May 23, 2026

When a Single Facility Can Derail an Entire Conglomerate

In large integrated metals groups, the financial architecture is rarely as diversified as it appears on the surface. A company might operate across multiple continents, serve dozens of end markets, and hold exposure to several commodity cycles simultaneously, yet still carry a hidden concentration risk that no commodity price rally can fully neutralise. When one subsidiary accounts for roughly 60% of group revenue, its operational health is not merely a divisional concern. It becomes the central variable in group-level earnings.

This is the structural reality that explains why Hindalco Industries, one of India's most prominent aluminium and copper producers and a constituent of the Aditya Birla Group, delivered a deeply disappointing quarterly result in Q4 FY2026, despite operating in an environment of sharply rising base metal prices. Hindalco misses profit estimates as Novelis disruptions weigh has become the defining financial narrative for the company across two consecutive quarters, and understanding precisely why requires a closer look at the mechanics of downstream aluminium processing, facility-level operational risk, and the limits of commodity price tailwinds. Furthermore, this case raises broader questions about how concentration risk is priced across diversified metals conglomerates — questions relevant to aluminium industry leaders and investors alike.

When big ASX news breaks, our subscribers know first

The Numbers That Told the Story

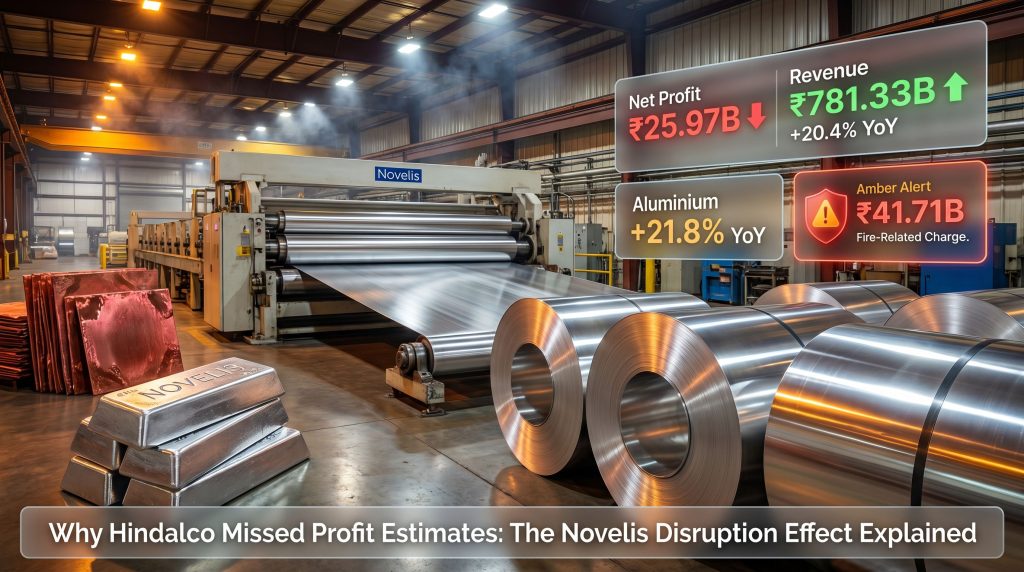

Hindalco's consolidated net profit for the quarter ended March 31, 2026, came in at ₹25.97 billion, representing a 50.8% year-on-year decline. Against an analyst consensus forecast of approximately ₹43.12 billion, this represented a shortfall of roughly ₹17 billion, or nearly 40% below expectations. As reported by Reuters, the miss was largely attributed to the extraordinary disruptions at the Novelis subsidiary.

What makes this miss particularly striking is that it occurred alongside a significant revenue beat. The group's overall revenue from operations climbed 20.4% year-on-year to ₹781.33 billion, comfortably exceeding the analyst estimate of ₹723.96 billion. Revenue growth and profit collapse occupying the same quarterly result is a rare and analytically significant combination, and it points unambiguously toward a single cause: an extraordinary charge that overwhelmed operating leverage.

| Metric | Reported | Analyst Estimate | Variance |

|---|---|---|---|

| Consolidated Net Profit | ₹25.97 billion | ₹43.12 billion | -39.8% miss |

| Revenue from Operations | ₹781.33 billion | ₹723.96 billion | +7.9% beat |

| Novelis Revenue Contribution | ~60% of top line | — | — |

| Novelis Revenue Growth (YoY) | +10.3% | — | — |

| Exceptional Charge (Fire-Related) | ₹41.71 billion | — | — |

The ₹41.71 billion exceptional charge recorded in Q4 FY2026 was directly attributable to fire-related incidents at Novelis' Oswego, New York facility. This single line item effectively erased the profit contribution that elevated aluminium and copper prices would otherwise have generated. Consequently, the relationship between commodity prices and earnings proved far more complex than standard models anticipated.

