How Much Rebar Does Mexico Produce and Consume?

Mexico's steel industry experienced a notable rebound in May 2025, with rebar production reaching 1.65 million tonnes, marking a significant 27% increase from April's 1.30 million tonnes. This recovery demonstrates the resilience of Mexico's steel sector despite facing various economic challenges throughout the year.

Domestic consumption followed a similar trajectory, climbing to 1.60 million tonnes in May 2025, representing a robust 29% month-over-month growth from April's 1.24 million tonnes. However, despite this impressive monthly recovery, year-over-year figures tell a different story, with consumption declining by 3.3% compared to May 2024.

The Mexican steel association CANACERO's data reveals a pattern of volatility in the market, characterized by strong monthly rebounds counterbalanced by longer-term downward pressure. This dichotomy suggests that while immediate market conditions have improved, structural challenges remain.

Industry Insight: Despite declining construction activity trends, Mexican rebar production and demand managed a significant recovery on a monthly basis compared to April 2025. This suggests temporary environmental or financial impacts rather than long-term industry collapse. The ability of the sector to rebound so quickly indicates underlying strength in Mexico's steel manufacturing capacity.

Rebar Production and Consumption Trends

The monthly production surge of 27% demonstrates the Mexican steel industry's manufacturing flexibility and ability to quickly respond to market demands. Production facilities ramped up operations significantly from April to May, suggesting either a clearing of previous production backlogs or anticipation of improved market conditions.

Similarly, the 29% month-over-month increase in consumption indicates renewed activity among construction companies and steel buyers. This consumption spike, occurring despite seasonal challenges, points to either delayed projects finally moving forward or strategic inventory building by construction firms ahead of anticipated price changes.

What Drives Fluctuations in Mexico's Rebar Industry?

The fluctuations in Mexico's rebar industry stem primarily from construction sector performance, which according to the National Institute of Statistics and Geography (INEGI) experienced a 2.7% year-over-year decline in April 2025. This contraction in construction activity stands in stark contrast to the broader Mexican economy, which grew by 1.4% during the same period.

Two principal factors have created these market conditions: adverse weather and financial constraints. As a Mexico-based distributor told Fastmarkets, "Between June and September, there is heavier rainfall in the region, which complicates construction, so I believe this market is likely to remain calm." This weather-related insight helps explain the seasonal challenges facing the construction sector.

Credit availability represents another significant constraint. The same market participant noted that "credit is tight," reflecting the financial difficulties facing construction companies and developers. This credit squeeze has restricted cash flow throughout the construction supply chain, ultimately impacting rebar demand.

Monthly Rebound in Production & Demand: Understanding the Factors

The sharp monthly recovery in both production (27%) and consumption (29%) likely stems from a combination of factors:

- Seasonal adjustment: April typically experiences lower production levels, with May representing a normalization period

- Inventory replenishment: Distributors and end-users restocking after depleting inventories

- Project timing cycles: Construction projects advancing to steel-intensive phases

- Weather windows: Brief improvements in weather conditions enabling construction progress

Despite these monthly gains, the persistent year-over-year decline indicates that fundamental economic challenges continue to weigh on the sector. The construction industry's underperformance relative to Mexico's broader economic growth reflects sector-specific challenges rather than a general economic downturn.

How Are Mexican Rebar Prices Positioned in the Americas?

