May 17, 2026

Understanding China's Precious Metals Investment Revolution

The global precious metals landscape has undergone a seismic shift as institutional capital allocation strategies increasingly favour hard assets over traditional financial instruments. This transformation reflects deeper concerns about monetary policy effectiveness, currency stability, and the sustainability of debt-driven economic models that have dominated investment thinking for decades. The precious metals craze in China exemplifies this broader trend, as central banks worldwide grapple with inflation control while maintaining growth, prompting investors to rediscover the fundamental role of precious metals as portfolio stabilisers and wealth preservation vehicles.

Economic uncertainty has intensified the search for alternative investment strategies, particularly in emerging markets where currency volatility creates additional layers of complexity for wealth management. Furthermore, the intersection of technological advancement, geopolitical tensions, and monetary policy divergence has created conditions where traditional asset pricing models require recalibration to account for structural changes in global capital flows.

When big ASX news breaks, our subscribers know first

Understanding China's Investment Market Evolution

China's precious metals investment landscape has experienced unprecedented transformation throughout 2025, driven by a convergence of monetary policy concerns, currency devaluation fears, and institutional portfolio diversification strategies. The People's Bank of China's accommodative policies, combined with global liquidity conditions, have prompted both institutional and retail investors to seek alternative stores of value beyond conventional financial instruments.

This shift represents a fundamental departure from China's historically industrial-focused approach to precious metals consumption. Where silver, gold, and platinum were previously viewed primarily as manufacturing inputs for electronics, solar panels, and industrial applications, they have now emerged as sophisticated investment vehicles attracting significant capital from domestic wealth management strategies.

The precious metals craze in China has been amplified by the development of accessible investment products that democratise exposure to these traditionally institutional asset classes. Listed Open-Ended Funds (LOFs) and Exchange-Traded Funds have created new pathways for retail participation, enabling investors to gain exposure to precious metals without the complexities of physical storage or international market access.

Consequently, social media platforms have accelerated this transformation by facilitating knowledge transfer regarding arbitrage opportunities and investment strategies. Educational content regarding precious metals investing has proliferated across Chinese digital platforms, creating informed investor communities that actively pursue sophisticated trading strategies previously limited to professional market participants.

Investment Vehicle Development and Market Access

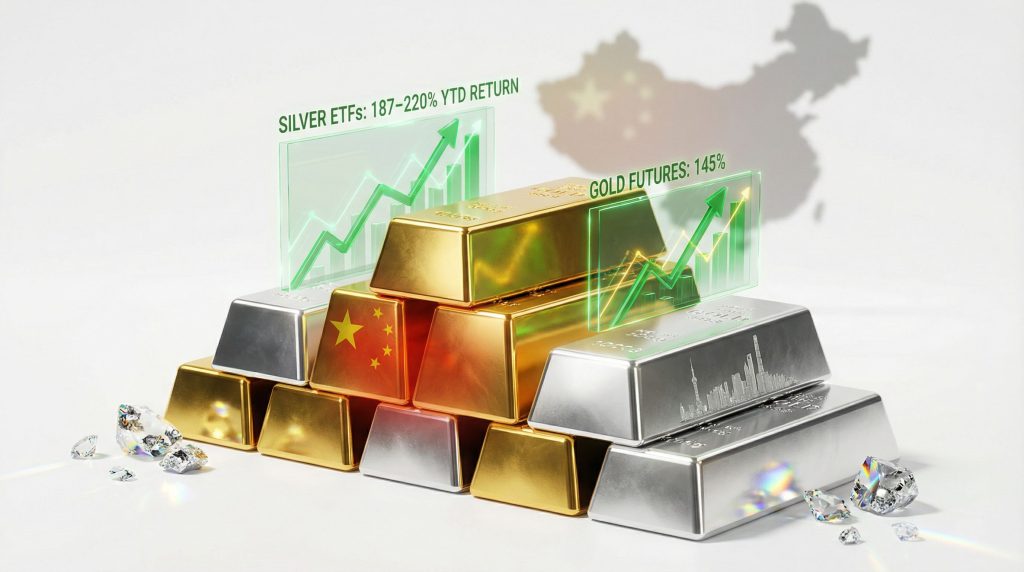

The emergence of specialised precious metals investment products has fundamentally altered China's financial landscape, creating unprecedented opportunities for retail and institutional investors to participate in global commodity markets. The UBS SDIC Silver Futures Fund LOF exemplifies this evolution, generating remarkable returns of 187% year-to-date in 2025 while providing domestic access to international silver price movements.

