June 6, 2026

The global mining industry stands at a critical juncture where operational resilience increasingly determines competitive advantage. The impact of Iran war on iron-ore fuel costs has created unprecedented disruption across traditional cost structures, forcing iron ore producers to navigate a complex landscape of energy dependencies. The intersection of geopolitical risk and energy security has fundamentally altered the strategic calculus for mining operations worldwide.

Rising Energy Costs Transform Mining Economics

The financial implications of energy price volatility have reached unprecedented levels across the iron ore sector. Current market conditions demonstrate the material sensitivity of mining operations to fuel cost fluctuations, with industry leaders quantifying exposure in specific terms that highlight the scale of potential impact.

Fortescue Metals Group, operating as the world's fourth-largest iron ore supplier, has disclosed that every 10-cent movement in diesel prices translates to a $70 million impact on their operational costs. This sensitivity metric provides insight into the fuel-intensive nature of large-scale mining operations, where diesel consumption spans extraction, processing, and transportation activities.

Industry-Wide Exposure Analysis

The cumulative impact across major producers reveals the systemic nature of fuel cost exposure within the iron ore sector. Analysis of the top four global iron ore producers indicates that each 10-cent diesel price movement generates a combined $500 million cost impact across these operations.

This exposure calculation encompasses:

- Open-pit mining equipment and machinery operation

- Ore processing and beneficiation facilities

- Internal transportation and logistics networks

- Power generation for remote operations

- Heavy machinery maintenance and support systems

The scale of these impacts reflects the diesel-intensive nature of iron ore production, where fuel serves as a primary input across multiple operational phases. Mining companies typically consume diesel for mobile equipment including haul trucks, excavators, drilling rigs, and auxiliary power generation in remote locations where grid connectivity remains limited.

Regional Fuel Sourcing Dependencies

Australian iron ore producers face particular vulnerabilities through their reliance on Southeast Asian fuel supply chains. Fortescue sources the majority of its fuel requirements from this region, creating exposure to supply disruptions that extend beyond immediate operational boundaries.

Current fuel inventory management strategies focus on maintaining sufficient reserves to sustain operations during short-term supply interruptions. However, extended geopolitical conflicts present scenarios that challenge traditional inventory planning assumptions, requiring mining companies to reassess their fuel security protocols.

The geographic concentration of fuel sourcing creates strategic dependencies that mining companies increasingly recognise as material operational risks. Alternative sourcing strategies involve diversifying supplier relationships and exploring regional fuel distribution networks that provide greater supply chain resilience.

When big ASX news breaks, our subscribers know first

Geopolitical Disruption Creates Energy Market Volatility

The escalation of military operations involving Iran has severely impacted global energy transportation networks, with particular focus on the Strait of Hormuz shipping corridor. This strategic waterway typically facilitates approximately 20% of global petroleum liquids trade, making its disruption a significant factor in worldwide energy markets.

Current conditions indicate that military activities have substantially reduced shipping volumes through this critical passage, creating supply constraints that transmit directly to regional fuel markets. The resulting price pressures affect diesel availability and costs across mining operations that depend on imported fuel supplies.

Oil Price Trajectory and Mining Impact

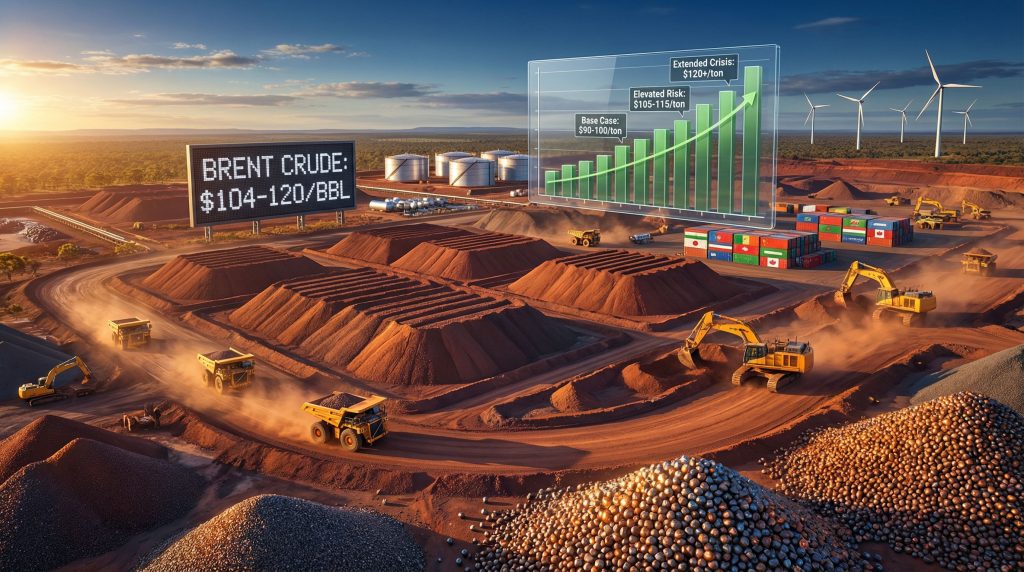

Energy market analysts project potential oil price scenarios ranging from baseline levels to crisis-driven peaks exceeding $120 per barrel. These projections reflect the uncertain duration and intensity of current geopolitical tensions, with mining operations particularly sensitive to sustained price elevation.

