August 6, 2026

The Baseload Blind Spot: Why India's Renewable Energy Mix Is Missing Its Most Critical Component

Every serious discussion about energy transition eventually collides with the same inconvenient reality: solar panels stop generating at night, and wind turbines go still when the air does. For a country as large, industrially complex, and energy-hungry as India, managing this intermittency problem is not merely a technical inconvenience. It is a structural vulnerability embedded at the heart of the country's renewable energy strategy. India geothermal potential offers a compelling answer to this challenge that has, until recently, been largely overlooked.

Geothermal energy does not share this limitation. Drawing heat continuously from the Earth's crust regardless of season, weather, or time of day, geothermal power plants routinely achieve capacity utilisation rates exceeding 80%, placing them in an entirely different performance category from solar assets that typically operate at 15% to 25% capacity factors in Indian conditions. That single distinction makes geothermal not just another renewable source but a genuinely complementary one, capable of providing the firm, dispatchable generation that batteries and demand-response programmes cannot yet reliably replace at national scale.

What makes the current moment particularly significant is that India's geothermal resources are no longer simply a geological curiosity mapped by survey teams in the 1970s. A convergence of improved subsurface data, advances in deep drilling technology, and a newly established national policy framework has fundamentally repositioned India geothermal potential from scientific footnote to strategic energy asset. Furthermore, this shift is occurring precisely when critical minerals and energy security concerns are reshaping how nations think about their long-term power infrastructure.

When big ASX news breaks, our subscribers know first

Quantifying the Opportunity: What the Numbers Actually Mean

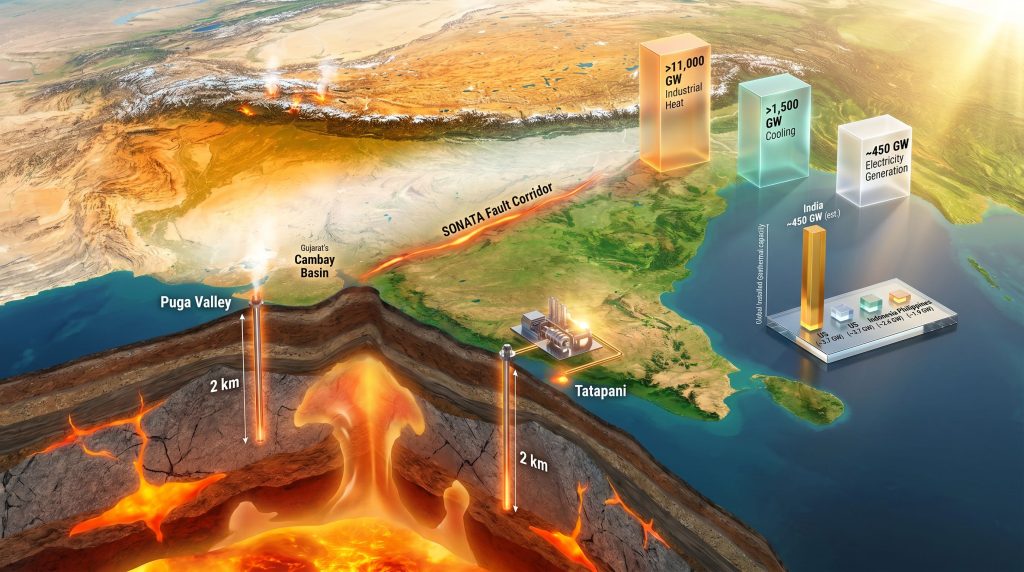

A landmark study titled The Future of Geothermal in India, published in May 2026 by Project InnerSpace in partnership with the Council on Energy, Environment and Water (CEEW), placed India's total technical geothermal potential at figures that are difficult to fully absorb at first reading.

| Application Category | Estimated Technical Potential | Primary Beneficiaries |

|---|---|---|

| Industrial Heat | >11,000 GW | Manufacturing, data centres, heavy industry |

| Cooling Applications | >1,500 GW | Urban centres, commercial buildings |

| Electricity Generation | ~450 GW | Grid supply, baseload power |

The 450 GW electricity generation figure is particularly striking because it is roughly equivalent to India's entire current installed power generation capacity from all sources combined. To put this in further context, total global installed geothermal power capacity stands at approximately 16 GW, meaning India's untapped electricity potential alone represents roughly 28 times the entire world's current geothermal output.

