June 3, 2026

The Invisible Tax on European Industry: How Energy Chokepoints Translate Into Metal Market Crises

Energy market analysts have long understood that the global industrial economy runs on a network of geographic pressure points. When those pressure points become contested, the consequences ripple outward in ways that rarely follow the linear paths that initial risk models project. Few disruptions illustrate this dynamic more clearly than the current Europe aluminium squeeze unfolding in the wake of the Strait of Hormuz closure, which has been in effect since February 28, 2026, following US-Israeli military action against Iran.

What makes this episode particularly instructive is the speed and severity of premium escalation. European aluminium markets have absorbed supply shocks before, but the simultaneous compression of energy flows, primary metal shipments, and raw material inputs has created a layered crisis that is structurally distinct from previous stress events. Understanding why requires examining how aluminium production works at a technical level, how Europe's domestic capacity arrived in its current diminished state, and what the forward curve is actually signalling about physical market conditions right now.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Matters More to European Aluminium Than Most Analysts Expected

The Strategic Chokepoint: A Primer on Global Energy and Metal Flow Dependency

The Strait of Hormuz is a narrow maritime corridor separating the Persian Gulf from the Gulf of Oman. At its narrowest point it measures roughly 21 nautical miles across, yet approximately 20% of globally traded oil and liquefied natural gas transits this passage daily, according to the US Energy Information Administration. The strategic concentration of energy exports through a single waterway has been a known vulnerability in global commodity markets for decades. What has become apparent over the past three months is that this vulnerability extends far beyond the crude oil markets most commonly associated with the strait.

For the European aluminium sector specifically, the transmission mechanism operates through two distinct channels. The first is the direct energy cost channel: when LNG flows are disrupted, European wholesale natural gas prices rise, which in turn pushes electricity generation costs higher across the continent. Aluminium smelters, which are among the largest electricity consumers in heavy industry, absorb these cost increases with unusual directness and speed.

The second channel is the supply chain channel: Gulf region smelters, which collectively supply approximately 20% of Europe's primary aluminium needs, simultaneously lose access to the energy they require to operate their own production facilities. The European metals energy squeeze compounds these pressures further, as pre-existing structural weaknesses amplify the impact of any new geopolitical disruption.

The compounding effect of both channels activating simultaneously is what distinguishes the current disruption from previous regional supply shocks. In past episodes, European buyers could often offset Gulf supply disruptions by sourcing from other regions or drawing down inventory. The current situation has removed that buffer option as both the supply and the energy underpinning European domestic production face simultaneous pressure.

Aluminium's Structural Vulnerability to Energy Price Spikes

Primary aluminium is produced through the Hall-Héroult electrolytic reduction process, which has remained essentially unchanged since its independent development by Charles Hall and Paul Héroult in 1886. The process dissolves alumina into a molten cryolite bath held at approximately 950-980 degrees Celsius and passes an electrical current through the melt to reduce aluminium ions to metallic aluminium.

The physics of this process cannot be optimised away: the International Aluminium Institute confirms that producing one tonne of primary aluminium requires approximately 14 to 15 megawatt-hours of electricity, compared with roughly 3 to 5 MWh for copper and 3 to 4 MWh for zinc.

This energy intensity has two critical implications for market dynamics. First, energy costs typically represent 30 to 40% of total cash costs for a primary aluminium smelter, making the metal far more sensitive to electricity price movements than competing base metals. Second, and less widely understood, aluminium potlines cannot be easily throttled back in response to high energy prices without risking catastrophic damage to the electrolyte bath.

If a potline is shut down rapidly or loses power unexpectedly, the molten cryolite can solidify around the carbon anodes, destroying the cell infrastructure and requiring extensive and expensive recommissioning before production can resume. This technical constraint explains why European smelter operators have historically faced a binary choice between operating at full capacity and accepting compressed margins, or undertaking full curtailments that can take six to twelve months to reverse.

As Fastmarkets senior analyst Andy Farida has noted, elevated energy prices are set to persist and could worsen if the Strait of Hormuz does not reopen soon, with Europe's summer restocking season creating additional upward pressure on already constrained supply conditions.

What Does Europe's Aluminium Supply Chain Actually Look Like?

