August 1, 2026

The American energy sector continues its relentless search for economically viable drilling opportunities amid volatile commodity markets. While traditional oil and gas basins face mounting pressure from depleting sweet spots and escalating development costs, one geological formation maintains its position as the crown jewel of North American unconventional resource development. Understanding the strategic distribution and quality assessment of remaining Permian Basin drilling locations has become critical for operators navigating an increasingly complex investment landscape.

Recent analysis from Enverus Intelligence Research reveals that the Permian Basin contains approximately 55,000 drilling locations capable of breaking even below $50 per barrel, representing a 10% year-over-year growth in economically viable inventory. This expansion, driven by ongoing resource delineation and improved well performance, underscores the basin's unique position in sustaining development activity through commodity price cycles. Moreover, recent market dynamics and oil price rally insights suggest that operators are increasingly optimising their investment strategies to capitalise on favourable pricing conditions.

Geographic Foundation and Formation Architecture

The Permian Basin's competitive advantage stems from its multi-zone geological architecture spanning approximately 75,000 square miles across Texas and New Mexico. This vast expanse encompasses three distinct sub-basins, each offering unique development characteristics and economic profiles that collectively support sustained drilling activity. The geological diversity of the Permian Basin provides operators with numerous formation targets and development opportunities.

The Midland Basin represents the primary producing area, with concentrated development activity across Howard, Martin, and Midland counties. This region benefits from mature infrastructure networks and established supply chain relationships that reduce operational costs compared to frontier development areas. Furthermore, the Delaware Basin, encompassing Reeves, Culberson, Ward, and Loving counties in Texas plus Eddy and Lea counties in New Mexico, provides substantial co-development opportunities through its Bone Spring and Wolfcamp formations.

Formation Diversity and Stacked Pay Opportunities

The basin's stacked pay architecture creates development flexibility rarely matched in other North American plays. The Wolfcamp Formation, divided into A, B, C, and D benches, has historically served as the primary development focus. However, emerging deeper zones are expanding the technical and economic runway significantly.

Recent performance data indicates that wells in the Midland Basin's Barnett-Woodford interval have exceeded average basin results, with breakeven costs aligning in the low-$40 per barrel range under current cost assumptions. This deeper formation development represents a significant expansion of economically viable inventory beyond traditional Wolfcamp A-C targets.

The Spraberry Formation overlying the Wolfcamp provides additional horizontal development potential, whilst the Delaware Basin's Bone Spring Formation offers robust co-development opportunities. According to Enverus Intelligence Research, much of the incremental resource growth is concentrated in these emerging deeper zones, including Barnett-Woodford and Wolfcamp D intervals.

Infrastructure Density and Cost Advantages

The Permian Basin's established pipeline network connecting to major refining centres and export terminals provides a competitive transportation cost advantage. Multiple processing plants and compression facilities reduce midstream costs compared to basins requiring new infrastructure investment.

Key infrastructure advantages include:

• Pipeline connectivity to major Gulf Coast refining centres

• Processing capacity with established compression and treatment facilities

• Transportation networks reducing product delivery costs

• Service provider concentration supporting operational efficiency

• Supply chain maturity enabling cost optimisation through competition

When big ASX news breaks, our subscribers know first

High-Value Location Distribution and Development Trends

The concentration of premium drilling locations within the Permian Basin reflects both geological favourability and infrastructure accessibility. Understanding these distribution patterns has become essential for operators prioritising capital allocation across expansive acreage positions. Additionally, US drilling activity trends provide context for how market conditions influence development priorities.

Midland Basin Core Development Areas

The Howard, Martin, and Midland County corridor represents the highest concentration of proven, high-return drilling locations. These areas benefit from extensive well performance databases enabling sophisticated EUR (Estimated Ultimate Recovery) forecasting and completion optimisation.

Extended lateral drilling capabilities now routinely exceed 10,000 feet, with some operators pursuing laterals of 15,000 feet or more. This lateral extension increases location density per section whilst potentially improving per-well economics through increased reservoir contact.

Well spacing optimisation has evolved from historical 40-acre spacing to tighter configurations of 660-foot to 880-foot lateral spacing. This evolution reflects improved understanding of pressure communication and interference effects between parent and child wells.

