June 16, 2026

The Geology Is Not the Problem: Why Rare Earth Processing Concentration Defines the Real Crisis

Rare earth elements sit beneath the surface of dozens of countries across six continents. They are not, in the conventional sense, scarce. The term "rare" was coined not because these seventeen elements are geologically unusual, but because they almost never appear in concentrations dense enough to mine economically, and almost never in deposits that contain only the elements you actually want. This geological nuance matters enormously, and it is central to understanding rare earth supply chain diversification as a policy and investment challenge.

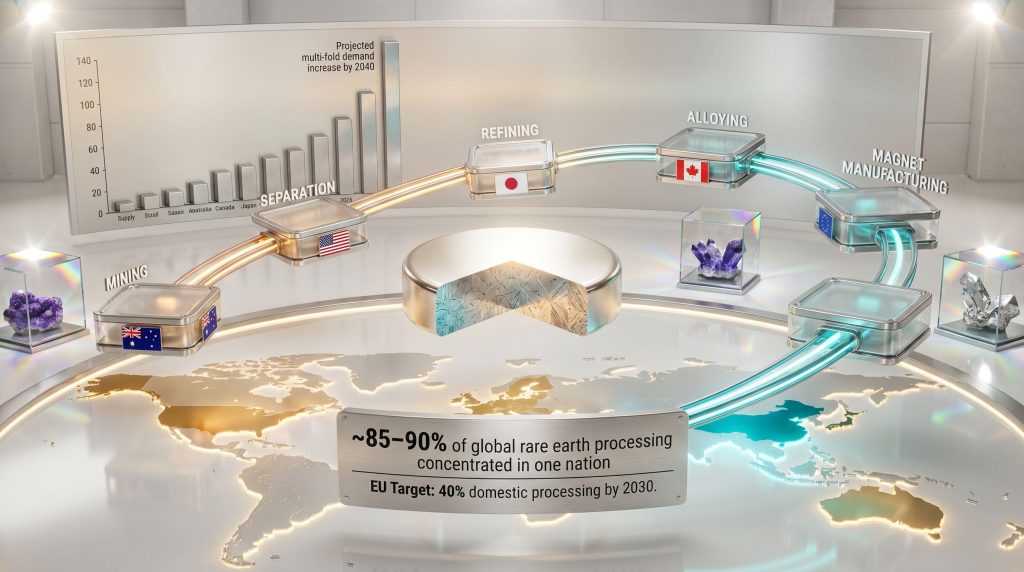

That second question is where the real supply chain crisis lives. According to data compiled by the United States Geological Survey (USGS), China has consistently accounted for roughly 85 to 90 percent of global rare earth separation and processing capacity, even as its share of raw mine output has declined somewhat as projects in Australia, the United States, and Myanmar have expanded. The distinction between ore extraction and processing is the central tension in rare earth supply chain diversification, and it is the reason that well-funded mining ambitions in Western nations have not yet translated into genuine supply security.

When big ASX news breaks, our subscribers know first

Understanding the Full Mine-to-Magnet Value Chain

The Five Stages Most Discussions Skip Past

A productive way to understand rare earth supply chain diversification is to map the full value chain rather than treating mining as the primary goal. The journey from geological deposit to finished permanent magnet involves five distinct stages, each with its own capital requirements, technical barriers, and geopolitical footprint:

-

Mining – extracting ore bearing rare earth minerals from the earth, typically through open-cut or underground methods depending on deposit geometry.

-

Mineral separation – physically separating the rare earth mineral concentrate from gangue material using flotation, magnetic separation, or gravity methods.

-

Chemical separation and refining – the most technically demanding stage, where individual rare earth oxides are isolated using solvent extraction circuits involving dozens of sequential mixer-settler stages.

-

Alloying – converting refined rare earth oxides into metals and alloys, particularly neodymium-iron-boron (NdFeB) alloy, which forms the feedstock for permanent magnets.

-

Magnet manufacturing – pressing, sintering, and finishing NdFeB magnets to precise specifications for use in electric vehicle motors, wind turbine generators, robotics, and defence systems.

Western investment has largely concentrated at stage one and, to a lesser degree, stage two. The critical bottleneck sits at stages three through five, where China's decades of investment in hydrometallurgical infrastructure have created a practical monopoly that cannot be replicated quickly. As outlined in analysis of rare earth processing challenges, building a commercial solvent extraction facility requires not just capital, but specialised chemistry knowledge, trained operators, and environmental approvals that can take years to obtain in jurisdictions with rigorous regulatory frameworks.