The transmission mechanism from crude oil prices to diesel costs operates through refining margins and distribution networks. Furthermore, the crude oil price rally creates both direct fuel cost increases and secondary impacts from elevated transportation and logistics expenses throughout supply chains.

Energy price volatility creates planning challenges for mining operations that require predictable cost structures for production optimisation and financial forecasting. Companies increasingly implement hedging strategies and alternative energy investments to mitigate exposure to these market fluctuations.

Maritime Transport Cost Escalation

Dry bulk shipping rates experience upward pressure from multiple factors related to current geopolitical conditions. Energy costs for vessel operations increase directly with fuel price movements, while route diversions and extended transit times compound overall transportation expenses.

Insurance premiums for vessels operating in affected regions have risen substantially, reflecting increased risk assessments by maritime insurers. These premium increases flow through to cargo rates, affecting the delivered cost of iron ore shipments to key markets.

Port congestion at alternative shipping routes creates additional delays and costs as maritime traffic redirects away from traditional passages. The resulting inefficiencies in global shipping networks contribute to elevated logistics costs across the iron ore supply chain.

Strategic Decarbonisation as Risk Mitigation

Mining companies increasingly position energy transition investments as operational risk management rather than purely environmental initiatives. This strategic reframing reflects the recognition that renewable energy infrastructure provides hedging benefits against fossil fuel price volatility.

Fortescue's decarbonisation program demonstrates this dual-benefit approach, targeting annual savings of at least $100 million through electrification and renewable energy integration. The company projects reducing diesel consumption by one billion litres equivalent over several years, representing substantial operational cost mitigation.

Technology Implementation and Cost Benefits

The integration of renewable energy sources into mining operations encompasses multiple technology applications, with decarbonisation benefits extending beyond environmental compliance:

- Solar photovoltaic systems for stationary power requirements

- Battery storage systems for load balancing and power quality

- Electric vehicle adoption for mobile mining equipment

- Hybrid power systems combining renewables with conventional generation

- Energy management systems optimising consumption patterns

Capital investments in renewable energy infrastructure require substantial upfront expenditure but provide long-term operational cost advantages. Mining companies evaluate these investments based on fuel price assumptions, operational lifespan, and financing costs to determine optimal implementation timelines.

The competitive advantage from energy independence extends beyond immediate cost savings to include operational resilience during supply disruptions. Companies with greater renewable energy integration maintain production capacity during fuel supply constraints that affect competitors relying entirely on imported fuels.

Supply Chain Risk Management Evolution

Advanced fuel hedging mechanisms enable mining companies to manage price volatility through financial instruments that provide cost certainty for future periods. These strategies include forward contracts, options, and swap agreements that establish predetermined fuel costs for specific timeframes.

Regional diversification of energy suppliers reduces dependency on individual supply sources and provides alternative procurement options during market disruptions. However, the impact of Iran war on iron-ore fuel costs demonstrates that even diversified supply chains remain vulnerable to major geopolitical events.

Emergency inventory protocols establish minimum fuel reserves sufficient to maintain operations during extended supply interruptions. These protocols consider consumption rates, supply lead times, and storage capacity to determine appropriate inventory levels for different operational scenarios.

Market Price Dynamics Under Conflict Scenarios

Iron ore pricing mechanisms incorporate multiple variables including supply-demand fundamentals, transportation costs, and geopolitical risk premiums. Current market conditions create upward pressure on prices through both direct cost increases and risk-based valuation adjustments.

Market scenario analysis indicates potential price trajectories based on conflict duration and intensity, with iron ore price trends showing significant sensitivity to energy cost fluctuations:

| Conflict Scenario | Price Range ($/tonne) | Primary Drivers |

|---|---|---|

| Baseline Conditions | $90-100 | Normal supply-demand balance |

| Elevated Risk Environment | $105-115 | Energy cost increases, risk premium |

| Extended Crisis Period | $120+ | Severe supply chain disruption |

These projections reflect the transmission of energy costs through mining operations and the additional risk premiums that markets assign during periods of geopolitical uncertainty.

Chinese Demand and Inventory Management

China's role as the dominant global steel producer creates concentrated demand for iron ore that influences global pricing dynamics. Current port inventory levels in China maintain approximately 30-35 days of supply coverage, representing 120-130 million tonnes of stored material.

Chinese steel producers adjust production rates in response to input cost increases, creating demand variability that affects iron ore pricing. Higher energy costs for steel production may reduce Chinese demand for iron ore, potentially offsetting upward price pressures from supply-side cost increases.