Delaware Basin Expansion Corridors

Reeves County in Texas and Eddy and Lea counties in New Mexico represent primary Delaware Basin development areas with expanding permit activity. The strategic focus on Bone Spring and Wolfcamp co-development enables operators to develop multiple zones simultaneously, reducing cycle time and infrastructure costs per barrel of oil equivalent.

Produced water management solutions, including recycling and disposal strategies, have become critical operational considerations as development intensity increases. These water management systems enable sustained development whilst addressing environmental compliance requirements.

Emerging Zone Performance Metrics

The Barnett-Woodford interval emergence as a commercially viable play demonstrates the ongoing expansion of the basin's development inventory. Wells in this interval have recently demonstrated performance exceeding average basin results whilst maintaining breakeven costs in the low-$40 per barrel range.

This performance validation enables operators to expand their development portfolios beyond traditional targets, effectively extending drilling runway length and improving long-term inventory quality. The technical success of these deeper formations also validates enhanced completion designs and extended lateral drilling capabilities.

Economic Evaluation and Location Quality Assessment

Operators employ sophisticated screening criteria to evaluate drilling location quality across diverse geological and economic parameters. These assessment frameworks balance technical risk with economic returns whilst considering development sequencing implications. In addition, understanding oil production decline analysis helps inform strategic planning decisions.

Technical Screening Framework

Resource density metrics form the foundation of location evaluation, measuring barrels of oil equivalent per section across different formation intervals. These calculations incorporate reservoir thickness, porosity, and hydrocarbon saturation to estimate total recoverable volumes.

Completion optimisation analysis focuses on proppant loading and fracture stage design tailored to specific formation characteristics. Deeper formations such as Wolfcamp D and Barnett-Woodford may require different completion parameters than traditional Wolfcamp A targets, affecting both costs and ultimate recovery estimates.

Pressure depletion modelling has become increasingly sophisticated as operators address parent-child well interference effects. These studies inform optimal well spacing decisions and development sequencing to maximise recovery whilst minimising interference-related production losses.

Economic Return Analysis

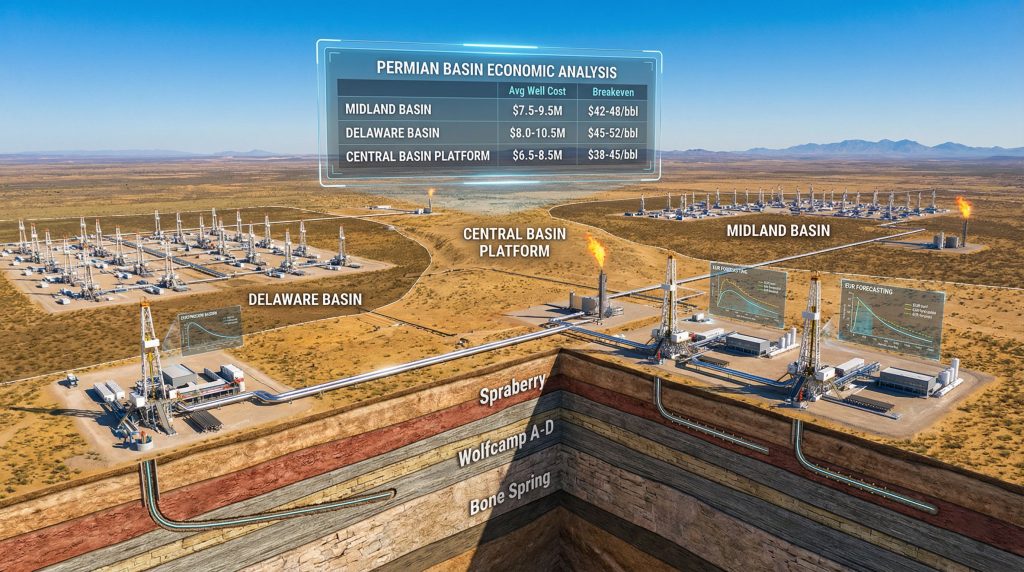

The following cost structure analysis reflects current market conditions across major Permian sub-basins:

