June 22, 2026

When Dormant Deposits Come Back to Life: The Economics Behind South Africa's Underground Gold Renaissance

There is a pattern that repeats itself across mining history with striking regularity. A commodity price cycle peaks, projects get shelved, technical files gather dust in corporate archives, and then a new price environment arrives and suddenly the economics of those same deposits look entirely different. What was once marginal becomes compelling. What was once shelved becomes strategic. The Pan African Poplar gold project is one of the clearest contemporary examples of this dynamic playing out in real time across the Witwatersrand Basin.

Understanding why Poplar matters requires looking beyond the project itself and examining the broader conditions that have made South African underground gold development viable again at a scale not seen in decades.

When big ASX news breaks, our subscribers know first

The Gold Price Shift That Changed Everything

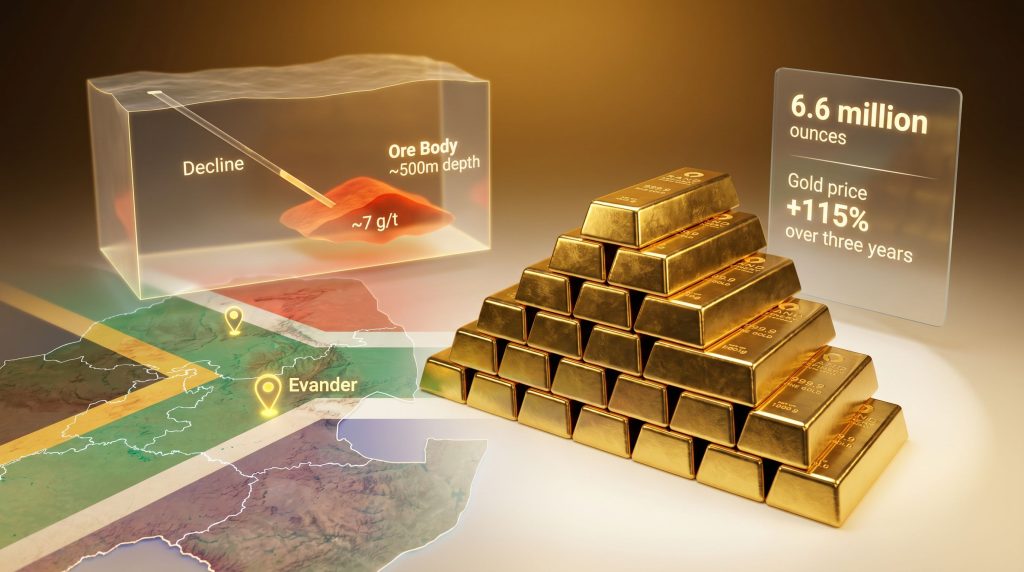

Gold prices have risen by approximately 115% over the past three years, a magnitude of price movement that fundamentally rewrites the economic feasibility calculations for underground development projects across Southern Africa. This is not a marginal improvement at the edges of profitability. It is a structural repricing of what constitutes a viable orebody. Reviewing the gold price outlook helps contextualise just how dramatically this shift has altered the landscape for producers and developers alike.

To understand why this matters so much for underground operations specifically, it helps to appreciate the cost structure involved. Underground gold mining carries high fixed costs: shaft or decline development, ventilation, ground support, hoisting, dewatering. These costs exist whether production is running at full capacity or not. When gold was trading at lower levels, many deposits with otherwise attractive geology simply could not generate sufficient revenue per tonne of ore to justify those fixed cost burdens. At today's gold prices, the calculus is different.

The Evander district in Mpumalanga province, where Pan African Resources operates its Evander Gold Mines, has historically been considered underexplored relative to other parts of the broader Witwatersrand Basin. That comparison is now drawing fresh attention from capital allocators who understand that the Witwatersrand remains the most enduringly productive gold-bearing geological formation on the planet, hosting an estimated 50% of all gold ever mined globally.

Furthermore, the relationship between gold price and mining equities has never been more relevant, as rising spot prices amplify margins for operators with high-grade, low-depth assets precisely like Poplar.

Technical Profile of the Pan African Poplar Gold Project

The Pan African Poplar gold project is not a greenfield exploration story. It is a historically documented deposit that last received substantive technical investigation in the 1990s when it fell under the Gengold corporate structure, a predecessor entity within the South African gold industry. The re-emergence of Poplar as a live development candidate is directly attributable to the gold price environment described above.

The deposit's technical fundamentals are genuinely competitive within the South African underground gold context:

| Parameter | Reported Figure |

|---|---|

| Estimated Gold Grade | ~7 grams per tonne (g/t) |

| Total Resource Estimate | ~6.6 million ounces |

| Projected Depth | ~500 metres |

| Distance from Evander Gold Mines | ~6 kilometres north |

| Proposed Access Method | Underground decline |

| Indicative Annual Production Target | ~100,000 ounces per year |

The grade figure of approximately 7 g/t is particularly significant. Most investors outside the mining sector may not immediately appreciate the context, but South African underground operations have historically operated at far lower grades. Many legacy Witwatersrand mines run between 2 g/t and 4 g/t, with some ultra-deep operations processing ore at even lower grades while relying on sheer volume and established infrastructure to generate returns. A 7 g/t grade in this context represents a genuinely high-quality ore body.