Strategic stockpiling considerations become more prominent during supply uncertainty, with Chinese buyers potentially increasing inventory levels as insurance against future supply disruptions. These iron ore demand insights indicate that stockpiling behaviour can temporarily elevate demand and support higher iron ore prices.

Long-Term Structural Market Changes

Energy security integration represents a fundamental shift in mining industry strategic planning. Companies increasingly evaluate operational decisions through the lens of energy independence, viewing renewable energy investments as competitive advantages rather than regulatory compliance measures.

This strategic evolution reflects investor and shareholder pressure for operational resilience that extends beyond traditional cost optimisation. Mining companies report changing stakeholder expectations that prioritise energy security and supply chain resilience alongside financial performance metrics.

Infrastructure Investment Acceleration

Renewable energy infrastructure development timelines accelerate as mining companies recognise the strategic value of energy independence. Capital allocation priorities shift toward projects that reduce fossil fuel dependencies whilst maintaining operational capacity and efficiency.

Technology adoption patterns favour solutions that provide immediate fuel efficiency improvements alongside longer-term energy transition security benefits. Mining companies implement integrated approaches that combine short-term efficiency gains with strategic infrastructure investments.

Partnership formations with renewable energy developers and technology providers enable mining companies to access specialised expertise and accelerated implementation timelines. These partnerships often involve long-term agreements that provide cost certainty and operational support.

Investment Implications and Valuation Adjustments

Mining company valuations increasingly incorporate energy cost sensitivity and renewable energy adoption as material factors affecting long-term competitiveness. Investment analysis frameworks expand beyond traditional mining metrics to include energy security and operational resilience assessments.

Risk premium calculations reflect the operational vulnerabilities associated with fossil fuel dependence, particularly for companies with concentrated geographic exposure or limited supply diversification. These risk adjustments influence cost of capital and investment returns across the mining sector.

Competitive Positioning Through Energy Efficiency

Companies with advanced energy transition programs demonstrate improved operational resilience during periods of fuel price volatility. This resilience translates to more stable operational costs and reduced sensitivity to external energy market disruptions.

Capital allocation toward energy independence projects provides measurable returns through fuel cost savings and operational risk reduction. In addition, mining companies could face billions more in fuel costs if current geopolitical tensions persist.

ESG considerations drive institutional investment decisions, with energy transition progress serving as a key differentiator among mining company investment options. Companies demonstrating clear pathways to energy independence attract investment flows that support continued expansion and development.

The next major ASX story will hit our subscribers first

Extended Conflict Impact on Global Supply

Production disruption risk assessment becomes critical for mining operations with high fuel dependencies and limited energy alternatives. Extended geopolitical conflicts present scenarios where fuel supply interruptions could force production curtailments or temporary operations suspension.

Critical threshold analysis identifies the fuel price levels and supply availability conditions that threaten operational viability for different mining operations. Companies with higher fuel intensity face greater vulnerability to sustained energy market disruptions.

Alternative Energy Source Scalability

The timeline for implementing alternative energy solutions varies significantly based on operational requirements, geographic location, and existing infrastructure. Mining companies evaluate scalability options that provide incremental fuel reduction capabilities whilst maintaining production capacity.

Force majeure considerations become relevant when energy supply disruptions prevent companies from meeting contractual obligations. Mining companies review contract terms and insurance coverage to understand their exposure and obligations during extended supply interruptions.

Global steel industry adaptation strategies influence iron ore demand patterns as steel producers optimise their operations for higher input costs. These adaptations may include production efficiency improvements, alternative raw material utilisation, and regional market rebalancing.

Strategic Response Framework for Mining Operations

The impact of Iran war on iron-ore fuel costs necessitates comprehensive response frameworks that address both immediate operational challenges and long-term strategic positioning. Mining companies develop multi-faceted approaches that combine risk mitigation with competitive advantage development.

Operational contingency planning encompasses fuel supply diversification, inventory management optimisation, and alternative energy source integration. Companies establish clear protocols for managing supply chain disruptions whilst maintaining production capacity and meeting contractual obligations.

"The intersection of energy security and operational resilience has become a defining characteristic of competitive advantage in global iron ore production. Companies that successfully navigate this transition position themselves for sustained profitability in an increasingly volatile energy environment."

The strategic implications extend beyond immediate operational concerns to encompass long-term industry structure changes. Mining companies that prioritise energy independence and supply chain resilience demonstrate improved capacity to maintain production and market position during periods of geopolitical and economic uncertainty.

Investment Disclaimer: This analysis contains forward-looking statements and market projections that involve inherent uncertainties. Commodity prices, geopolitical developments, and operational outcomes may differ materially from projections presented. Readers should conduct independent research and consult qualified advisors before making investment decisions based on this information.

Ready to Capitalise on Mining Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping investors identify actionable opportunities in volatile markets before broader recognition occurs. Begin your 14-day free trial with Discovery Alert today and gain the market-leading advantage needed to navigate complex commodity cycles and geopolitical disruptions.