July 25, 2026

The Minerals Beneath the Megacycle: Why Chile's Export Engine Is Accelerating

Few economic narratives in the current decade are as structurally compelling as the convergence between global decarbonisation ambitions and the geographic concentration of the minerals required to achieve them. The planet's shift away from fossil fuels is not simply an energy story — it is a materials story, and the countries sitting atop the most critical deposits are experiencing a fundamental revaluation of their economic weight. Chile occupies a singular position in this transition, holding two of the most coveted commodities in the clean energy supply chain simultaneously: copper and lithium. Understanding what is driving the exportaciones mineras de Chile impulsadas por cobre y litio requires more than reading headline figures; it demands a closer look at the technical, geopolitical, and market forces reshaping global resource trade.

When big ASX news breaks, our subscribers know first

Chile's Mining Sector as the Backbone of National Trade

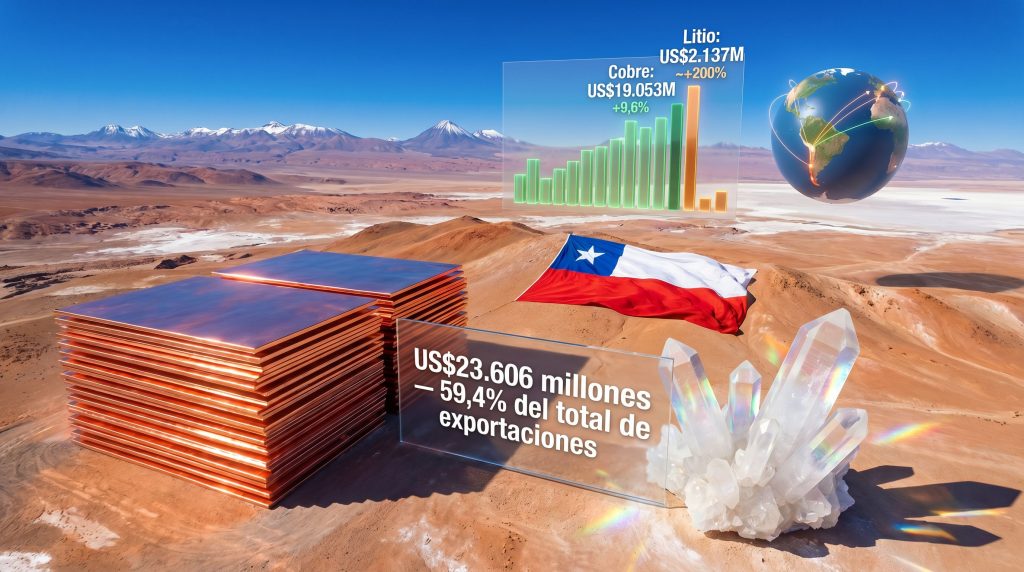

The relationship between Chile's mining industry and its broader economy is unlike almost any other developed mineral producer in the world. The sector does not merely contribute to national output; it effectively defines the character and rhythm of the entire export economy. Between January and April 2026, mining exports reached US$23.606 billion, equivalent to 59.4% of all Chilean exports during the same period, according to data reported by the Subsecretaría de Relaciones Económicas Internacionales (Subrei).

This proportion is not a temporary spike driven by a single commodity price surge. It reflects a multi-decade pattern in which Chilean mineral wealth has consistently underpinned trade balances, fiscal revenues, and regional employment. What distinguishes the 2026 performance is the dual-commodity momentum: copper and lithium growing simultaneously at different rates and for structurally different reasons.

Total national exports reached US$39.772 billion during the first four months of 2026, representing a 12% year-over-year increase compared to the same period in 2025. The mining sector's own growth rate of 19.6% year-over-year outpaced total export growth by a significant margin, illustrating that mining is not merely keeping pace with the broader economy but accelerating ahead of it.

Chile's export performance since 2020 has established consecutive annual records. The first four months of 2026 maintain this trajectory, with Subrei confirming the country has sustained record-breaking export volumes every year for the past six years and that active policy work continues to protect that momentum.

Understanding Chile's Position in the Global Critical Minerals Map

Chile's geological fortune is not accidental. The country straddles one of the most mineralogically productive corridors on Earth — the Andes mountain chain and the Atacama Desert — a combination that has produced the world's largest known copper deposits and one of its most concentrated lithium brine resources. Furthermore, the role of critical minerals in energy transition policy has elevated Chile's strategic importance to governments and manufacturers worldwide.

