July 10, 2026

When Supermajors Exit, Independents Advance: Understanding the Gulf of America Deepwater Ownership Shift

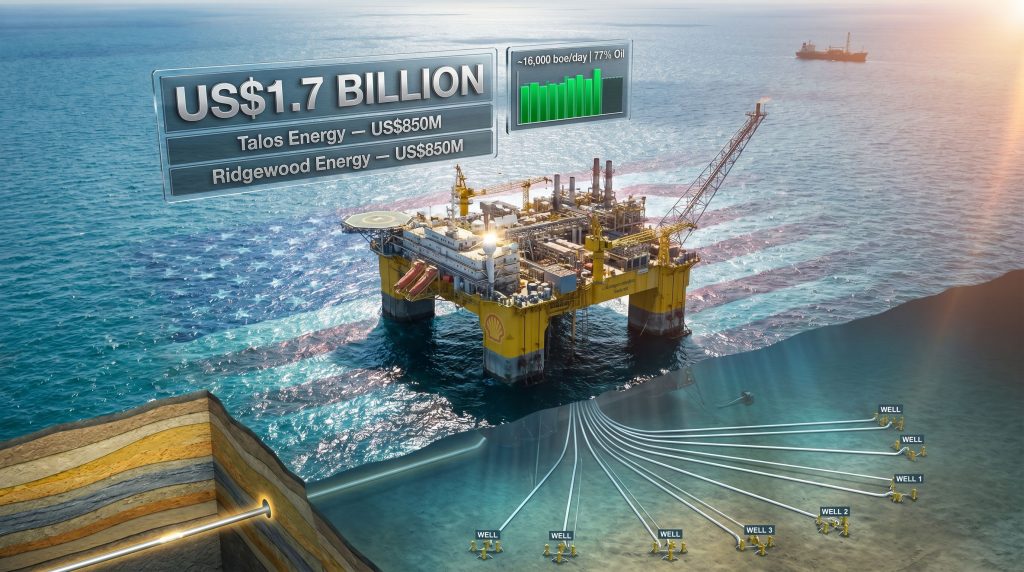

The deepwater Gulf of America has always operated on a simple but brutal economic logic: those who own the infrastructure control the future of the basin. For two decades, supermajors like Shell and BP constructed, funded, and operated the floating production hubs that turned ultra-deepwater geology into commercial output. But in 2026, that ownership structure is visibly fracturing. The Shell Na Kika and Coulomb sale to Talos Energy and Ridgewood Energy, valued at a combined US$1.7 billion, is not simply a transaction. It is a window into how the economics of deepwater asset ownership are being fundamentally repriced and redistributed across a new generation of independent operators.

When big ASX news breaks, our subscribers know first

Why Supermajors Are Exiting Mature Deepwater Positions

The conventional narrative around divestiture focuses on portfolio simplification, but the underlying mechanics are more precise. Supermajors measure capital performance against a blended threshold that non-operated, plateau-stage assets increasingly fail to meet. When a producing asset no longer delivers incremental returns above internal hurdle rates, the equity position becomes an inefficient use of balance sheet capacity, regardless of whether it still generates positive cash flow.

Shell's internal production modelling reportedly projects that both Na Kika and Coulomb will cease making a material contribution to group output by 2030. In 2025, the combined assets contributed approximately 37,000 boe/day to Shell's net production, a figure that was already declining. For a company of Shell's scale, that trajectory represents diminishing relevance within a global portfolio rather than a meaningful revenue stream.

What makes this divestiture structurally notable is the parallel timing. Within the same month in 2026, BP separately announced it was marketing minority stakes in its own Gulf flagship developments, Kaskida and Tiber, each carrying individual peak production targets of 80,000 b/d. Two of the world's largest energy companies executing simultaneous Gulf of America portfolio rationalisations is not coincidence. It reflects a shared capital discipline framework that has concluded the same thing: minority equity in mature, non-operated Gulf assets is no longer worth carrying when higher-return operated developments compete for the same dollars.

Furthermore, oil price movements in recent years have reinforced the urgency behind these decisions, as volatile commodity cycles compress the internal return profiles of plateau-stage assets in ways that accelerate divestiture timelines.

