July 27, 2026

Fortescue to buy Alta Copper is reshaping the mining landscape as iron ore giants pivot toward critical metals exposure. This strategic acquisition demonstrates how traditional bulk commodity producers are positioning themselves ahead of anticipated copper supply constraints driven by the global energy transition.

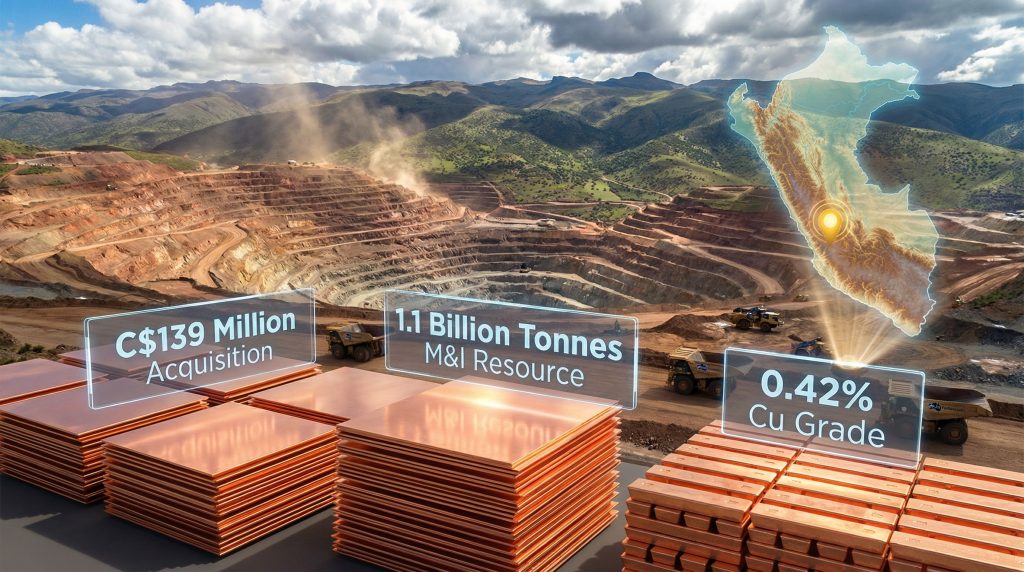

Fortescue Metals Group's decision to acquire the remaining 64% stake in Alta Copper Holdings Inc. for C$139 million represents more than portfolio diversification. The transaction signals heightened competition for development-stage copper assets as major mining companies recognise the strategic value of securing future production capacity.

Strategic Context: Iron Ore Giants Enter Copper Consolidation Phase

The global mining landscape is witnessing a fundamental shift as iron ore producers pivot toward copper exposure through strategic acquisitions. This transition reflects deeper structural forces reshaping commodity markets, where traditional bulk material specialists are recognising copper's critical role in the energy transition economy.

Fortescue to buy Alta Copper exemplifies this strategic evolution through its acquisition valued at approximately $101 million USD. The transaction represents more than a simple portfolio diversification play. It signals the emergence of a new competitive dynamic where iron ore majors are leveraging their capital advantages to secure copper assets before supply constraints become critical.

Table: Major Mining Companies' Copper Exposure Strategies

| Company | Primary Focus | Copper Strategy Status | Strategic Rationale |

|---|---|---|---|

| Fortescue | Iron ore | Active acquisition (Alta Copper) | Portfolio diversification |

| BHP Group | Diversified mining | Seeking copper opportunities | Critical minerals exposure |

| Rio Tinto | Iron ore/aluminium | Portfolio evaluation | Energy transition positioning |

| Vale | Iron ore/base metals | Project development focus | Supply chain integration |

The timing of these moves reflects several converging factors. Iron ore markets face cyclical volatility tied to Chinese steel demand patterns, whilst record-high copper prices show sustained growth driven by electrification infrastructure requirements.

Mining companies with strong balance sheets are positioning themselves ahead of what analysts describe as a potential copper supply deficit emerging in the late 2020s. Furthermore, copper investment strategies increasingly focus on securing long-term production capability.