Understanding Novelis: The Downstream Aluminium Engine

What Novelis Actually Does and Why It Is Difficult to Replace

Novelis is not a conventional mining or smelting operation. It sits at the downstream end of the aluminium value chain, transforming primary metal into flat-rolled aluminium products used across high-value, specification-sensitive industries. Its core customers include:

- Beverage can manufacturers requiring precise gauge and alloy specifications

- Automotive original equipment manufacturers using aluminium sheet for body panels, closures, and structural components

- Packaging and industrial clients demanding consistent surface quality and formability

This downstream positioning carries several important characteristics that distinguish Novelis from upstream aluminium production. First, it operates on long-term supply contracts with major customers, providing revenue visibility that pure commodity producers rarely enjoy. Second, its recycling-intensive model, where a significant proportion of input material comes from post-consumer scrap, gives it a structurally lower carbon footprint than primary smelting operations — a dimension that aligns closely with the growing importance of low-carbon metals production across the sector. This ESG alignment has become increasingly relevant as institutional investors apply carbon-intensity screens to metals sector holdings.

Third, and most critically for understanding the Oswego disruption impact, the automotive and beverage can industries operate on just-in-time supply principles. Customers do not carry large inventory buffers and cannot easily substitute a supplier mid-contract. When a key Novelis facility goes offline, the downstream consequences extend beyond Hindalco's own financial statements into customer supply chains.

The Concentration Dynamic That Amplifies Subsidiary Risk

Because Novelis contributes approximately 60% of Hindalco's consolidated top-line revenue, any meaningful operational disruption at a major Novelis facility does not stay contained within a divisional profit and loss account. It propagates directly into group-level earnings with a force that minority-weight subsidiaries simply cannot replicate.

When a subsidiary of this scale experiences an unplanned production halt, it functions less like a business unit disruption and more like a balance sheet event for the parent company.

This concentration dynamic is often underappreciated by investors who assess diversified conglomerates through a geographic or commodity diversification lens. Hindalco operates across India and the United States, across aluminium and copper, and across upstream and downstream segments. Yet none of that diversification could absorb the Oswego impact. In addition, the Hindalco metals expansion strategy that has underpinned long-term growth has paradoxically amplified the group's exposure to a single subsidiary's operational performance.

The Oswego Fire Incidents: What Happened and What It Cost

A Sequence of Events That Compounded Over Months

Novelis' Oswego, New York facility holds historical significance as the company's first United States operational site. It is a rolled aluminium production plant feeding North American customers across the beverage can and automotive segments. In September and November 2025, the facility experienced two separate fire-related incidents that caused significant production interruptions extending into the Q4 FY2026 reporting period.

The sequential nature of the disruptions is important. A single isolated incident might be contained within one quarter. Two separate events across a compressed timeframe created a compounding production loss that proved much harder to manage through alternative supply arrangements or capacity reallocation across Novelis' global network.

Hindalco management confirmed that the Oswego plant restart was expected to occur within weeks of the May 2026 earnings announcement, suggesting the physical rehabilitation of the facility was largely complete even as the financial accounting of the damage was being finalised.

The $1.6 Billion Total Impact Estimate: Breaking It Down

Hindalco previously disclosed that the total financial impact of the Oswego fire events could reach up to $1.6 billion. This figure encompasses several distinct cost categories:

- Direct production losses arising from the volume of flat-rolled aluminium that could not be manufactured and delivered during the outage period

- Asset damage to plant, equipment, and infrastructure requiring repair or replacement

- Remediation costs including environmental assessment, structural rehabilitation, and safety compliance work required before restart authorisation

- Customer-related costs potentially including contractual penalties, expediting fees, or costs incurred to source alternative supply for affected customers

The Q4 FY2026 exceptional charge of ₹41.71 billion represents the portion of this total impact recognised within the current quarter's accounts. The gap between this figure and the broader $1.6 billion estimate suggests that additional charges may flow through future quarters, particularly if insurance recovery proceeds are delayed or if restart costs exceed current projections.

The distinction between the quarterly charge and the total estimated impact is a critical variable that forward earnings models must incorporate explicitly, not as a footnote.

Commodity Price Tailwinds: Powerful but Not Powerful Enough

The Arithmetic of an Overridden Tailwind

The broader commodity price environment during Q4 FY2026 was genuinely supportive for an integrated aluminium and copper producer. Benchmark three-month aluminium futures rose 21.8% year-on-year, while copper prices surged 36.7% year-on-year over the same period. Under normal operational conditions, these price movements would translate into materially higher revenue per tonne, expanded margins, and a significant year-on-year profit uplift for a business of Hindalco's scale and integration.

