August 5, 2026

Global energy markets face unprecedented vulnerability as geopolitical tensions reshape supply chains and economic stability frameworks worldwide. The interconnected nature of modern energy infrastructure creates cascading risks that extend far beyond immediate conflict zones, affecting industrial production, trade flows, and macroeconomic balance across multiple regions. Understanding these systemic vulnerabilities requires examining how energy dependencies translate into economic pressures through complex transmission mechanisms.

Critical Energy Chokepoints and Supply Chain Dependencies

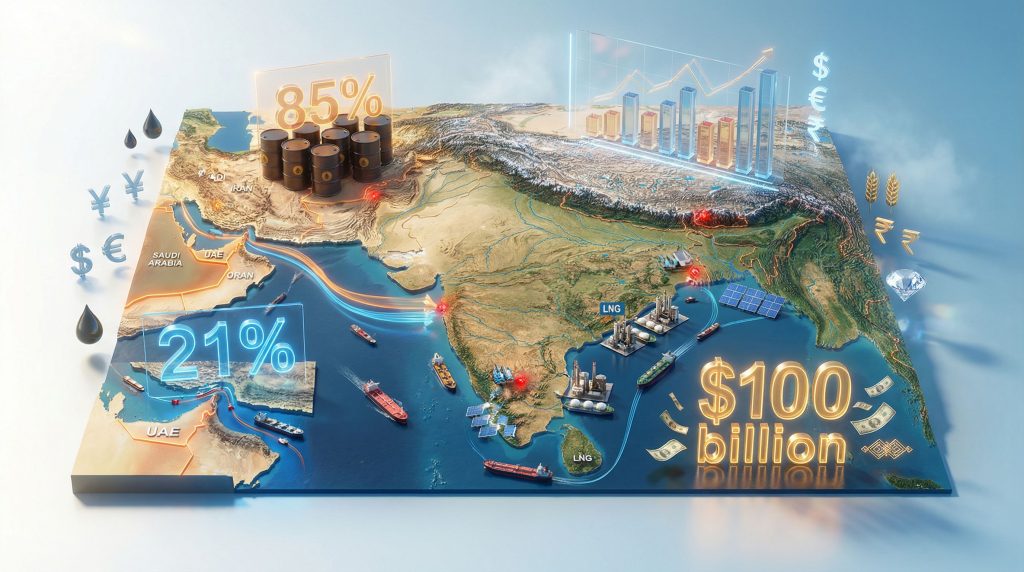

West Asian energy infrastructure controls essential global supply arteries that cannot be easily replicated or substituted. The Strait of Hormuz processes approximately 21% of global petroleum liquids, making it the world's most critical energy transit point. This geographic concentration creates systemic risk where single-point disruptions generate worldwide price volatility and supply uncertainty.

India's exposure to this vulnerability stems from structural energy import dependencies that have developed over decades of industrial growth. The country imports 85% of its crude oil requirements and 50% of its LNG needs, with substantial volumes transiting through West Asian infrastructure. Current crisis conditions demonstrate how quickly energy market disruptions transmit through India's economy, affecting everything from industrial input costs to currency stability.

Furthermore, the West Asia crisis impact on India manifests through multiple transmission channels that amplify volatility across sectors. Price transmission occurs through multiple channels simultaneously, with Brent crude prices increasing from $66-67 per barrel to $82-84 per barrel between February and March 2026, representing a 23-26% price surge. Asian spot LNG markets experienced even more dramatic volatility, with prices jumping from $10/MMBtu to $24-25/MMBtu, a 140-150% increase that directly impacts industrial operations across India.

Transportation cost increases represent another transmission channel. Alternative shipping routes through the Cape of Good Hope add 10-14 days to voyage times, increasing freight expenses and working capital requirements for importers. Marine insurance premiums have risen by 0.5-1.5% of cargo values, adding to landed costs for affected commodities.

When big ASX news breaks, our subscribers know first

Sectoral Vulnerability Analysis and Trade Disruption Patterns

Export-oriented sectors face immediate revenue pressure from demand destruction and logistical complications. India's basmati rice industry exemplifies concentrated vulnerability, with 70-72% of export volumes destined for West Asian markets. This geographic concentration means regional disruptions directly translate into demand destruction and working capital cycle pressure.

The diamond polishing sector demonstrates complex supply chain interdependencies where both input sourcing and output distribution create dual exposure points. Israel and UAE account for 68% of rough diamond imports and 18% of polished diamond exports for Indian companies. Unlike commodity markets with geographic demand distribution, specialised sectors like diamond processing rely on established hub relationships that cannot be rapidly substituted.