Fortescue's approach through its Nascent Exploration subsidiary demonstrates sophisticated transaction structuring. This vehicle allows operational independence for copper development activities whilst maintaining clear separation from the parent company's established iron ore operations.

The competitive landscape among iron ore producers has intensified as companies recognise that copper assets with advanced feasibility studies are becoming scarce. Projects like Cañariaco command premium valuations precisely because they offer shorter development timelines compared to early-stage exploration targets.

When big ASX news breaks, our subscribers know first

What Does the C$139 Million Valuation Signal About Copper Asset Pricing?

The Alta Copper acquisition provides critical insights into how the market values development-stage copper assets in today's supply-constrained environment. Fortescue's acquisition announcement of C$1.40 per share represents a 14.8% premium to Alta Copper's Friday closing price.

Valuation Metrics Analysis

- Total transaction value: C$139 million for 64% stake

- Implied total equity value: Approximately C$217 million

- Resource base: 2.0 billion tonnes total (1.1 billion M&I + 0.9 billion Inferred)

- Effective cost per tonne: ~C$108.5 per tonne of total resource

- Contained copper value: Approximately 4.6 billion pounds in M&I category

This valuation framework reveals several important market dynamics. The transaction implies Fortescue to buy Alta Copper at roughly $22 million per billion pounds of measured and indicated copper resource. This metric places significant value on resource certainty and geological confidence.

The pricing also reflects Peru's position as a relatively stable mining jurisdiction. However, the country faces periodic political uncertainty and community relations challenges. This regulatory stability premium becomes particularly valuable as miners evaluate global development opportunities.

Risk-Adjusted Valuation Factors

The Cañariaco project's dual copper-gold nature adds complexity to valuation calculations. Porphyry deposits containing both metals require specialised processing circuits, increasing capital expenditure requirements but also providing revenue diversification.

Processing considerations significantly impact project economics. Copper-gold separation requires flotation circuits capable of producing separate concentrate streams, each with different metallurgical recovery rates and processing costs. These technical requirements influence both initial capital investment and ongoing operational expenditure projections.

The transaction also signals broader market expectations about copper price trajectories. With copper recently hitting record levels above $5.46 per pound, acquiring development-stage projects at current valuations reflects confidence that elevated pricing will persist through project development timelines.

How Does the Cañariaco Project Compare to Global Copper Development Pipeline?

Cañariaco's position within the global copper development landscape reveals both its competitive advantages and the strategic value that attracted Fortescue's acquisition interest. The project's 2.0 billion tonne resource base places it among significant undeveloped copper deposits worldwide.

Resource Quality Assessment

The measured and indicated resource of 1.1 billion tonnes grading 0.42% copper equivalent represents substantial tonnage at grades typical of large porphyry systems. This grade profile aligns with gold-copper exploration insights demonstrating industry trends toward larger, lower-grade operations.

Table: Cañariaco Versus Global Development Projects

| Project | Resource (Billion Tonnes) | Grade (% Cu) | Location | Development Status |

|---|---|---|---|---|

| Cañariaco Norte/Sur | 2.0 (combined) | 0.42% / 0.29% | Peru | Advanced feasibility |

| Pebble (Alaska) | 6.4 | 0.40% | USA | Permitting challenges |

| Resolution (Arizona) | 1.9 | 1.47% | USA | Environmental review |

| Escondida Phase 4 | Various | 0.5-0.8% | Chile | Expansion planning |

The comparison reveals Cañariaco's competitive positioning. Whilst smaller than mega-projects like Pebble, its advanced feasibility status provides near-term development potential that larger, more complex projects cannot match.

Production Potential Analysis

Industry projections for Cañariaco suggest annual copper production capacity between 150,000 and 200,000 tonnes once fully operational. This scale positions the project as a mid-tier copper producer, contributing meaningfully to global supply.

- Accelerated development scenario: Production by 2030

- Base case timeline: Commercial production 2031-2032

- Conservative approach: Phased development beginning 2032-2033

The project's location in northern Peru provides access to established mining infrastructure. This infrastructure availability reduces both development costs and execution risks compared to greenfield projects in remote locations.

Technical Considerations and Challenges

Cañariaco's porphyry-style mineralisation presents both opportunities and complexities. The copper-gold association provides revenue diversification but requires sophisticated metallurgical processing to achieve optimal recovery rates.

