June 21, 2026

Understanding the Oil and Gas Market Downturn

What Caused the Recent Oil and Gas Stock Slide?

The recent decline in oil and gas stocks stems from two major factors: OPEC+ production increases and proposed tariffs by U.S. President Donald Trump. On April 3, 2025, the S&P 500 Energy index fell by 5.4%, marking its most significant intraday decline since March 2023. All 23 member stocks in the index experienced decreases, with Devon Energy Corporation leading the downturn with a drop of nearly 12%.

This dramatic sell-off represented the energy sector's worst single-day performance in over two years, reflecting deep market concerns about both the supply glut and potential demand destruction. ExxonMobil and Chevron, traditional market stalwarts, weren't spared, with both experiencing declines exceeding 4% amidst trading volumes 40% above 30-day averages.

Unlike previous oil market corrections, this downturn is unique in being triggered simultaneously by both supply and demand factors, creating what analysts call a "perfect storm" for energy equities.

OPEC+ Production Boost Details

The Decision to Increase Output

OPEC+ members announced plans to increase oil production starting in May 2025, with Saudi Arabia contributing 300,000 barrels per day (bpd) and the UAE adding 200,000 bpd to global supply. This decision has had immediate impacts on global commodities market insights, with Crude Oil WTI Futures falling 7.6% to $66.25 and Brent Oil Futures declining 6.9% to $69.73 as of 11:18 EST (15:18 GMT) on the announcement day.

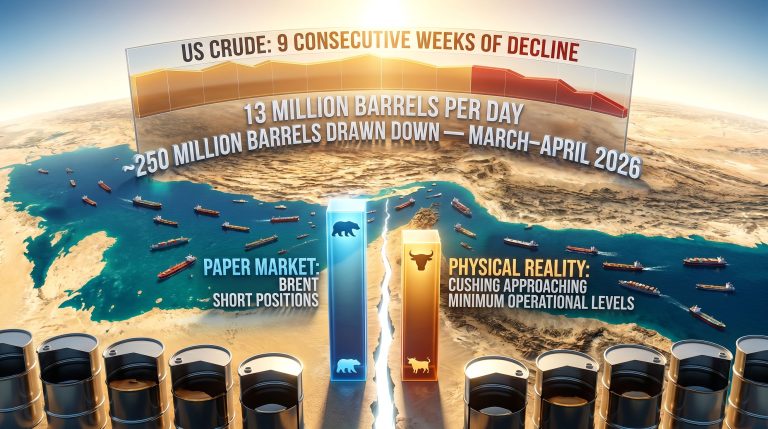

The timing of this production boost is particularly significant as it comes when global crude inventories have already risen to 4.2 billion barrels in March 2025, according to International Energy Agency data—the highest level since 2021. Market watchers note that OPEC+ compliance with previously agreed production cuts had already deteriorated to 85% in early 2025, down from 95% in 2024.

Expert Analysis of OPEC+ Strategy

Roth MKM Senior Energy Analyst Leo Mariani provided insight into OPEC's decision, suggesting that the organization was likely aware their production increase would put downward pressure on oil prices in the near term. According to Mariani, this move could be interpreted in two ways:

- A punitive measure against non-compliant members who have exceeded production quotas, specifically Russia which exceeded its allocation by 120,000 bpd in Q1 2025

- A strategic response anticipating production losses from sanctioned countries like Iran and Venezuela, which together face an estimated 800,000 bpd loss in 2025

Energy Aspects, a respected industry consultancy, noted in their latest report: "This signals OPEC+'s confidence in absorbing Iranian and Venezuelan supply gaps while maintaining market discipline among its core members."

When big ASX news breaks, our subscribers know first

Trump's Tariff Plans and Energy Market Impact

Proposed Tariff Structure

President Donald Trump's recently announced tariff plans have compounded the pressure on oil and gas stocks. These tariffs represent a significant shift in U.S. trade policy with potential global economic implications. The proposed measures target approximately $300 billion in imports, including a 15% tariff on refined petroleum products and 10% on industrial machinery used throughout the energy supply chain.

Industry economists point out that energy-related tariffs alone are projected to raise U.S. inflation by 1.2%, according to JPMorgan analysis. This inflationary pressure could trigger tighter monetary policy, further constraining economic growth.