Key Vulnerability Metrics by Sector:

- Basmati Rice: 70-72% export concentration to West Asia

- Diamond Processing: 68% import dependency, 18% export exposure

- Fertiliser Supply: 40% of imports from West Asia (12% of total consumption)

- Ceramic Manufacturing: 15% of export volumes to West Asian markets

Fertiliser supply chains face compound disruption from both raw material sourcing and energy cost impacts. India imports approximately 30% of total fertiliser requirements, with West Asia supplying 40% of these imports. Critical raw materials including rock phosphate, phosphoric acid, and muriate of potash show significant regional concentration, creating agricultural input cost pressures that transmit through food production systems.

Working capital cycle disruptions affect mid-sized traders and processors disproportionately. Extended payment cycles from 30-60 days to 40-74 days create refinancing pressure for companies operating on 90-180 day working capital cycles. This timing mismatch forces liquidity adjustments even for well-capitalised firms.

Energy-Intensive Manufacturing and Cost Structure Impacts

Industrial sectors with high energy content in their cost structures face immediate margin pressure from volatile input prices. Synthetic textile manufacturing demonstrates severe exposure, with 70-80% of production costs linked to crude oil derivatives. Limited pass-through capability means manufacturers absorb input cost increases until market conditions allow pricing adjustments.

Cost Structure Vulnerability Assessment:

| Industry Sector | Energy-Linked Cost Share | Margin Impact Risk | Price Pass-Through Ability |

|---|---|---|---|

| Synthetic Textiles | 70-80% | High | Limited |

| Flexible Packaging | 70-80% | High | Moderate |

| Tyre Manufacturing | 50% | Medium-High | Delayed |

| Ceramics | Variable | Medium | Market-Dependent |

| Paints & Chemicals | 30% | Medium | Moderate |

LNG-dependent manufacturing faces dual pressure from supply constraints and price volatility. City gas distribution networks, with 40% LNG import dependency, must balance industrial supply commitments against residential demand obligations. Consequently, ceramics manufacturing, heavily reliant on LNG for high-temperature processes, faces potential production curtailment if supplies tighten further.

The fertiliser manufacturing sector experiences compound pressure affecting both domestic production and import requirements. Urea production facilities depend on LNG availability and pricing for operational viability, while import requirements increase when domestic production becomes economically unviable. Government subsidy requirements expand with higher input costs, creating fiscal pressure alongside industrial disruption.

For instance, alternative fuel options provide limited hedging benefits because substitute energy sources also correlate with crude oil prices. This price linkage means manufacturers cannot easily switch to cost-effective alternatives during energy market disruptions.

Macroeconomic Transmission and Currency Stability Pressures

Current account balance deterioration represents the primary macroeconomic transmission channel from energy market disruptions. Each $10 per barrel increase in crude oil prices adds approximately $15-17 billion to India's annual import bill at current consumption levels. The recent price surge translates into substantial additional foreign exchange requirements that pressure currency stability.

Moreover, OPEC production impacts and subsequent oil price movements create ripple effects throughout India's economic structure. Inflation transmission occurs through multiple pathways simultaneously, with direct energy costs affecting transportation, electricity generation, and industrial heating expenses. Indirect cost-push effects transmit through manufacturing inputs, logistics networks, and packaging materials.

Service sector impacts include airlines facing 35-40% fuel cost exposure and logistics companies managing freight rate increases. Currency depreciation pressures from higher import costs require careful policy management to avoid destabilising capital flows while maintaining export competitiveness. The rupee faces downward pressure from widening trade deficits, but excessive depreciation could trigger capital flight and further economic instability.

Projected Economic Impact Scenarios:

- Moderate Disruption: 0.3-0.5 percentage point GDP growth reduction

- Severe Disruption: 0.8-1.2 percentage point impact on annual growth

- Current Account Deficit: Additional 0.4-0.7% of GDP pressure

However, monetary policy faces complex trade-offs between supporting growth and managing imported inflation pressures. Current retail inflation at 2.75% provides some policy flexibility, but sustained energy price increases could force restrictive measures that conflict with growth objectives.

Energy Market Correlations and Regional Impacts

The West Asia crisis impact on India extends beyond crude oil dependencies to encompass broader energy market correlations. Natural gas forecasts suggest continued volatility as regional supply disruptions affect global pricing mechanisms. This interconnectedness means Indian industries face compound pressures from multiple energy sources simultaneously.

