July 27, 2026

The Coming Scarcity: Why the De Beers Sale Matters Beyond the Boardroom

Every generation or so, the global diamond industry experiences a structural reset that reshapes supply chains, recalibrates pricing power, and redefines who controls the world's most emotionally marketed commodity. The pending sale of De Beers by Anglo American is one of those moments. To understand why the De Beers sale in weeks not months timeline carries such weight, you need to look past the transaction itself and toward the deeper forces converging on the natural diamond market simultaneously.

The timing is not incidental. A tightening supply outlook, a bifurcating demand environment, and a once-in-a-generation ownership transition are colliding in a way that will reshape the industry's architecture for decades. Furthermore, the broader mining consolidation trends shaping the sector in 2025 provide important context for understanding why Anglo American moved when it did.

When big ASX news breaks, our subscribers know first

Anglo American's Strategic Exit and Why It Took Two Years

Anglo American placed its 85% stake in De Beers on the market in May 2024, as part of a deliberate restructuring effort aimed at concentrating its portfolio around copper, iron ore, and crop nutrient assets. The decision was not made in isolation. A prolonged period of diamond price weakness, accelerating synthetic diamond penetration into mainstream retail, and sustained investor pressure to simplify Anglo's asset base all converged to make De Beers a logical divestiture candidate.

Two years is a long runway for a major asset sale, and that timeline reflects the transaction's unusual complexity. De Beers is not a straightforward commodity asset. It carries brand equity, a proprietary sightholder sales system, sovereign stakeholder entanglements across four African nations, and a marketing heritage that no pure-play mining acquisition can replicate.

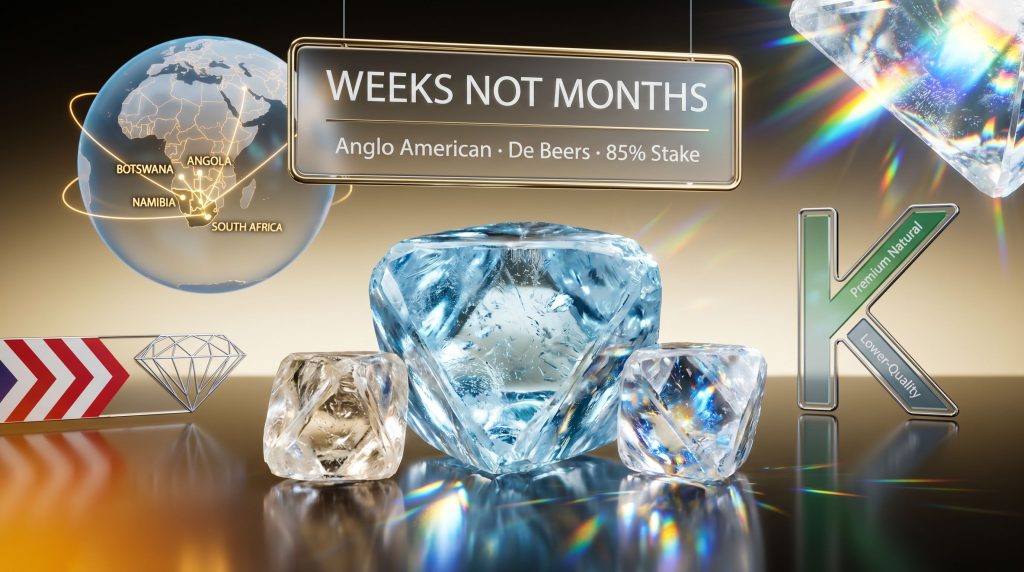

De Beers CEO Al Cook confirmed at the Reuters NEXT Europe conference in London that negotiations have reached a stage of maturity placing a formal transaction closer than at any previous point in the process, with the possibility of closure measured in weeks rather than months. In major resource M&A, this kind of precise, public language from a sitting CEO at an institutional forum is rarely imprecise. It signals that term sheets are advanced, exclusivity arrangements may be in place, and the final commercial and governance terms are being resolved rather than negotiated from scratch.

From Six Consortia to Two: How the Bidding Field Collapsed

At the height of competitive interest in 2025, as many as six separate consortia were pursuing Anglo American's De Beers stake. By mid-2026, that field had narrowed to two remaining groups. This compression is entirely normal in large-scale resource M&A, where early-stage interest is abundant but the capacity to commit multi-billion-dollar capital across complex multi-jurisdictional governance structures filters out all but the most serious participants.

The two surviving consortia share a notable structural characteristic: both incorporate diamond-producing nation governments alongside private capital partners. Botswana, which already holds a 15% equity stake in De Beers, is understood to be an anchor participant in at least one consortium. The governments of Namibia and Angola are also reported to be involved in bidding groups. For context on how these nations compare more broadly, the leading diamond-producing countries are each navigating their own strategic interests within this process.

