Understanding Mine-to-Market Graphite Strategy

The mine-to-market graphite strategy represents a comprehensive approach to the graphite value chain where companies control every stage from resource extraction through processing to final product delivery. This vertical integration model allows businesses to maximize value while addressing critical vulnerabilities in graphite supply chains that have become increasingly important in global commerce and defense.

Rather than focusing solely on mining or processing, integrated companies manage the entire production journey, creating resilience against market fluctuations and geopolitical risks while capturing value at multiple stages of production. As the mining industry evolution continues to accelerate, companies pursuing vertical integration are positioning themselves advantageously.

Key Components of Vertical Integration

The foundation of successful vertical integration in the graphite sector includes several essential elements:

- Resource ownership and extraction: Securing high-quality graphite deposits with favorable geology and mining conditions

- Primary processing facilities: Establishing capabilities to convert raw ore to graphite concentrate through flotation and classification

- Advanced processing capabilities: Developing specialized equipment to transform concentrate into value-added products

- Market access and distribution: Creating direct channels to end-users in battery, industrial, and defense sectors

- Strategic geographical positioning: Locating facilities to optimize logistics costs and market access across multiple regions

Benefits of the Integrated Approach

Companies pursuing mine-to-market strategies realize several competitive advantages:

- Supply chain security: Significantly reduced dependence on external suppliers, particularly from geopolitically sensitive regions

- Value addition: Ability to capture margins across multiple production stages rather than just one segment

- Quality control: Maintaining consistent standards from mine site through to final customer delivery

- Market responsiveness: Enhanced capacity to adapt production specifications to evolving customer requirements

- Strategic positioning: Reduced vulnerability to trade disruptions, export controls, and other geopolitical factors

Why is Graphite a Critical Strategic Mineral?

Graphite has emerged as an essential resource for advanced economies due to its irreplaceable role in several high-growth technologies. Its designation as a critical mineral by numerous governments reflects both its strategic importance and the concentrated nature of global supply chains.

The mineral's unique properties—electrical conductivity, thermal stability, and lubricity—make it indispensable for applications ranging from battery anodes to defense systems, with demand growth significantly outpacing other industrial minerals. Furthermore, graphite plays a crucial role in the critical minerals energy transition as countries worldwide strive to reduce carbon emissions.

Growing Demand in Strategic Applications

Graphite demand is projected to increase dramatically through 2030 and beyond, driven primarily by energy transition technologies:

Table: Projected Graphite Demand Growth by Sector

| Sector | 2023 Demand (tonnes) | 2030 Projected Demand (tonnes) | Growth % |

|---|---|---|---|

| EV Batteries | 250,000 | 1,000,000+ | 300% |

| Energy Storage | 75,000 | 300,000 | 300% |

| Traditional Industries | 850,000 | 1,100,000 | 29% |

| Defense Applications | 40,000 | 90,000 | 125% |

The United States currently imports a major portion of its graphite requirements, creating significant vulnerability for both economic security and defense industrial base needs. This import dependency has elevated graphite's strategic profile among policymakers and defense planners.

Current Supply Chain Vulnerabilities

The graphite supply chain faces several critical challenges that make vertical integration increasingly attractive:

- Geographic concentration: Over 80% of natural graphite processing occurs in China, creating single-point vulnerability

- Processing bottlenecks: Limited capacity for high-purity processing outside Asia with few alternative suppliers

- Quality inconsistencies: Variable specifications from different suppliers complicating qualification processes

- Regulatory pressures: Growing restrictions on sourcing from regions with environmental or labor concerns

- Increasing trade barriers: Tariffs, export controls, and other restrictions affecting global supply networks

These vulnerabilities have prompted both government action and corporate strategy shifts, with integrated mine-to-market approaches emerging as a resilient solution for supply chain security. In response, many nations are developing comprehensive defense critical materials strategies to reduce their dependence on foreign sources.

How Do Companies Implement a Mine-to-Market Strategy?

Implementing a comprehensive mine-to-market graphite strategy requires careful planning across multiple operational domains. Companies must develop capabilities spanning geological assessment through advanced manufacturing, often across multiple jurisdictions with varying regulatory environments.

The execution typically follows a staged approach, beginning with resource development and progressively expanding into higher-value processing activities.