Furthermore, Saudi exploration licenses and related development projects influence long-term supply security considerations for Indian energy planners. These strategic decisions by major producers create ripple effects across Asian energy markets, affecting pricing and availability for import-dependent economies.

Additionally, the broader geopolitical context, including US–China trade impacts, shapes energy market dynamics and alternative supply chain development. These interconnected factors create complex vulnerability patterns that require comprehensive analysis for effective risk management.

Diaspora Economic Links and Remittance Flow Risks

India's economic relationship with West Asia extends beyond trade flows to include substantial human capital and remittance dependencies. Approximately 1 crore Indian nationals work across Gulf countries, generating over $100 billion in annual remittances that support household consumption and current account financing.

Conflict-related job losses or evacuation requirements could significantly reduce these flows, creating both domestic economic pressure and balance of payments challenges. Return migration would create labour market adjustment pressures while eliminating foreign exchange earnings that currently support India's external sector stability.

Regional employment patterns show concentration in construction, services, and skilled technical roles that cannot be easily replicated in other markets. Unlike trade relationships that can potentially diversify across suppliers, employment-based economic links require time and institutional development to establish in alternative locations.

Household consumption effects from reduced remittance flows would disproportionately affect rural and semi-urban communities that depend on Gulf employment for income support. This transmission creates domestic economic multiplier effects that extend crisis impacts beyond direct trade exposure.

The next major ASX story will hit our subscribers first

Strategic Economic Resilience and Policy Response Frameworks

India's diversified economic structure provides substantial resilience against external shocks, but energy import dependencies create structural vulnerabilities requiring proactive policy responses. Strategic petroleum reserves offer some short-term price volatility management, but sustained disruptions require broader economic adjustment mechanisms.

Energy source diversification accelerates under crisis conditions, potentially increasing renewable energy investments and alternative supplier relationships. This transition requires significant capital allocation and policy support to develop infrastructure and commercial relationships outside traditional supply chains.

Policy Response Mechanisms:

- Strategic reserve utilisation for price smoothing

- Fertiliser subsidy adjustments to protect agricultural inputs

- Export promotion for affected industries seeking alternative markets

- Currency intervention to manage depreciation pressures

- Monetary policy calibration balancing growth and inflation

Trade route resilience building becomes essential for long-term economic security. Alternative corridor development, port capacity expansion for handling rerouted cargo, and digital trade facilitation to reduce transaction costs represent infrastructure investments that strengthen supply chain flexibility.

Economic diplomacy initiatives focus on strengthening relationships with alternative suppliers and markets, potentially reshaping long-term trade patterns and investment flows. These adjustments require time to develop but provide essential diversification benefits for future crisis resilience.

What Are the Long-term Implications for Indian Economic Policy?

The West Asia crisis impact on India demonstrates how regional geopolitical disruptions transmit through interconnected global systems to affect distant economies. While India's strong macroeconomic fundamentals and diverse economic structure provide meaningful resilience, energy import dependencies and diaspora exposure create vulnerabilities requiring comprehensive policy responses.

The crisis catalyses acceleration of energy transition and supply chain diversification strategies essential for long-term economic stability and growth sustainability. Policymakers must balance immediate crisis management with structural reforms that reduce future vulnerability to regional disruptions.

Furthermore, the experience highlights the importance of developing comprehensive assessment frameworks for evaluating geopolitical risks and their economic transmission mechanisms across sectors.

How Can Indian Businesses Build Resilience?

Indian businesses must develop adaptive capacity through diversified supply chains, flexible financing arrangements, and enhanced risk management systems. The current crisis provides valuable lessons for building operational resilience against future external shocks.

Companies should prioritise supplier diversification, alternative energy sourcing, and financial hedging strategies to mitigate future vulnerability. Strategic partnerships with alternative suppliers and markets become essential for maintaining competitive positioning during crisis periods.

"The economic fallout from West Asian conflicts requires a calibrated response that balances immediate crisis management with long-term structural resilience building." – Economic Policy Analysis

Investment Disclaimer: This analysis contains forward-looking assessments based on current market conditions and geopolitical developments. Energy market volatility, geopolitical outcomes, and economic policy responses remain subject to significant uncertainty. Investors should conduct independent research and consider risk tolerance before making investment decisions related to energy-dependent sectors or currency-sensitive investments.

Looking for Energy-Dependent Investment Opportunities During Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, helping subscribers identify actionable opportunities in energy and commodity markets ahead of broader market recognition. Explore historic examples of major discoveries and their substantial returns, then begin your 14-day free trial today to position yourself strategically during current market volatility.