Indonesia's comprehensive approach to nickel ore pricing represents fundamental market structure transformation rather than temporary policy intervention, establishing new economic foundations for global battery metal supply chains through sophisticated resource management. As China demand and price trends continue to evolve, these changes reshape the strategic landscape for global battery materials.

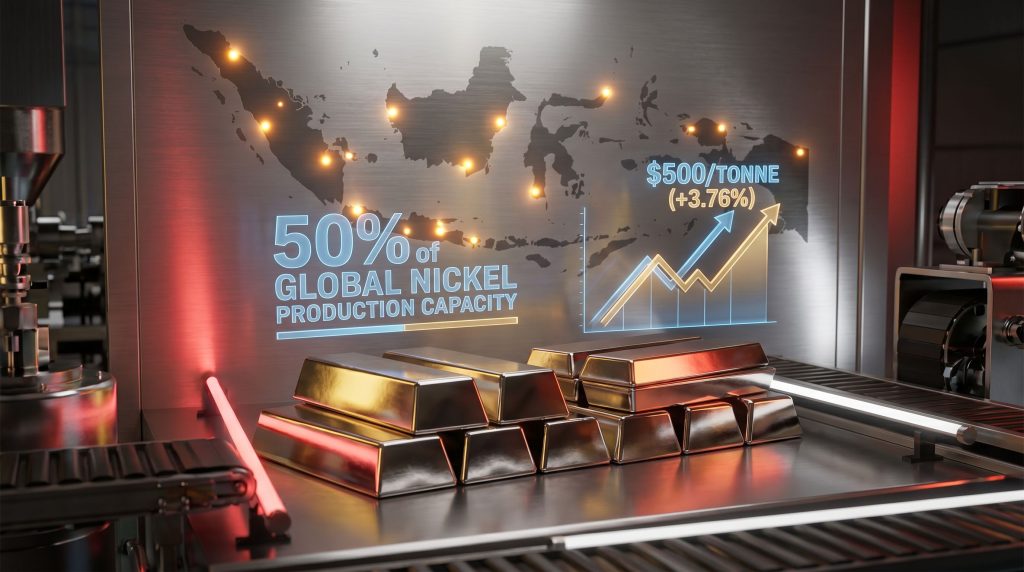

The archipelago nation, controlling approximately 50% of global nickel production capacity, has implemented enhanced mineral pricing mechanisms that transform pricing dynamics from reactive market responses to proactive value optimization. These Indonesia nickel ore pricing changes establish new economic foundations for global battery metal supply chains through systematic policy engineering rather than simple revenue maximization.

The Technical Architecture of Pricing Reform

The revised Harga Patokan Mineral (HPM) structure represents a multi-dimensional value capture system that fundamentally alters Indonesia's position from passive ore supplier to active price-setting authority. The Indonesian government increased the percentage of metal price included in the HPM calculation from 17% to 30% for nickel pig iron (NPI) production, representing a 76.5% relative increase in the metal price correlation coefficient.

More significantly, the framework now incorporates previously unmonetised byproduct streams, particularly cobalt revenues that historically accrued to producers at zero cost to ore suppliers. Industry analysis indicates that cobalt can represent 30% to 50% of total production revenue per pound, transforming this integration from minor adjustment to fundamental economic restructuring.

Enhanced HPM Formula Impact Analysis

| Production Method | Previous Structure | New Structure | Cost Impact |

|---|---|---|---|

| Nickel Pig Iron | 17% price correlation | 30% correlation + cobalt | +$500/tonne |

| HPAL Operations | Ore + $150/t sulfur | Ore + $1,000/t sulfur + HPM | +$11,000/tonne |

| Integrated Producers | Captive supply advantage | Maintained position | Minimal impact |

| Merchant Buyers | Market pricing | Premium pressure | +5-6% immediate |

According to industry analysis, these adjustments increase nickel pig iron production costs by nearly $500 per ton, translating to over $2,500 per ton for finished nickel. This represents approximately 3.76% cost escalation that establishes a new minimum price floor around $18,000 USD per tonne.

When big ASX news breaks, our subscribers know first

Economic Sovereignty Through Strategic Resource Control

Indonesia's pricing transformation demonstrates sophisticated understanding of resource economics and global supply chain leverage. The policy addresses historical value leakage where Indonesian miners received minimal premiums above production costs, particularly during periods of coordinated buyer pressure from Chinese purchasers seeking artificially depressed pricing.