Why Heavy Rare Earths Present a Harder Problem

The rare earth family divides broadly into light rare earth elements (LREEs), such as lanthanum, cerium, praseodymium, and neodymium, and heavy rare earth elements (HREEs), including dysprosium, terbium, erbium, and yttrium. This classification is not merely chemical but commercially and strategically significant.

LREEs are more geologically abundant and more widely distributed across known deposit types. HREEs, by contrast, are primarily sourced from ion-adsorption clay deposits, a deposit type concentrated in southern China, and from a small number of other deposit styles such as carbonatites and alkaline intrusions. Dysprosium and terbium, both HREEs, are essential additives to NdFeB magnets to maintain coercivity at elevated operating temperatures, which is critical for EV motors and wind turbine generators that experience significant heat cycling.

This means the HREE supply security problem is structurally more difficult than the LREE problem. Even if Western nations successfully build neodymium and praseodymium processing capacity, dependency on Chinese-sourced dysprosium and terbium could persist for much longer, creating a meaningful residual vulnerability in the magnet supply chain.

What Is Driving the Urgency for Rare Earth Diversification in 2025-2026?

Demand Acceleration From Clean Energy Transitions

The International Energy Agency's landmark 2021 report on critical minerals in clean energy transitions provided the most widely cited quantitative foundation for rare earth demand projections. Under scenarios aligned with the Paris Agreement, the IEA projected that rare earth demand for clean energy applications could increase several-fold by 2040 relative to 2020 baseline levels, with electric vehicle motors and direct-drive wind turbines representing the dominant demand growth vectors.

This projection has since been reinforced by country-level EV adoption targets across the United States, European Union, Japan, South Korea, and China itself. The scale of EV production required to meet these targets implies a corresponding increase in NdFeB magnet demand that current non-Chinese supply chains cannot come close to satisfying. Furthermore, the critical minerals demand driven by wind energy expansion compounds this pressure, as offshore wind turbines utilising direct-drive generators consume substantially more rare earth magnet material per megawatt of installed capacity than conventional geared designs.

Defence and aerospace applications add a strategic demand layer that operates independently of commodity market dynamics. Precision-guided munitions, radar systems, sonar arrays, and advanced aircraft all incorporate rare earth components where there is no acceptable performance substitute, creating a demand floor that is insensitive to price and largely insulated from commercial procurement decisions.

The 2010 Precedent and Its Long Shadow

The episode that crystallised rare earth supply chain risk into policy consciousness occurred in 2010, when Chinese export quotas and effective shipment suspensions to Japan caused spot prices for certain rare earth oxides to surge by several multiples within months. Industry price reporting data from that period shows that some heavy rare earth oxide prices increased by more than tenfold before eventually subsiding. The WTO later ruled against China's rare earth export restriction regime in a 2014 dispute resolution decision, but the damage to buyer confidence in single-source supply chains had already been done.

The strategic lesson of 2010 was not lost on Japan, which accelerated its own diversification strategy, invested in overseas mine equity stakes, and committed significant resources to rare earth recycling research and motor design substitution. What Japan understood then is now being absorbed by the United States, European Union, and Australia: geological access and geopolitical access are fundamentally different things, and only the latter guarantees supply. China's export restrictions continue to demonstrate how rapidly this dynamic can reshape global markets.

Price Volatility as an Ongoing Commercial Catalyst

Beyond the acute 2010 shock, rare earth markets have exhibited persistent price volatility driven by the structural reality of supply concentration. When a single producing nation can influence both volumes and pricing through export policy decisions, downstream manufacturers face cost structure uncertainty that is qualitatively different from commodity price risk in more distributed markets. This volatility imposes a real option value on supply chain diversification: even if diversified supply costs more per tonne under normal conditions, the insurance value against price spikes and supply interruptions justifies a meaningful diversification premium for manufacturers with high rare earth content in their products.

Where Are Alternative Rare Earth Supply Chains Being Built?

United States: Rebuilding From Mountain Pass

The Mountain Pass mine in California's Mojave Desert represents the anchor of US domestic rare earth mining capacity. Operated by MP Materials, Mountain Pass holds the distinction of being the only operating rare earth mine in the United States and one of the highest-grade carbonatite-hosted rare earth deposits in the world. The facility's ore grades are among the highest of any producing mine globally, which provides a meaningful cost advantage at the mining stage.

