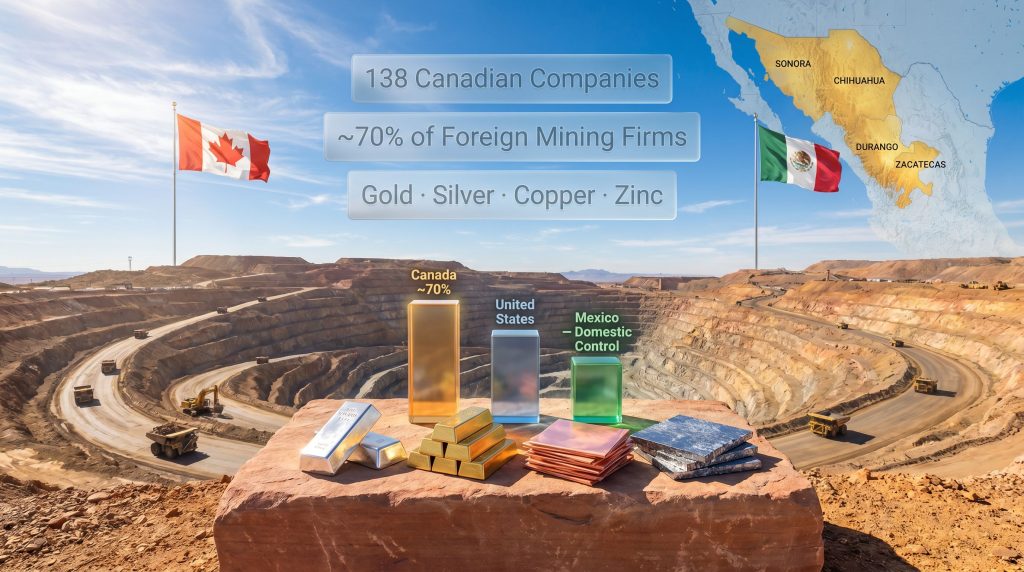

The numerical reality of Canada's position is striking. Approximately 138 Canadian companies are currently active across Mexico's mining sector, and Canadian-headquartered firms account for roughly 70% of all foreign mining companies operating in the country. Perhaps equally telling is that mining absorbs approximately 40% of Canada's total investment into Mexico, underscoring how central the sector is to the bilateral economic relationship. Furthermore, Canada maintains mining leadership in Mexico while the United States continues to face structural limitations in expanding its own presence.

Critical Context: Canada's dominance among foreign operators should not be conflated with control of Mexico's mining industry overall. Mexican companies retain majority ownership of the sector by asset value and production volume. Canadian capital leads specifically among foreign participants, functioning as a complementary financing and operational layer rather than a controlling interest.

This distinction matters enormously for risk assessment. Canadian operators work within a framework where the host nation's own capital retains ultimate industry leadership, which shapes the political dynamics of investment protection and regulatory negotiation in ways that differ from jurisdictions where foreign capital holds majority sectoral control.

From a global perspective, Mexico's contribution is substantial enough that it helps position Canada as 7th globally for overseas mining assets, a ranking that reflects the cumulative weight of Canadian capital deployed internationally, with Mexico serving as the single largest Latin American contributor to that figure.

How Canada Compares to the United States in Mexican Mining

One of the least examined dimensions of Canada mining leadership in Mexico is the structural constraint facing American operators by comparison. Despite sharing a border with Mexico and possessing significant mining capital of its own, the United States has consistently maintained a far smaller footprint in Mexican mining than geography alone would suggest.

| Dimension | Canada | United States |

|---|---|---|

| Share of Foreign Mining Companies in Mexico | ~70% | Significantly lower |

| Strategic Relationship Depth | Deep, long-standing | Periodically strained |

| Regulatory Alignment History | Historically cooperative | More friction-prone |

| Primary Commodity Focus | Gold, silver, copper, zinc | Less concentrated |

| Post-2020 Investment Trajectory | Cautious but maintained | Limited expansion |

| Diplomatic Capital in Mining Context | High | Reduced by trade tensions |

The constraints facing U.S. mining capital in Mexico are partly geopolitical and partly structural. Periods of tariff friction, immigration-linked political tensions, and energy sector disputes between Washington and Mexico City have periodically created an environment less hospitable to American capital than to Canadian investment. However, the broader tariffs and supply chains dynamic continues to reshape how North American mining capital is deployed across the region.