Economic Consequences for Oil Demand

Mizuho Securities USA's Energy Team, led by Paul Sankey, highlighted on Thursday that the proposed tariffs pose a substantial threat to the global economy and could lead to decreased demand for crude oil. Their analysis specifically noted that:

- Global economic growth may slow by 0.5% in 2025, translating to approximately 1 million bpd lower oil demand

- Transportation disruptions could reduce jet fuel demand by 15% in Q3 2025 if trade wars escalate

- The combination of increased supply and potentially reduced demand creates a bearish outlook for oil prices

These projections align with historical precedent from the 2018-2019 tariff implementation, which the International Monetary Fund estimated created a 0.5% drag on global GDP. The energy sector is particularly vulnerable to such macroeconomic headwinds given its high correlation with industrial activity and transportation demand.

How Energy Stocks Are Responding

S&P 500 Energy Index Performance

The S&P 500 Energy index experienced its worst single-day performance in over two years, with all 23 member companies registering losses. This widespread decline demonstrates the market's significant concern about both supply increases and potential demand destruction.

Trading volumes reached approximately 250 million shares, significantly above the 30-day average of 180 million, indicating panic selling rather than ordinary market rotation. More telling is that the correlation coefficient between energy stocks and oil prices rose to 0.92, well above the 2025 year-to-date average of 0.85, suggesting investors are pricing in a sustained period of lower commodity prices.

Individual Stock Movements

The impact varied across energy companies, with some notable performances:

- Devon Energy Corporation (NYSE:DVN): Led declines with a drop of up to 11.9%, particularly vulnerable due to having only 40% of its 2025 output hedged at $75/barrel

- Marathon Oil: Declined 9%, despite recently announcing a share buyback program

- ConocoPhillips: Fell 7%, though analysts note its more diversified asset base provides better downside protection

- Integrated majors like Chevron and ExxonMobil showed more resilience with 4-5% declines, cushioned by their downstream refining operations that typically benefit from lower crude prices

This divergence in performance highlights the importance of company-specific factors such as hedging strategies, debt levels, and operational diversity in weathering market turbulence.

Market Outlook for Oil and Gas

Price Trajectory Predictions

The dual pressures of increased OPEC+ production and Trump's policy impact on global commodity markets suggest continued volatility in oil prices. Current price levels show:

- WTI crude trading at $66.25, down 7.6%

- Brent crude at $69.73, down 6.9%

Goldman Sachs has revised its 2025 Brent average forecast to $75 per barrel, down from its previous estimate of $85. Meanwhile, Citigroup's bear case scenario puts WTI at $60 if tariffs are fully implemented as announced.

When compared to historical corrections, this drop remains less severe than the 2014 oil price collapse (-40% in six months) or the 2020 COVID-driven demand shock, suggesting potential stabilization ahead.

Factors That Could Stabilize the Market

Despite current downward pressure, several factors could potentially stabilize energy markets:

- Actual implementation details of OPEC+ production increases, which historically often fall short of announced targets

- Final scope and timing of proposed tariffs, which may be modified during implementation

- Potential compensatory production cuts from other producers concerned about price stability

- Seasonal demand increases approaching summer driving season, expected to add 1.5 million bpd according to EIA projections

- Strategic Petroleum Reserve dynamics, with the U.S. currently holding 550 million barrels (2025 capacity)

Additionally, geological constraints in some key production regions may naturally limit how quickly supply can actually increase, regardless of OPEC+ announcements. North American shale basins, for instance, are showing signs of geological maturity with higher decline rates in established fields.

Investment Implications

How Should Investors Respond to the Downturn?

Risk Assessment Strategies

Investors in the energy sector should consider:

- Portfolio exposure to companies with higher production costs that may be more vulnerable

- Geographic diversification of energy holdings

- Balance sheet strength of energy companies during potential extended price weakness

Debt-to-EBITDA ratios have become increasingly important metrics in this environment, with Chevron (1.2x), ExxonMobil (1.5x), and Devon Energy (2.1x) representing different risk profiles. Companies with ratios above 2.5x may face particular scrutiny if prices remain depressed through 2025.