The Non-Operated Interest Problem in Modern Upstream Strategy

A critical but often underappreciated distinction in deepwater M&A is the difference between operated and non-operated working interests. Non-operated positions generate production cash flow, but they offer no control over:

- Development timing and well sequencing decisions

- Capital expenditure budgets and cost management

- Tie-back prioritisation for nearby subsea tiebacks

- Operational efficiency improvements that affect unit lifting costs

Shell's 50% non-operated stake in Na Kika exposed it to BP-controlled production decisions without any authority over how the asset was managed or how capital was deployed. Divesting that position while retaining commercial exposure through offtake agreements and royalty instruments allows Shell to preserve commodity upside without shouldering the capital obligations of equity ownership. This is a fundamentally different risk posture, and it is increasingly becoming the template for how supermajors manage mature basin exposure.

The Na Kika Platform and Coulomb Field: Asset-Level Analysis

Na Kika: More Than Two Decades as a Deepwater Production Hub

The Na Kika semisubmersible platform sits in the Mississippi Canyon area of the Gulf of America and achieved first oil in November 2003, making it one of the earliest large-scale deepwater floating production systems ever deployed in the basin. Originally conceived as a technically ambitious 50/50 joint venture between BP and Shell, the platform represented a frontier engineering achievement at the time of its development.

Its operational architecture follows what is often described as an octopus-like configuration: a central semisubmersible floating production host gathering output from multiple subsea tiebacks radiating outward across the seafloor. The associated fields currently feeding the platform include Kepler, Ariel, Fourier, and Herschel, each connected to the host via subsea flowlines. BP holds operatorship with a 50% working interest, and Shell's departing 50% non-operated stake is the subject of this transaction.

One lesser-known aspect of mature deepwater hub economics is the tie-back optionality embedded in platform ownership. A semisubmersible host like Na Kika carries significant residual processing capacity value that is not captured in current production metrics alone. Any new subsea discovery within economic tieback range of the platform can be developed at a fraction of the standalone development cost, making platform ownership strategically more valuable than current throughput numbers suggest. This is precisely why Shell negotiated overriding royalty interests on future Na Kika tiebacks as part of the divestiture, ensuring it participates in that exploration upside without funding the associated capital expenditure.

Coulomb: Operatorship as the Key Value Differentiator

The Coulomb subsea tieback is a structurally distinct asset proposition from Na Kika. Shell held 100% ownership of Coulomb prior to this transaction, with production commencing in 2005. Talos Energy is acquiring a 50% working interest plus full operatorship of Coulomb, which represents a meaningfully different commercial position than the non-operated Na Kika interest.

Operatorship of a deepwater tieback asset gives the holder direct authority over:

- Well intervention and workover scheduling

- Future development well planning

- Potential new subsea tieback evaluations

- Cost structure and contractor negotiations

For an independent E&P company like Talos, which has built its Gulf of America identity around infrastructure-led deepwater consolidation, acquiring operatorship of Coulomb is not incidental. It is a strategic beachhead that could anchor future bolt-on tie-back development in the surrounding acreage.

Breaking Down the US$1.7 Billion Transaction Structure

Deal Architecture and Buyer Allocation

| Transaction Component | Talos Energy | Ridgewood Energy |

|---|---|---|

| Na Kika Interest Acquired | 25% non-operated working interest | 25% non-operated working interest |

| Coulomb Field Interest | 50% working interest + operatorship | Not included |

| Gross Purchase Price | US$850 million | US$850 million |

| Total Combined Deal Value | US$1.7 billion | — |

Why the Effective Date Changes the Real Acquisition Cost

One of the most consequential and least understood mechanisms in deepwater asset transactions is the effective date structure. The Shell Na Kika and Coulomb sale carries an effective date of July 1, 2025, meaning all cash flows generated by the assets from that date forward are credited against the purchase price at closing. Expected closing is targeted by the end of 2026, pending regulatory approvals.

The practical result is material: based on interim cash flows accrued since the effective date, Talos anticipates its final net cash outlay will range between US$450 million and US$500 million, representing a reduction of approximately US$350 million to US$400 million from the headline US$850 million figure. For investors modelling acquisition economics, the effective date mechanism produces a significantly more attractive entry valuation than the headline number implies.