The industrial heat category, at more than 11,000 GW, dwarfs the electricity figure by an order of magnitude. This matters because industrial process heat is one of the most stubbornly difficult segments of any economy to decarbonise. Many manufacturing, chemical, food processing, and textile operations require sustained temperatures in the 80°C to 200°C range, conditions that are technically and economically challenging to achieve through electrification alone. Geothermal resources operating within this temperature band could directly displace fossil fuel combustion in sectors where the energy transition has made the least progress.

How Does This Compare to Earlier Assessments?

The dramatic scale of these estimates becomes even clearer when set against India's historical geothermal baseline. The Geological Survey of India (GSI) identified 381 hot springs distributed across 10 distinct geothermal provinces, with 113 sites assessed as technically suitable for exploitation. Early GSI assessments, conducted primarily in the 1970s and 1980s, estimated India's power generation potential at approximately 10,600 MW (10.6 GW), a figure that remained relatively unchallenged for decades.

The gap between 10.6 GW and 450 GW is not the result of discovering new geological formations. It reflects three fundamental shifts:

- Deeper drilling capability: Modern technology can reach reservoir depths that were commercially inaccessible when the GSI conducted its original surveys

- Enhanced Geothermal Systems (EGS): EGS technology allows heat extraction from hot dry rock formations that lack natural fluid permeability, dramatically expanding the resource definition beyond conventional hydrothermal systems

- Higher-resolution subsurface imaging: Advanced seismic and geophysical mapping tools now provide far greater confidence in reservoir characterisation before drilling commences

The original GSI assessments were technically sound for their era but were constrained by the tools and commercial frameworks available at the time. They were never intended to represent the full exploitable resource, only what was accessible with mid-20th century technology and economics. According to geothermal resource assessments published in the Journal of the Geological Society of India, India's geological characteristics position it as one of the most promising emerging geothermal markets globally.

A Regional Resource Map: Where India's Geothermal Heat Is Concentrated

India's geothermal resources are not evenly distributed. They cluster along specific geological structures, and understanding those structures is essential to prioritising development.

The Himalayan Belt: High-Temperature Prospects Driven by Active Tectonics

The most thermally energetic geothermal environments in India occur along the Himalayan arc, where active tectonic processes along the Indo-Eurasian plate boundary generate elevated heat flow at relatively shallow depths. Puga Valley in Ladakh stands as the most advanced prospect in this corridor, with estimated reservoir temperatures between 180°C and 230°C and documented surface hot spring temperatures reaching 123°C, conditions that meet the threshold for direct electricity generation without requiring additional heat enhancement.

Additional high-temperature sites along this corridor include Manikaran in Himachal Pradesh and Tapoban in Uttarakhand. The Beas and Parvati river valleys in Himachal Pradesh are also under active exploration consideration.

The SONATA Fault Zone: Central India's Geothermal Backbone

The Son-Narmada-Tapi fault system, commonly referred to as the SONATA zone, represents one of India's most structurally significant geothermal corridors and runs across a densely populated and industrially active region of central India. Tatapani in Chhattisgarh has recorded surface water temperatures of 112.5°C, with reservoir estimates ranging from 150°C to 230°C, and has been identified as a candidate for a 25 MW pilot power project. The Anhoni-Samoni area in Madhya Pradesh represents another documented thermal site within this zone.

Western India and Gujarat: Industrial Heat and Emerging Digital Infrastructure

Gujarat's combination of geothermal heat availability and existing industrial infrastructure creates one of the most commercially compelling development scenarios in the country. The Cambay Basin and associated localities, including Jhagadia, Dholera, Tuwa, and Tulsishyam, present viable geothermal resources in close proximity to petrochemical, textile, and pharmaceutical manufacturing clusters that have significant heat demand.

Gujarat also hosts emerging data centre development corridors, particularly around Dholera, where continuous baseload power supply and geothermal cooling applications would directly address the operational requirements of energy-intensive digital infrastructure.

