July 16, 2026

The Inflation-Rate Trap: Why War in the Middle East Is Pushing Gold Lower

Most investors instinctively reach for gold when geopolitical risk intensifies. Decades of market history have reinforced this reflex, from Cold War anxiety to post-9/11 uncertainty and the early months of the Russia-Ukraine conflict. Yet something unusual is unfolding in mid-2026: an active military conflict between two major powers is actively working against gold. Understanding this paradox requires moving beyond surface-level safe-haven logic and examining the precise transmission mechanism through which war, in the right circumstances, becomes a bearish catalyst for precious metals.

The critical variable is energy. When conflict disrupts oil supply, it does not simply raise commodity prices in isolation. It triggers a chain reaction that runs directly through inflation expectations, central bank policy, currency valuations, and the opportunity cost of holding non-yielding assets. Gold falls as mideast escalation dims hopes of easing inflation, and that single sentence captures a far more complex and consequential set of dynamics than it first appears. Furthermore, the geopolitical drivers of gold pricing are rarely as straightforward as conventional wisdom suggests.

When big ASX news breaks, our subscribers know first

Understanding the Energy-Inflation-Rates Feedback Loop

How Oil Supply Disruption Becomes a Monetary Policy Problem

The Strait of Hormuz is the most consequential maritime chokepoint on the planet, responsible for transporting roughly 20% of the world's total oil supply on any given day. When military activity threatens the security of this corridor, oil markets reprice risk almost instantly, regardless of whether physical supply has yet been interrupted.

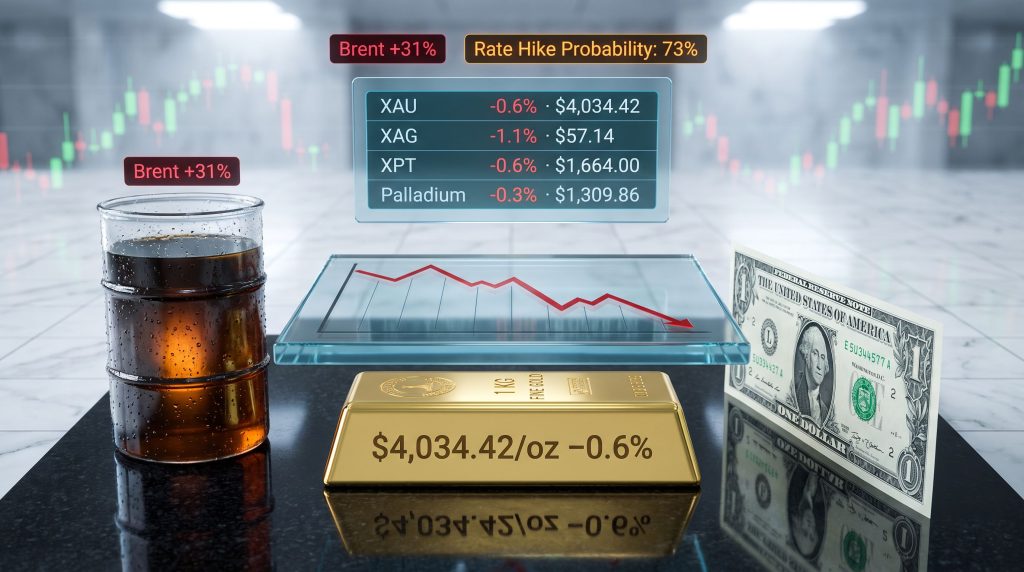

In the current escalation, Brent crude has surged approximately 31% across four consecutive sessions of gains, driven by a combination of U.S. military strikes on Iranian coastal defence infrastructure and a re-imposed naval blockade of Iranian ports. Iran's retaliatory strikes on U.S. military installations in neighbouring countries have further reduced the probability of a swift diplomatic resolution, locking in elevated supply-risk premiums.