Shell's Retained Commercial Instruments

The divestiture architecture Shell constructed around this sale reveals a sophisticated approach to exiting equity while preserving basin participation. According to Shell's official announcement of the transaction, the retained instruments include:

- Uncapped upside-sharing payments through the end of 2027, activated when realised oil prices exceed US$60 per barrel

- Overriding royalty interests (ORRI) on production from any future Na Kika subsea tiebacks

- Offtake rights from both Na Kika and Coulomb production, executed through Shell Trading US Company

This combination converts equity risk into structured financial exposure. Shell absorbs no future capital expenditure obligations on these assets, but retains meaningful revenue participation if commodity prices cooperate and if future tie-back developments add production. It is a risk-adjusted financial architecture that traditional asset sale metrics often fail to fully capture.

What This Transaction Adds to Talos Energy's Production Profile

Production and Reserves Addition

| Metric | Figure (Net to Talos) |

|---|---|

| Q1 2026 Production | ~16,000 boe/day |

| Oil as % of Production | ~77% |

| Proved Reserves Added | ~23 million boe |

| Probable Reserves Added | ~10 million boe |

| Total Potential Reserves Addition | ~33 million boe |

Adding approximately 16,000 boe/day of producing, infrastructure-connected deepwater output represents a step-change in scale for an independent operator. The 77% oil weighting is particularly significant at current commodity price levels, where oil price realisations substantially exceed the economics of associated gas and NGL volumes. In addition, the broader influence of trade war oil prices on global demand expectations adds further context to why this oil-weighted production profile is strategically attractive at this point in the cycle.

Financing the Acquisition

Talos will fund the transaction through a combination of existing cash and incremental debt. The company secured US$150 million in additional lender commitments from its existing banking syndicate, expanding its borrowing base from US$700 million to US$850 million upon closing. The willingness of lenders to expand the borrowing base specifically in support of this acquisition reflects institutional confidence in the near-term cash generation capacity of the Na Kika and Coulomb asset base at prevailing oil prices.

BP's Preferential Purchase Right: The Binary Risk Every Investor Must Model

How the Right of First Refusal Works

BP, as the existing 50% owner and operator of Na Kika, holds a 30-day preferential purchase right over Shell's departing interest. If exercised, BP would acquire Shell's full 50% stake at the terms already negotiated with Talos and Ridgewood, effectively consolidating 100% ownership of the Na Kika platform. This would remove both Talos and Ridgewood from the Na Kika equation entirely.

Two Possible Transaction Outcomes

Scenario A: BP Does Not Exercise the Preferential Right

- Talos acquires 25% non-operated interest in Na Kika (Kepler, Ariel, Fourier, Herschel fields) plus 50% operatorship of Coulomb

- Ridgewood acquires the remaining 25% non-operated Na Kika interest

- Full US$1.7 billion transaction proceeds as structured

- Talos adds approximately 16,000 boe/day to its production base

Scenario B: BP Exercises the Preferential Right

- BP consolidates to 100% ownership of Na Kika, becoming sole platform owner and operator

- Talos retains only the 50% working interest and operatorship of the Coulomb field

- Ridgewood's participation in any Na Kika interest is blocked entirely

- Talos's production and reserves additions are materially reduced from guided figures

The BP preferential right introduces genuine binary outcome risk into this transaction. All production guidance and reserves addition figures that Talos has disclosed are contingent on BP choosing not to exercise a right that is both commercially and strategically motivated by BP's own capital priorities and platform consolidation interests.

From an investor psychology perspective, this contingency creates a valuation fog that the market must price. If BP consolidates Na Kika to 100%, it removes a competing operator from a platform it already controls while simultaneously eliminating Talos's most significant production addition from the deal. BP's decision will ultimately reflect its own view on whether the capital deployment into a maturing asset improves its portfolio returns more than alternative uses of US$850 million.