That this did not occur quantifies the Oswego disruption in concrete financial terms. A 20%-plus increase in the benchmark aluminium price is not a marginal tailwind. It represents a structural earnings boost for any producer with meaningful aluminium exposure. The fact that Hindalco misses profit estimates despite this tailwind illustrates that the ₹41.71 billion exceptional charge did not merely reduce profit — it reversed the direction of the earnings trajectory entirely.

Why Standard Earnings Models Failed to Anticipate the Miss

Analyst consensus models for diversified metals producers typically incorporate the following variables:

- Forward commodity price curves

- Historical margin ranges by segment

- Volume forecasts based on capacity utilisation

- Known capital expenditure and depreciation schedules

What these models structurally cannot incorporate in advance is a facility-specific catastrophic event. Exceptional charges arising from industrial accidents, fires, or natural disasters are not amenable to probabilistic modelling in the same way that commodity price sensitivity can be parameterised. The result is a systematic forecast error when such events occur, and in this case, the error magnitude was approximately ₹17 billion.

For investors, this points toward an underappreciated analytical practice: applying an operational risk discount to earnings forecasts for heavy industrial operations, particularly those involving high-temperature aluminium processing environments where fire risk is a structural and ongoing concern.

India Operations: The Earnings Floor That Held

Record Performance Across Domestic Segments

While the Novelis disruption dominated the group-level narrative, Hindalco's India business delivered what management characterised as a record performance across all three of its primary domestic operating segments. The Q4 period is seasonally advantageous for India's industrial economy, with:

- Construction activity peaking ahead of the monsoon season, driving demand for aluminium and copper used in building and electrical infrastructure

- Automotive manufacturers pushing production and sales volumes to meet year-end financial targets, supporting flat-rolled aluminium demand

- Higher commodity prices flowing through to improved realisations on primary metal output

The three India segments that delivered record results were:

- Aluminium upstream covering primary metal production from bauxite through smelting

- Aluminium downstream covering value-added fabricated and rolled products for the domestic market

- Copper where Hindalco operates as India's largest integrated copper producer, benefiting directly from the 36.7% year-on-year copper price appreciation

How the India Business Limits Group-Level Downside

The India segment's strength is not merely a positive data point within a disappointing result. It functions as a structural earnings floor that prevents the Novelis disruption from catastrophically impairing the group's overall financial position. Even with a ₹41.71 billion exceptional charge at the subsidiary level, Hindalco's revenue from operations still grew by more than 20% year-on-year and exceeded consensus estimates.

This dynamic illustrates the genuine diversification value within Hindalco's business architecture, even if that diversification is less effective at protecting profit than it is at sustaining revenue. Furthermore, it underscores the extent to which mining consolidation trends and integrated group structures can provide partial, though not complete, resilience against subsidiary-level shocks.

The next major ASX story will hit our subscribers first

The Recurrence Pattern: Switzerland Before Oswego

A Prior Disruption That Established a Warning Signal

The Oswego incident was not the first major operational disruption in Novelis' recent history. The company had previously experienced a significant production disruption at its Switzerland facility, an event that contributed to Hindalco falling short of first-quarter profit estimates in an earlier reporting period. That Switzerland disruption generated a net cash impact of approximately $80 million, a figure that, while material, was substantially smaller than the scale of the Oswego impact.

The occurrence of two significant facility disruptions across different geographies and different time periods within approximately twelve months raises questions that go beyond any single incident explanation. Industrial fire events and unplanned production outages in aluminium rolling operations can occur for various reasons including:

- Molten metal handling accidents where liquid aluminium contacts water or other reactive materials

- Hydraulic system failures in rolling mill equipment operating under extreme pressure

- Electrical faults in the high-amperage systems required for aluminium processing

- Casthouses and melt furnaces where thermal runaway scenarios are an ongoing operational risk

The aluminium rolling industry is inherently a high-energy, high-temperature environment. Flat-rolled aluminium production involves casting molten metal, hot rolling at temperatures exceeding 400 degrees Celsius, and cold rolling under significant mechanical stress. These processes require rigorous maintenance discipline and operational safety protocols.

Two significant disruptions across separate continents within a 12-month window is a pattern that demands scrutiny of enterprise-wide operational risk management practices, not just site-specific explanations.