Alongside sovereign participants, the consortia reportedly include:

- Former De Beers CEO Gareth Penny, now serving as chair of asset manager Ninety One

- A Qatari sovereign-linked investment fund, reflecting the Gulf region's deepening appetite for hard-asset exposure

- Israeli businessman Nir Livnat, adding a privately-held strategic dimension

This composition matters because it signals that the future ownership architecture of De Beers will not be a conventional corporate acquisition. It will be a hybrid governance model where nation-state interests, institutional capital, and strategic industry operators must collectively manage one of the world's most complex diamond businesses.

The Public-Private Partnership Model: Governance Risks Rarely Discussed

The phrase public-private partnership sounds collaborative in theory. In practice, when applied to a company like De Beers, it introduces structural tensions that investors and analysts rarely examine in depth.

Sovereign government shareholders typically prioritise employment preservation, in-country beneficiation, royalty maximisation, and national economic objectives. Private capital partners, however, prioritise return on invested capital, distribution efficiency, and balance sheet discipline. These are not inherently compatible in periods of market stress.

Consider the precedent already set by Botswana. In 2023, the Botswanan government successfully renegotiated its Debswana sales agreement with De Beers, securing a larger proportion of rough diamond production to be processed domestically rather than exported in raw form. This shift away from traditional cutting centres like Antwerp and Mumbai toward in-country beneficiation is a template that Namibia and Angola are likely to pursue aggressively under a new ownership structure.

The emerging ownership model blends sovereign economic priorities with private capital efficiency demands, creating a governance architecture that will require exceptional diplomatic and commercial management to navigate effectively.

For the global sightholder network, which depends on predictable rough diamond allocation from De Beers' periodic sales events called sights, this governance complexity introduces meaningful supply allocation uncertainty.

What Is a Diamond Sight?

A sight is De Beers' proprietary rough diamond sales mechanism, through which a carefully vetted group of pre-approved buyers called sightholders receive allocations of rough stones at fixed prices. Sightholders cannot negotiate the price or reject individual parcels without consequence. The system has historically given De Beers extraordinary pricing power and supply discipline.

The cancellation of De Beers' August 2026 sight, merged into a combined September event, reflects deliberate volume management in response to weak market conditions. This kind of supply discipline, while operationally disruptive to sightholders in the short term, demonstrates De Beers' willingness to prioritise per-carat economics over volume throughput. Notably, the De Beers sale details covered by JCK outline further nuances of how this transition may affect commercial operations.

The Diamond Market's K-Shaped Recovery: What It Actually Means

Al Cook has described the current diamond demand environment as K-shaped, a term borrowed from macroeconomic analysis to describe a bifurcated recovery where different segments of the market move in opposite directions simultaneously.

In diamond market terms, this means:

- Premium-quality natural diamonds (high clarity, exceptional colour, large carat weights) are experiencing strengthening demand and firming prices, driven by ultra-high-net-worth consumers globally

- Lower-to-mid quality natural diamonds remain at structurally depressed valuations, where price competition from lab-grown alternatives has been most severe

This divergence has profound strategic implications. It rewards producers with high average stone quality and strong brand associations, while penalising volume-focused producers whose output competes directly with synthetics on price.

| Market Segment | Recovery Trajectory | Primary Driver |

|---|---|---|

| Premium natural diamonds (D-IF to VVS) | Strengthening | Scarcity premium, UHNW demand |

| Mid-range natural diamonds | Flat to slightly recovering | Partial synthetic substitution |

| Lower-quality natural diamonds | Structurally depressed | Lab-grown price parity achieved |

| Lab-grown diamonds | Rapid supply expansion | Manufacturing cost compression |

| Coloured natural diamonds | Appreciating | Extreme rarity, collector demand |

The lab-grown diamond sector has not, as some predicted, destroyed the natural diamond market uniformly. Instead, it has acted as a structural filter, separating genuinely scarce natural stones from commodity-grade production. This is arguably one of the most underappreciated dynamics in the diamond industry today.

Supply Contraction: The Geological Reality Most Investors Overlook

Beyond the ownership transition and the demand recovery narrative lies a geological constraint that fundamentally alters the long-term supply picture for natural diamonds. The consolidation pressures in mining more broadly have, in addition, accelerated a shift toward fewer, higher-quality operations globally.

The global diamond mining industry has recorded only one commercially viable new diamond discovery in the entire 21st century. This is an extraordinary statistic. Kimberlite pipes, the primary geological formation hosting gem-quality diamonds, are extraordinarily rare, and the economics of finding, evaluating, and developing a new diamond mine from discovery to production typically span 15 to 25 years and require multi-billion-dollar capital commitments.