Resource Development and Mining Operations

The foundation of any mine-to-market strategy begins with securing high-quality graphite resources:

Critical Factors in Graphite Mining

- Deposit quality: Focus on large-flake, high-grade graphite (>5% TGC) for maximum processing flexibility

- Mining methodology: Surface mining often preferred due to graphite's relative softness and near-surface deposits

- Environmental considerations: Implementing sustainable extraction practices to meet increasing ESG requirements

- Resource scale: Ensuring sufficient reserves to support long-term operations and justify processing investments

- Infrastructure access: Establishing proximity to transportation networks and reliable energy resources

Companies like International Graphite have prioritized resource development through projects such as Springdale in Western Australia, which serves as the foundation for their integrated supply chain strategy.

Primary Processing Technologies

Converting raw graphite ore into marketable concentrate requires specialized processing capabilities:

Processing Steps for Graphite Concentrate

- Crushing and grinding: Reducing ore to appropriate particle size without destroying valuable flakes

- Flotation: Separating graphite from waste minerals through selective reagent systems

- Classification: Sorting by flake size and purity to optimize value and application suitability

- Purification: Achieving target carbon content (typically 94-98% TGC) through thermal or chemical methods

- Drying and packaging: Preparing concentrate for transport or further processing at specialized facilities

These primary processing steps form the intermediate stage in the value chain, producing a marketable concentrate that can either be sold directly or further processed into specialized products.

Advanced Processing for Value-Added Products

The highest value in the graphite supply chain comes from converting concentrate into specialized products:

High-Value Graphite Products

- Spherical graphite: Processed and shaped specifically for battery anodes through micronization and spheronization

- Coated spherical graphite (CSG): Enhanced performance for lithium-ion batteries with protective carbon coatings

- Expandable graphite: Chemically treated material used in fire retardants and thermal management applications

- Micronized graphite: Precision-sized particles for industrial lubricants, conductive coatings, and additives

- High-purity flake graphite: Specialty material for technical applications requiring 99.95%+ carbon content

International Graphite exemplifies this approach with facilities at Collie (Western Australia) for micronizing operations and plans for battery anode materials production, demonstrating the progressive implementation of advanced processing capabilities. These developments also highlight the importance of sustainable mining transformation in modern resource industries.

Strategic Facility Placement

Successful mine-to-market strategies require careful consideration of facility locations:

Location Factors for Processing Facilities

- Proximity to resources: Reducing transportation costs for raw materials by locating near mining operations

- Energy availability: Securing access to reliable, affordable power sources for energy-intensive processing

- Market access: Positioning near end-users or transportation hubs to minimize finished product logistics

- Regulatory environment: Selecting jurisdictions with favorable permitting and operational conditions

- Workforce availability: Ensuring access to skilled labor and technical expertise for specialized operations

International Graphite's multi-jurisdictional approach—spanning Western Australia, Germany, and potential US operations in Georgia—demonstrates how strategic facility placement can address market access needs while mitigating geographic concentration risks.

What Are the Economic Benefits of Mine-to-Market Integration?

The economic case for mine-to-market integration in graphite production centers on value capture across multiple production stages, risk mitigation, and strategic positioning in growing markets. Companies implementing this approach can realize significantly higher returns than those focused solely on mining or processing activities.

The financial benefits compound as operations mature and achieve scale efficiencies across integrated facilities. In-depth mining economics insights show that vertical integration can dramatically improve profitability in the graphite sector.

Enhanced Profit Margins

Vertical integration allows companies to capture value at multiple stages of production:

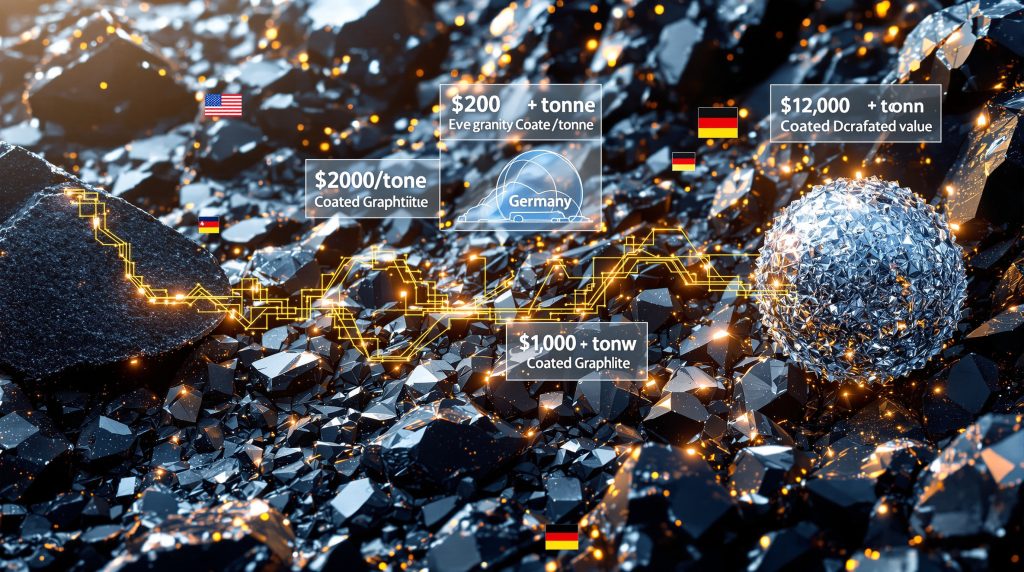

Value Addition Through Processing

| Product Stage | Approximate Value (USD/tonne) | Value Multiplier |

|---|---|---|

| Raw Graphite Ore | $100-200 | 1x |

| Graphite Concentrate (95% TGC) | $800-1,200 | 6x |

| Purified Graphite (99.95%) | $3,000-5,000 | 25x |

| Spherical Graphite | $4,500-7,000 | 35x |

| Coated Spherical Graphite | $7,000-12,000 | 60x |

This value progression explains why companies like International Graphite target revenue of approximately US$30 million from 10,000 tonnes of high-value graphite products—representing significantly higher returns than equivalent volumes of unprocessed material.

Reduced Supply Chain Risks

Integrated operations provide significant risk mitigation advantages:

- Price volatility protection: Reduced exposure to market fluctuations in intermediate products

- Supply assurance: Guaranteed access to critical materials regardless of market conditions

- Quality consistency: Maintained specifications throughout production for reliable performance

- Reduced logistics complexity: Fewer transportation and handling stages minimizing disruption risks

- Intellectual property protection: Proprietary processes remain in-house rather than outsourced

These risk mitigation benefits have become increasingly valuable as graphite supply chains face growing geopolitical pressures and market uncertainties, particularly for battery and defense applications where supply security is paramount.

How Are Government Policies Shaping Mine-to-Market Strategies?

Government policies worldwide are increasingly influencing the development of graphite supply chains, with particular emphasis on reducing dependency on concentrated sources and supporting domestic processing capabilities. These policy interventions create both opportunities and imperatives for companies pursuing mine-to-market strategies.

The evolving regulatory landscape has become a central consideration in strategic planning for graphite producers.

Critical Minerals Initiatives

Governments worldwide are implementing policies to secure graphite supply chains:

Key Policy Developments

- Defense procurement requirements: Preference for domestically sourced materials to support national security

- Financial incentives: Grants, loans, and tax benefits for establishing processing facilities in strategic locations

- Research funding: Support for advanced processing technologies to reduce energy consumption and environmental impact

- Trade measures: Tariffs and restrictions on imports from certain regions to encourage supply diversification

- Strategic partnerships: Government-industry collaborations for supply security in critical applications

International Graphite's participation in Australia Trade and Invest delegations to Washington DC demonstrates how companies can leverage government initiatives to advance their integrated development strategies.

Case Study: US Critical Minerals Strategy

The United States has implemented several measures specifically targeting graphite supply chain development:

- Defense Production Act: Authorizing funding for domestic graphite processing to support defense industrial base

- Inflation Reduction Act: Tax credits for domestically sourced battery materials including graphite components

- DOD funding programs: Supporting feasibility studies and facility development through defense industrial base consortium programs

- EXIM Bank financing: Providing capital for critical minerals projects to reduce import dependency

- Trade restrictions: Limiting dependence on Chinese graphite sources through targeted policy measures

International Graphite has already received positive feedback from the US Department of Defense on a submission for feasibility funding, with its proposal meeting the criteria for "Award/Basket Consideration" under the defense industrial base consortium program. This exemplifies how government policy is directly influencing corporate strategy in the graphite sector.

What Challenges Do Mine-to-Market Strategies Face?

Despite the compelling strategic and economic benefits, implementing a mine-to-market graphite strategy presents significant challenges that companies must navigate successfully. These obstacles span technical, financial, and market dimensions, requiring careful planning and execution.

Companies pursuing integrated strategies must realistically assess and mitigate these challenges to achieve their strategic objectives.