Listed Open-Ended Funds operate through a dual-trading mechanism that enables both exchange-based trading between investors and direct transactions with fund management companies. This structure creates unique arbitrage opportunities when market premiums develop between exchange prices and underlying asset values, attracting sophisticated investors who exploit these pricing inefficiencies.

The fund experienced extreme premium expansion, reaching over 60% above its underlying silver futures contracts during peak speculation periods in December 2025. This premium structure indicates intense domestic demand that exceeded available supply through traditional investment channels, forcing investors to pay substantial premiums for convenient precious metals exposure.

Key Investment Product Performance (2025)

| Product Category | Year-to-Date Performance | Peak Premium Level | Regulatory Response |

|---|---|---|---|

| Silver LOFs | 187% returns achieved | 60% above NAV | Subscription restrictions |

| Shanghai Silver Futures | 145% price appreciation | Moderate premiums | Enhanced monitoring |

| Gold Investment Products | Significant gains | 7-15% premium range | Standard oversight |

Regulatory interventions became necessary as speculation intensified, with fund management companies implementing subscription limits to protect investors from potential market reversals. The reduction of Class C share subscription limits from 500 yuan to 100 yuan ($14.26) demonstrates proactive risk management in response to unsustainable premium levels.

Pricing Dynamics and Geographic Arbitrage

Chinese precious metals markets consistently trade at premiums to international benchmark prices, reflecting the intensity of domestic demand relative to available supply channels. Shanghai Gold Exchange and Shanghai Futures Exchange pricing demonstrates persistent divergence from London and New York markets, creating potential arbitrage opportunities for investors with access to multiple geographic markets.

Current market data reveals silver trading at approximately $77 per ounce on international markets, while Shanghai markets maintain premiums that reflect domestic supply constraints and investment demand intensity. This pricing structure suggests either regulatory barriers limiting international arbitrage or domestic demand levels that exceed international traders' willingness to supply Chinese markets.

The gold-silver ratio analysis based on current pricing ($4,552 gold, $77 silver) indicates a ratio of approximately 59:1, significantly different from historical norms that often ranged closer to 80:1. This ratio compression suggests either relative silver strength or gold weakness, influencing investor perceptions about relative value opportunities between precious metals categories.

Geographic pricing disparities create complex considerations for international investors seeking exposure to Chinese precious metals demand. However, transaction costs, regulatory barriers, and currency hedging requirements must be evaluated against potential arbitrage profits when considering cross-border precious metals strategies.

Industrial Consumption Versus Speculative Demand

China's position as the world's largest silver consumer creates a unique dual-demand structure where industrial requirements establish baseline consumption while investment speculation adds volatile additional layers. Electronics manufacturing, solar panel production, and emerging technological applications maintain steady industrial demand that provides fundamental support for precious metals prices.

The transformation from viewing silver as purely an industrial commodity to recognising its investment potential represents a significant mindset shift among Chinese market participants. Global silver markets gained approximately 150% during 2025, fundamentally altering investor perceptions about precious metals as portfolio components rather than manufacturing inputs.

Traditional jewellery purchases have experienced notable declines as consumers redirect spending toward investment-grade precious metals products. This behavioural shift reflects changing wealth preservation strategies, where consumers prioritise purity and liquidity over decorative applications for their precious metals holdings.

Consumer Demand Transformation Indicators

- Industrial consumption maintains baseline support

- Investment demand creates price volatility

- Jewellery purchases decline in favour of investment products

- Social media education accelerates investment adoption

- Retail investors seek leveraged precious metals exposure

The precious metals craze in China has created conditions where investment demand can rapidly amplify or dampen price movements beyond what industrial consumption alone would justify. This dynamic creates both opportunities and risks for investors seeking exposure to Chinese precious metals markets.

Supply Chain Constraints and Inventory Analysis

Global precious metals markets face structural supply challenges that have intensified throughout 2025, creating conditions supportive of continued price appreciation. Production constraints, exploration limitations, and mine development delays contribute to supply-side tightness that amplifies the impact of increased Chinese investment demand.

Mining industry analysts observe that new precious metals production requires substantial lead times for exploration, permitting, and development phases that can span decades. This supply inelasticity means that sudden demand increases, such as those experienced in Chinese investment markets, cannot be quickly addressed through increased production.

Inventory management across major exchanges reflects the tension between growing investment demand and limited supply availability. While specific inventory figures require verification through official exchange publications, the general trend toward inventory depletion supports the thesis of structural supply shortages affecting global precious metals markets.