Mapping Europe's Primary Aluminium Dependency

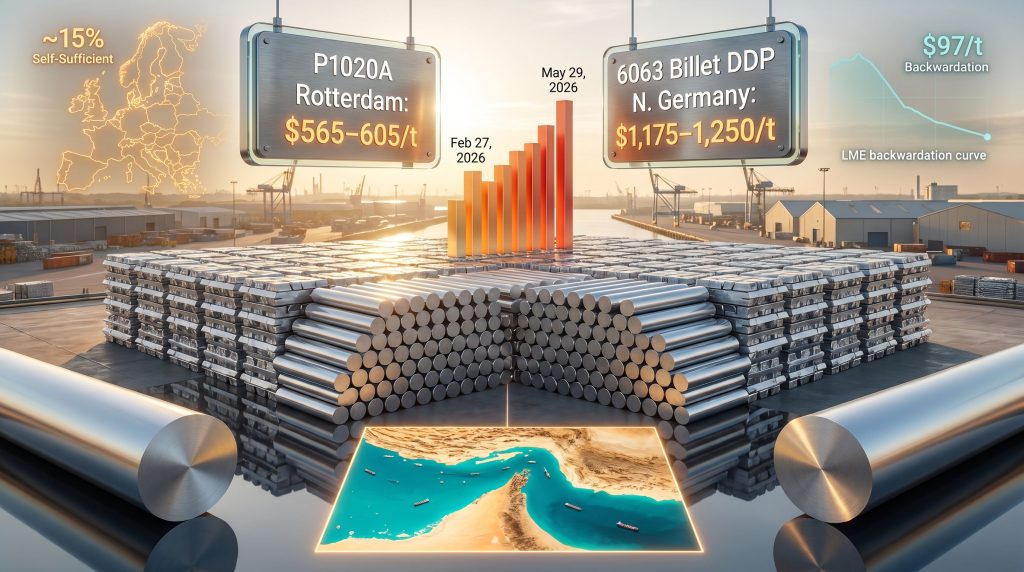

Europe's domestic primary aluminium production capacity has been systematically eroded over the past decade by a combination of high energy costs, carbon pricing pressures, and competition from producers in regions with cheaper and more stable electricity supply. According to data from the Foundation of European Aluminium (FACE), European smelters now produce only approximately 15% of the continent's internal primary aluminium requirements.

This structural import dependency means that European buyers are disproportionately exposed to disruptions in the global seaborne aluminium trade relative to consuming regions with stronger domestic production bases. Furthermore, the aluminium market pressures generated by US tariff policy have added another layer of complexity to an already strained procurement environment.

The geographic concentration of Europe's import exposure adds a further layer of vulnerability. Approximately 20% of European primary aluminium supply originates from Middle Eastern producers, according to Fastmarkets market data. These producers, clustered primarily around the Persian Gulf, depend on the same energy infrastructure that the Strait of Hormuz closure has disrupted. The result is that Europe faces a dual exposure: diminished domestic production capacity on one side, and reduced availability from its most structurally important import source on the other.

The Two-Way Bottleneck Effect: Metal Out, Raw Materials In

A dimension of the Strait of Hormuz disruption that has received less attention in general market commentary is its bidirectional impact on aluminium supply chains. The strait does not merely block outbound metal shipments from Gulf smelters to European buyers. It simultaneously disrupts the inbound flow of alumina, the refined aluminium oxide that serves as the primary feedstock for electrolytic reduction.

Gulf smelters are heavily dependent on seaborne alumina imports from Australia, Brazil, and Jamaica, all of which must transit the strait or navigate significantly longer alternative routes at substantially higher freight costs. This means that even smelters with sufficient domestic energy supply face constraints on raw material availability, creating a compounding supply reduction that goes beyond the direct energy cost impact. Smelters operating at reduced alumina availability are forced to curtail output not because they lack power but because they lack feedstock.

This dynamic helps explain why production losses across the Middle Eastern region have been so severe relative to what a pure energy cost analysis would predict. The structural implication of this two-way bottleneck is also critical for understanding recovery timelines. Even if the Strait of Hormuz were to reopen today, affected smelters could not immediately resume full output. Potlines that have been partially or fully curtailed require six to twelve months of controlled restart procedures before reaching rated capacity, meaning European buyers should not expect rapid premium normalisation even in optimistic geopolitical scenarios.