| Economic Metric | Midland Basin | Delaware Basin | Central Platform |

|---|---|---|---|

| Average Well Cost | $7.5-9.5M | $8.0-10.5M | $6.5-8.5M |

| Breakeven Oil Price | $42-48/bbl | $45-52/bbl | $38-45/bbl |

| Peak Production Rate | 1,200-1,800 boe/d | 1,400-2,000 boe/d | 800-1,200 boe/d |

| 30-Year EUR | 850-1,200 Mboe | 950-1,350 Mboe | 650-950 Mboe |

These metrics demonstrate the economic variability across sub-basins, with the Delaware Basin commanding higher well costs but potentially delivering superior peak production rates and ultimate recoveries.

Development Sequencing Strategy

According to Enverus Intelligence Research, development sequencing is expected to play a larger role in determining project economics as operators shift toward more complex zones and maturing acreage. This sequencing optimisation balances immediate cash flow generation with long-term inventory preservation.

Cube development strategies enable simultaneous multi-zone targeting, reducing surface footprint whilst maximising reservoir recovery. This approach requires sophisticated coordination of drilling and completion operations but can significantly improve capital efficiency per barrel of oil equivalent produced.

Manufacturing drilling techniques, employing assembly-line completion processes, have reduced cycle times and operational costs. These standardised approaches enable operators to achieve economies of scale across large drilling programs whilst maintaining consistent well performance.

Technology-Driven Inventory Expansion

The 10% year-over-year growth in sub-$50 per barrel drilling locations reflects ongoing technological advancement and geological understanding. These improvements continue expanding the basin's economically viable inventory despite nearly two decades of intensive development. However, oil price movements overview demonstrates how market dynamics influence development timing and economics.

Enhanced Recovery Technologies

Extended lateral drilling capabilities now routinely exceed historical norms, with 15,000+ foot laterals becoming increasingly common. These extended reach capabilities increase location density per drilling unit whilst potentially improving well economics through increased reservoir contact.

Enhanced completion designs incorporating higher intensity fracturing programs have improved EUR performance, particularly in deeper formations. Increased proppant loading and optimised fracture stage spacing contribute to better reservoir stimulation and hydrocarbon recovery.

Downspacing feasibility studies demonstrate that tighter well spacing configurations can be achieved without proportional EUR degradation in many areas. This capability effectively increases location count within established acreage positions.

Geological Understanding Advances

Improved seismic imaging through 3D and 4D survey applications enhances subsurface understanding and reduces drilling risk. These advanced imaging techniques enable better fault identification, structural mapping, and sweet spot delineation within established fields. For comprehensive geological mapping resources, detailed Permian Basin maps provide valuable insights into formation characteristics.

Core analysis insights support completion optimisation by providing detailed rock property measurements and mechanical strength data. This information guides fracture design and proppant selection to maximise stimulation effectiveness.

Pressure communication studies quantify inter-well interference effects, enabling optimisation of well spacing and completion timing. Understanding these pressure dynamics helps operators minimise parent-child well interference whilst maximising ultimate recovery.

Resource Delineation Progress

Total undeveloped inventory approaches 100,000 locations when including geologically viable resources, according to Enverus Intelligence Research. This expansion reflects ongoing resource delineation efforts that continue identifying commercial development opportunities.

Recent additions have significantly expanded both location count and recoverable volumes, with much of the incremental resource concentrated in emerging deeper zones. The validation of Barnett-Woodford and Wolfcamp D intervals as commercial plays represents substantial inventory expansion beyond traditional development targets.

Operator Inventory Control and Market Dynamics

The distribution of high-quality drilling inventory among various operator categories reflects both historical acreage acquisition strategies and ongoing industry consolidation trends. Understanding these ownership patterns provides insight into competitive positioning and development capability. Furthermore, global market conditions and OPEC meeting impact influence regional development strategies.

Major Operator Positioning

Integrated oil companies including Chevron and ExxonMobil maintain substantial Permian Basin drilling locations acquired through strategic acquisitions and long-term acreage accumulation. These companies benefit from balance sheet strength enabling sustained development through commodity price cycles.