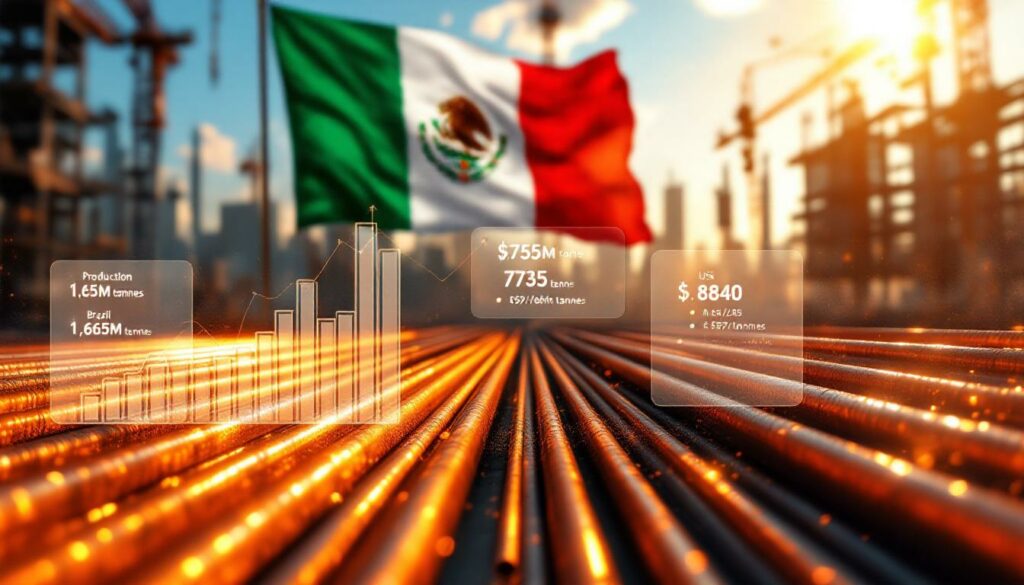

Mexico established its position in the regional rebar market with its inaugural Fastmarkets price assessment at $735 per tonne in late June 2025. This pricing positions Mexican rebar strategically between its major regional competitors: higher than Brazilian offerings but below U.S. prices.

This mid-tier pricing reflects Mexico's unique position in the Americas steel market—balancing competitive production costs with proximity advantages to North American markets. As Fastmarkets noted, Mexican rebar is "positioning itself below US levels, but above Brazil, amid stable, but cautious market fundamentals."

Initial Price Levels and Benchmarking

The pricing landscape across the Americas reveals distinct market conditions in each country:

| Region/Country | June 2025 Rebar Price | Price Unit |

|---|---|---|

| Mexico | $735 | per tonne |

| Brazil | $597–$639 | per tonne |

| United States | $840 | per short ton |

Brazil's lower pricing ($597-639 per tonne, converted from 3,310-3,540 Reais) reflects its challenging domestic construction market conditions and competitive export positioning strategy. The more aggressive pricing stems from Brazil's need to stimulate demand in a stagnant construction environment.

In contrast, U.S. rebar commands a premium at $840 per short ton (approximately $926 per metric tonne), supported by restricted imports and domestic supply constraints rather than robust end-user demand. This pricing disparity creates both challenges and opportunities for Mexican producers navigating regional trade dynamics.

Market Positioning Analysis: Mexico's intermediate price point creates a compelling value proposition, particularly for North American buyers seeking alternatives to higher-priced U.S. material. The $735 per tonne price point represents a strategic balance—maintaining profitability while remaining competitive against both higher-cost U.S. production and lower-cost Brazilian exports.

What Are the Latest Export Trends for Mexican Rebar?

Mexico's rebar exports reached 59,000 tonnes in May 2025, representing an 11.3% increase from April's 53,000 tonnes. However, this monthly gain occurs against a backdrop of year-over-year decline, with exports falling 15.3% compared to May 2024's 69,000 tonnes.

This export pattern mirrors the domestic consumption trend—showing short-term recovery amid longer-term pressure. The divergence between monthly and annual performance metrics suggests that while immediate export conditions have improved, structural challenges to Mexico's export competitiveness persist.

Analysis of Export Volumes & Primary Markets (2025)

The United States continues to dominate as Mexico's primary export destination, accounting for 73.9% of all Mexican steel exports. This heavy dependence on the U.S. market creates both opportunities and vulnerabilities for Mexican producers. While proximity offers logistical advantages, reliance on a single market exposes exporters to US–China trade war impact and economic fluctuations.

Canada and Colombia represent Mexico's second and third largest export markets, accounting for 4.6% and 2.9% of exports respectively. These secondary markets, while currently modest in volume, offer diversification potential as Mexican exporters seek to broaden their customer base.

The Effect of Nearshoring on Export Trade Routes

Market participants in Mexico have noted an emerging shift in export patterns, with some rebar originally destined for the U.S. market being redirected to Canada or other Latin American countries. This reorientation reflects evolving trade dynamics influenced by nearshoring trends—where companies relocate production closer to end markets.