European Smelter Capacity: A Pre-Weakened Industrial Base

The European aluminium industry arrived at this crisis point from a position of pre-existing structural weakness. Multiple major smelters had already curtailed operations in previous energy price cycles, leaving the continent's domestic production base significantly below its historical peak.

| Smelter | Country | Status | Capacity Impact |

|---|---|---|---|

| Aldel | Netherlands | Offline since 2021 | Full curtailment |

| KAP (Uniprom) | Montenegro | Curtailed 2023 | Partial loss |

| Rheinwerk (Speira) | Germany | Shut 2023 | Full curtailment |

| San Ciprián (Alcoa) | Spain | Restarted, near full capacity | 228,000 tpa online |

The Alcoa San Ciprián smelter in Spain, which carries a capacity of 228,000 tonnes per year, offers a useful case study in the operational complexity facing European aluminium production. After curtailing output in 2021 due to high energy costs, the facility subsequently restarted and is now operating near full capacity. The smelter benefits from energy hedging arrangements extending through 2027 and is reportedly exploring longer-term power procurement options, illustrating how heavily dependent European smelter economics are on power contract structures rather than underlying generation cost competitiveness.

The secondary aluminium sector, which produces aluminium from recycled scrap rather than bauxite, might be expected to provide a buffer against primary supply disruptions. However, data reported by Massimo Grifone, commercial director at Cauvin Metals, indicates that recycled aluminium production in Germany fell by 3% in the first quarter of 2026. This confirms that even the less energy-intensive secondary production pathway is under pressure from high energy costs, compressed margins, and weak downstream demand.

How Has the Hormuz Disruption Reshaped Global Aluminium Supply?

The Middle Eastern Production Collapse: Scale and Timeline

The scale of the production disruption across Middle Eastern aluminium smelters has exceeded initial market estimates. According to Fastmarkets analysts, output from affected smelters in the region is projected at approximately 3.445 million tonnes in 2026, representing a decline of roughly 44% from the 6.151 million tonnes produced in 2025. This is an extraordinary volume reduction by any historical standard and positions 2026 as one of the most significant single-year supply contractions in the modern aluminium industry.

To contextualise this figure: global primary aluminium consumption typically runs at approximately 70 million tonnes per year. A 2.7 million tonne reduction from Middle Eastern producers alone represents roughly 3.9% of global annual consumption. When combined with curtailments from other affected facilities globally, the total supply shortfall is material enough to justify sustained premium escalation across multiple regional markets simultaneously.

Key Smelter Disruptions Across the Gulf and Beyond

The operational status of major Gulf aluminium producers reveals the breadth and depth of the supply disruption. Global aluminium producers have rarely faced such simultaneous and severe curtailments across a single region:

-

Alba (Bahrain): Operating at approximately 50% of rated capacity as of late April 2026, according to market sources cited by Fastmarkets. Alba is one of the world's largest single-site aluminium smelters with annual capacity exceeding 1.5 million tonnes, making its curtailment particularly significant for global supply balances.

-

Emirates Global Aluminium (EGA): Declared force majeure on select customer contracts on March 28, 2026. EGA operates two smelters in the UAE with combined capacity of approximately 2.6 million tonnes per year, making it one of the world's largest primary aluminium producers outside China.

-

Qatalum (Qatar): Operating at approximately 60% of rated capacity due to energy supply shortages as of March 12, 2026. Hydro, the Norwegian aluminium and energy company, holds a 50% stake in Qatalum, meaning this curtailment has direct implications for a major European aluminium producer's supply volumes.

-

Mozal (Mozambique): South32's Mozambique smelter was placed on care and maintenance on March 16, 2026, due to high energy costs, with reduced output confirmed in subsequent quarterly results. While geographically outside the Gulf, Mozal's curtailment reflects the wider global energy cost pressure emanating from the Hormuz disruption.

A trader source with direct market experience has described the current physical availability situation in stark terms, stating that market participants have never encountered such limited metal availability, with the typical pipeline of uncommitted tonnes simply absent from the market.

Alumina Supply Chains Under Simultaneous Pressure

The disruption to inbound alumina supply represents a compounding factor that standard supply disruption models often underweight. Gulf smelters depend on seaborne alumina imports to feed their reduction cells, with Australia representing the dominant supply source. Shipments from Australian refineries to Gulf smelters must navigate longer alternative routes in the absence of strait access, adding freight costs and transit time that reduce the effective economics of those supply routes.

For smelters already operating under compressed margins due to energy cost pressure, the additional burden of elevated alumina landed costs can push operations below the economic viability threshold even where power supply is technically available. Consequently, supply chain disruption risks that were previously considered tail risks have materialised simultaneously, creating a systemic challenge that procurement models had not adequately stress-tested.