Morgan Stanley's recent research note advises investors to "prioritize companies with breakeven prices below $50," highlighting Saudi Aramco ($45) and ConocoPhillips ($55) as examples of producers with superior cost structures.

Potential Opportunities in the Volatility

Market corrections often create potential entry points for long-term investors:

- Companies with lower production costs may weather the downturn better

- Integrated majors with diversified operations across the value chain typically offer more stability

- Energy infrastructure companies with fee-based models may be less exposed to commodity price swings

The sector's average dividend yield has risen to 4.2%, up from 3.8% in 2024, potentially creating attractive income opportunities for patient investors. However, sustainability of these payouts requires careful analysis of individual company cash flows under various price scenarios.

Long-term Considerations for Energy Investors

Supply-Demand Fundamentals

While short-term pressures exist, long-term energy demand continues to grow globally. Investors should consider:

- The pace of energy transition versus ongoing fossil fuel demand

- Global economic growth projections and energy intensity

- Geopolitical factors that could quickly reverse current supply increases

The current market turbulence also obscures significant structural changes in global oil markets, including declining production from conventional fields and increased concentration of lowest-cost reserves in fewer countries. These factors could create pricing power for certain producers over longer investment horizons.

In the midst of these market shifts, JHN Elixir Energy's groundbreaking gas resource discovery demonstrates that despite current downturns, new developments continue to reshape the energy landscape. Additionally, BHP's strategic response to global trade challenges provides a blueprint for how major energy players might navigate the current volatility.

Dividend Sustainability

Many energy companies offer attractive dividends, but price pressures may test payout sustainability:

- Evaluate dividend coverage ratios under various price scenarios

- Consider companies with histories of maintaining dividends through previous downturns

- Assess balance sheet strength and capital expenditure flexibility

Companies that have implemented variable dividend structures may demonstrate greater resilience through this correction compared to those committed to fixed payouts that could strain capital resources if prices remain depressed. According to recent IEEFA analysis, oil producers face significant profit squeezes amid the shifting policy landscape, further emphasizing the importance of balance sheet strength.

The next major ASX story will hit our subscribers first

FAQ: Oil and Gas Market Turbulence

Why did OPEC+ decide to increase production now?

According to analyst Leo Mariani, OPEC+ may be either penalizing non-compliant members for over-production or anticipating production losses from countries under sanctions like Iran and Venezuela. The timing also coincides with global crude inventories reaching 4.2 billion barrels, 15% above the 2015-2025 average according to EIA data.

How much have oil prices fallen due to these developments?

As of the reporting time, Crude Oil WTI Futures were down 7.6% to $66.25, while Brent Oil Futures declined 6.9% to $69.73. This represents the steepest single-day price decline for both benchmarks in 2025, as reported by major financial outlets.

Which energy stock was most affected by the news?

Devon Energy Corporation (NYSE:DVN) led the decline with a plunge of as much as 11.9%. The company's higher vulnerability stems partially from its hedging position covering only 40% of 2025 production at $75/barrel.

How do tariffs affect oil prices?

Mizuho analysts note that tariffs threaten global economic growth, potentially reducing demand for crude oil by approximately 1 million barrels per day. Additionally, any disruptions to global transportation would negatively impact crude oil consumption, with jet fuel demand potentially falling 15% in Q3 2025 if trade tensions escalate.

What was the overall impact on the energy sector?

The S&P 500 Energy index fell by 5.4%, marking its most substantial intraday decline since March 2023, with all 23 member stocks experiencing decreases. Trading volumes reached approximately 250 million shares, 40% above typical 30-day averages.

Which sectors benefit from lower oil prices?

Airlines stand to benefit significantly, as fuel costs represent 25-30% of their operating expenses. Petrochemical companies also typically see margin expansion when crude oil prices decline, as their feedstock costs decrease while product pricing adjusts more gradually. Furthermore, the ongoing role of mining in the clean energy transition creates interesting cross-sector dynamics as traditional energy markets face disruption.

Are You Monitoring ASX Mining Discoveries?

Stay ahead of the market with real-time alerts on significant ASX mineral discoveries through Discovery Alert's proprietary Discovery IQ model, turning complex data into actionable investment opportunities. Visit our dedicated discoveries page to understand why major mineral discoveries can lead to substantial market returns.