Water management represents a critical operational consideration in Peru's arid northern regions. Large-scale copper processing requires substantial water volumes for ore processing, dust control, and tailings management.

Why Are Iron Ore Majors Targeting Copper Now?

The strategic rationale driving iron ore companies toward copper acquisition reflects fundamental shifts in global copper supply forecast patterns and long-term market structure evolution.

Demand Trajectory Analysis

Global copper demand faces unprecedented growth drivers linked to electrification trends across multiple sectors. Electric vehicle production requires 2-4 times more copper per unit than conventional vehicles, whilst renewable energy infrastructure demands substantial copper content.

- Electric vehicle sector: Growing from 10% to potentially 50%+ of global auto production

- Renewable energy: Wind and solar installations requiring significant copper infrastructure

- Grid modernisation: Transmission upgrades supporting renewable integration

- Energy storage: Battery systems and supporting electrical infrastructure

Supply Constraint Reality

Copper supply growth faces structural limitations that create compelling investment opportunities. Major producing mines worldwide are experiencing grade decline as higher-grade ore bodies become depleted.

New discovery rates have declined significantly over recent decades. Major copper discoveries exceeding 5 million tonnes contained copper have become increasingly rare, with most new resources coming from extensions of existing deposits.

Strategic Positioning Advantages

Iron ore companies possess unique capabilities that translate effectively to copper development:

- Capital availability: Multi-billion dollar balance sheets supporting large-scale development projects

- Operational expertise: Experience managing complex mining operations and large-scale infrastructure

- Regulatory relationships: Established government and community relations in key mining jurisdictions

- Technical capabilities: Engineering and metallurgical expertise applicable across commodity types

Portfolio Risk Management

Copper diversification provides iron ore producers with exposure to different demand cycles and price dynamics. Iron ore markets remain heavily influenced by Chinese steel production patterns, creating cyclical volatility.

The energy transition also presents potential long-term challenges for steel demand as construction materials shift toward lower-carbon alternatives. Copper's central role in electrification provides exposure to growth sectors likely to expand regardless of traditional steel industry evolution.

What Are the Regulatory and Operational Risk Factors?

Peru's mining regulatory framework presents both opportunities and challenges for international copper developers. The country hosts numerous successful copper operations, demonstrating regulatory pathway viability, but recent political developments have introduced additional complexity.

Regulatory Environment Assessment

Peru's mining code provides established frameworks for permitting, environmental compliance, and operational oversight. The country has attracted significant mining investment over decades, creating institutional knowledge and procedural precedents.

Table: Peru Mining Risk Assessment Matrix

| Risk Factor | Risk Level | Impact Severity | Mitigation Strategies |

|---|---|---|---|

| Political stability | Medium | High | Long-term agreements, government relations |

| Environmental permitting | Medium-High | Medium | Early community engagement, environmental planning |

| Tax regime changes | Medium | Medium | Fiscal stability agreements, legal protection |

| Community relations | High | Medium | Social investment programmes, local employment |

| Infrastructure access | Low | Low | Existing regional connectivity |

Political Risk Dynamics

Peru has experienced political volatility in recent years, with changes in government potentially affecting mining policy approaches. However, mining remains a critical component of Peru's economy, generating substantial government revenues and employment.

Successful mining companies in Peru typically establish long-term relationships with communities, government agencies, and regional authorities. These relationships provide stability during political transitions and help navigate regulatory changes.

Environmental and Social Considerations

Large-scale copper development requires comprehensive environmental impact assessment addressing water usage, tailings storage, air quality, and ecosystem impact. Peru's environmental permitting process has become increasingly rigorous.

Community engagement represents a critical success factor. Mining projects must demonstrate tangible benefits for local communities through employment opportunities, infrastructure development, and social investment programmes.

Technical Operational Challenges

Water availability and management present significant operational considerations for copper projects in Peru's arid regions. Large-scale processing requires substantial water volumes, necessitating careful resource management and recycling systems.