What Is Happening to European Aluminium Premiums Right Now?

Rotterdam P1020A Premium: A Benchmark Under Pressure

The Rotterdam P1020A premium is the primary benchmark for physical aluminium availability in the European market. This assessment reflects the premium paid above the London Metal Exchange base price for standard grade primary aluminium available for prompt delivery into warehouse in Rotterdam, and serves as the reference point for physical purchase contracts across European industry.

Fastmarkets assessed the aluminium P1020A premium, in-warehouse delivered Rotterdam, at $565 to $605 per tonne on May 29, 2026. Three months earlier, on February 27, 2026, the same assessment stood at $360 to $390 per tonne. This represents a premium increase of approximately 55 to 60% over a three-month period, a pace of escalation that reflects genuine physical scarcity rather than speculative positioning. According to Reuters, the European aluminium billet premium effectively doubled following the supply disruption caused by the Iran war.

Extrusion Billet Premiums: The Downstream Indicator

Extrusion billet premiums provide a downstream signal about conditions in the value-added aluminium supply chain. The 6063 alloy extrusion billet is the primary feedstock for aluminium profile and tube manufacturing, feeding into construction, automotive, and consumer goods applications across European industry.

Fastmarkets assessed the aluminium 6063 extrusion billet premium, delivered duty paid to North Germany (Ruhr region), at $1,175 to $1,250 per tonne on May 29, 2026. On February 27, 2026, the equivalent assessment was $560 to $600 per tonne. The billet premium has therefore effectively doubled over the same three-month window during which P1020A premiums increased by 55 to 60%.

| Premium Benchmark | February 27, 2026 | May 29, 2026 | Change |

|---|---|---|---|

| P1020A Rotterdam (in-warehouse) | $360-390/t | $565-605/t | ~+55 to 60% |

| 6063 Billet DDP North Germany | $560-600/t | $1,175-1,250/t | ~+100% |

The more pronounced escalation in billet premiums relative to P1020A premiums reflects the additional supply chain complexity involved in billet production. Converting primary aluminium to extrusion billet requires alloying, casting, and homogenising steps that add further processing costs and create additional supply constraints beyond the availability of primary metal itself. The fact that billet premiums have returned to levels last seen during the 2022 European energy crisis is a significant reference point for understanding the severity of the current squeeze.

Backwardation as a Market Signal: What the Curve Is Telling Traders

At the time of Fastmarkets' most recent assessment, the LME cash-to-three-month aluminium spread registered a $97 per tonne backwardation, deepening from a $73 per tonne backwardation recorded just three days earlier on May 26, 2026. Backwardation, where prompt delivery prices exceed forward prices, is an unusual condition in aluminium markets that signals acute near-term physical scarcity.

As Andy Farida of Fastmarkets has explained, the market is effectively incorporating a short-term scarcity premium into the prompt price structure, even while the broader fundamental picture for aluminium further out along the forward curve remains more clearly understood and priced.

The nuance of backwardation as a market signal is worth elaborating for non-specialist readers. In a normal contango market structure, holding aluminium inventory is incentivised by a forward price that covers storage and financing costs. In backwardation, the opposite is true: holders of inventory are economically incentivised to sell into the prompt market rather than roll their positions forward. A trader source has noted that this backwardation dynamic will push suppliers, particularly those with trading rather than industrial holding strategies, to release volumes into the market. The implication is that sustained deep backwardation contains a partial self-correcting mechanism, but only insofar as discretionary inventory holders exist and choose to act on the economic signal.

Is Demand Holding Up, or Is the Squeeze Creating Its Own Demand Destruction?

The Demand Softening Signal: When High Prices Suppress Consumption

Premium escalation and supply tightness do not operate in isolation from demand dynamics. As physical aluminium premiums have surged, multiple market participants have reported a discernible softening in purchasing sentiment across European end-use sectors. The feedback loop operates through two channels simultaneously: elevated energy costs raise manufacturing input costs and compress the margins of downstream processors, while higher aluminium premiums increase raw material costs for fabricators and manufacturers who consume primary or semi-fabricated aluminium.

Fastmarkets analyst James Moore has articulated the demand destruction risk in terms of the cumulative burden being placed on manufacturing and consumer sectors, noting that prolonged energy crisis conditions force the absorption of higher fuel and metal prices alongside higher interest rates, progressively eroding both industrial capacity utilisation and end-consumer purchasing power. In addition, industrial decarbonisation pressures continue to compound the challenge, as manufacturers face simultaneous pressure to reduce emissions at a time when input costs are already elevated.

