June 17, 2026

The Quiet Revolution Reshaping Global Reserve Architecture

For most of recorded financial history, the composition of sovereign reserve portfolios has shifted glacially. Central banks are not known for speed. Their mandate demands caution, consensus, and long time horizons. Yet something unusual has been unfolding across reserve management desks worldwide, and the pace of change is anything but slow. Over the past four years, central banks increasing gold reserves has become a defining structural trend, with the official sector accumulating gold at roughly double the rate observed in the preceding decade.

Understanding why this is happening requires stepping back from the headlines and examining the deeper mechanics of how reserve managers think about risk, liquidity, and long-term wealth preservation in an era when the geopolitical foundations of the post-war monetary system are visibly fracturing.

When big ASX news breaks, our subscribers know first

Gold's Transformation From Legacy Asset to Strategic Priority

How Reserve Managers Now Classify Gold

The old framing of gold as a relic of the Bretton Woods era, carried on balance sheets more out of inertia than conviction, has been decisively replaced. The World Gold Council's 2026 Central Bank Gold Reserves Survey, now in its ninth consecutive edition, documents a sustained and measurable intensification in positive sentiment toward gold across both advanced economies and emerging market and developing economy central banks.

What the data reveals is not a reactive response to a single crisis, but a deliberate repositioning. Central banks increasingly classify gold as an active strategic instrument, one that is managed, sized, and stored with the same intentionality applied to foreign exchange portfolios or sovereign bond holdings.

The Dollar Question That Reserve Managers Are No Longer Avoiding

The most consequential structural driver behind the gold accumulation trend is the gradual, but increasingly explicit, reassessment of U.S. dollar dominance in global reserves. Survey data from the 2026 edition indicates that 74% of respondents anticipate moderate to significant reductions in dollar holdings within global reserves over the next five years.

Critically, this anticipated reduction is not expected to flow into competing fiat currencies. Respondents broadly expect the euro and renminbi shares of global reserves to remain unchanged. The implied beneficiary is gold, positioning it not merely as a hedge but as the primary alternative reserve instrument in a transitioning monetary order. Furthermore, the declining trust in the US dollar is reinforcing this shift at a structural level.

The structural shift away from dollar-denominated reserves does not appear to be a short-term sentiment swing. It reflects deep concerns about sanctions exposure, dollar weaponisation risk, and the long-term sustainability of U.S. fiscal trajectories.

How Fast Are Central Banks Increasing Gold Reserves? The Data Behind the Surge

Four Years of Unprecedented Accumulation

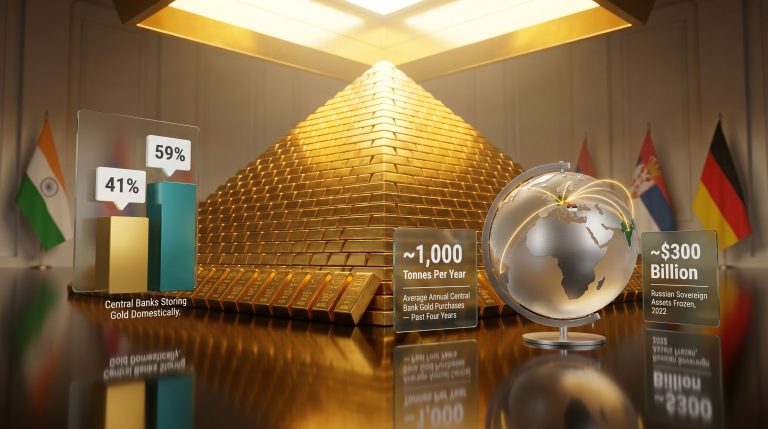

The quantitative evidence for the acceleration in central bank gold buying is striking. Annual net purchases have averaged more than 1,000 tonnes per year over the past four years, compared with an average of approximately 500 tonnes per year across the preceding decade. This doubling in the pace of accumulation has pushed total global central bank gold holdings beyond 35,000 metric tonnes, representing roughly one-fifth of all gold ever mined in human history.

In value terms, gold's share of total global reserves is estimated to have risen to approximately 25% by the end of 2025, up from around 15% at the beginning of the accumulation cycle, driven by a combination of new purchases and substantial price appreciation.

| Metric | Previous Decade Average | Recent 4-Year Average |

|---|---|---|

| Annual central bank gold purchases | ~500 tonnes | ~1,000+ tonnes |

| Global central bank gold holdings | ~33,000 tonnes | 35,000+ metric tonnes |

| Gold's estimated share of global reserves (value) | ~15% | ~25% (est. end 2025) |

| Central banks planning to increase holdings (2026) | Not tracked at this level | 45% (record high) |

| Respondents expecting global reserves to rise (2026) | Not tracked at this level | 89% |

Who Is Driving the Surge?