Copper reserves and production are centred primarily in the Atacama and Antofagasta regions, where porphyry copper deposits of exceptional scale and grade have been mined for over a century. Operations such as Escondida (operated by BHP), the world's single largest copper mine by production volume, and El Teniente, one of the deepest underground copper mines globally, anchor Chile's position as the world's leading copper producing nation with approximately 21% of global mine production based on data from the United States Geological Survey (USGS).

Lithium resources are concentrated in the Salar de Atacama, a high-altitude salt flat that hosts some of the world's richest lithium brine deposits. The lithium brine extraction process differs fundamentally from hard-rock mining: lithium-rich saline groundwater is pumped to the surface and evaporated in large pond systems over several months, concentrating lithium carbonate or lithium chloride solutions before chemical processing. This method is generally lower-cost than hard-rock spodumene mining but is sensitive to water use constraints in an already arid environment.

Chile has historically held approximately 78% of global exports of lithium carbonate, positioning it as the dominant supplier to battery manufacturers worldwide. This share has faced modest competitive pressure from Argentine projects in recent years, but Chile's established infrastructure, processing expertise, and scale continue to distinguish it from newer entrant producers. In addition, the broader Chile lithium strategy centres on maintaining this dominance while moving toward higher-value processed products.

First Quarter 2026: A Statistical Breakdown of Record Performance

The January to April 2026 export data provides a clear statistical portrait of where growth is originating and what is driving it.

| Indicator | Value (Jan–Apr 2026) | Year-on-Year Change |

|---|---|---|

| Total Chilean Exports | US$39.772 billion | +12% |

| Total Mining Exports | US$23.606 billion | +19.6% |

| Mining Share of Total Exports | 59.4% | Rising trend |

| Copper Export Revenue | US$19.053 billion | +9.6% |

| Lithium Export Revenue | US$2.137 billion | ~+200% (approx. tripling) |

| Non-Traditional Exports | US$18.201 billion | +11.4% |

| Services Exports | US$1.197 billion | Not specified |

| Total Trade Exchange | US$69.963 billion | +8.2% |

Several dimensions of this data deserve specific attention beyond the headline numbers.

The non-traditional export figure of US$18.201 billion represents the strongest start to a year in Chilean export history for this category, growing at 11.4% year-on-year. This matters because it signals that the Chilean economy is not purely dependent on mining's success. Agribusiness, processed foods, industrial chemicals, and technology-related services are contributing meaningfully to diversifying export revenue streams.

The total trade exchange figure of US$69.963 billion growing at 8.2% suggests that domestic demand and industrial activity are also expanding, not merely export volumes. An economy absorbing more imports while simultaneously growing exports reflects underlying economic dynamism rather than a narrowly driven commodity windfall. According to reporting on Chile's record export performance, total trade exchange approaching US$70 billion in just four months underscores the extraordinary scale of Chile's current mineral trade cycle.

Copper: The Structural Engine Driving Mineral Export Value

Copper generated US$19.053 billion in export revenue between January and April 2026, representing roughly 80.8% of total mining export revenue despite being just one commodity category. Its 9.6% growth rate is moderate by historical standards during commodity booms, but the sustained nature of that growth across all copper product categories is notable. The Chile copper price outlook remains closely watched by global investors given its outsized influence on national fiscal performance.

What Copper Export Categories Are Growing

The growth in copper exports was broad-based rather than concentrated in a single product tier, which indicates underlying volume expansion rather than a price-only effect:

- Copper cátodos (cathodes): High-purity refined copper at 99.99% Cu concentration, the premium tier of copper exports. Cathodes are directly used in wiremaking, electrical infrastructure, and high-conductivity industrial applications. Demand from power grid expansion projects and EV charging infrastructure construction drove increased offtake.

- Copper concentrates: Partially processed ore containing 20–40% copper by weight, mixed with sulfur and iron compounds. Concentrates require buyer-side smelting and refining, making them the preferred product for export to Asian processing hubs with integrated smelter capacity.

- Copper ánodos and blíster: Intermediate refining stages that serve specific downstream processors. Ánodos (anodes) are used in electrolytic refining to produce final cathode product. Blíster copper at 98–99% purity serves markets that conduct final refining within their own facilities. Both categories contributed positively to total copper export growth in the period.