- Water sourcing: Securing adequate water rights for processing operations

- Waste management: Tailings storage facility design and long-term stability

- Power supply: Grid connection versus independent renewable generation options

- Transportation logistics: Concentrate transport to port facilities for export

How Will This Deal Impact Copper Market Dynamics?

The Fortescue-Alta Copper transaction represents a significant milestone in copper market evolution, signalling broader structural changes in how the industry approaches supply security and development financing.

Supply Chain Consolidation Effects

Major mining companies acquiring development-stage copper projects accelerates mining industry consolidation trends. This concentration reduces the number of independent developers whilst increasing resources available for project advancement.

Market Share Implications

Cañariaco's potential production profile positions Fortescue to capture 1-2% of global copper mine supply once fully operational. Whilst this represents a relatively modest market share, the strategic value lies in securing long-term production capability.

Table: Projected Market Impact Timeline

| Phase | Timeline | Production Status | Market Effect |

|---|---|---|---|

| Development | 2026-2029 | Pre-production | Reduced available development assets |

| Commissioning | 2030-2031 | Ramp-up phase | Initial supply contribution |

| Commercial | 2032+ | Full production | 150,000-200,000 tonnes annual capacity |

| Expansion | 2035+ | Potential growth | Additional capacity development |

Competitive Response Dynamics

This acquisition may catalyse accelerated bidding for remaining independent copper developers as major mining companies compete to secure development pipelines. Companies with advanced feasibility studies become increasingly valuable as the pool of available assets diminishes.

The transaction establishes valuation benchmarks for similar copper development projects. Furthermore, other companies holding comparable assets may benefit from increased market valuations whilst potential acquirers face rising acquisition costs.

Investment Capital Allocation

Fortescue's entry into copper development demonstrates how mining companies are allocating capital toward critical minerals exposure. This trend may accelerate similar moves by other iron ore and coal companies seeking portfolio diversification.

The success of this transaction could encourage other strategic buyers to evaluate copper acquisition opportunities, potentially increasing competition for quality assets and driving further consolidation across the sector.

The next major ASX story will hit our subscribers first

What Investment Implications Emerge for Stakeholders?

Fortescue to buy Alta Copper creates multiple investment implications across different stakeholder categories, from immediate shareholder impacts to broader sector positioning opportunities for market participants.

Alta Copper Shareholder Analysis

Alta Copper shareholders receive immediate liquidity at a substantial premium to recent trading levels. The C$1.40 per share cash offer eliminates development funding risks and provides certain exit value for investors.

The premium paid reflects several value components:

- Immediate liquidity: Elimination of development timeline uncertainty

- Development risk transfer: Fortescue assumes operational and funding responsibilities

- Scale benefits: Access to major company operational capabilities and expertise

Fortescue Strategic Value Creation

For Fortescue shareholders, the acquisition represents strategic portfolio diversification with exposure to copper's favourable long-term demand trajectory. The relatively modest transaction size provides meaningful copper exposure without substantial balance sheet impact.

Investment Return Projections

Successful development of Cañariaco could generate substantial returns on the acquisition investment. With projected annual production of 150,000-200,000 tonnes of copper, the operation could generate hundreds of millions in annual revenue.

- Revenue potential: 175,000 tonnes × $12,000/tonne = $2.1 billion annual revenue

- Development costs: Estimated $1-2 billion capital investment for construction

- Payback period: Potentially 3-5 years from commercial production

Sector Investment Opportunities

The transaction highlights broader investment themes across the copper development sector:

- Remaining independent developers: Companies with advanced copper projects may experience valuation increases

- Acquisition targets: Junior miners with feasibility-stage projects become strategic acquisition candidates

- Major mining companies: Operators with balance sheet capacity for copper acquisitions

- Copper supply chain: Processing, transportation, and infrastructure companies

Risk Considerations for Investors

Development Execution Risks

- Construction timeline: Potential delays in project development and commissioning

- Capital cost escalation: Construction cost increases beyond feasibility study projections

- Technical challenges: Processing performance below design specifications

- Regulatory approvals: Permitting delays or additional environmental requirements

Market Risk Factors

- Copper price volatility: Revenue sensitivity to commodity price fluctuations

- Currency exposure: Canadian dollar transaction costs versus USD copper pricing

- Operating cost inflation: Rising labour and material costs affecting project economics

Future Scenario Planning: What's Next for Copper M&A?