Deposits with grades above 6 g/t at accessible depths are increasingly rare in the South African mining landscape, and their scarcity in a rising gold price environment makes them disproportionately valuable to mid-tier producers seeking meaningful production growth.

The depth profile of approximately 500 metres is another differentiating characteristic. South Africa's mining legacy includes operations descending to depths of 3,500 metres or more, where extreme heat, pressure, and ventilation requirements create immense technical and financial complexity. At 500 metres, Poplar sidesteps these challenges almost entirely. The geotechnical environment at that depth is considerably more manageable, rock temperatures remain within workable ranges without extraordinary cooling infrastructure, and ground support requirements are far less demanding than at ultra-deep operations.

Decline Access: What It Means and Why It Matters

The proposed development method for Poplar is a decline-based underground access system, as distinct from conventional vertical shaft sinking. For readers unfamiliar with mining terminology, a decline is essentially a tunnelled ramp driven at a downward angle into the ground, wide enough to accommodate vehicles and equipment. This allows trucks, loaders, and personnel to drive directly into the mine rather than using a vertical hoisting system.

The practical implications of choosing a decline over a shaft are significant:

- Decline development is generally faster to execute than vertical shaft sinking, which can take three to five years at depth

- Capital costs per metre of access development are typically lower for declines at shallower depths

- Declines provide greater operational flexibility, allowing multiple mining fronts to be accessed simultaneously

- The method is well-suited to the 500-metre depth profile of Poplar, where the additional travel time compared to a shaft remains commercially acceptable

Importantly, Pan African Resources already holds the mining right covering the Poplar deposit, which removes a critical early-stage regulatory hurdle. New mining rights applications in South Africa can take years to resolve and represent one of the most significant execution risks in African resource development. The fact that Poplar sits within an existing right boundary is a structural advantage that is easy to overlook but genuinely meaningful.

Infrastructure Leverage: The Kinross Plant Advantage

One of the most commercially significant attributes of the Pan African Poplar gold project is its proximity to existing processing infrastructure. Pan African Resources holds spare processing capacity at the Kinross plant, the processing facility associated with its Evander operations. For a proposed new underground mine, the ability to deliver ore to an existing, operational processing facility rather than constructing a standalone plant represents a substantial reduction in both capital requirements and project execution risk.

Standalone processing plants for underground gold operations can cost hundreds of millions of dollars depending on throughput capacity and metallurgical complexity. Eliminating that line item from the capital plan changes the project economics materially and shortens the timeline from construction commencement to first production.

The combination of existing mining rights, spare processing capacity, and established infrastructure in the surrounding operational corridor effectively means that Poplar is being assessed against a lower capital intensity threshold than a comparable deposit in a greenfield setting would face. In addition, gold as an inflation hedge continues to attract institutional capital into the sector, further supporting the investment case for assets of this quality.

Co-Investor Interest: What the Market Is Signalling

Pan African Resources' CEO Cobus Loots confirmed in June 2026, as reported by MiningMX, that multiple parties had approached the company expressing interest in potentially participating in the Poplar project. He noted that this level of engagement was uncommon for a deposit at such an early evaluation stage, and acknowledged the broader attractiveness of finding a deposit of this character in the current gold price environment.

The significance of inbound co-investor interest before feasibility completion should not be underestimated. In mining project finance, co-investment conversations typically emerge at the prefeasibility or bankable feasibility stage, once resource confidence levels are higher and project parameters are better defined. Interest arriving before that point generally indicates that the grade, scale, infrastructure position, and gold price context are sufficiently compelling that external capital is willing to accept early-stage uncertainty in exchange for entry at lower valuations.

Co-investment structures in African gold development are also gaining broader traction for structural reasons beyond Poplar:

- Capital requirements for underground development have risen sharply with input cost inflation

- Balance sheet discipline has become a priority for mid-tier producers navigating high interest rate environments

- Risk-sharing mechanisms allow producers to advance multiple assets simultaneously without sacrificing shareholder return commitments

- Streaming and royalty finance providers are increasingly active in the African gold space, offering non-dilutive capital alternatives

Capital Allocation: Balancing Poplar Against the Broader Growth Agenda

Understanding the Pan African Poplar gold project requires situating it within the company's overall capital spending framework. Pan African Resources has guided toward capital expenditure of approximately $328 million in its next financial year, nearly double its prior-year level. The primary driver of this elevated spending is the ramp-up of Tennant Mines, the company's Australian gold operation, rather than any South African growth initiative.