Supply-Demand Balance Considerations

- Mine production requires multi-year development timelines

- Exploration success rates remain historically challenging

- Environmental regulations increase development costs

- Chinese demand growth outpaces supply expansion

- Secondary supply (recycling) provides limited relief

Furthermore, regulatory export controls and licensing requirements add additional complexity to international precious metals supply chains. These administrative barriers can create artificial supply constraints that amplify natural market tightness, particularly during periods of intense regional demand such as the current precious metals craze in China.

The next major ASX story will hit our subscribers first

Economic Implications and Future Market Trajectories

The intensity of China's precious metals investment boom reflects broader concerns about traditional financial system stability and currency depreciation risks. Institutional and retail investors alike are repositioning portfolios to include hard assets as hedges against potential economic turbulence, indicating reduced confidence in conventional investment vehicles.

Central banking policies across major economies continue to maintain accommodative stances despite inflation concerns, creating conditions where precious metals offer potential protection against currency debasement. The combination of low real interest rates and quantitative easing programmes provides fundamental support for precious metals as alternative stores of value.

In addition, the historic gold surge and gold price forecast 2025 suggest continued momentum in precious metals markets. China's domestic precious metals consumption patterns increasingly influence global pricing mechanisms, particularly given the country's significant industrial demand combined with growing investment appetite.

The silver market squeeze has been particularly pronounced, with analysts from China's precious metals investment surge noting unprecedented fund subscription demand. Meanwhile, Asian precious metals trading has reached record highs amid holiday trading periods.

Projected Market Development Scenarios

| Economic Scenario | Chinese Demand Impact | Global Price Effect | Investment Implications |

|---|---|---|---|

| Continued Growth | 20-25% annual increase | Strong upward pressure | Sustained precious metals strength |

| Economic Slowdown | 10-15% demand growth | Moderate price support | Defensive portfolio positioning |

| Policy Intervention | Demand normalisation | Price consolidation | Reduced speculation premium |

The macroeconomic environment suggests continued support for precious metals investments, with Chinese demand serving as a significant driver of global market dynamics. However, regulatory interventions and potential market maturation could moderate the extreme speculation characteristics observed during 2025.

Investment Strategy Considerations and Risk Management

International investors seeking exposure to precious metals markets must carefully evaluate the spillover effects from Chinese market volatility and regulatory intervention risks. The extreme premiums and rapid policy responses observed in Chinese markets create uncertainty that extends beyond domestic boundaries to affect global precious metals pricing.

Currency hedging considerations become particularly important when investing in precious metals markets influenced by Chinese demand. Exchange rate fluctuations between the Chinese yuan and major reserve currencies can significantly impact the relative attractiveness of precious metals investments for Chinese participants, creating feedback effects on global markets.

Portfolio diversification strategies should account for the correlation patterns between Chinese economic policy, domestic precious metals demand, and international commodity prices. For instance, the US-China trade impact demonstrates how regional investment trends can create global market implications that require sophisticated risk management approaches.

Risk Management Framework Elements

- Geographic diversification of precious metals exposure

- Understanding of Chinese regulatory cycle patterns

- Currency hedging for international investors

- Monitoring of social media-driven speculation trends

- Position sizing appropriate for volatility levels

Professional investment managers must balance the opportunities created by Chinese precious metals demand against the risks associated with regulatory unpredictability and market speculation. The development of China's precious metals investment infrastructure suggests continued evolution that will influence global markets regardless of short-term speculation cycles.

Investment Considerations for 2025

The transformation of China's precious metals markets from industrial consumption to sophisticated investment strategies represents a fundamental shift in global commodity dynamics. While regulatory interventions may moderate short-term speculation, the underlying drivers of Chinese precious metals demand suggest continued influence on international markets as economic uncertainty persists and investment strategies evolve.

Investment Disclaimer: Precious metals investments carry significant risks including price volatility, regulatory changes, and market speculation effects. The information presented reflects market conditions as of December 2025 and should not constitute investment advice. Prospective investors should consult qualified financial professionals and conduct independent research before making investment decisions. Past performance does not guarantee future results, and all investments carry the risk of loss.

Consequently, the precious metals craze in China represents more than a temporary speculative phenomenon—it signals a fundamental revaluation of hard assets within modern portfolio construction. As traditional financial instruments face increasing scrutiny amid global monetary policy uncertainty, the Chinese market's embrace of precious metals investment vehicles may serve as a harbinger of broader institutional adoption worldwide.

Ready to Capitalise on the Next Precious Metals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, instantly empowering investors to identify actionable opportunities ahead of the broader market. Explore Discovery Alert's dedicated discoveries page to understand why historic discoveries can generate substantial returns, then begin your 30-day free trial to position yourself ahead of the market.