The Industrial Margin Compression Dynamic

The downstream implications of this dual cost pressure are visible across several European industrial sectors. Aluminium's three largest end-use segments in Europe are:

- Automotive (approximately 25 to 30% of European aluminium demand)

- Construction (approximately 25%)

- Packaging (approximately 20%)

Each of these sectors is experiencing its own demand-side pressure independent of aluminium input costs: automotive faces ongoing EV transition uncertainty and weakening consumer confidence, construction is constrained by high interest rates and reduced development activity, and packaging reflects subdued consumer spending. When elevated input costs are layered onto already-challenged end markets, the result is accelerated demand destruction that can transform a supply-side shock into a more prolonged market imbalance.

The German secondary aluminium data provides a concrete illustration of how this pressure is manifesting in the supply chain. Secondary aluminium production, which uses recycled scrap rather than virgin metal, is typically the lower-cost and more energy-efficient alternative that should see increased demand when primary aluminium becomes expensive and scarce. However, the 3% production decline in German recycled aluminium output during Q1 2026, reported by Cauvin Metals, indicates that even this lower-cost production pathway is not immune to the current combination of energy cost pressure and weak downstream demand.

Comparing Current Conditions to Previous European Aluminium Stress Periods

| Period | Primary Trigger | Premium Response | Demand Outcome |

|---|---|---|---|

| 2021-2022 Energy Crisis | European gas price spike | Premiums surged to record highs | Demand curtailed; multiple smelters closed |

| 2023 Smelter Curtailments | Sustained high energy costs | Premiums elevated but gradually easing | Gradual demand recovery as energy stabilised |

| 2026 Hormuz Disruption | Geopolitical energy and supply shock | Billet premiums back at 2022 levels | Demand softening; sentiment cautious |

The parallels with the 2021-2022 energy crisis are instructive but incomplete. That episode was driven primarily by European gas price escalation following reduced Russian pipeline flows. The current disruption shares the energy cost component but adds the additional dimension of direct Middle Eastern primary aluminium supply loss. In 2022, Gulf producers generally continued to operate and could partially offset European domestic supply losses. Today, those same Gulf producers are among the most severely curtailed operations in the global market. Fastmarkets has reported extensively on how the Strait of Hormuz closure is simultaneously fuelling supply concerns across both European and US aluminium markets.

The next major ASX story will hit our subscribers first

What Are the Scenarios for Resolution, and How Long Could This Last?

Scenario Modelling: Three Pathways for the Strait of Hormuz and European Aluminium

Scenario 1: Rapid Resolution (0 to 3 months)

If the Strait of Hormuz were to reopen in the near term, the initial market response would likely involve some premium compression as physical supply anxiety eased. However, the structural reality of smelter restart timelines means that actual metal availability would recover only gradually. With six to twelve months required to bring curtailed potlines back to rated capacity, a prompt geopolitical resolution would not translate into a prompt supply resolution. European premiums would likely ease from current peaks but remain elevated through the remainder of 2026.

Scenario 2: Prolonged Disruption (3 to 9 months)

A continued closure deepens the structural European aluminium deficit through the restocking season and into the autumn. Additional European smelter curtailments become increasingly probable as energy costs remain elevated during the peak summer consumption period. Premium levels would be expected to hold near current levels or escalate further, particularly if restocking demand arrives simultaneously with ongoing supply constraints. Demand destruction accelerates across exposed manufacturing sectors.

Scenario 3: Extended Geopolitical Realignment (9 or more months)

A prolonged or permanent disruption triggers structural rerouting of Middle Eastern aluminium export flows through alternative maritime corridors. European buyers would be compelled to secure long-term supply agreements with producers in Australia, Canada, and Norway, reshaping the geographic architecture of European aluminium procurement. This scenario involves structural premium repricing and potential acceleration of renewable energy investment by European smelter operators seeking to insulate their competitiveness from Middle Eastern geopolitical risk.

The Summer Restocking Season as a Near-Term Pressure Amplifier

A timing consideration that deserves specific attention is the intersection of current supply constraints with the European industrial restocking cycle. European aluminium buyers and fabricators typically build inventory ahead of the summer period, during which many processing facilities undertake scheduled maintenance shutdowns. This seasonal demand increase is arriving into a market where physical supply availability is already critically constrained.