The minimum ore price formula was originally established five to six years prior to address Chinese producers colluding to pay minimal premiums above cost. The recent enhancements represent evolution rather than revolution, building upon established policy frameworks that have demonstrated resilience through multiple commodity cycles.

Policy Coordination and Market Management

The Indonesian government employs dual mechanism strategy combining volume management through December ore quota announcements with enhanced pricing mechanisms. This coordination prevents market circumvention while establishing sustainable economic advantages for domestic producers. Volume quotas prevent supply flooding even as prices rise, while enhanced price floors ensure profit margins remain viable during commodity downturns.

This approach reflects permanent structural modification rather than temporary market intervention. The combination of volume restrictions and cost-based price support establishes new foundations for global nickel pricing while demonstrating governmental commitment to long-term value capture from strategic resource positioning.

Furthermore, the policy evolution demonstrates consistency and resolve through historical precedent. Indonesia previously implemented an ore export ban, initially withdrawing it due to insufficient downstream investment before successfully reinstating it. This pattern of policy persistence suggests current pricing mechanisms will maintain stability through market cycles and external pressure.

Technology-Specific Production Cost Analysis

Different nickel production technologies face varying degrees of cost pressure from Indonesia nickel ore pricing changes, creating fundamental shifts in global competitiveness rankings and operational viability. This transformation aligns with broader energy transition and critical minerals requirements driving demand for nickel.

HPAL Operations Under Severe Margin Compression

High-pressure acid leach facilities experience the most severe cost impacts due to multiple simultaneous pressures. Beyond the $2,500 per tonne increase from enhanced HPM pricing, HPAL operations face extraordinary sulfur cost inflation that has escalated from $150 per tonne to nearly $1,000 per tonne, representing approximately 567% inflation.

The combined $11,000 per tonne cost increase comprises:

- Enhanced HPM pricing: $2,500 per tonne

- Sulfur price escalation: $8,500 to $9,000 per tonne

- Geographic supply vulnerability: 75% Indonesian sulfur originates from Middle Eastern sources

This cost structure fundamentally alters HPAL economics that appeared attractive just two years prior when sulfur costs remained manageable and cobalt prices reached elevated levels. The combined pressures have pushed HPAL producers toward cost curve positions previously occupied by NPI facilities, eliminating historical competitive advantages.

Integration as Competitive Differentiation

Critical Cost Advantage Assessment

Vertically integrated operations with captive ore supplies experience minimal impact from HPM adjustments, as they avoid exposure to enhanced ore pricing while maintaining operational efficiency. This integration premium represents structural insulation from policy-driven cost shocks rather than temporary market advantage.

Tsingshan and other integrated producers demonstrate greater resilience compared to non-integrated HPAL operators who must purchase ore at elevated HPM prices. This dynamic shifts non-integrated producers rightward on the industry cost curve, creating permanent competitive disadvantage versus integrated competitors.

Nickel Pig Iron Operational Resilience

NPI production technology demonstrates superior adaptability to policy changes due to lower sulfur intensity requirements and established operational efficiency. The $500 per tonne cost increase represents manageable margin compression while maintaining competitiveness against alternative nickel sources globally.

The technology route benefits from reduced exposure to sulfur price volatility and simplified processing requirements that minimise vulnerability to input cost escalation. These characteristics position NPI producers favourably relative to processing-intensive alternatives during periods of elevated input costs.

Strategic Advantages for Western Development Projects

Indonesia nickel ore pricing changes create fundamental shifts in global nickel cost curves, repositioning Western projects from previously uncompetitive positions to potentially attractive investment opportunities through structural cost curve dynamics rather than absolute price improvements.

Cost Curve Repositioning Mechanics

As Indonesian marginal producers shift rightward on the global cost curve due to enhanced pricing mechanisms, Western projects previously considered economically unviable achieve competitive positioning without requiring commodity price increases beyond supply-demand fundamentals.

Western Project Competitive Advantages:

- Stable cost structures: Western projects maintain predictable operating costs while Indonesian costs increase

- Technology diversification: Alternative processing routes reduce exposure to sulfur price volatility

- Jurisdiction stability: Political and regulatory certainty provides long-term operational security

- Supply chain diversification demand: End-users increasingly seek non-Indonesian sources for strategic security

In addition, the current critical minerals strategy emphasises securing supply chains through geographic diversification, creating additional value for Western nickel projects.