However, the broader US domestic supply chain picture remains incomplete. Federal funding mechanisms have been deployed through the Department of Energy and the Department of Defense to support processing and magnet manufacturing projects, but the gap between current processing capacity and the scale required for genuine supply independence remains substantial. Permitting reform initiatives have been discussed as a pathway to accelerating project timelines, though environmental review processes for solvent extraction facilities remain complex and time-consuming regardless of policy intent.

Australia: Processing Ambition Beyond Ore Export

Australia holds one of the world's largest rare earth reserve bases outside China, anchored by deposits in Western Australia and the Northern Territory. Lynas Rare Earths, the largest rare earth producer outside China, operates the Mount Weld mine in Western Australia and has historically processed its ore in Malaysia, though the company has invested in building additional processing capability closer to the mine site.

The strategic shift underway in Australia involves moving beyond the historical model of exporting ore or partially processed material for separation elsewhere. Allied partnership frameworks, including defence and industrial policy alignment with the United States and Japan, are providing a geopolitical rationale for co-investment in Australian processing capacity that goes beyond purely commercial considerations. According to analysis from Benchmark Minerals, geopolitics will remain the primary driver of supply diversification decisions in the years ahead.

Europe: The Critical Raw Materials Act Framework

The European Union's Critical Raw Materials Act established binding diversification targets requiring that at least 40 percent of the EU's annual consumption of strategic raw materials be processed domestically by 2030. For rare earths, this represents a substantial departure from near-total import dependency. European rare earth processing projects are advancing in connection with Scandinavian and Greenlandic deposit development, with Greenland critical minerals representing both a significant resource opportunity and a geopolitically complex one, given the island's autonomous status within the Kingdom of Denmark and the intense international interest in its mineral wealth.

Japan and South Korea: The Technology-Led Model

Japan's post-2010 diversification playbook remains the most mature and instructive example for other importing nations. The strategy combined four elements simultaneously: securing equity stakes in overseas mines, investing in rare earth recycling infrastructure, funding substitution research to reduce per-unit rare earth intensity, and coordinating government-to-government supply agreements with producing countries. South Korea, with its significant NdFeB magnet manufacturing sector, has pursued a similar logic, treating upstream supply security as a prerequisite for maintaining competitive advantage in downstream industries.

Canada and Africa: Emerging Nodes in the Allied Network

Canadian rare earth projects, including carbonatite-hosted deposits in Ontario and Quebec, are advancing through feasibility stages with alignment to North American supply chain objectives reinforced by bilateral trade and industrial policy frameworks. In Africa, rare earth deposit development has become a focal point for competition between Western development finance institutions and Chinese investment, with countries including Tanzania, Madagascar, and South Africa hosting projects of strategic interest to multiple external parties.

The Biggest Barriers to Scaling Rare Earth Diversification

Why Capital Markets Hesitate

The financing challenge for rare earth projects is structural rather than cyclical. Project lead times from exploration to commercial production typically span ten to fifteen years, a timeframe that sits uncomfortably against the return horizons of most private equity and institutional capital. This is compounded by a well-documented pattern: China's ability to suppress rare earth spot prices during periods when Western investment is accelerating undermines the revenue projections that underpin project financing. Investors have witnessed this dynamic repeatedly, creating a rational reluctance to commit capital to projects whose commercial viability depends on prices remaining above a level that a single actor can influence.

Government risk-sharing instruments, including loan guarantees, strategic reserve purchase commitments, and procurement mandates, are therefore not merely policy tools but structural prerequisites for private capital mobilisation in this sector. Without a credible demand anchor provided by government off-take, most rare earth projects outside China face a financing gap that commercial terms alone cannot bridge.

The Workforce and Technical Barrier

The global shortage of rare earth processing expertise outside China is a less-discussed but equally binding constraint. Hydrometallurgical solvent extraction for rare earth separation requires a specific knowledge base that China has developed over decades of continuous operational experience. Training programs, research institution investment, and retention of the small community of non-Chinese rare earth processing experts represent long-lead human capital investments that are harder to accelerate than physical infrastructure.

The China Price Problem

Chinese rare earth producers, many operating with significant state enterprise involvement, have historically demonstrated the ability to sustain output at cost structures that undercut non-Chinese projects when market conditions require it. This creates a persistent commercial challenge: the economics of non-Chinese rare earth projects are most compelling when prices are elevated, but elevated prices are also the conditions most likely to trigger additional Chinese supply responses. Policy responses under consideration across multiple jurisdictions include import tariffs, strategic stockpile purchases, and content-based procurement mandates that create price-insensitive demand anchors for allied-supply material.