Why Global Copper Demand Is Structurally Different Now

Historically, copper demand tracked construction cycles, industrial output, and general economic activity. However, the current demand cycle has fundamentally changed character. Three structural drivers now underpin long-term copper consumption in ways disconnected from traditional economic cycles:

- Renewable energy infrastructure: Solar photovoltaic and wind power installations require between 1 and 2 tonnes of copper per megawatt of installed capacity for wiring, inverters, and grid interconnection. According to the International Renewable Energy Agency (IRENA), global renewable additions have accelerated substantially since 2022, with hundreds of gigawatts added annually worldwide.

- Electric vehicle adoption: A single battery electric vehicle requires approximately 60–100 kilograms of copper compared to 20–30 kilograms in a conventional internal combustion engine vehicle. The International Energy Agency (IEA) has documented global EV sales reaching approximately 14 million vehicles in 2023, with projections pointing toward 35–40 million annually by 2030.

- Grid modernisation and electrification: Power transmission and distribution upgrades in both developed and emerging economies require enormous copper volumes for cables, transformers, and substations. India, Southeast Asia, and parts of Africa represent multi-decade electrification demand that has barely begun to materialise.

Industry analysts and commodities research firms, including S&P Global and Fitch Solutions, have projected the emergence of structural copper supply deficits by 2027–2028 if current mine development pipelines fail to accelerate. New copper deposits face 15–20 year development timelines from discovery to first production, meaning supply responsiveness to current demand signals is severely constrained.

The emerging copper supply crunch is consequently reinforcing Chile's strategic importance to governments and manufacturers seeking to secure reliable access to refined copper and concentrate volumes over the medium term.

Chile's Competitive Positioning in Global Copper Markets

| Metric | Data |

|---|---|

| Chile's share of global copper concentrate exports (2024) | ~29% |

| Chile's share of global copper cathode exports (2024) | ~20% |

| Chile's share of global copper mine production | ~21% (USGS data) |

| Copper export growth rate (Jan–Apr 2026) | +9.6% year-on-year |

| Copper share of total mining exports (Jan–Apr 2026) | ~80.8% |

One underappreciated dynamic in Chilean copper production is the grade decline challenge. Average ore grades at many of Chile's flagship deposits have been declining over time as higher-grade ore at shallower depths becomes depleted. Lower grades require processing more rock to extract the same amount of copper, increasing energy consumption, water use, and operational costs per unit of output. This represents a meaningful medium-term constraint on Chile's ability to grow copper export volumes even as demand accelerates.

Lithium: The Fastest-Growing Commodity in Chile's Export Portfolio

If copper is the structural engine of Chilean mineral exports, lithium is its most dynamic accelerant. Between January and April 2026, lithium exports reached US$2.137 billion, representing an approximate tripling of revenue compared to the same period in 2025. This makes lithium the fastest-growing commodity within the entire Chilean export basket by percentage, and consequently its trajectory carries implications far beyond the current reporting period.

The Chemistry of Chilean Lithium Exports

Understanding why different lithium compounds command different market positions requires a brief technical primer:

- Lithium carbonate (Li₂CO₃): The primary export form from Chilean operations, produced from brine processing at the Salar de Atacama. Used predominantly by cathode manufacturers in China, South Korea, and Japan as an input for lithium iron phosphate (LFP) and other battery chemistries.

- Lithium hydroxide (LiOH·H₂O): A higher-processed form preferred for nickel-manganese-cobalt (NMC) and nickel-cobalt-aluminium (NCA) cathode chemistries used in high-performance EV batteries. Commands a price premium over carbonate and requires additional chemical conversion steps.

- Lithium sulfate: An intermediate chemical compound produced during certain processing routes, with niche industrial applications and specialty export markets.

The product mix shift within Chilean lithium exports — with hydroxides gaining relative importance alongside carbonate and sulfate volumes — reflects a broader industry objective to capture more value domestically before export rather than selling lower-processed intermediates.

Where Chilean Lithium Is Going

| Destination | Estimated Share | Primary Application |

|---|---|---|

| China | ~55% (est. US$840 million+) | Battery cell manufacturing, cathode production |

| South Korea | Significant | EV battery supply chains (Samsung SDI, LG Energy) |

| Japan | Significant | Consumer electronics, energy storage |

| United States | Growing | Critical mineral supply chain diversification |

China's dominance as a lithium offtake destination reflects its position as the world's largest battery manufacturing ecosystem. However, the United States' growing share reflects a shifting geopolitical calculus: North American battery supply chain development initiatives are creating new demand pathways for Chilean lithium that were minimal just five years ago. Chilean mining exports in 2026 have consequently attracted renewed attention from trade analysts examining how export destination diversification is reshaping Chile's commercial relationships.