State-Level Development Readiness Overview

| State | Key Sites | Primary Application | Development Stage |

|---|---|---|---|

| Ladakh / J&K | Puga Valley | Power generation | Advanced exploration |

| Gujarat | Cambay Basin, Dholera | Industrial heat, data centres | Moderate exploration |

| Chhattisgarh | Tatapani | Power generation (25 MW pilot) | Planning stage |

| Himachal Pradesh | Manikaran, Beas Valley | Power + direct use | Early exploration |

| Telangana | Manuguru | Direct use, power | Early exploration |

| West Bengal | Multiple sites | Low-enthalpy applications | Preliminary |

| Maharashtra | Multiple sites | Industrial heat | Preliminary |

| Andhra Pradesh | Multiple sites | Mixed applications | Preliminary |

The Project InnerSpace and CEEW report identified Gujarat, Uttar Pradesh, West Bengal, Telangana, Maharashtra, and Andhra Pradesh as leading states for geothermal deployment, reflecting a broader geographic distribution than the Himalayan and SONATA zones alone. The eastern and northeastern frontier zones, including Deulajhari in Odisha and sites across Meghalaya, Assam, and Bihar, contain documented thermal anomalies but remain at earlier characterisation stages.

The Barriers That Have Kept Geothermal Sidelined

Understanding why India's geothermal sector has remained largely dormant despite this scale of potential requires examining the structural barriers that have historically suppressed development. Three core constraints stand out.

1. Exploration Risk and Subsurface Uncertainty

Unlike solar or wind installations, where resource assessment is relatively low-cost and highly predictable, geothermal development demands substantial capital commitment before a project can confirm whether a commercially viable reservoir actually exists. Most historical Indian geothermal exploration has been conducted at relatively shallow depths, limiting the ability to confirm the deep reservoir temperatures and fluid flow rates required for power generation. Priority sites such as Puga and Tatapani require drilling to depths approaching 2 kilometres before meaningful resource characterisation is possible.

2. The Historical Absence of a Policy Framework

Until 2025, India had no dedicated regulatory architecture for geothermal energy. Developers faced unclear licensing pathways, no revenue certainty mechanisms, and no risk-sharing provisions. The dominance of competitively priced coal-based power generation also suppressed the commercial logic for investing in higher-risk geothermal exploration during the decades when the sector might otherwise have developed.

3. Technology and Capital Access Gaps

Deep drilling expertise, EGS engineering capability, and high-resolution subsurface imaging have historically required international partnerships that the Indian geothermal sector lacked the institutional structures to facilitate. Countries that have successfully scaled geothermal, including Kenya, Iceland, and the Philippines, have done so with the support of concessional exploration risk funds and state-backed de-risking mechanisms that India had not yet established.

The study released by Project InnerSpace and CEEW confirmed that geothermal deployment in India has remained limited to pilot projects due precisely to this combination of exploration risks, uncertain drilling outcomes, and the absence of enabling policy frameworks. (ETEnergyWorld, May 2026)

How the Policy Landscape Is Shifting in 2025 and Beyond

The introduction of India's National Policy on Geothermal Energy by the Ministry of New and Renewable Energy (MNRE) in 2025 represents the most significant structural change in the sector's history. For the first time, geothermal energy in India has a dedicated regulatory home, with provisions that directly address the barriers outlined above. In addition, this policy arrives at a moment when critical minerals demand for clean energy technologies is accelerating globally, strengthening the strategic case for diversifying India's energy mix.

Key strategic directions embedded in the policy include:

- Encouraging established oil and gas drilling companies, including entities with ONGC-type capabilities, to redirect existing subsurface expertise toward geothermal exploration

- Creating pathways for converting decommissioned or underperforming oil and gas wells into geothermal production assets, potentially reducing early-stage drilling costs substantially

- Setting large-scale power generation ambitions that integrate geothermal into India's broader renewable capacity expansion framework

- Facilitating technology and knowledge transfer from geothermal-advanced nations, including the United States and the Philippines

The oil-and-gas well repurposing provision deserves particular attention. India's hydrocarbon sector has thousands of drilled wells, many of which have reached end-of-economic-life status. Retrofitting suitable wells for geothermal fluid extraction could dramatically reduce the capital intensity of early-stage development, because a significant portion of the exploration cost in conventional geothermal development is the drilling itself.

The Role of Advanced Subsurface Mapping

Running in parallel with the policy development is a data infrastructure initiative that could prove equally transformative. Project InnerSpace's GeoMap™ India tool, developed from 2023 onward, integrates more than 175 distinct data layers to produce high-resolution geothermal resource maps across the country. By combining geological, geophysical, geochemical, and infrastructure datasets, the tool identifies optimal development sites and prioritises candidates for coal plant-to-geothermal conversions.