Advanced-Stage Project Analysis

Canada Nickel's Metallurgical Innovation

Canada Nickel operates low-grade ultramafic deposits in Ontario's Timmins district, employing concentrate grade optimisation rather than ore grade maximisation strategies. The company's deposits produce concentrates at 25-30% nickel content versus typical 10-15% concentrates, creating processing efficiency advantages that offset lower ore grades through enhanced metallurgical recovery.

Talon Metals' Exceptional Mineralisation

Talon Metals demonstrates the opposite strategic approach through exceptional mineral grades showing over 5% nickel, 7% copper, and nearly 12 grams of platinum, palladium, and gold per tonne. These grades represent unprecedented mineralisation outside Russia's Norilsk district, providing natural hedge against commodity price volatility through diversified metal exposure.

Centaurus Metals' Commercial Readiness

Centaurus Metals approaches final investment decision with one million tonnes of contained nickel at approximately 1% grade and secured Glencore offtake arrangements. The company benefits from advanced permitting progress and established commercial relationships that enable rapid production response to improved price environments.

Magna Mining's Operational Integration

Magna Mining combines high-grade footwall development with operational experience from McCreedy West mine operations. The company's footwall deposits show 23% copper, 5% nickel, 21.4 g/t platinum, palladium, and gold, and 225.0 g/t silver over selected intersections, while operational experience provides realistic cost modelling with $100 per tonne mining costs and $200 per tonne all-in costs.

Market Dynamics Supporting Price Appreciation

Multiple supply and demand factors converge to support sustained nickel price appreciation beyond immediate policy impacts, creating conditions for extended price strength rather than temporary policy-driven increases. These dynamics reflect broader mining industry evolution trends affecting global resource markets.

Supply Constraint Fundamentals

Chinese nickel ore inventories have reached multi-year lows, typically indicating restocking requirements as seasonal Philippine supply patterns normalise. However, limited merchant ore availability outside Indonesia and the Philippines constrains supply response capabilities during restocking cycles.

The combination of Indonesian volume quotas implemented in December and enhanced pricing mechanisms creates dual pressure on global supply availability. This coordination demonstrates sophisticated market management rather than reactive policy intervention, suggesting sustainable supply constraint maintenance.

Merchant Ore Availability Assessment:

While limited ore supplies may emerge from Ivory Coast and other jurisdictions, total merchant ore volumes remain insufficient to offset Indonesian supply management. This structural limitation supports sustained price appreciation as buyers compete for constrained supply sources.

Demand Amplification Through Value Chain Dynamics

Historical patterns indicate structural nickel price increases trigger anticipatory purchasing throughout stainless steel and battery manufacturing value chains. This phenomenon creates demand amplification beyond fundamental consumption growth, potentially driving price momentum beyond equilibrium levels established by supply-demand balance.

The restocking dynamic contributed to double-digit demand growth during previous nickel price appreciation cycles, as value chain participants attempted to secure supply ahead of further cost increases. Current inventory depletion combined with enhanced price floors creates similar conditions for demand amplification.

Price Target Framework and Resistance Analysis

| Price Level (USD/tonne) | Technical Significance | Market Psychology |

|---|---|---|

| $18,000 | HPM floor / First royalty threshold | Established support base |

| $20,000 | Target based on cost analysis | High probability achievement |

| $21,000 | Second royalty activation | Moderate resistance expected |

| $25,000 | Historical peak consideration | Speculative upside scenario |

The current price structure provides minimal resistance until $21,000 per tonne, where the next Indonesian royalty threshold activates. This intermediate window creates favourable conditions for sustained price appreciation without triggering additional policy-based supply responses.

Long-Term Strategic Market Implications

Indonesia's nickel policy evolution establishes precedents for resource nationalism and value capture optimisation that may influence similar approaches across other critical mineral jurisdictions globally. This trend supports Australia's position in green metals leadership through stable jurisdiction advantages.

Resource Nationalism Template Development

The success of Indonesian pricing policy implementation provides a tested framework for other resource-rich nations seeking enhanced economic benefits from mineral endowments. Similar approaches may emerge in copper, lithium, and rare earth element jurisdictions as governments observe Indonesian value capture success.