Independent producers such as Pioneer Natural Resources, ConocoPhillips, and EOG Resources have built focused Permian portfolios through targeted acquisitions and organic acreage development. Their operational specialisation often enables superior drilling and completion performance.

Permian specialists including Diamondback Energy, Coterra Energy, and Devon Energy concentrate their operations primarily within the basin, developing deep operational expertise and regional infrastructure advantages.

Private Operator Advantages

Enverus Intelligence Research notes that private and smaller operators hold a meaningful share of low-cost drilling locations, despite major operators controlling a significant portion of high-quality inventory. This distribution reflects several competitive dynamics:

• Capital flexibility enabling longer-term planning horizons

• Acquisition agility for bolt-on purchases and acreage consolidation

• Operational focus on specific geographic areas or formation targets

• Joint venture participation enabling risk sharing and capital efficiency

• Technology access through service provider partnerships and industry collaboration

Competitive Landscape Evolution

The competitive landscape continues evolving through ongoing merger and acquisition activity, joint venture formation, and acreage trading. Private equity backing has enabled numerous independent operators to compete effectively for high-quality drilling locations.

Market Insight: While major operators control substantial high-quality inventory, the fragmented nature of Permian ownership creates ongoing opportunities for focused operators to capture value through operational excellence and strategic positioning.

Market Conditions and Development Timing

Commodity price volatility significantly influences development timing across different quality tiers of drilling locations. Understanding these relationships enables operators to optimise capital allocation and preserve inventory value through price cycles.

Oil Price Sensitivity Framework

The basin's ability to sustain drilling activity through commodity price cycles reflects the depth of its sub-$50 per barrel inventory. Different price environments activate distinct location tiers based on economic return thresholds:

$40-50/bbl Price Environment:

• Core location development prioritisation

• Highest-return project focus

• Capital program reduction and efficiency emphasis

• Inventory preservation for higher-price environments

$50-65/bbl Price Environment:

• Tier-2 location activation

• Expanded drilling program execution

• Infrastructure investment acceleration

• Service capacity utilisation increase

$65+/bbl Price Environment:

• Full inventory development acceleration

• Marginal location commercial viability

• Maximum drilling program deployment

• Service cost inflation management challenges

Capital Market Influences

Access to capital markets significantly affects development timing and scope. Operators balance capital discipline with longer-term inventory management, as noted by Enverus Intelligence Research.

Debt capacity constraints limit drilling program scope through borrowing base limitations and financial covenant compliance requirements. These constraints become particularly relevant during low-price environments when cash flow generation declines.

Equity market access through public offerings and private placements enables development acceleration but requires investor return threshold satisfaction. Public companies face quarterly earnings pressures that may conflict with optimal long-term development sequencing.

Return threshold requirements typically target minimum IRR levels of 15-25% depending on risk profile and investor expectations. These thresholds influence location development prioritisation and completion design optimisation.

Service Sector Dynamics

Rig availability cycles affect development timing through drilling contractor capacity and pricing variations. Tight service markets can constrain development pace whilst creating cost inflation pressures.

Completion crew scheduling limitations affect fracturing equipment and personnel availability, potentially creating bottlenecks in drilling program execution.

Supply chain management including proppant and chemical procurement affects both costs and operational timing. Input cost volatility and transportation logistics require sophisticated procurement strategies.

The next major ASX story will hit our subscribers first

Long-Term Sustainability and Resource Management

The Permian Basin's long-term development sustainability depends on resource preservation, environmental stewardship, and technological advancement. Operators increasingly focus on optimising long-term value rather than maximising short-term production.

Resource Depletion Analysis

Decline curve analysis using extensive well performance databases enables sophisticated EUR forecasting and type curve development. These analytical frameworks inform long-term development planning and inventory valuation.

Pressure maintenance through waterflooding and enhanced recovery techniques may extend field life and improve ultimate recovery factors. Secondary recovery opportunities including CO2 injection could provide additional development phases in mature areas.

Enhanced oil recovery methods adapted from conventional reservoir management may find application in unconventional developments as primary production declines. These techniques could unlock additional value from existing well infrastructure.