The significance of this tool for de-risking early investment decisions should not be understated. Subsurface uncertainty is the primary reason private capital has historically avoided geothermal exploration. A data platform that meaningfully narrows that uncertainty before a drill bit enters the ground changes the investment calculus for developers and financiers alike.

Which Sectors Benefit Most From Geothermal Deployment?

The CEEW and Project InnerSpace report explicitly identified data centres, cities, and industrial operations as the primary demand sectors where geothermal energy can support rising energy needs while simultaneously reducing emissions and improving system resilience.

Data Centres: India's data centre capacity is expanding rapidly in response to cloud adoption, AI infrastructure investment, and digital economy growth. Data centres require continuous, uninterrupted power supply, a requirement that intermittent renewables cannot meet without substantial battery backup. Geothermal baseload generation is structurally well-matched to this demand profile, while geothermal cooling systems could reduce the considerable electricity load associated with conventional air conditioning in large facilities.

Industrial Heat Decarbonisation: The hard-to-abate industrial heat challenge is where geothermal's largest potential category, the more than 11,000 GW of industrial heat capacity, becomes most relevant. Sectors including chemicals, food processing, pharmaceuticals, and textiles that require sustained medium-temperature heat input could substitute geothermal thermal supply for the gas and coal combustion currently serving these processes. This aligns closely with broader renewable energy solutions being pursued across energy-intensive industries worldwide.

Urban Cooling and Grid Stress Management: India's urban heat island effect and rising ambient temperatures are driving an accelerating surge in air conditioning demand that threatens to overwhelm grid capacity during summer peak periods. Geothermal district cooling systems, already in operation in several international cities, could provide a low-carbon alternative and materially reduce electricity demand during exactly the periods when the grid faces its greatest stress.

The next major ASX story will hit our subscribers first

India in Global Context: A Sleeping Giant

To fully appreciate the scale of India's geothermal opportunity, it is worth positioning the country within the current global landscape.

| Country | Installed Geothermal Capacity | Key Development Factors |

|---|---|---|

| United States | ~3.7 GW | Mature regulatory framework, private investment |

| Indonesia | ~2.4 GW | Rich volcanic resources, state-backed development |

| Philippines | ~1.9 GW | Policy incentives, international financing |

| Kenya | ~0.9 GW | State exploration risk model, GDC structure |

| Iceland | ~0.75 GW | National energy identity, district heating integration |

| India (potential) | ~450 GW (estimated) | Policy nascent, exploration ongoing |

Kenya's Geothermal Development Company (GDC) model is widely cited as the most relevant international reference point for emerging geothermal markets. Under this structure, a state entity absorbs the highest-risk exploration phase, drilling confirmation wells and characterising reservoirs before transferring proven assets to private operators for commercial development. This approach directly addresses the capital barrier that has historically prevented private investment from entering the exploration stage.

Even realising just 5% of India's estimated 450 GW electricity potential would yield approximately 22.5 GW of installed geothermal capacity, placing India ahead of every country in the world except the United States in terms of installed geothermal power generation.

A Realistic Deployment Pathway: Phase by Phase

Translating technical potential into operational capacity requires a sequenced, realistic development pathway that manages risk at each stage.

Phase 1: Exploration and De-risking (2025 to 2028)

- Deep drilling confirmation campaigns at highest-priority sites including Puga, Tatapani, and the Cambay Basin

- Expansion of GeoMap™ India data coverage to reduce subsurface uncertainty across secondary priority regions

- Establishment of public risk-sharing mechanisms, potentially modelled on the Kenyan GDC structure, to attract private capital into the exploration stage

Phase 2: Pilot-to-Commercial Transition (2028 to 2032)

- First commercial-scale geothermal power commissioning at confirmed high-temperature sites

- Development of geothermal industrial heat networks within Gujarat's industrial zones

- Integration of geothermal cooling systems into high-heat-stress urban development projects

Phase 3: Scaled Deployment and Grid Integration (2032 to 2040)

- Potential to approach 10 GW of installed geothermal power capacity under sustained policy and investment conditions

- Nationwide expansion of lower-temperature direct-use applications across agriculture, aquaculture, and district heating

- Coal plant conversion projects leveraging existing grid connections and skilled workforces

The timing and scale of each phase will depend significantly on the depth of policy implementation, the pace of international technology transfer under the 2025 framework, and the degree to which public risk capital successfully mobilises private investment in the exploration stage. These are projections based on current policy settings and resource estimates, not guaranteed outcomes, and actual deployment timelines will be subject to geological, financial, and regulatory variables that are difficult to predict with precision.