The downstream consequences of this oil price surge are what matter most for gold traders. The mechanism operates as follows:

| Transmission Stage | Mechanism | Market Outcome |

|---|---|---|

| Military escalation in Middle East | Disrupts regional oil supply routes | Brent crude surges ~31% |

| Oil price spike | Raises energy costs across global supply chains | Headline inflation re-accelerates |

| Inflation re-acceleration | Forces central banks to maintain hawkish stance | Rate cut expectations collapse |

| Rate cut expectations collapse | Raises opportunity cost of non-yielding assets | Gold prices decline |

| Dollar strengthens on rate outlook | Makes gold more expensive in foreign currencies | Additional downward price pressure |

Each stage amplifies the next, creating a compounding bearish force that the traditional geopolitical risk premium cannot offset.

Gold's Current Price and Recent Trajectory

Where Spot and Futures Markets Are Trading

As of July 16, 2026, spot gold has declined 0.6% to $4,034.42 per ounce, while U.S. gold futures for August delivery have retreated 0.3% to $4,039.90. These figures reflect not an isolated daily move, but the continuation of a broader pattern of price compression that has developed alongside the deteriorating geopolitical situation.

Looking back across recent months provides critical context:

- March 2026: Gold plunged more than 8% in a single session, falling to approximately $4,097.99 as rate-hike fears first surged in response to inflationary pressures.

- June 2026: Spot gold declined 3.5% to $4,111.95, marking its lowest level since late March as U.S.-Iran hostilities initially intensified.

- July 16, 2026: A further 0.6% decline to $4,034.42 as the collapse of the interim peace framework removes the remaining cushion of disinflation optimism from market pricing.

Precious Metals Broader Market Performance

The weakness is not confined to gold. The entire precious metals complex is under pressure from the same macro forces:

| Metal | Price Movement | Current Price |

|---|---|---|

| Spot Gold (XAU) | -0.6% | $4,034.42/oz |

| Gold Futures (August) | -0.3% | $4,039.90/oz |

| Spot Silver (XAG) | -1.1% | $57.14/oz |

| Platinum (XPT) | -0.6% | $1,664.00/oz |

| Palladium | -0.3% | $1,309.86/oz |

Silver's sharper decline of 1.1% reflects its dual role as both a monetary and industrial metal, leaving it exposed to both the rate-driven selling pressure affecting gold and any growth concerns that accompany sustained energy price inflation. In addition, the trade war impact on gold and broader precious metals has compounded these existing macro pressures throughout 2025 and into 2026.

The Opportunity Cost Problem: Why Rates Are Gold's Greatest Adversary

Non-Yielding Assets in a High-Rate Environment

Gold's structural weakness in the current environment stems from a fundamental characteristic: it produces no income. No interest payments, no dividends, no coupon. In low-rate environments, this matters very little because the competing yield from bonds or cash is minimal. In high-rate environments, the calculus reverses entirely.

When interest rates are elevated or rising, investors holding gold are forgoing meaningful returns available elsewhere. The opportunity cost becomes tangible and quantifiable, particularly for institutional allocators managing large portfolios where even a small yield differential represents significant absolute returns at scale.

- When rates are low or falling: holding gold is nearly costless, demand tends to rise.

- When rates are high or rising: bonds, money market instruments, and cash equivalents offer competitive returns, reducing gold's relative appeal.

- When rate cut expectations are priced out: the forward-looking investment case for gold weakens significantly, as the anticipated catalyst for gold's next leg higher is removed.

However, understanding gold-bond dynamics across economic cycles reveals that this relationship is not always linear, and context matters enormously when assessing gold's relative positioning.

The gold market in mid-2026 is not simply reacting to current interest rate levels. It is reacting to the collapse of the rate-cut narrative itself. Every oil price increase that re-ignites inflation expectations eliminates another basis point from the anticipated easing cycle, directly eroding the investment thesis that drove gold higher in the first place.

Federal Reserve Policy Signals and Market Pricing

The Federal Reserve's positioning is central to understanding gold's vulnerability. CME FedWatch Tool data currently indicates approximately a 73% probability of a December 2026 rate hike, a figure that has climbed sharply as energy-driven inflation fears have resurfaced. Consequently, gold as an inflation hedge has become a more nuanced and contested proposition under these conditions.

Key signals from Fed officials reinforce this hawkish market interpretation:

- Fed Governor Lisa Cook has stated her readiness to take action if inflation does not begin decelerating meaningfully.

- Fed Chairman Kevin Warsh has reaffirmed the central bank's determination to bring inflation under control, without providing a specific timeline or signalling imminent policy relief.