The combination of cyclical restocking demand and structural supply deficit creates conditions where premiums could escalate further before any supply-side relief materialises, irrespective of geopolitical developments.

What Should European Aluminium Buyers, Manufacturers, and Investors Monitor?

Key Indicators to Track for Market Direction

Participants navigating the current Europe aluminium squeeze should prioritise monitoring the following indicators:

-

Strait of Hormuz transit status: Any change in geopolitical conditions affecting maritime access will represent the primary catalyst for a premium direction shift, though the supply lag means the effect on physical availability will be delayed.

-

Gulf smelter operating rates: Published reports on Alba and EGA capacity utilisation serve as leading indicators of Middle Eastern supply recovery, with any movement above current levels (approximately 50% and force majeure respectively) signalling early-stage normalisation.

-

LME cash-to-three-month spread: The depth and direction of backwardation provides real-time insight into physical market tightness. Narrowing backwardation would signal easing near-term scarcity even before premium benchmarks respond.

-

Rotterdam P1020A premium weekly assessments: The primary benchmark for European physical market conditions and the most directly relevant pricing reference for industrial buyers.

-

European natural gas and electricity forward curves: As the structural cost floor for any European smelter restart, energy price movements will determine whether curtailed domestic capacity becomes economically viable to bring back online.

-

Alumina spot price and freight rates: As a leading indicator of smelter operating economics across the Gulf region, alumina availability and cost signal whether raw material constraints are easing independently of energy supply conditions.

Strategic Considerations for Industrial Buyers

European manufacturers and fabricators with significant aluminium input requirements face a range of strategic decisions in the current environment:

-

Hedging strategy in backwardated markets: Purchasing forward cover in a backwardated market involves paying a premium relative to the spot price curve. Buyers must weigh the cost of forward hedges against the risk of further spot premium escalation, a calculation that depends heavily on individual inventory positions and contract pricing structures.

-

Supply diversification: Accelerating the diversification of primary aluminium sourcing away from Gulf-dependent supply chains represents a medium-term structural response. Norwegian producers (Hydro's Norwegian smelters), Canadian producers, and Australian primary metal are the primary alternative supply pools. Lead times for establishing new supply contracts and logistics arrangements typically range from three to six months.

-

Secondary aluminium substitution: Where alloy specifications permit, increasing the proportion of recycled aluminium content in manufacturing inputs can partially offset primary supply constraints. The caveat is that German secondary production data confirms that secondary supply is itself under pressure, limiting the substitution potential.

-

Demand-side hedging: Some downstream manufacturers have begun passing aluminium cost increases through to end customers via surcharge mechanisms or price escalation clauses in supply contracts, effectively transferring a portion of the premium risk to end buyers.

Frequently Asked Questions: Europe Aluminium Squeeze and the Strait of Hormuz

Why is the Strait of Hormuz so important to European aluminium supply?

The Strait of Hormuz functions as a critical energy and commodity corridor through which approximately 20% of global oil and LNG flows transit daily. For European aluminium, the strait creates a dual exposure: it is the transit route for metal shipments from Gulf producers who supply approximately 20% of Europe's primary aluminium, and it carries the energy that powers those same Gulf smelters. Disruption to the strait therefore simultaneously constrains both the supply of finished metal to Europe and the production capacity of the region's most important aluminium manufacturing cluster.

How much have European aluminium premiums increased since the disruption began?

Rotterdam P1020A premiums rose approximately 55 to 60% between February 27 and May 29, 2026, moving from $360 to $390 per tonne to $565 to $605 per tonne. Over the same period, extrusion billet premiums in northern Germany effectively doubled, rising from $560 to $600 per tonne to $1,175 to $1,250 per tonne, returning to levels last seen during the 2022 European energy crisis.

What is backwardation in aluminium markets and what does it signal?

Backwardation describes a market structure in which the price for immediate or near-term delivery exceeds the price for delivery in future months. In normal market conditions, aluminium trades in contango, where forward prices are higher than spot prices to reflect storage and financing costs. Backwardation signals that demand for prompt physical metal is outpacing available near-term supply, indicating genuine physical market tightness. The current cash-to-three-month backwardation of $97 per tonne, deepening from $73 per tonne just days earlier, represents a meaningful scarcity signal in a market where backwardation is historically unusual.

Which Middle Eastern aluminium smelters have been most affected?