Canada's historical positioning as a diplomatic counterpart to Mexico within the North American framework has generated a form of soft institutional trust that translates into preferential access conditions, even when not formalised in specific treaty language.

The Commodity Landscape: Where Canadian Capital Is Concentrated

Precious Metals: The Core Thesis

Gold and silver remain the primary draw for Canadian operators in Mexico. The Sierra Madre Occidental's epithermal and mesothermal vein systems have historically produced ore grades that rival the world's best, with some underground operations in Durango and Chihuahua recording silver grades exceeding 300 grams per tonne in high-grade zones, a figure that renders these deposits globally competitive even at conservative metal price assumptions.

Canadian operators have shown particular preference for underground high-grade mining models over open-pit bulk tonnage approaches in Mexico, partly for geological reasons and partly because open-pit development has faced increasing regulatory resistance in recent years.

Base Metals and the Growing Copper Imperative

Copper and zinc represent a secondary but expanding priority. Mexico's porphyry copper systems in Sonora, most notably concentrated in the same geological province as Arizona's Bisbee district across the border, have attracted growing Canadian exploration interest as global copper demand forecasts tighten in response to electrification trends. Zinc-lead skarn and carbonate replacement deposits in Zacatecas and Chihuahua similarly represent established Canadian operating territory.

The Lithium Frontier: Opportunity Bounded by Sovereignty

Mexico's lithium potential adds a new and highly contested dimension to the investment landscape. The country holds lithium clay deposits, particularly in Sonora, that could represent significant resources relevant to battery supply chains. In addition, the lithium market opportunities across Latin America more broadly have intensified competition for strategic resource access. However, the 2022 legislative reform nationalising lithium as a strategic resource fundamentally altered the access framework for foreign capital.

Watch Point: Mexico's lithium nationalisation creates a bifurcated investment environment. Traditional metals remain accessible to Canadian capital under established concession frameworks, while lithium requires state partnership structures through LitioMx, the state entity created to manage lithium resources, fundamentally altering the risk-return profile for any company seeking exposure to this commodity in Mexico.

Canadian companies considering lithium exposure in Mexico must now model joint-venture or service-contract arrangements rather than direct ownership structures. Consequently, direct lithium extraction technologies and methodologies are becoming increasingly relevant as companies seek operationally viable pathways within tighter sovereign frameworks, introducing a layer of partnership risk not present in conventional precious or base metal projects.

The Regulatory Transformation: How the Rules Have Changed

Fiscal Pressure Points

The regulatory landscape governing foreign mining in Mexico has shifted materially since 2018. Several changes have recalibrated project economics across the sector:

- A special mining royalty of 7.5% applied to earnings before interest, taxes, depreciation, and amortisation (EBITDA) for all mining operators

- An additional 0.5% royalty on gold and silver revenues, layered on top of the standard rate

- Restrictions on new open-pit mining concessions, with environmental justification cited but the operational impact falling disproportionately on large-scale foreign operators

- Water-use restrictions in arid mining corridors that create permitting complexity for projects in Sonora and parts of Chihuahua, where groundwater access is already constrained

Tax Enforcement as Policy Instrument

Perhaps the most significant and least anticipated regulatory development has been the use of retroactive tax enforcement actions against foreign mining operators. Mexican tax authorities have pursued claims involving alleged price manipulation over extended periods, with some disputes reaching into the hundreds of millions of dollars. This enforcement posture signals that fiscal authorities view tax claims not merely as revenue collection tools but as mechanisms for renegotiating the effective terms of foreign participation in the sector.

For Canadian operators, this introduces a liability dimension that does not appear on standard project-level financial models but must be incorporated into entity-level risk assessments. The broader mining geopolitical landscape increasingly reflects this tension between resource nationalism and foreign capital participation across multiple jurisdictions simultaneously.

Concession Reform: From Automatic Renewal to Discretionary Grant

The transition away from near-automatic concession renewal toward a more discretionary, condition-based grant system represents a structural shift in how exploration and development rights are secured and maintained. Companies that built long-term mine plans on the assumption of routine concession continuity must now model concession risk as a genuine variable in CAPEX planning and project timeline forecasting. Indeed, environmental reforms in Mexico have further complicated this landscape for Canadian operators navigating an increasingly complex regulatory environment.