Emerging market and developing economy central banks have collectively accounted for the majority of net purchases, though the trend spans both advanced and developing nations. The most active accumulators in recent years have included:

- China conducting sustained, systematic accumulation as part of a long-term de-dollarisation framework

- India accelerating purchases whilst emphasising domestic storage and sovereign control over physical holdings

- Turkey emerging as one of the most aggressive buyers relative to total reserve size

- Poland standing out as the most active buyer among European emerging economies

- Uzbekistan maintaining consistent accumulation reflective of a broader Central Asian diversification trend

A landmark data point from April 2026 confirmed that BRICS-plus nations collectively grew their central bank gold reserves beyond 6,000 tonnes, underscoring the degree to which the bloc's reserve strategy is oriented toward reducing structural dependency on Western financial infrastructure.

What Is Driving Central Banks to Buy Gold? A Multi-Factor Framework

Inflation, Geopolitics, and Sanctions Exposure

The motivations behind the central bank gold accumulation trend operate across several distinct but reinforcing dimensions. The World Gold Council identifies three primary themes consistently cited by survey respondents: gold's performance during crisis periods, portfolio diversification benefits, and inflation hedging characteristics.

Beyond these established drivers, two newer factors have gained significant weight in reserve management thinking:

- Geopolitical risk hedging: The freezing of Russian sovereign foreign exchange reserves in 2022 demonstrated that foreign-held reserve assets can be rendered inaccessible through political decisions made by counterparty nations. This event fundamentally altered how reserve managers in non-allied nations calculate custodial risk.

- Sanctions resilience: Gold held domestically cannot be frozen, seized, or sanctioned by a foreign government. This physical property of gold has acquired new strategic value in a world of escalating financial coercion.

The Three Core Investment Objectives Gold Satisfies

For central bank reserve managers, investment decisions must satisfy three non-negotiable criteria. Gold is increasingly recognised as uniquely capable of meeting all three simultaneously:

- Safety: Gold carries no counterparty risk and no default exposure. Its value is not contingent on the creditworthiness of any issuer.

- Liquidity: Physical gold is universally tradeable across jurisdictions and market conditions, including during periods of severe financial stress when other assets may face illiquidity.

- Return: Gold has demonstrated consistent outperformance during episodes of systemic stress, precisely when other reserve assets tend to underperform.

The convergence of safety, liquidity, and return characteristics in a single asset class is genuinely rare. Most instruments excel on one or two dimensions but require trade-offs on the third. Gold's ability to satisfy all three simultaneously is central to its growing share of sovereign portfolios.

How Are Central Banks Funding New Gold Purchases?

The Domestic Purchase Programme Model

One of the more analytically revealing findings from the 2026 survey concerns how central banks intend to fund new gold acquisitions. Approximately 50% of respondents indicated they would source new gold through domestic purchase programmes denominated in local currency, whilst 38% indicated they would sell existing reserve assets to finance new positions.

The domestic purchase programme model deserves particular attention. When a central bank buys gold directly from domestic miners or refiners in local currency, several simultaneous objectives are achieved:

- It builds gold reserves without depleting foreign exchange holdings

- It supports domestic mining industry revenues and employment

- It reduces dependence on international gold markets and pricing mechanisms

- It strengthens the domestic currency by creating demand for local currency in gold settlement

Uganda's 2026 domestic gold purchase programme launch exemplifies this logic. For a mid-sized emerging economy managing currency depreciation pressure and limited access to dollar-denominated instruments, sourcing gold directly from domestic mining output offers a compounding strategic advantage that extends well beyond simple reserve diversification.

Where Is Central Bank Gold Being Stored? The Vaulting Geography Is Shifting

Current Vaulting Preferences

Perhaps the most underreported dimension of the central bank gold story is the accelerating shift in vaulting preferences. The 2026 survey reveals not only where central banks currently store their gold, but a clear directional trend toward repatriation and geographic diversification. According to data on gold reserves by country, these holdings are increasingly diversified across domestic and international custodians.

| Storage Location | 2026 Preference | 2025 Preference | Change |

|---|---|---|---|

| Bank of England | 57% | ~58% | Marginal decline |

| Domestic storage | 49% | ~44% | Notable increase |

| Bank for International Settlements | 16% | ~14% | Slight uptick |

| Swiss National Bank | 6% | 12% | Significant decline |

The Jurisdictional Risk Factor

The movement toward domestic storage is not driven by cost considerations. It reflects a growing concern among reserve managers about jurisdictional control, particularly following high-profile episodes in which sovereign assets held abroad were frozen or made inaccessible through sanctions mechanisms.

The data tells a compelling story of acceleration:

- 9% of respondents increased domestic storage in the past 12 months, up from 5% the prior year

- 10% diversified overseas storage locations in the same period, up sharply from just 2% previously

- 7% plan to increase domestic storage in the coming 12 months

- 9% plan to further diversify overseas vaulting arrangements going forward

The Swiss National Bank's notable decline in preference, falling to 6% from 12% in 2025, is particularly significant. Switzerland's reputation for financial neutrality has historically made it a preferred vaulting location, and its declining appeal signals how fundamentally reserve managers are rethinking even traditionally safe custodial arrangements.

The next major ASX story will hit our subscribers first

Does Central Bank Gold Buying Push Up Gold Prices?