Several factors drive this export diversification:

- Efforts to reduce dependence on the volatile U.S. market

- Development of alternative trade relationships to mitigate policy risks

- Strategic positioning to capitalize on infrastructure development in emerging Latin American markets

- Optimization of logistics networks to improve delivery times and reduce transportation costs

This gradual export diversification represents a strategic adaptation by Mexican producers to changing regional market conditions and tariffs and investments.

What Factors Influence Mexico's Wire Rod Sector in Comparison to Rebar?

Mexico's wire rod sector, while closely related to rebar production, shows distinct performance patterns. Wire rod production reached 989,000 tonnes in May 2025, experiencing a 23.8% month-over-month increase from April's 799,000 tonnes. This robust monthly growth parallels rebar's recovery pattern, suggesting similar short-term market dynamics affecting both products.

However, wire rod consumption reveals a more pronounced year-over-year decline than rebar. Wire rod consumption reached 1.03 million tonnes in May 2025, representing a 4.6% year-over-year decrease compared to rebar's 3.3% decline. This larger contraction indicates potentially different end-market conditions or application-specific challenges.

Comparative Production Overview (Wire Rod vs. Rebar)

Both wire rod and rebar demonstrated strong monthly recoveries in May 2025, but with subtle differences in performance metrics:

| Product | May Monthly Growth (%) | Annual Decline (%) |

|---|---|---|

| Rebar | +27% (production); +29% (consumption) | Production: -1.5%; Consumption: -3.3% |

| Wire Rod | +23.8% (production); +24.2% (consumption) | Production: -0.2%; Consumption: -4.6% |

This comparative data reveals that while both products face similar market pressures, wire rod production has been slightly more resilient on an annual basis (-0.2% vs. rebar's -1.5%), while its consumption has contracted more significantly (-4.6% vs. rebar's -3.3%).

The difference likely stems from the products' distinct end-use applications—rebar primarily serves structural reinforcement in concrete construction, while wire rod feeds into diverse manufacturing applications including mesh, nails, springs, and other fabricated products. This end-use diversity creates different demand dynamics despite the products sharing similar production processes and raw material inputs.

How Does the Mexican Steel Market Compare Regionally (Brazil & US Case Studies)?

The Mexican steel market operates within a diverse regional landscape, positioned between Brazil's struggling domestic market and the supply-constrained U.S. environment. These contrasting conditions create both challenges and opportunities for Mexican producers navigating regional trade flows.

Brazil's Steel Market Dynamics

Brazil's rebar market has experienced persistent downward price pressure, with domestic prices ranging from $597-639 per tonne (3,310-3,540 Reais). This pricing weakness stems from fundamental domestic economic challenges, particularly in the construction sector.

A Brazilian distributor provided stark insight into market conditions, telling Fastmarkets: "The market is paralyzed. With interest rates where they are, no one is going to buy rebar like it's cement. Credit is tight, the sector is insecure and the government needs to take more steps to build investor confidence."

This assessment highlights several critical factors suppressing Brazil's steel demand:

- High interest rates restricting investment and financing

- Tight credit conditions limiting purchasing power

- Low market confidence inhibiting project commitments

- Insufficient government action to stimulate construction activity

United States Steel Market Challenges

In stark contrast to Brazil's declining prices, U.S. rebar prices have strengthened to $840 per short ton, despite what market participants describe as "lackluster demand." This price strength stems primarily from supply-side constraints rather than robust consumption.

As a U.S.-based trader explained to Fastmarkets: "[Domestic] supply [in the US] is quite tight despite continuing lackluster demand because imports are exceptionally challenging and mostly absent [right now]." This insight reveals that U.S. price increases reflect restricted supply rather than demand strength—a fundamentally different market dynamic than Brazil's demand-driven price weakness.

The U.S. market's supply constraints stem from:

- Import restrictions limiting foreign competition

- Mill-led price initiatives in a concentrated domestic market

- Production discipline among U.S. manufacturers

- Logistics and transportation constraints affecting material flow

Regional Market Contrast: Mexico occupies a strategic middle ground between Brazil's demand-constrained market and the U.S.'s supply-constrained environment. This positioning allows Mexican producers to potentially capitalize on both dynamics—offering competitive alternatives to high-priced U.S. material while maintaining premium positioning relative to Brazilian exports.