A Speculative but Plausible Scenario: The Hydroxide Premium Shift

An underappreciated dynamic worth flagging for industry observers is the potential acceleration of lithium hydroxide's market share relative to carbonate over the next five years. As NMC battery chemistries gain ground in the premium EV segment, demand for hydroxide is expected to grow faster than carbonate demand. Chilean producers that have invested in conversion infrastructure to produce hydroxide domestically will be positioned to capture this premium, provided they can compete on conversion cost with Asian hydroxide producers who currently hold significant scale advantages.

Disclaimer: Projections regarding lithium hydroxide demand growth, market share shifts between battery chemistries, and Chilean producer positioning involve significant uncertainty and should not be interpreted as investment advice. Commodity markets are subject to technological disruption, policy changes, and competitive dynamics that can materially alter outcomes.

The next major ASX story will hit our subscribers first

Mining Concentration vs. Structural Diversification: Reading Both Signals

The 59.4% share of total exports represented by mining is simultaneously a source of strength and a structural vulnerability that economic analysts and policymakers have grappled with for decades.

The Concentration Risk Dynamic

High commodity concentration exposes national economies to several interconnected risks:

- Price volatility pass-through: Sharp declines in copper or lithium prices translate directly into export revenue reductions, fiscal shortfalls, and reduced government spending capacity. This pro-cyclicality has historically produced boom-bust patterns in resource-dependent economies.

- Demand concentration risk: China absorbing a dominant share of Chilean mineral exports creates a bilateral dependency that makes Chilean revenues sensitive to Chinese economic conditions, trade policy decisions, and domestic industrial transitions.

- Production stagnation risk: Despite strong revenue growth in 2026, Chilean copper production volumes have shown signs of stagnation in physical output terms in recent years. Revenue growth driven primarily by prices rather than volumes is less sustainable over multi-year horizons.

The Diversification Signal Within the Data

The non-traditional export figure of US$18.201 billion (+11.4%) and its status as the best start to a calendar year in Chilean history for this category provides a meaningful counter-narrative. Even within traditionally mining-dominated regions, new dynamics are emerging. The Antofagasta region reportedly recorded export growth exceeding 80% in sectors unrelated to copper or lithium during the first quarter of 2026, suggesting that industrial ecosystems around mining infrastructure are beginning to generate independent economic activity.

Services exports of US$1.197 billion represent another diversification vector, encompassing mining-related technical services, financial services, and increasingly technology and professional services that leverage Chile's relative institutional stability and infrastructure quality compared to regional peers.

The Long-Term Demand Horizon for Chilean Minerals

| Mineral | Primary Demand Driver | Forward Outlook |

|---|---|---|

| Copper | Electrification, EVs, renewables | Structural deficit projected post-2027 |

| Lithium | EV batteries, grid storage | Potential demand tripling by 2030 |

| Additional critical minerals | Regional mining diversification | Expanding across northern Chile |

The World Bank has identified copper as having one of the highest demand-growth trajectories among all industrial metals through 2050, with cumulative copper requirements for energy transition infrastructure potentially exceeding total copper production in the previous 30 years. Lithium faces an equally compelling demand projection: the IEA's stated policies scenario suggests global lithium demand could more than triple between current levels and 2030, driven almost entirely by the EV battery manufacturing ramp.

These projections carry important caveats. Battery technology evolution, particularly the commercial maturation of sodium-ion chemistries for short-range vehicles and stationary storage, could reduce per-vehicle lithium intensity at the margin. Furthermore, recycling rates for both metals will increase as more end-of-life batteries and electrical infrastructure reach recyclable condition, creating secondary supply streams that partially offset primary mine demand.

Risk Factors That Could Constrain Chile's Export Trajectory

Despite the strength of the current performance, several structural risks require consideration:

- Physical production stagnation in copper: Revenue growth masks the challenge that actual copper tonnage produced has shown limited growth in recent years. Without new major mine development or processing efficiency improvements, Chilean copper export growth remains price-dependent rather than volume-driven.