This trend supports strategic arguments for supply chain diversification and domestic processing capacity development in consuming nations. The Indonesian model demonstrates how sophisticated resource management can achieve economic objectives while maintaining market competitiveness.

Technology Innovation Incentives

Enhanced ore pricing creates economic incentives for technological innovation in nickel processing, particularly for operations handling lower-grade or metallurgically complex ore types. Cost pressures may accelerate development of alternative processing technologies that reduce dependence on traditional HPAL or NPI production routes.

Furthermore, the policy framework also incentivises efficiency improvements and operational optimisation across existing facilities, potentially driving productivity gains that partially offset pricing impacts through technological advancement rather than cost absorption alone.

Geopolitical Supply Chain Reconfiguration

Indonesia nickel ore pricing changes occur within broader geopolitical contexts of critical mineral supply security and strategic resource competition. Western governments increasingly recognise nickel supply vulnerability and may accelerate domestic mining development support to reduce Indonesian dependence.

This dynamic creates policy alignment between Indonesian value maximisation and Western supply diversification objectives, potentially supporting sustained higher prices through reduced supply substitutability and increased strategic importance recognition. Industry reports suggest these policy changes benefit Western nickel companies significantly.

The next major ASX story will hit our subscribers first

Investment Strategy Framework for Nickel Exposure

Investors evaluating nickel market opportunities should prioritise cost curve positioning analysis rather than simple commodity price exposure, as structural changes create permanent competitive advantages for specific operational profiles.

Portfolio Positioning Through Cost Analysis

Strategic Investment Considerations:

- Integration assessment: Vertically integrated operations demonstrate superior resilience to policy-driven cost shocks

- Technology evaluation: Processing route selection impacts sensitivity to input price volatility

- Jurisdiction analysis: Political and regulatory stability affects long-term competitiveness sustainability

- Scale economics: Larger operations typically achieve better cost management and operational efficiency

Projects positioned on the left side of the revised global cost curve benefit disproportionately from Indonesia's price floor establishment and experience margin expansion rather than margin compression during policy implementation.

Market Timing and Entry Considerations

The current environment presents opportunities for strategic positioning in Western nickel assets before full price appreciation materialises in equity valuations. However, careful evaluation of individual project economics, development timelines, and financing requirements remains essential for successful investment outcomes.

Near-term catalysts include quarterly earnings from major producers, Chinese inventory data releases, and potential announcements of additional Indonesian policy measures. These events may create volatility providing tactical entry opportunities for strategic positioning.

Risk Management Framework:

Investors should balance upside exposure to nickel price appreciation with downside protection through diversified metal exposure, established offtake agreements, and operational flexibility during development phases.

Structural Transformation in Global Battery Metal Markets

Indonesia's comprehensive approach to nickel ore pricing represents fundamental market structure transformation rather than temporary policy intervention, establishing new economic foundations for global battery metal supply chains through sophisticated resource management.

The combination of enhanced pricing mechanisms, coordinated volume management, and sustained policy implementation creates permanent support for elevated nickel prices while providing competitive advantages to Western development projects in stable jurisdictions.

For market participants, understanding these dynamics provides essential context for long-term investment decisions in the evolving nickel landscape. The Indonesian framework demonstrates how resource-rich nations can achieve economic sovereignty through strategic mineral policy while maintaining global market competitiveness.

Investment Implications Summary:

The policy evolution rewards cost-competitive operations in stable jurisdictions while penalising high-cost, non-integrated producers dependent on Indonesian ore supply. This structural shift supports arguments for supply diversification and creates sustained value for projects positioned advantageously on the revised global cost curve.

The implications extend beyond immediate price impacts to encompass competitive positioning, technology development incentives, and geopolitical considerations in critical mineral supply chains. Recognition of these structural changes provides competitive advantage for investors capable of identifying projects benefiting from Indonesia's resource nationalism evolution.

This analysis is based on publicly available information and industry commentary as of April 2026. Readers should conduct independent research and consider professional advice before making investment decisions. Commodity markets involve significant risks including price volatility, regulatory changes, and operational challenges.

Ready to Capitalise on Major Nickel Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant nickel and battery metal discoveries across the ASX, turning complex geological announcements into actionable trading insights ahead of the broader market. Explore historic examples of how major mineral discoveries have generated exceptional returns, then begin your 14-day free trial to position yourself strategically in Australia's evolving critical minerals landscape.