What Are Future Projections & Opportunities for Mexico's Rebar Industry?

While the available market data focuses primarily on current conditions rather than forward projections, several factors will likely influence Mexico's rebar industry moving forward. The industry faces both challenges and opportunities that will shape its trajectory.

Potential Growth Drivers

The Mexican rebar sector could benefit from several potential developments:

- Infrastructure investment: Government-sponsored infrastructure programs could stimulate construction activity and steel demand

- Housing development: Residential construction represents a key consumption segment for rebar

- Export market diversification: Expanding beyond U.S. dependence to serve growing Latin American markets

- Manufacturing growth: Mexico's industrial expansion driving construction of new facilities

Risks to Watch

Several factors pose ongoing challenges to Mexico's rebar market:

- Seasonal weather patterns: As noted by industry participants, the June-September rainy season traditionally hampers construction activity

- Credit availability: Tight financial conditions restrict project development and material purchasing

- Competition from imports: Lower-priced imports from countries like Brazil may pressure domestic producers

- U.S. market volatility: Dependence on U.S. exports creates vulnerability to policy and economic changes

Recommended Strategies for Industry Stakeholders

Based on current market conditions, several strategic approaches may benefit industry participants:

- Geographic diversification: Reducing dependence on any single export market

- Price positioning optimization: Maintaining competitive advantage between U.S. and Brazilian price points

- Value-added services: Enhancing offering beyond base products to improve margins

- Supply chain efficiency: Improving logistics to reduce costs and delivery times

The iron ore trends and iron ore forecast will undoubtedly play a significant role in determining production costs and, subsequently, pricing strategies for Mexican rebar producers. Furthermore, the commodity price impact on raw materials will continue to influence the competitiveness of Mexican steel products in regional markets.

FAQ: Mexican Rebar Market Insights

What is the current price level of Mexican rebar?

As of June 2025, Mexican rebar was assessed at approximately $735 per tonne according to Fastmarkets' inaugural price assessment. This positions Mexican rebar at a mid-range price point in the Americas market—above Brazilian levels but below U.S. prices.

Why did Mexican rebar consumption decline year-over-year despite the recent monthly surge?

The year-over-year decline in rebar consumption (3.3%) reflects broader challenges in Mexico's construction sector, which contracted by 2.7% according to INEGI data. This construction slowdown stems from a combination of adverse weather conditions and tight credit availability restricting project development. The monthly surge (29%) likely represents a temporary recovery from even more depressed April levels rather than a reversal of the longer-term trend.

What influences the monthly price publication schedule for Mexican rebar?

Fastmarkets' price assessments follow a structured schedule that can be affected by market holidays and significant events. For example, the U.S. Independence Day holiday may occasionally shift assessment timing. Market participants rely on these assessments for contract negotiations and strategic planning, making the publication schedule an important consideration for industry stakeholders.

How do weather patterns affect Mexico's rebar market?

According to industry participants, Mexico experiences a rainy season between June and September that "complicates construction." This seasonal weather pattern creates a recurring challenge for construction activities, potentially suppressing rebar demand during these months regardless of other economic factors. Construction schedules often account for these weather patterns, affecting the timing of rebar purchases and project execution.

What is the relationship between construction activity and rebar demand in Mexico?

The 2.7% year-over-year decline in construction activity correlates closely with the 3.3% reduction in rebar consumption, demonstrating the direct relationship between these metrics. Rebar serves as a primary material in reinforced concrete construction, making its consumption a key indicator of construction sector health. This tight correlation means that economic factors affecting construction activity directly impact rebar demand, as confirmed by recent consumption data from Mexico.

Are You Following Critical Market Trends in Mining and Commodities?

Stay ahead of the next major mineral discovery with Discovery Alert's proprietary Discovery IQ model, delivering real-time notifications on significant ASX mineral discoveries and turning complex market data into actionable insights. Explore historic examples of exceptional investment returns on our dedicated discoveries page and position yourself for success in the commodities market.