Technical Hurdles

Implementing a fully integrated graphite supply chain presents significant technical challenges:

- Processing complexity: Achieving battery-grade specifications requires sophisticated technology and expertise

- Scale requirements: Economic viability demands substantial production volumes to justify capital investment

- Quality consistency: Maintaining uniform specifications across production batches for demanding applications

- Energy intensity: Managing high power consumption for processing operations, particularly purification

- Waste management: Handling byproducts and processing residues in environmentally responsible ways

These technical challenges explain why companies like International Graphite adopt a phased approach to integration, progressively developing capabilities across different processing stages rather than attempting simultaneous implementation.

Financial Considerations

The capital-intensive nature of mine-to-market strategies creates financial challenges:

- High upfront investment: Substantial capital required for facilities and equipment across multiple locations

- Extended payback periods: Longer time to reach positive cash flow compared to single-stage operations

- Market uncertainty: Evolving demand patterns and pricing structures creating revenue projection challenges

- Financing availability: Limited funding sources for integrated projects spanning multiple jurisdictions

- Risk concentration: Exposure across multiple operational segments requiring comprehensive risk management

International Graphite's target timeline—aiming for fully operational facilities by 2027—reflects the extended development periods typical for integrated graphite operations, with significant capital deployment required before realizing the full economic benefits.

How Are Companies Implementing Mine-to-Market Strategies Globally?

Companies are implementing mine-to-market graphite strategies across multiple jurisdictions, creating geographically diversified supply chains that balance resource access, processing capabilities, and market proximity. These approaches reflect both strategic positioning and risk mitigation considerations.

Successful implementation typically involves phased development across multiple locations, progressively expanding processing capabilities while maintaining operational flexibility.

Case Study: International Graphite's Integrated Approach

International Graphite exemplifies the mine-to-market strategy with its expanding global footprint:

Key Elements of International Graphite's Strategy

- Resource development: Advancing the Springdale graphite project in Western Australia to secure raw material supply

- Domestic processing: Establishing micronizing facilities in Collie, Western Australia for initial value addition

- International expansion: Developing processing capabilities in Bitterfeld, Germany to serve European markets

- US market development: Investigating processing opportunities in Savannah, Georgia on similar scale to Australian operations

- Government engagement: Securing support from Australian and US authorities through strategic partnerships

This multi-jurisdictional approach demonstrates how companies can create resilient supply chains that balance resource access, processing capabilities, and market proximity while reducing geographic concentration risk.

Production Targets and Economic Impact

The company's integrated approach aims to achieve significant production milestones:

- Combined processing capacity: Approximately 10,000 tonnes of high-value graphite products across global operations

- Revenue potential: Estimated US$30 million in annual revenue by 2027 from integrated operations

- Employment creation: Skilled jobs across multiple jurisdictions in mining, processing, and technical roles

- Supply chain security: Providing non-Chinese graphite sources to Western markets for critical applications

- Technology development: Advancing processing capabilities for battery-grade materials to support energy transition

These targets illustrate the economic scale and strategic impact achievable through successful implementation of a mine-to-market graphite strategy, particularly when aligned with government priorities for critical minerals development.

How Does a Mine-to-Market Strategy Support Battery Supply Chains?

Battery manufacturing depends on secure, consistent supplies of high-quality graphite materials, making integrated suppliers particularly valuable to this rapidly growing sector. Mine-to-market strategies address several critical requirements for battery producers seeking to reduce supply chain risks while meeting stringent performance specifications.

The growth of electric vehicle and energy storage markets has elevated the strategic importance of reliable graphite supply chains. According to SmallCaps, International Graphite's expansion into European and US markets highlights the global nature of this demand.

Meeting EV Battery Requirements

The electric vehicle revolution depends on secure supplies of battery-grade graphite:

Critical Graphite Specifications for Batteries

- Purity levels: Minimum 99.95% carbon content to ensure battery performance and safety

- Particle sizing: Precise spherical dimensions for anode materials to optimize capacity and cycle life

- Surface treatments: Specialized coatings for performance enhancement and improved electrolyte interaction

- Consistency standards: Uniform quality across production batches for reliable manufacturing

- Performance testing: Meeting rigorous battery manufacturer specifications for electrochemical properties

International Graphite's focus on battery anode materials production capabilities directly addresses these requirements, creating a secure supply channel for this critical component of the battery supply chain.