Environmental Considerations

Water sourcing strategies increasingly emphasise brackish groundwater utilisation and produced water recycling to reduce freshwater consumption. These approaches address community concerns whilst reducing operating costs.

Air quality management through emission reduction technologies and continuous monitoring supports social licence maintenance and regulatory compliance. Advanced detection systems enable rapid response to potential environmental issues.

Community impact mitigation addressing traffic, noise, and infrastructure planning helps maintain positive relationships with local stakeholders. These considerations increasingly influence development planning and operational procedures.

Technology Evolution Impacts

Artificial intelligence applications in drilling optimisation and predictive maintenance could improve operational efficiency whilst reducing costs. Machine learning algorithms applied to historical performance data may identify optimisation opportunities not apparent through traditional analysis.

Automation advancement through unmanned operations and remote monitoring capabilities could reduce operating costs whilst improving safety performance. These technologies may enable economic development of currently marginal locations.

Carbon capture integration combining enhanced oil recovery with CO2 sequestration could create additional revenue streams whilst addressing environmental concerns. These integrated approaches may extend the basin's economic life beyond traditional depletion timelines.

Strategic Investment Framework and Market Implications

The Permian Basin's extensive drilling inventory creates unique investment opportunities across multiple risk and return profiles. Understanding these strategic implications enables informed capital allocation decisions in an evolving energy landscape.

Portfolio Diversification Benefits

Geographic risk distribution within a single region provides operational efficiency whilst reducing geological uncertainty. The basin's multiple sub-basins and formation targets enable diversification without sacrificing operational focus.

Formation risk mitigation through stacked pay zone development provides optionality as reservoir understanding evolves. Multiple formation targets within single acreage positions reduce exploration risk whilst providing development flexibility.

Operational scale advantages through shared infrastructure and service contracts improve capital efficiency. Large-scale operations enable negotiation of favourable service terms whilst spreading fixed costs across multiple projects.

Competitive Positioning Strategy

First-mover advantages in emerging zones such as Barnett-Woodford provide superior acreage positioning before widespread industry recognition. Early technical success enables strategic acreage accumulation at advantageous pricing.

Technology differentiation through proprietary completion and drilling techniques can create sustainable competitive advantages. Operational excellence becomes increasingly important as acreage quality equalises across major operators.

Integration opportunities connecting drilling operations with midstream and downstream assets enable value capture across the energy supply chain. Vertical integration can provide cost advantages and revenue diversification.

Future Scenario Planning

Energy transition timelines affect long-term oil demand trajectories and price assumptions. The basin's low-cost inventory provides resilience across various demand scenarios whilst maintaining development optionality.

Regulatory evolution at federal and state levels may influence development pace and environmental compliance costs. Operators must balance immediate development opportunities with evolving regulatory frameworks.

Global supply competition from international resource development and geopolitical factors affects long-term price assumptions. The basin's cost competitiveness provides strategic positioning regardless of global supply dynamics.

Investment Risk Assessment

Disclaimer: The analysis presented involves forecasts, geological assumptions, and economic projections that carry inherent uncertainty. Commodity price volatility, regulatory changes, and technological developments may significantly affect actual outcomes. Investors should conduct independent due diligence and consider professional consultation before making investment decisions.

The Permian Basin's 55,000 sub-$50 per barrel drilling locations represent a substantial inventory capable of sustaining development activity through various market conditions. The 10% annual growth in economically viable locations demonstrates the ongoing value creation through technological advancement and geological understanding.

As development shifts toward emerging deeper zones and operators balance capital discipline with inventory management, strategic positioning within these premier Permian Basin drilling locations remains critical for long-term value creation in the evolving energy landscape.

Are You Tracking the Next Major Energy Discovery?

Whilst the Permian Basin offers substantial drilling opportunities, Discovery Alert's proprietary Discovery IQ model scans the Australian markets for breakthrough mineral discoveries that could deliver exceptional returns. Historical examples from Discovery Alert's dedicated discoveries page demonstrate how major mineral finds can generate substantial market returns, often surpassing traditional energy sector opportunities. Begin your 14-day free trial today and position yourself ahead of the market with instant alerts on significant ASX mineral discoveries.