The next major ASX story will hit our subscribers first

Why Canadian Companies Continue to Invest Despite These Headwinds

The Viability Assessment Process

Experienced Canadian operators have adapted their project evaluation methodology to account for the new risk environment. A rigorous viability assessment now typically follows a structured sequence:

- Geological screening – Evaluate ore grade, deposit type, resource size, and metallurgical characteristics against global benchmarks to confirm Mexico-specific economic thresholds are met

- Regulatory mapping – Assess current concession status, open-pit applicability, water access rights, and proximity to protected or restricted zones

- Fiscal modelling – Incorporate the full royalty stack (7.5% EBITDA royalty plus the precious metals surcharge) alongside potential retroactive tax exposure into NPV and IRR calculations

- Social licence assessment – Evaluate Indigenous consultation requirements under Mexican law, community opposition history, and proximity to areas with documented conflict records

- Infrastructure audit – Map access to processing facilities, road networks, energy supply, and skilled labour pools within viable distance

- Political risk scoring – Apply both country-level and state-level governance risk weightings, recognising that states like Sonora and Zacatecas carry different risk profiles

- Investment decision – Proceed, defer, or restructure project parameters based on risk-adjusted return thresholds set against the company's portfolio benchmark

Scenario Pathways: Three Futures for Canadian Mining in Mexico

| Scenario | Driver | Canadian Outcome |

|---|---|---|

| Regulatory Stabilisation (Base Case) | New administration signals pro-investment policy | Greenfield exploration resumes; CAPEX accelerates |

| Continued Tightening (Downside) | Royalties rise further; restrictions expand | Junior exodus; majors renegotiate under duress |

| State Partnership Model (Structural Shift) | JV framework formalised across new projects | Canadian operators adapt equity structures; lithium template applied broadly |

Key Metrics at a Glance

| Metric | Data Point |

|---|---|

| Canadian companies active in Mexico | 138 |

| Canadian share of foreign mining companies in Mexico | ~70% |

| Mining's share of Canada's total investment in Mexico | ~40% |

| Mexico's ranking for mining FDI in Latin America | #1 |

| EBITDA royalty rate applied to mining operations | 7.5% |

| Additional precious metals royalty | 0.5% |

| Canada's global rank for overseas mining assets | 7th |

| Primary Canadian commodity focus | Gold, silver, copper, zinc |

| Emerging strategic commodity (state-controlled) | Lithium |

Strategic Takeaways for Investors and Industry Stakeholders

Canada's entrenched position across Mexican mining reflects structural depth, not recent opportunism. The 70% foreign company share held by Canadian operators has been built across decades of capital deployment, geological expertise, and institutional relationship-building. That foundation is not easily dismantled, but it is no longer insulated from policy-driven erosion.

Several conclusions are critical for investors positioning around Canada mining leadership in Mexico:

- Regulatory risk is now a first-order variable in Mexican project economics, not a secondary discount factor applied after NPV calculation

- The lithium nationalisation has drawn a clear sovereign boundary between traditional metals, where foreign capital retains access under concession frameworks, and strategic resources, where state co-investment is now required

- Retroactive tax enforcement represents an underappreciated liability risk that entity-level due diligence must incorporate beyond project-level financial models

- U.S. operators face compounding structural constraints that will likely sustain Canadian advantage in Mexico through at least the medium term, barring significant diplomatic realignment

- Long-term competitiveness for Canadian firms will depend on their capacity to adapt capital structures to evolving state-partnership models, with larger, well-capitalised operators better positioned to absorb friction than junior explorers

This article is intended for informational purposes only and does not constitute financial or investment advice. Mining investment involves material risks including regulatory change, commodity price volatility, and geopolitical uncertainty. Readers should conduct their own due diligence before making any investment decisions.

Want to Stay Ahead of Major ASX Mineral Discoveries in Real Time?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements the moment they are released, instantly translating complex mineral data across 30+ commodities into clear, actionable insights for both short-term traders and long-term investors — explore Discovery Alert's discoveries page to understand how historic finds have generated exceptional market returns, and begin your 14-day free trial today to secure a decisive edge before the broader market reacts.