Recycling, Substitution, and the Long-Term Demand Picture

The Urban Mining Opportunity

Global rare earth recycling rates from end-of-life permanent magnets remain below 5 percent of available material, representing a substantial missed opportunity. The first generation of EVs sold between 2015 and 2020 is now beginning to approach end-of-life, creating an emerging feedstock stream of recoverable NdFeB magnet material. Technical barriers to rare earth recovery from end-of-life magnets include the difficulty of separating magnet alloys from complex assembled components without contamination and the energy intensity of reprocessing.

Policy frameworks requiring rare earth content labelling, design-for-disassembly standards, and manufacturer recycling obligations are being developed across the EU and, to a lesser extent, the United States. These frameworks will not deliver material volumes at scale within the current decade but represent a necessary foundation for building a closed-loop rare earth economy over the 2030s.

Substitution Research: Promising But Not Near-Term

Research programs targeting reduced heavy rare earth content in NdFeB magnets, including grain boundary diffusion techniques that concentrate dysprosium at magnet grain boundaries rather than distributing it throughout the bulk material, have achieved meaningful reductions in dysprosium consumption per kilogram of magnet. Alternative motor architectures, including switched reluctance motors and wound field synchronous motors, can reduce or eliminate rare earth magnet requirements but typically involve trade-offs in power density, efficiency, or manufacturing complexity that limit their applicability in high-performance EV drivetrains.

The realistic assessment is that substitution research will reduce the growth rate of heavy rare earth demand rather than eliminate it, and that primary supply diversification remains the central challenge regardless of substitution progress. Consequently, strengthening rare earth supply chains across allied nations remains the most critical near-term priority.

The next major ASX story will hit our subscribers first

What a Commercially Viable Rare Earth Supply Chain Outside China Requires

The Five Conditions for Structural Success

Strategic Insight: Policy researchers and industry analysts consistently identify five structural conditions as necessary for non-Chinese rare earth supply chains to achieve commercial sustainability: long-term offtake agreements, government demand anchors, processing hub co-investment, workforce development programs, and allied coordination frameworks.

-

Secured demand signals – long-term contracts from EV manufacturers, defence procurement agencies, and wind turbine producers providing revenue certainty across project payback periods.

-

Processing infrastructure – co-located or regionally proximate separation and refining capacity that captures value above the raw ore stage.

-

Government risk-sharing – loan guarantees, strategic reserve purchases, and procurement mandates that de-risk private investment against the China price problem.

-

Allied coordination – multilateral frameworks connecting mines, processors, and end users across politically aligned nations to build integrated non-Chinese supply chains.

-

Recycling integration – closed-loop systems and secondary supply pathways that reduce primary demand growth over time.

Key Data Summary

| Metric | Current Status | Target or Projection |

|---|---|---|

| China's share of global rare earth processing | ~85-90% | Policy targets aim to reduce below 50% by 2035 |

| US domestic rare earth processing | Limited, Mountain Pass primary site | Multiple projects in development stages |

| EU Critical Raw Materials Act target | Near-zero domestic processing | 40% of annual consumption processed domestically by 2030 |

| Rare earth demand growth (clean energy) | 2024 baseline | Projected multi-fold increase by 2040 (IEA) |

| NdFeB magnet production outside China | Minimal at commercial scale | Expansion projects active in US, EU, and Japan |

| Rare earth recycling rate (global) | Below 5% of end-of-life content | Policy frameworks targeting 20%+ recovery rates |

The 18-Month Window

Global law firm White and Case has assessed the current period as transitional for rare earth supply chain diversification, noting that US-led efforts to build alternative supply chains are moving from policy ambition toward commercial execution. The investment decisions being made now will determine the processing and magnet manufacturing capacity available to Western manufacturers in the early 2030s, when EV production volumes and wind energy installation rates are expected to create their most acute demand pressure.

The risk is not that diversification fails entirely, but that policy momentum generates strategy documents and feasibility studies without progressing to financial close on the processing and midstream infrastructure that actually delivers supply security. The gap between mining investment and processing investment has widened with each previous wave of rare earth diversification enthusiasm, and closing it in the current cycle requires simultaneous commitment across the full value chain rather than sequential investment that stalls at the ore extraction stage. The IEA's guidance on supply chain risks reinforces that new projects, partnerships, and policies must advance in tandem to achieve meaningful progress.