Frequently Asked Questions: India Geothermal Potential

What is India's total geothermal energy potential?

India's technical geothermal potential is estimated at more than 11,000 GW for industrial heat, over 1,500 GW for cooling applications, and approximately 450 GW for electricity generation, according to a May 2026 report by Project InnerSpace and the Council on Energy, Environment and Water.

Which states in India have the highest geothermal potential?

The Project InnerSpace and CEEW report identified Gujarat, Uttar Pradesh, West Bengal, Telangana, Maharashtra, and Andhra Pradesh as leading states for geothermal deployment. The Himalayan belt, particularly Ladakh and Himachal Pradesh, and the SONATA fault zone in Chhattisgarh and Madhya Pradesh host the highest-temperature prospects suitable for power generation.

Does India have any operational geothermal power plants?

As of 2026, India has no major operational geothermal power plants. Development has remained at pilot-scale exploration and feasibility assessment, with Tatapani in Chhattisgarh at the planning stage for a 25 MW pilot project.

What is the National Policy on Geothermal Energy?

India's Ministry of New and Renewable Energy introduced the National Policy on Geothermal Energy in 2025. It is India's first dedicated regulatory framework for geothermal development, addressing oil and gas sector collaboration, well repurposing, large-scale power generation targets, and international technology partnerships.

How does geothermal energy compare to solar and wind in India?

Geothermal energy is not intermittent. It operates at capacity utilisation rates exceeding 80%, functioning as a baseload renewable source that delivers continuous output regardless of weather, season, or time of day, making it a direct complement to India's solar and wind portfolio rather than a competitor to it.

What are the main barriers to geothermal development in India?

The primary barriers have been high upfront exploration risk, limited subsurface characterisation data, the absence until 2025 of a dedicated policy framework, and a lack of institutional financing structures for early-stage drilling. The historical availability of low-cost coal power also reduced commercial incentives to pursue higher-risk geothermal investment. However, innovations such as direct lithium extraction and other advanced resource technologies demonstrate how rapidly the sector can evolve once policy and capital align.

The Strategic Verdict: Geothermal as India's Missing Energy Pillar

India's geothermal endowment is among the most underutilised strategic energy assets of any major economy. The confluence of a new national policy framework, improved subsurface mapping infrastructure, rising industrial energy demand, and international technology partnerships has created conditions for geothermal commercialisation that are more favourable than at any previous point in the country's history.

The sector's development will not happen automatically. It will require public risk capital for early-stage exploration, regulatory clarity and consistency for private developers, and deliberate integration of geothermal into India's industrial decarbonisation planning. The countries that have successfully scaled this resource share a common developmental thread: state-backed de-risking of the exploration phase followed by structured private sector participation in commercial development. Consequently, the clean energy transition pathway for India will be considerably stronger if geothermal is treated as a core pillar rather than an afterthought.

India geothermal potential of 450 GW for electricity generation alone is not a distant theoretical number. With the right institutional architecture and sustained commitment, it represents a credible pathway toward a form of clean energy that India's existing renewable portfolio simply cannot provide: firm, dispatchable, continuous power from beneath the ground on which the country's industrial economy already stands.

This article contains forward-looking statements, scenario projections, and capacity estimates derived from third-party research. These figures represent technical potential assessments and should not be interpreted as guaranteed outcomes. Energy development timelines and deployment scales are subject to geological, financial, regulatory, and policy variables. Readers should conduct independent research before making any investment or policy-related decisions.

Want to Stay Ahead of the Next Major Energy Minerals Discovery?

As India's geothermal sector moves from policy framework to commercial exploration, the demand for critical minerals underpinning clean energy infrastructure is accelerating — and significant ASX mineral discoveries don't wait for investors to catch up. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, turning complex geological data into actionable investment insights; explore historic discoveries and their exceptional returns to understand what's at stake, then start your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.