- Markets are closely monitoring upcoming remarks from Dallas Fed President Lorie Logan and Fed Vice Chair Philip Jefferson for additional signals about the pace and duration of restrictive monetary policy.

This constellation of hawkish communication, combined with the energy-driven inflation resurgence, makes a near-term Fed pivot toward rate cuts increasingly difficult to justify from a data-driven policy perspective.

Dollar Strength as a Compounding Bearish Force

The Currency Mechanism Most Gold Investors Underestimate

Beyond the direct opportunity cost argument, dollar strength adds a second layer of downward pressure on gold that is frequently underappreciated in mainstream commentary. Because gold is globally priced in U.S. dollars, any appreciation in the dollar's value makes gold more expensive in local currency terms for international buyers.

This is not a trivial concern. The world's largest gold-consuming markets, including China, India, and much of Southeast Asia, are acutely sensitive to local currency purchasing power when making gold investment or jewellery purchasing decisions. Central banks influencing gold demand in these regions further complicates the picture, as reserve managers weigh currency considerations alongside their strategic allocation targets.

The compounding dynamic in the current environment looks like this:

- Military conflict escalates in the Middle East.

- Oil prices surge, raising U.S. inflation expectations.

- Elevated inflation expectations push markets to price in more Fed rate hikes.

- Rate hike expectations attract capital into dollar-denominated assets.

- The dollar strengthens against major currencies.

- Gold becomes more expensive for non-dollar buyers.

- International demand softens, adding further downward price pressure.

This sequence means that the same geopolitical event which might logically be expected to boost safe-haven demand is simultaneously strengthening the currency that makes gold more expensive for the buyers who would otherwise provide that demand.

June's Inflation Data: A Snapshot of a World That No Longer Exists

Why the Disinflation Window Has Already Closed

Both the U.S. Consumer Price Index and Producer Price Index for June 2026 showed measurable moderation, providing temporary relief to markets anticipating the end of the tightening cycle. The primary driver of this moderation was a pullback in energy product costs, which created the statistical appearance of progress toward the Fed's inflation objectives.

However, this data carries a critical interpretive caveat: it was compiled before the breakdown of the interim peace framework between the U.S. and Iran. The energy price relief that produced June's benign inflation readings has since been fully reversed and then some, as Brent crude's 31% surge demonstrates. Reuters reports that inflation concerns were already lingering even before the latest escalation, suggesting the disinflation narrative was fragile well ahead of the current crisis.

Investors treating June's CPI and PPI figures as a reliable forward indicator for monetary policy should account for the structural shift in the energy price outlook caused by renewed hostilities. The disinflation trend captured in that data reflects conditions that no longer prevail in the physical commodity markets feeding into Q3 2026 inflation readings.

The June data is not irrelevant, but its signalling value for Fed policy has been materially degraded by the subsequent geopolitical deterioration. Markets that were positioning for rate cuts based on that data have been forced to rapidly unwind those positions, contributing to the selling pressure on gold.

The next major ASX story will hit our subscribers first

Reassessing Gold's Safe-Haven Status in Portfolio Construction

When Defensive Properties Are Overridden by Macro Forces

Gold's reputation as a safe-haven asset is neither myth nor absolute truth. It is conditional. The metal tends to perform its defensive role most effectively in specific macro environments: currency crises, financial system stress, deflationary shocks, and periods of broad risk-asset selloffs where capital seeks stores of value outside the financial system.

What the 2026 U.S.-Iran escalation illustrates is a different scenario structure, one where the inflationary consequences of conflict overwhelm the risk-premium demand that would otherwise support gold prices:

| Geopolitical Risk Type | Gold Market Response | Key Differentiator |

|---|---|---|

| Typical regional conflict (contained) | Safe-haven buying, gold rises | Inflation impact limited |

| Financial system stress event | Strong gold bid, correlation with risk-off | No rate-hike pressure |

| 2026 U.S.-Iran escalation | Oil shock drives rate fears, gold falls | Direct inflation transmission via energy |

| Sanctions-driven supply disruption | Mixed response | Scale and duration-dependent |

The current environment combines five simultaneous bearish forces:

- Inflation re-acceleration triggered by the energy price shock.