Supply Chain Security for Battery Manufacturers

Battery producers benefit significantly from integrated graphite suppliers:

- Traceability: Complete visibility throughout the production process from mine to final product

- Certification compliance: Meeting ESG and responsible sourcing requirements increasingly demanded by OEMs

- Supply guarantees: Long-term agreements with reliable producers reducing allocation risk

- Technical collaboration: Joint development of specialized materials optimized for specific battery chemistries

- Reduced qualification time: Streamlined approval processes for new suppliers with consistent quality control

These benefits make integrated graphite producers particularly valuable partners for battery manufacturers seeking to reduce supply chain vulnerabilities while meeting increasingly stringent performance and sustainability requirements. As noted by International Graphite, their German expandable graphite plant is specifically designed to boost Europe's supply security.

What Does the Future Hold for Mine-to-Market Graphite Strategies?

The graphite sector is evolving rapidly, with integrated mine-to-market strategies likely to play an increasingly important role as demand grows and supply chain security concerns intensify. Future developments will be shaped by technological innovation, market evolution, and policy interventions across multiple jurisdictions.

Companies positioning themselves now with integrated capabilities will be well-placed to capture opportunities in this dynamic landscape.

Emerging Trends and Innovations

The graphite sector continues to evolve with several key developments on the horizon:

- Synthetic graphite competition: Balancing natural and synthetic sources based on cost, performance, and sustainability factors

- Recycling integration: Incorporating recovered graphite into the supply chain to reduce primary material requirements

- Advanced processing techniques: Reducing energy consumption and environmental impact of purification processes

- Specialized product development: Creating custom formulations for specific applications beyond standard specifications

- Supply chain digitalization: Implementing blockchain and traceability technologies to verify provenance and ESG compliance

These innovations will reshape the competitive landscape, potentially creating new value-capture opportunities within integrated supply chains.

Strategic Positioning for Future Growth

Companies pursuing mine-to-market strategies are preparing for significant industry changes:

- Capacity expansion: Scaling operations to meet projected demand growth from battery and energy storage sectors

- Geographic diversification: Establishing presence in multiple strategic markets to mitigate regional risks

- Technology acquisition: Securing proprietary processing capabilities for competitive differentiation

- Strategic partnerships: Collaborating with end-users and technology developers to align product development

- Sustainability leadership: Setting new standards for responsible graphite production to meet increasing ESG requirements

International Graphite's investigation of opportunities in Savannah, Georgia demonstrates this forward-looking approach, positioning the company to serve the growing US market for critical minerals while aligning with government priorities for supply chain security.

FAQ: Mine-to-Market Graphite Strategy

What makes graphite a critical mineral?

Graphite is designated as critical due to its essential role in batteries, defense applications, and clean energy technologies, combined with concentrated supply chains that create vulnerability for Western economies. The US currently imports a major portion of its graphite needs, with the mineral recognized as an important component for maintaining and building its defense industrial base and economic security.

Why is vertical integration important for graphite producers?

Vertical integration allows producers to capture more value, ensure quality control throughout the production process, and reduce dependence on external suppliers in geopolitically sensitive regions. Companies can generate approximately 60 times more value from coated spherical graphite compared to raw graphite ore.

How does a mine-to-market strategy reduce supply chain risks?

By controlling multiple stages of production, companies can ensure consistent supply, maintain quality standards, and reduce vulnerability to trade disruptions or price volatility in intermediate products. This integrated approach provides resilience against geopolitical tensions affecting critical minerals markets.

What processing steps are required to produce battery-grade graphite?

Battery-grade graphite requires mining, concentration, purification to 99.95%+ carbon content, micronization, spheronization, classification, and surface coating—all requiring specialized equipment and expertise. These complex processing requirements explain why vertical integration is particularly valuable in the graphite sector.

How are governments supporting domestic graphite processing?

Governments are providing funding for feasibility studies, offering grants and loans for facility development, implementing favorable procurement policies, and establishing strategic minerals programs to reduce import dependence. International Graphite has already received positive feedback from the US Department of Defense on a submission for feasibility funding under the defense industrial base consortium program.

What are the main challenges in implementing a complete mine-to-market strategy?

Key challenges include high capital requirements, technical complexity of processing, extended development timelines, market uncertainty, and the need to compete with established low-cost producers. Companies typically adopt a phased approach, targeting operational capability by 2027 for fully integrated facilities.

Further Exploration:

Readers interested in learning more about graphite supply chains can also explore related educational content from SmallCaps, which offers coverage of critical minerals developments in the Australian market.

Want to Stay Ahead of Major ASX Mineral Discoveries?

Discovery Alert's proprietary Discovery IQ model instantly notifies you of significant mineral announcements across the ASX, transforming complex data into actionable investment insights. Explore historic returns from major discoveries and position yourself for market-beating opportunities at Discovery Alert's discoveries page.