Recovery Outlook: What Investors Are Watching

Key Variables in the Normalisation Timeline

The path to earnings normalisation for Hindalco depends on several interconnected factors, each with its own uncertainty range:

| Recovery Factor | Status (as of May 2026) | Investor Significance |

|---|---|---|

| Oswego plant restart | Weeks away | Critical for production volume recovery |

| Insurance recovery proceeds | Pending quantification | Could materially reduce net $1.6B impact |

| Aluminium price trajectory | Elevated (+21.8% YoY) | Higher realisations per tonne upon restart |

| Novelis revenue trend | +10.3% YoY despite disruption | Confirms underlying business health |

| India segment momentum | Record performance | Provides earnings stability during recovery |

| Future exceptional charge risk | Dependent on total impact crystallisation | Key unknown for near-term forecasts |

The Insurance Recovery Variable

One of the most analytically underweighted aspects of the Oswego disruption is the potential for insurance recovery proceeds to significantly reduce the net financial impact on Hindalco's consolidated accounts. Large-scale industrial facilities of Novelis' type typically carry substantial property and business interruption insurance coverage.

The timing and quantum of insurance recoveries are difficult to forecast precisely, as they depend on claims assessment, policy terms, and insurer negotiations that can extend over multiple quarters. However, if insurance proceeds are material relative to the $1.6 billion total impact estimate, the actual net cost to Hindalco's financial position could be considerably lower than the headline figure suggests. This potential offset is arguably the most significant positive catalyst for accelerating Hindalco's earnings recovery timeline.

A Framework for Evaluating Operational Risk in Metals Conglomerates

Rethinking How Concentration Risk Is Priced

The situation in which Hindalco misses profit estimates as Novelis disruptions weigh offers a case study that extends well beyond a single company's quarterly results. For investors evaluating diversified metals and mining conglomerates, the conventional diversification framework often focuses on commodity exposure breadth, geographic spread, and end-market balance. These are legitimate analytical dimensions, but they do not adequately capture subsidiary concentration risk.

A more comprehensive analytical approach would incorporate:

- Revenue concentration ratios identifying subsidiaries contributing more than 40% of group top-line revenue as concentration risk triggers

- Facility criticality mapping assessing which individual plants are irreplaceable within a subsidiary's production network

- Business interruption insurance adequacy relative to peak quarterly production value at critical facilities

- Multi-site production redundancy evaluating whether volume losses at one facility can be meaningfully offset by others within the same network

- Operational risk history as a distinct analytical factor separate from financial performance metrics

When one subsidiary commands 60% of group revenue and one facility within that subsidiary can generate a $1.6 billion total impact event, the standard diversification premium attached to conglomerate structures may be significantly overstated.

FAQ: Hindalco Profit Miss and Novelis Disruptions

Why Did Hindalco Miss Profit Estimates Despite Rising Aluminium Prices?

An exceptional charge of ₹41.71 billion related to fire-related incidents at the Novelis Oswego plant fully offset the earnings benefit generated by a 21.8% year-on-year increase in benchmark aluminium prices during the quarter.

What Does Novelis Produce and Who Are Its Customers?

Novelis manufactures flat-rolled aluminium products supplied to beverage can producers, automotive manufacturers, and packaging clients across North America, Europe, South America, and Asia.

How Large Could the Total Oswego Financial Impact Be?

Hindalco has estimated the total financial impact at up to $1.6 billion, covering production losses, asset damage, and remediation costs. Insurance recoveries may reduce the net impact significantly, though their timing and scale remain uncertain.

When Was the Oswego Plant Expected to Restart?

As of Hindalco's May 2026 earnings announcement, management indicated a restart was expected within the following few weeks.

How Did Hindalco's India Business Perform?

The India business delivered record results across aluminium upstream, aluminium downstream, and copper segments, providing a meaningful earnings contribution that partially offset the Novelis-related drag.

Has Novelis Experienced Disruptions Before Oswego?

A prior disruption at Novelis' Switzerland facility generated an approximate $80 million net cash impact and contributed to an earlier quarterly earnings miss, establishing a pattern that has drawn scrutiny from analysts and investors. Consequently, the broader question of whether Hindalco misses profit estimates again in coming quarters will depend heavily on whether operational risk management practices are strengthened across the Novelis network.

Want To Spot The Next Major Metals Discovery Before The Market Does?

While Hindalco's Novelis disruptions illustrate the risks of downstream concentration in established metals conglomerates, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time to deliver instant alerts on significant mineral discoveries — turning complex exploration data into actionable opportunities for investors at every level. Explore historic discovery returns that demonstrate just how transformative early positioning can be, and begin your 14-day free trial today to secure a genuine market-leading edge.