The most significantly impacted facilities include Bahrain's Alba, operating at approximately 50% of rated capacity as of late April 2026; Emirates Global Aluminium in the UAE, which declared force majeure on select contracts on March 28, 2026; and Qatalum in Qatar, operating at approximately 60% of rated capacity due to energy shortages as of March 12, 2026. South32's Mozal smelter in Mozambique was placed on care and maintenance on March 16, 2026 due to the wider global energy cost impact.

How long will it take for aluminium supply to recover if the Strait reopens?

Even in the most optimistic geopolitical scenario, Fastmarkets analysts project a six to twelve month recovery timeline for affected smelter output. This reflects the technical requirements of recommissioning aluminium potlines following curtailment, during which electrolyte baths must be carefully restored to operating temperature and electrical flow before full production capacity can be achieved. Supply recovery will therefore substantially lag any geopolitical resolution.

What industries in Europe are most exposed to the aluminium supply squeeze?

The four most significantly exposed European end-use sectors are automotive manufacturing, construction and infrastructure, aerospace and defence, and packaging. Automotive is among the largest consumers of both primary aluminium and extruded billet for vehicle structural components and body panels. Construction uses aluminium extensively in window frames, facades, and structural profiles. Aerospace depends on high-specification aluminium alloys for structural applications. Packaging, particularly beverage can production, consumes large volumes of aluminium sheet. Each of these sectors faces the compounding pressure of higher aluminium input costs at a time when their own end-market demand conditions are already challenged.

Conclusion: A Structural Stress Test for European Industrial Supply Chains

The Convergence of Geopolitical, Energy, and Industrial Risk

The Europe aluminium squeeze currently unfolding represents a qualitatively different challenge from previous supply stress events. The 2021-2022 European energy crisis was primarily a gas price phenomenon that affected domestic smelting economics. The 2023 curtailment cycle was a continuation of that energy cost pressure. The current disruption combines a major external geopolitical supply shock with pre-existing domestic production weakness and a cyclical demand environment that offers limited absorptive capacity. The three layers of pressure are not merely additive but interact in ways that amplify each individual component.

The data points are unambiguous. A 44% projected decline in Middle Eastern smelter output. Rotterdam premiums up 55 to 60%. Billet premiums doubled. LME backwardation deepening to $97 per tonne. German secondary production contracting even in the supposedly more resilient recycled segment. Each of these indicators individually would warrant attention. Together, they describe a physical market under exceptional strain.

The Path Forward: Supply Diversification as a Strategic Imperative

The structural lesson of this disruption is that European aluminium supply chains carry a geographic concentration risk that has been consistently underpriced in historical procurement strategies. The over-reliance on Gulf producers for approximately 20% of primary aluminium supply, combined with a structurally weakened domestic production base, has left European industrial consumers with limited options when that import channel is disrupted.

The strategic response requires action at multiple levels. Individual buyers need to accelerate supply chain diversification toward producers in lower-risk geographies including Norway, Canada, and Australia. The broader European industrial policy framework needs to confront the structural economic question of whether the continent's aluminium smelting capacity can be maintained at a scale sufficient to provide meaningful domestic supply security.

The longer this disruption persists, the more likely it is to accelerate structural shifts in European aluminium procurement architecture that outlast the immediate geopolitical trigger. Whether those structural shifts ultimately strengthen or further erode Europe's industrial supply resilience will depend substantially on decisions being made by procurement teams, energy policymakers, and investment committees over the next twelve to eighteen months.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Commodity market conditions, geopolitical developments, and price assessments described herein reflect information available at the time of publication and are subject to rapid change. Readers should conduct their own due diligence and consult qualified advisers before making investment or procurement decisions. Forward-looking statements and scenario projections involve inherent uncertainty and should not be relied upon as predictions of future outcomes.

Further Exploration: Readers seeking ongoing price data and market analysis on European aluminium premiums and supply chain conditions may find value in exploring commodity intelligence resources such as Fastmarkets, which publishes regular price assessments and analytical commentary across aluminium and base metals markets.

Want to Track the Next Major Commodity Disruption Before the Market Prices It In?

When geopolitical shocks compress supply chains and reshape metal markets at speed, early awareness is everything. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex commodity data into actionable opportunities for both short-term traders and long-term investors. Start your 14-day free trial with Discovery Alert today, or explore how historic discoveries have generated extraordinary returns on the Discovery Alert discoveries page.