Compounding this structural scarcity are near-term mine closures projected across South Africa, Lesotho, and Canada by the end of 2027. These are not speculative. They represent known end-of-mine-life scenarios for several established operations whose ore reserves are depleting without viable extensions. The global mine depletion trends visible in precious metals offer a useful parallel for understanding how this contraction may unfold in diamonds.

The supply-demand framework for natural diamonds beyond 2027 looks substantially different from today:

| Factor | Direction | Timeframe |

|---|---|---|

| Major mine closures (SA, Lesotho, Canada) | Supply reduction | 2025-2027 |

| New commercial kimberlite discoveries | Near-zero pipeline | Long-term structural |

| De Beers' deliberate volume cuts | Short-term supply tightening | 2024-2026 |

| Lab-grown supply expansion | Ongoing volume growth | Continuous |

| Premium natural diamond demand | Gradual recovery | 2025-2028 |

This supply contraction thesis does not mean natural diamond prices will automatically recover uniformly. The K-shaped dynamic suggests that scarcity premiums will accrue most aggressively to high-quality stones, while synthetic alternatives continue suppressing the commodity end of the market. Furthermore, the declining discovery pipeline across the broader minerals sector reinforces just how structurally challenged new supply origination has become.

The next major ASX story will hit our subscribers first

China's Marriage Rate Decline: A Structural Demand Shock

One of the most consequential but underreported drivers of diamond demand weakness over the past three years has been the structural decline in China's marriage rate. China became one of the world's largest engagement ring markets during the early 21st century, absorbing substantial volumes of De Beers' mid-range production.

Chinese registered marriages have been declining consistently since peaking in 2013, falling from approximately 13.5 million marriages annually to around 6.8 million in 2023, according to China's Ministry of Civil Affairs data. This is not a cyclical fluctuation driven by economic sentiment. It reflects deep demographic and cultural shifts, including urbanisation, rising female educational attainment, increasing average marriage age, and changing attitudes toward traditional family formation.

For De Beers and the broader natural diamond industry, this represents a permanent reduction in a key demand segment, not a recoverable cyclical dip. The engagement ring market in China that existed in 2015 is unlikely to return at the same scale regardless of macroeconomic conditions.

What Anglo American Achieves Through the Sale

From Anglo American's perspective, completing the De Beers divestiture resolves several strategic problems simultaneously:

- It removes a structurally challenged, brand-dependent asset from a portfolio increasingly focused on industrial commodities with clearer long-term demand profiles

- It eliminates the earnings volatility associated with diamond price cycles from Anglo's financial reporting

- It generates significant capital proceeds that can be redeployed toward copper and crop nutrient assets, which carry stronger consensus demand outlooks tied to electrification and global food security

- It completes the restructuring program that Anglo initiated in 2024 in response to investor pressure to simplify its portfolio and improve valuation multiples

The divestiture also removes Anglo from the complex geopolitical and governance dynamics of multi-sovereign diamond operations, allowing the company to operate within a more straightforward corporate structure. Consequently, the De Beers sale in weeks not months represents a decisive endpoint to a two-year strategic repositioning effort.

Frequently Asked Questions

When Could the De Beers Sale Be Finalised?

Based on De Beers CEO Al Cook's public statements at the Reuters NEXT Europe conference in London, the De Beers sale in weeks not months is the expected timeline as of mid-2026. Anglo American has confirmed its intention to provide a formal update on the sale during 2026. No binding completion date has been publicly disclosed.

What Happens to De Beers' Operations After the Sale?

De Beers' operational footprint spanning Botswana, Namibia, Angola, South Africa, and Canada is expected to remain intact. The primary changes will occur at the ownership, governance, and strategic allocation level, particularly regarding where rough diamond processing occurs across producing nations.

How Does Lab-Grown Diamond Growth Affect the Transaction Valuation?

Synthetic diamond proliferation has structurally impacted the lower-quality natural diamond segment and contributed to three years of broad demand decline. This introduces valuation uncertainty around De Beers' commodity-grade production volumes, while the premium natural diamond segment retains stronger pricing power. Bidders will need to model both dimensions carefully into their acquisition pricing.

Why Did the Number of Bidders Fall from Six to Two?

The complexity of financing and structuring a multi-jurisdictional acquisition involving sovereign stakeholders, sightholder obligations, and a bifurcated market outlook filtered out all but the most capitalised and strategically motivated participants. This consolidation is consistent with large-scale natural resource M&A processes globally. The De Beers sale in weeks not months outcome, however, suggests that the remaining consortia have reached sufficient alignment to bring negotiations to a close.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, projections, and market analysis involve inherent uncertainty and should not be relied upon as the basis for any investment decision. Readers should conduct their own independent research and consult qualified financial professionals before making any investment decisions.

Want to Track the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, translating complex geological and market data into actionable investment insights for both short-term traders and long-term investors. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated extraordinary returns, and begin your 14-day free trial today to position yourself ahead of the market.