Frequently Asked Questions: Rare Earth Supply Chain Diversification

What are rare earth elements and why do they matter to supply chains?

The rare earth elements are a group of seventeen metallic elements comprising the fifteen lanthanides plus scandium and yttrium. Their critical supply chain importance derives from their irreplaceable functional roles in permanent magnets, phosphors, catalysts, and specialised alloys. The elements most strategically significant for clean energy and defence are neodymium, praseodymium, dysprosium, and terbium. The term "rare" reflects processing concentration rather than geological scarcity, as these elements are present in the earth's crust in concentrations comparable to many common industrial metals.

Which countries are furthest advanced in building mine-to-magnet capability?

Japan remains the most advanced non-Chinese nation in terms of integrated strategic planning, having initiated a coordinated diversification response after 2010. The United States is the furthest advanced in terms of near-term policy commitment and federal funding deployment, though its processing and magnet manufacturing capacity lags its mining capability. Australia is most advanced in ore production outside China and is actively developing separation capacity. The EU is at an earlier stage but has established the most binding policy framework through the Critical Raw Materials Act.

How long does it take to build a rare earth processing facility?

From initial project conception to commercial production, rare earth processing facilities typically require ten to fifteen years, encompassing exploration and resource definition, environmental impact assessment, permitting, engineering design, construction, commissioning, and ramp-up. Solvent extraction circuits for rare earth separation are among the most permitting-intensive chemical processing facilities due to the reagents involved and the management of radioactive co-products such as thorium that occur naturally in many rare earth ores.

What is the difference between light and heavy rare earths in supply terms?

LREEs, including neodymium and praseodymium, are more widely distributed geologically and present in large deposits across Australia, the United States, Canada, and Brazil. HREEs, particularly dysprosium and terbium, are primarily sourced from ion-adsorption clay deposits concentrated in southern China and a small number of other jurisdictions, making their supply chain more difficult to diversify and their geopolitical risk profile considerably higher.

Is recycling a realistic alternative to primary mining for rare earths?

In the near term, no. Current technical and economic constraints limit rare earth recovery from end-of-life magnets to a small fraction of available material. Over the medium to long term, as EV fleet volumes grow and policy frameworks mandate recovery, secondary supply could meaningfully supplement primary production, though industry analysts broadly agree that recycled material will reduce demand growth rather than replace primary supply as the dominant source.

The Strategic Outlook: From Aspiration to Execution

What the Next Phase Actually Requires

The defining test of the current rare earth diversification cycle is whether investment flows move decisively into processing and midstream infrastructure rather than concentrating again at the mining stage. Every previous wave of Western rare earth investment since 2010 has produced more mines and fewer separation facilities, perpetuating the processing gap that defines structural dependency.

Investors assessing the maturity of rare earth diversification projects should treat value chain completeness as a primary evaluation framework. A project that controls ore extraction but has no credible pathway to domestic separation and refining is not a supply chain solution; it is the upstream portion of a supply chain that still depends on the very concentration it is ostensibly designed to reduce.

Signals That Will Confirm Progress

The indicators that would confirm rare earth supply chain diversification has moved from transitional phase to structural reality include: financial close on processing and separation facilities outside China, long-term off-take agreements signed between non-Chinese processors and major EV or wind turbine manufacturers, and operational magnet manufacturing capacity in allied nations reaching a scale sufficient to supply a material fraction of domestic clean energy demand. Until those milestones accumulate, diversification remains a well-funded aspiration rather than an achieved structural condition.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Projections regarding rare earth demand growth, processing capacity targets, and policy outcomes involve inherent uncertainty and should not be relied upon as the basis for investment decisions. All statistics and forecasts cited are drawn from publicly available sources including the IEA, USGS, and official policy documents, and reflect conditions as reported at the time of their publication.

Readers seeking ongoing coverage of rare earth supply chain developments, critical mineral project updates, and global mining policy analysis can explore additional resources at Mining Magazine [https://www.miningmagazine.com], which publishes regular industry reporting and expert analysis relevant to rare earth diversification and critical mineral market dynamics.

Want to Track the Next Major Critical Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across rare earths and more than 30 other commodities — translating complex data into clear, actionable insights for investors at every level. Explore how historic mineral discoveries have delivered exceptional returns and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.