- Central bank hawkishness in response to persistent and rising price pressures.

- Dollar strengthening driven by widening rate divergence expectations.

- Opportunity cost escalation as yielding assets become comparatively more attractive.

- Destruction of the disinflation narrative that had been gold's primary bullish catalyst in early 2026.

Conditions Required for Gold to Resume an Uptrend

For gold to regain meaningful upward momentum from current levels, a confluence of reversals would be necessary. According to Yahoo Finance, gold has already slid significantly amid ongoing Middle East tensions, underscoring just how entrenched these headwinds have become.

- A credible ceasefire or diplomatic resolution that reduces the oil supply risk premium.

- U.S. inflation data demonstrating sustained deceleration despite elevated energy costs.

- Federal Reserve signals of a genuine pivot toward rate cuts or a substantive pause in tightening.

- Meaningful dollar weakening driven by shifting global capital flows or risk sentiment.

- Renewed institutional safe-haven demand strong enough to override the rate-driven selling pressure currently dominating price action.

None of these conditions appears imminent given the current geopolitical and monetary policy landscape.

FAQ: Gold, Inflation, and Middle East Conflict Explained

Why is gold falling when there is active conflict in the Middle East?

The conflict is generating an oil price shock that is re-accelerating inflation expectations. Because gold is a non-yielding asset, rising inflation that compels central banks to maintain or raise interest rates increases the opportunity cost of holding gold relative to bonds or cash instruments, making it structurally less attractive in the current environment.

What is the current gold price as of July 2026?

Spot gold is trading at approximately $4,034.42 per ounce, down 0.6% on July 16, 2026. U.S. gold futures for August delivery are priced at $4,039.90, down 0.3%.

How does an oil price surge affect gold specifically?

Higher oil prices raise headline inflation. Elevated inflation forces central banks to maintain restrictive monetary policy. Higher rates increase the opportunity cost of non-yielding assets like gold, applying sustained downward price pressure whilst simultaneously strengthening the dollar and reducing international gold demand.

What is the Federal Reserve's current policy stance?

Markets are pricing approximately a 73% probability of a December 2026 rate hike according to CME FedWatch Tool data. Multiple Fed officials have signalled readiness to tighten further if inflation does not demonstrate a credible and sustained downward trajectory.

Is gold still an effective inflation hedge in this environment?

Gold's inflation-hedging properties are most reliable when inflation is driven by monetary expansion or currency debasement. When inflation is triggered by supply shocks that simultaneously force central banks to raise rates, gold's hedging effectiveness is substantially diminished, as higher rates increase the cost of holding a zero-yield asset. This is precisely why gold falls as mideast escalation dims hopes of easing inflation, rather than rising as many investors might expect.

Key Forces Suppressing Gold in Mid-2026: A Summary Framework

| Bearish Force | Current Severity | Reversibility |

|---|---|---|

| Oil-driven inflation re-acceleration | High | Moderate, dependent on conflict resolution |

| Federal Reserve rate hike expectations | High | Low, requires sustained disinflation data |

| U.S. dollar strength | Moderate | Moderate, linked to rate divergence outlook |

| Collapse of disinflation narrative | High | Low, June data now predates key escalation |

| International demand reduction via FX | Moderate | Moderate, tied to dollar trajectory |

The 2026 Middle East escalation has fundamentally reshaped the near-term macro environment for precious metals. Rather than functioning as a conventional geopolitical safe haven, gold is being repriced as a direct casualty of the inflation-rate feedback loop that military conflict has activated through the global energy market. Until either the geopolitical situation stabilises or central banks provide credible signals of policy relief, the structural headwinds facing gold remain substantial.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. All price data and market probabilities referenced reflect conditions as of July 16, 2026. Past performance of any asset class is not indicative of future results. Readers should consult a qualified financial adviser before making investment decisions.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

While macroeconomic forces reshape the gold landscape, Discovery Alert's proprietary Discovery IQ model cuts through the complexity by delivering real-time alerts on significant ASX mineral discoveries — transforming dense geological announcements across 30+ commodities into clear, actionable insights for traders and investors alike. Explore historic discoveries and their extraordinary returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.