- Regulatory and environmental pressures: Expansion of mining operations in Chile requires increasingly complex environmental impact assessments and indigenous community consultation processes. Projects in the pipeline face multi-year approval timelines that delay capacity additions.

- Water scarcity in the Atacama: Both copper and lithium operations in northern Chile operate in one of the world's driest environments. Water use constraints are intensifying as climate change reduces the already minimal rainfall and communities and ecosystems compete with industrial users for scarce freshwater resources.

- Geopolitical trade risk: Should major consuming nations impose tariffs, redirect procurement toward alternative suppliers, or accelerate domestic recycling programmes, Chilean export volumes could face demand pressure regardless of underlying production capacity.

- Value chain positioning: Chile exports primarily raw and semi-processed minerals rather than manufactured components or final products. The economic value captured per tonne of copper or lithium exported is fundamentally lower than what accrues to countries manufacturing batteries, motors, or generators from those same minerals.

Strategic Opportunities Chile Is Positioned to Capture

The concentration risks outlined above are counterbalanced by a set of strategic opportunities with genuine long-term potential:

- Lithium industrialisation: Converting a greater share of lithium carbonate into hydroxide or more advanced cathode precursor materials domestically would increase export revenue per tonne and capture a larger share of battery supply chain value within Chile.

- ESG-compliant mining positioning: As European and North American buyers implement increasingly stringent supply chain due diligence requirements, Chilean producers operating under established environmental and social governance frameworks can differentiate from competitors in higher-risk jurisdictions.

- Expansion into additional critical minerals: Northern Chilean geology contains deposits of cobalt, manganese, and rare earth elements that remain underdeveloped. Diversification within the mineral portfolio would reduce concentration risk while leveraging existing mining infrastructure.

- Trade agreement deepening with Southeast Asia: Vietnam, Indonesia, Thailand, and other rapidly industrialising economies are emerging as significant battery manufacturing and EV assembly hubs. Strengthening commercial relationships with these markets would diversify export destinations away from China-concentration risk.

Frequently Asked Questions

How much did Chile's mining sector export in the first four months of 2026?

Chile's mining sector exported US$23.606 billion between January and April 2026, reflecting a 19.6% increase compared to the same period in 2025 and accounting for 59.4% of all national exports during the period.

Why did lithium exports nearly triple in early 2026?

The surge in lithium export revenue to US$2.137 billion in the first four months of 2026 reflected a combination of higher global demand for lithium carbonate, sulfate, and hydroxide products driven by battery manufacturing expansion, alongside increased export volumes from Chilean operations at the Salar de Atacama.

What is the difference between lithium carbonate and lithium hydroxide exports?

Lithium carbonate is the primary processed form of lithium produced from brine evaporation and is used in a wide range of battery cathode chemistries. Lithium hydroxide requires additional chemical conversion and commands a price premium due to its suitability for high-energy-density NMC battery applications used in premium electric vehicles.

What is the structural copper deficit and why does it matter for Chile?

Multiple commodities research firms project that global copper consumption will exceed annual mine supply capacity by 2027–2028 if the current mine development pipeline does not accelerate. This projected deficit creates price support for copper exports and increases the economic value of Chile's production capacity.

What share of global lithium carbonate exports does Chile hold?

Chile has historically maintained approximately 78% of global lithium carbonate export market share, though competitive pressure from Argentine brine projects and Australian hard-rock producers has introduced some variability into this figure in recent years.

What are Chile's non-mining export strengths?

Non-traditional exports reached US$18.201 billion in January through April 2026, their strongest opening period on record, growing at 11.4% year-on-year. Key non-mining export sectors include agribusiness products, processed food, forestry products, industrial chemicals, and technology-related services.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking projections regarding commodity demand, price trajectories, and export performance involve inherent uncertainty and should not be relied upon as forecasts of future outcomes. All financial figures cited are sourced from Subrei reporting as reproduced by Reporte Minero (May 2026). Independent verification from primary government statistical sources is recommended for formal analytical purposes.

Want to Capitalise on the Next Major Mineral Discovery Before the Market Moves?

Chile's copper and lithium export surge underscores just how transformative critical mineral discoveries can be — and Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts the moment significant mineral discoveries are announced, turning complex data across 30+ commodities into clear, actionable insights for investors at every level. Explore historic examples of discovery-driven returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to position yourself ahead of the broader market.