The Fortescue-Alta Copper acquisition serves as a catalyst for broader consolidation trends across the copper development sector. Analysis of potential future scenarios reveals multiple pathways for continued market evolution.

Consolidation Acceleration Scenarios

The success of this transaction may trigger increased acquisition activity as remaining major mining companies evaluate copper development opportunities. Companies observing Fortescue's strategic positioning may accelerate their own copper acquisition programmes.

Three-Year Market Evolution Framework

Scenario 1: Rapid Consolidation (40% probability)

- Multiple major miners announce copper acquisitions within 12-18 months

- Independent developer valuations increase 50-100% from current levels

- Limited high-quality development assets remain available by 2027

- Industry structure shifts toward major company-controlled development pipeline

Scenario 2: Selective Consolidation (45% probability)

- Measured acquisition activity focused on highest-quality assets

- Premium valuations for advanced feasibility projects

- Continued role for independent developers in early-stage exploration

- Balanced market structure with both major and junior company participation

Scenario 3: Market Correction (15% probability)

- Copper price volatility reduces acquisition urgency

- Development timelines extend due to regulatory or financing challenges

- Valuation premiums moderate as market conditions change

- Delayed consolidation until supply-demand fundamentals become more acute

Strategic Buyer Categories

Traditional Mining Companies

Major miners with diversified portfolios may accelerate copper acquisition programmes:

- BHP Group: Seeking large-scale development projects to complement existing copper operations

- Rio Tinto: Evaluating copper opportunities as part of portfolio optimisation

- Vale: Potential copper expansion beyond current nickel and iron ore focus

Technology and Industrial Companies

End-user companies may pursue vertical integration strategies through mining acquisition activities:

- Electric vehicle manufacturers: Securing copper supply chains for production certainty

- Renewable energy companies: Ensuring copper availability for infrastructure projects

- Electrical equipment manufacturers: Supply chain security for critical components

Target Asset Prioritisation Matrix

Tier 1 Targets: Advanced Development Projects

- Completed feasibility studies with established resource bases

- Permitting progress in stable jurisdictions

- Infrastructure access and established operational frameworks

- Examples: Projects similar to Cañariaco with feasibility-stage advancement

Tier 2 Targets: Producing Assets with Expansion Potential

- Operating mines with exploration upside or expansion opportunities

- Established infrastructure and operational teams

- Potential for production growth through additional investment

- Strategic value for companies seeking immediate copper exposure

Tier 3 Targets: Early-Stage High-Potential Projects

- Significant resource discovery potential in proven geological provinces

- Early-stage projects requiring substantial development investment

- Higher risk-return profiles suitable for companies with long-term development timelines

Market Structure Evolution

The copper development landscape may evolve toward greater concentration among major mining companies, similar to iron ore market structure. This evolution could create both opportunities and challenges.

Positive Outcomes:

- Improved development success rates: Better capitalisation and technical expertise

- Accelerated project timelines: Enhanced financial resources and operational capabilities

- Supply security: Major company commitment to copper production growth

- Technological advancement: Investment in processing and extraction innovation

Potential Concerns:

- Reduced exploration diversity: Fewer independent exploration programmes

- Market concentration: Limited number of major copper producers

- Investment accessibility: Reduced opportunities for smaller investor participation

- Innovation constraints: Potential reduction in development approach diversity

The Fortescue-Alta Copper transaction establishes important precedents for copper market evolution whilst highlighting the strategic value of development-stage copper assets in today's supply-constrained environment. Market participants should monitor subsequent acquisition activity and competitive responses to better understand how these trends will reshape the global copper supply landscape over the coming decade.

Investment decisions should be based on comprehensive analysis of individual company fundamentals, market conditions, and risk tolerance. Copper development projects involve substantial risks including commodity price volatility, regulatory changes, and execution challenges that may affect investment outcomes.

Ready to Capitalise on the Next Major Copper Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX copper and mineral discoveries, empowering investors to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional market outcomes, then begin your 30-day free trial today to position yourself ahead of the market.