Price Inelasticity and the Structural Demand Floor

Central banks do not behave like retail investors or institutional fund managers when it comes to gold. Their purchasing decisions are governed by strategic reserve management mandates and long-term allocation targets rather than short-term price signals. This price insensitivity creates a structural dynamic that differs materially from other sources of gold demand.

Key price dynamics created by sovereign demand:

- Central bank accumulation programmes establish a structural price floor that persists independently of cyclical movements in retail demand or ETF flows

- As gold prices rise, the proportional value of gold within total reserves increases, which mathematically reinforces the case for further accumulation to maintain target allocation ratios

- Periods of reduced private sector demand can be partially or fully offset by sustained official sector buying, dampening price volatility on the downside

Goldman Sachs analysis from mid-2026 concluded that central bank demand has been stronger than previously estimated by market models and is expected to reaccelerate, a finding that supports the thesis that official sector demand represents a durable, structurally embedded feature of the current gold market rather than a temporary anomaly.

Advanced Economy vs. Emerging Market Central Banks: Where They Agree and Diverge

A Comparison of Strategic Priorities

Despite pursuing the same asset, advanced economy central banks and their emerging market counterparts arrive at gold accumulation decisions through distinct strategic frameworks.

| Dimension | Advanced Economy Central Banks | Emerging Market Central Banks |

|---|---|---|

| Primary motivation | Portfolio diversification, inflation hedging | De-dollarisation, sanctions protection |

| Vaulting preference | Established international custodians | Increasing domestic storage |

| Funding mechanism | Asset reallocation within existing reserves | Domestic programmes in local currency |

| Sentiment trajectory | Positive, stable | Positive, intensifying |

Despite these divergences, both groups share a fundamental conviction in gold as a reliable long-term store of wealth. This shared confidence has strengthened measurably over the nine years the World Gold Council has tracked sentiment data, reaching its highest recorded level in the 2026 survey edition. The broader role of gold in the monetary system continues to evolve as these institutional commitments deepen.

Frequently Asked Questions: Central Banks and Gold Reserves

Why are central banks increasing gold reserves at such a rapid pace?

The acceleration reflects a convergence of pressures including persistent inflation, geopolitical instability, expanded sanctions risk following the freezing of sovereign foreign exchange assets in 2022, and a deliberate policy of reducing structural exposure to dollar-denominated reserve instruments. Gold satisfies all three core reserve objectives simultaneously, making it the preferred diversification vehicle in the current environment.

Which countries are the most active gold buyers?

China, India, Turkey, Poland, and Uzbekistan have been among the most active accumulators in recent years. BRICS-plus nations collectively hold more than 6,000 tonnes of gold, reflecting a broad bloc-level strategy to reduce dependency on Western financial infrastructure. Research from Brookings Institution further contextualises how significant these holdings are within the broader global financial system.

Will the trend continue?

The 2026 World Gold Council survey found that a record 45% of central banks plan to increase gold holdings in the next 12 months, whilst 89% expect global central bank gold reserves to grow over the same period. The structural drivers, including geopolitical fragmentation, dollar uncertainty, and sanctions exposure, show no signs of reversing.

Is this trend speculative?

The accumulation data is drawn from actual reported holdings and verified survey responses. The pace of future accumulation carries uncertainty, as with any forward-looking trend. However, nine consecutive years of intensifying positive sentiment, combined with record-high forward purchasing intentions, provide unusually strong empirical grounding for the thesis that official sector gold demand will remain a dominant market force.

The Long-Term Outlook: Three Conditions That Would Need to Change

The durability of the central banks increasing gold reserves trend is not guaranteed in perpetuity. Analysts can identify three conditions that would, in combination, be required to meaningfully slow the pace of official sector gold buying:

- A sustained and credible reduction in geopolitical tensions and cross-border sanctions risk

- A structural recovery in global confidence in U.S. dollar reserve assets, potentially requiring meaningful fiscal consolidation and a reversal of weaponisation concerns

- A prolonged period of gold price appreciation severe enough to make new purchases fiscally prohibitive for reserve managers operating under budget constraints

None of these conditions appears imminent based on current macro and geopolitical trajectories. The World Gold Council's own forward-looking assessment holds that official sector demand will remain healthy into the foreseeable future, a view reinforced by the record proportion of central banks signalling an intention to increase allocations in the 12 months ahead.

Disclaimer: This article is intended for informational and educational purposes only. It does not constitute financial advice or an investment recommendation. Forecasts, survey projections, and price-related commentary are inherently uncertain. Readers should conduct independent due diligence and consult qualified financial professionals before making investment decisions. Past performance of any asset class, including gold, is not indicative of future results.

Want To Capitalise on the Next Major Mineral Discovery Before the Broader Market Does?

The same structural forces driving central banks to accumulate gold at record levels are creating significant opportunities in ASX-listed mineral exploration — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant discoveries are announced on the ASX, turning complex data across 30-plus commodities into clear, actionable insights. Explore why historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the market.