The next major ASX story will hit our subscribers first

The Supermajor Playbook: Divesting Equity, Retaining Exposure

Shell and BP's Parallel Gulf Portfolio Moves

| Company | Asset Action | Retained Exposure |

|---|---|---|

| Shell | Divesting 50% non-operated Na Kika + 100% Coulomb | Offtake rights, ORRI on future tiebacks, upside-sharing through 2027 |

| BP | Marketing minority stakes in Kaskida and Tiber (80,000 b/d peak each) | Retaining operatorship and majority equity in flagship developments |

Shell's Upstream leadership has stated publicly that the Gulf of America remains one of its highest-value basins and that the company is actively shaping its upstream portfolio to maintain resilience and competitiveness. That framing is important context: this divestiture is not a basin exit. It is a capital reallocation within the basin, from mature non-operated positions toward future operated developments where Shell controls cost structures and development timing.

The simultaneity of Shell's Na Kika exit and BP's Kaskida and Tiber stake marketing within the same month in 2026 is analytically significant. When two of the world's largest hydrocarbon producers execute structurally similar transactions in the same geography within weeks of each other, it reflects a shared read on asset valuation, buyer appetite, and the relative attractiveness of alternative capital deployment options. The Gulf of America is not being abandoned; it is being repriced and reowned. Crude oil trends in 2025 and early 2026 have materially shaped the timing and terms of these decisions, influencing both seller motivations and buyer return expectations.

Why Independent E&P Companies Win in This Environment

The infrastructure consolidation thesis underpinning Talos Energy's acquisition logic is worth examining carefully. Deepwater production infrastructure, including floating platforms, subsea flowline networks, and processing systems, represents the primary barrier to entry in mature Gulf basins. Replicating the Na Kika platform and its associated subsea infrastructure from scratch in today's contracting environment would cost multiples of the US$850 million acquisition price.

For Talos, acquiring a working interest in Na Kika means gaining access to existing processing capacity, established subsea connections, and proximity to future tie-back opportunities at a fraction of greenfield development cost. Coulomb operatorship layers on top of that by giving Talos active control over one component of the infrastructure network, with direct implications for future development well timing, intervention costs, and potential new tie-back evaluations in surrounding acreage.

Moreover, the broader geopolitical mining landscape and energy sector dynamics have reinforced investor appetite for tangible, infrastructure-backed producing assets over speculative development exposure. At the effective acquisition cost of US$450 to US$500 million after interim cash flows, the production multiple implied by approximately 16,000 boe/day at 77% oil weighting makes this one of the more competitively priced deepwater entry points available to independent operators in the current market cycle. Whether that value is fully realised depends on BP's preferential right decision and the trajectory of oil prices relative to the US$60 per barrel threshold governing Shell's retained upside-sharing arrangement.

Key Takeaways for Investors and Industry Observers

The Shell Na Kika and Coulomb sale to Talos Energy and Ridgewood Energy crystallises several converging dynamics in the Gulf of America deepwater sector. Notably, commodity prices and miners across the broader energy and resources landscape are experiencing similar ownership transitions driven by the same capital efficiency pressures. According to reporting on the deal's full scope, the transaction represents one of the most significant Gulf deepwater ownership reshuffles in recent years. The key dynamics to monitor include:

- Supermajors are systematically converting non-operated equity positions into structured commercial instruments, exiting balance sheet exposure whilst preserving basin revenue participation

- Independent operators with proven deepwater infrastructure management capability are the primary beneficiaries of this ownership transition

- The effective date mechanism in deepwater M&A transactions consistently produces real acquisition costs meaningfully below headline figures, a dynamic that headline valuation analysis routinely misses

- BP's 30-day preferential purchase right over Na Kika creates binary outcome risk that is structurally impossible to hedge and must be modelled across both scenarios before assigning value to Talos's production guidance

- The parallel execution of Shell and BP Gulf of America portfolio moves in mid-2026 signals a basin-wide ownership restructuring that is likely to continue as additional mature non-operated positions come to market

This article contains forward-looking analysis based on publicly available information. References to production targets, acquisition cost estimates, and reserves additions reflect company disclosures and should not be construed as investment advice. Transaction outcomes remain subject to regulatory approvals, BP's preferential right decision, and commodity price movements.

Want to Spot the Next Major Resource Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological data into clear, actionable investment insights the moment they hit the exchange — explore historic discovery returns to understand what early positioning in transformative resource finds has meant for investors, and begin your 14-day free trial today to secure a market-leading edge.