This context is critical for investors assessing Poplar's development timeline:

| Financial Metric | Reported Position |

|---|---|

| Cash on Balance Sheet | ~$200 million |

| Production Growth (recent period) | ~40% increase |

| Dividend Policy | 40% to 50% of free cash flow after capex |

| Guided Capital Expenditure (next FY) | ~$328 million |

| FY2026 Financial Year Close | 30 June 2026 |

| Results Publication Date | 16 September 2026 |

Loots has been candid about the tension between growth capital and shareholder return expectations. His comments to MiningMX indicated that the company's shareholder base currently prioritises cash distributions over capital-intensive development commitments, a dynamic that directly influences the pace and structure of any Poplar development decision.

The company's strong cash generation provides genuine optionality. With approximately $200 million on the balance sheet after commissioning two major new projects within an 18-month window, Pan African is not a capital-constrained operator. The constraint is more one of sequencing and shareholder sentiment than financial capacity.

Disclaimer: Forward-looking statements regarding production targets, capital expenditure guidance, dividend payments, and development timelines involve inherent uncertainty. Investors should not treat these projections as guarantees of future performance.

The next major ASX story will hit our subscribers first

Risk Landscape: What Could Alter Poplar's Development Trajectory

A balanced assessment of the Pan African Poplar gold project requires acknowledging the genuine risks alongside the compelling fundamentals.

Capital Intensity and Sequencing Risk

Even with a decline-based access model and existing processing infrastructure, underground mine development at 500 metres depth carries substantial upfront capital requirements. If Poplar advances without a co-investment partner, Pan African would be funding development during an already elevated group capex cycle.

Shareholder Sentiment Risk

Management has directly acknowledged that income-focused shareholders may view a large new capital commitment unfavourably if it materially compresses near-term dividend capacity. This is not a theoretical risk but an explicitly stated constraint on decision-making pace.

Data Currency Risk

The most recent substantive technical work on the Poplar deposit dates to the 1990s. Converting a historically documented resource to a modern definitive feasibility study standard requires significant new drilling, geotechnical investigation, and metallurgical test work. Any unexpected grade variability or structural complexity identified during this process could alter project economics.

Furthermore, drilling programs and resource definition work will be essential to upgrading the confidence level of the existing historical estimate before any formal investment decision can proceed responsibly.

Permitting Timeline Risk

South Africa's mining permitting framework, while more established than many peer jurisdictions on the continent, introduces procedural timeline variability. Environmental authorisation, water use licensing, and community consultation processes each carry their own timeline uncertainties.

What to Watch as the Poplar Story Develops

For investors and industry observers tracking this project, the following milestones represent the logical sequence of decision gates:

- Final feasibility study completion and formal resource confidence upgrade

- Announcement of any co-investment or joint venture structure, if applicable

- Pan African FY2026 results publication on 16 September 2026, likely including updated capital allocation guidance

- Environmental and permitting review initiation or update

- Board-level final investment decision, the ultimate trigger for construction commencement

The project's development trajectory will ultimately be shaped less by geology, which appears genuinely strong, and more by the intersection of gold price durability, shareholder return expectations, and the availability of co-investment capital to share the development burden. Consequently, investors should monitor Pan African Resources' latest updates directly to stay informed as these decision gates approach.

Pan African Poplar Gold Project: Frequently Asked Questions

What is the Pan African Poplar gold project?

Poplar is a proposed underground gold mine being evaluated by Pan African Resources. Located approximately 6 kilometres north of Evander Gold Mines in Mpumalanga, South Africa, it hosts an estimated resource of around 6.6 million ounces at approximately 7 g/t gold.

Why is a 7 g/t grade considered high quality?

The average grade of operating South African underground gold mines is well below 7 g/t. Many Witwatersrand operations run between 2 g/t and 4 g/t. At 7 g/t, Poplar generates significantly more gold revenue per tonne of rock mined, improving operating margins and reducing the break-even gold price.

Has a final investment decision been made?

No. As of mid-2026, Poplar remains at an early feasibility stage. Pan African has indicated that final feasibility work and a permitting review must be completed before any formal commitment is made.

What does a decline-based mining method involve?

A decline is a tunnelled ramp driven at a downward angle into the earth, allowing wheeled and tracked equipment to access underground workings directly. It is generally faster and less capital-intensive than vertical shaft sinking at shallower depths, making it well-suited to Poplar's approximately 500-metre depth profile.

When does Pan African Resources report its FY2026 financial results?

The company's 2026 financial year closes on 30 June 2026, with results scheduled for release on 16 September 2026.

Want To Be First When the Next Major Gold Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across gold and 30+ other commodities — so subscribers can act before the broader market reacts. Start a 14-day free trial at Discovery Alert today, or explore historic discovery returns to understand just how transformative early positioning in a major find can be.