May 13, 2026

The Geological Clock Ticking Inside the World's Biggest Copper Nation

Long before copper prices become a headline, the real story is written underground. The grade of ore being extracted from a deposit, measured as the percentage of copper contained within each tonne of rock, determines everything that follows: the energy required, the water consumed, the capital deployed, and ultimately whether a mine remains economically viable at any given market price. When that grade declines, no amount of favourable pricing fully compensates for the deepening structural cost of extraction.

Chile's copper mining sector is living this reality in real time. The country sits atop the world's largest copper reserves and has long functioned as the backbone of global copper supply. Yet despite the record copper price in Chile's mining sector becoming a dominant market narrative in 2026, the nation's physical output has been trending in the opposite direction. Understanding why this divergence exists, and what it means for global supply chains, requires looking well past the price ticker.

When big ASX news breaks, our subscribers know first

When Revenue Growth Conceals a Production Crisis

Chile's copper export value reached $4.55 billion in January 2026, representing 7.9% year-on-year growth. On the surface, this looks like a sector firing on all cylinders. Dig deeper, however, and a more unsettling picture emerges.

That revenue growth was almost entirely the product of a 34% surge in copper prices, not any meaningful expansion in physical production volumes. The distinction is critical. Export revenue driven by price appreciation tells you something about global commodity markets. It tells you very little about the productive health of the mining sector generating those exports.

This is a pattern well-documented in resource economics. When commodity prices spike, fiscal receipts improve and export statistics look impressive. But if the volume of material being extracted is simultaneously declining, the underlying industrial capacity is weakening. Governments may temporarily benefit at the treasury level while the long-run productive base quietly erodes.

Furthermore, as noted by analysts monitoring record copper price pressures on Chile's mining sector, this dynamic is creating significant strategic risk for operators who may be misreading revenue signals as operational health.

Price-driven export growth is not the same as production-led export growth. One reflects market conditions; the other reflects industrial capacity. Conflating the two leads to policy complacency at exactly the wrong moment.

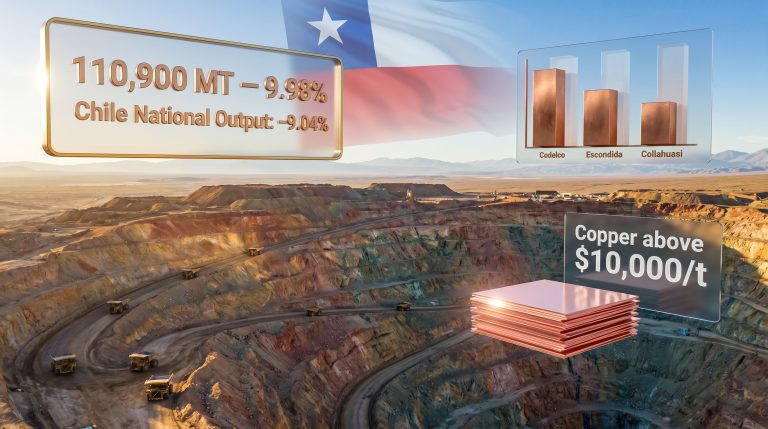

Chile recorded a 7% year-on-year production decline in the period leading into 2026, a figure that points firmly toward structural deterioration rather than a temporary cyclical dip. Five consecutive months of declining output reinforce the view that something more fundamental is underway. The Chile copper price forecast for 2025 had already flagged this divergence between price performance and volume recovery.

The Ore Grade Problem: Mining's Silent Margin Killer

To understand why Chile's production is declining despite elevated prices, it is necessary to understand ore grade dynamics. Copper ore grade refers to the concentration of copper within the rock being mined, typically expressed as a percentage. A deposit grading 1.5% copper contains 15 kilograms of recoverable copper per tonne of rock processed. A deposit grading 0.6% yields less than half that amount from the same volume of extraction effort.

Chilean copper deposits have been experiencing measurable, sustained grade decline for decades. Average ore grades across the country's major operations fell from approximately 1.2% around the turn of the millennium to roughly 0.8% by the early 2020s. That trajectory has continued. Lower grades mean:

- More rock must be mined to produce the same quantity of finished copper

- More energy is consumed per tonne of output

- More water is required for processing

- More waste material must be managed and stored

- Capital cost per pound of copper produced increases substantially

This grade deterioration is not confined to any single operator. It affects both state-controlled operations, most prominently those run by Codelco, Chile's national copper corporation, and internationally owned assets. The Chuquicamata deposit, one of the largest open-pit copper mines in history, has undergone a multi-billion dollar transition to underground operations in part because the accessible higher-grade ore near the surface has been substantially depleted.

What Is Driving the Record Copper Price in Chile's Mining Context?

The macro forces pushing copper to historic levels in 2026 are distinct from, though intertwined with, Chile's domestic production challenges. Several structural and cyclical drivers have converged:

- Monetary easing cycles across major economies have expanded global liquidity, historically positive for commodity valuations

- U.S. dollar weakness creates a mechanical lift for dollar-denominated commodity prices, as a softer dollar makes copper cheaper for non-dollar buyers, stimulating demand

- Inflation hedging demand has directed institutional capital into commodity allocations as a portfolio protection strategy

- Energy transition infrastructure buildout has structurally elevated copper demand forecasts, with electric vehicles, grid-scale battery systems, and renewable generation all requiring substantially more copper per unit than the technologies they replace

The benchmark figures illustrate the scale of the move. Copper reached a spot price peak of $5.02 per pound in 2026, with July COMEX futures trading around $4.7490 per pound, equivalent to approximately $10,470 per tonne.

Supply Constraints as a Price Amplifier

Here lies the self-reinforcing dynamic that commodity analysts find particularly significant. Chile's production declines are not merely a response to global copper market conditions. They are, in fact, actively contributing to those conditions. When the world's single largest national copper producer reduces its output, global supply balances tighten. Tighter supply, against a backdrop of robust or growing demand, pushes prices higher.

Higher prices, in theory, should incentivise more production. In Chile's case, however, this transmission mechanism is partially broken. The copper supply crunch facing the market means that elevated prices have not translated into volume recovery, a structural failure with long-term consequences.

Chile's Shrinking Share of Global Copper Supply

Chile remains the largest national copper producer globally, accounting for an estimated 24 to 27% of world copper supply. But that share has been gradually eroding. The competitive landscape has shifted, with other jurisdictions growing their production capacity while Chile's output has contracted.

| Country | Estimated Global Share | Production Trajectory |

|---|---|---|

| Chile | 24-27% | Declining |

| Peru | 10-12% | Moderately stable |

| Democratic Republic of Congo | 9-11% | Expanding |

| China | ~8% | Stable, domestic-focused |

| Australia | 4-5% | Growth-stage projects |

The DRC's expanding production trajectory is particularly noteworthy. The Congolese copper belt has attracted significant capital investment and is emerging as a more prominent swing producer. Australia, meanwhile, has several development-stage projects that could meaningfully increase its global share over the coming decade if sustained high prices justify the required capital expenditure.

Chile's copper supply role in balancing global markets remains critical, even as its proportional contribution comes under pressure from these competing producers.

Operational Headwinds Piling Up Across the Sector

The challenges confronting Chilean copper mining are layered and interconnected. No single factor explains the production decline. Instead, multiple operational pressures have compounded simultaneously.

Labour Relations and Industrial Disruption

Strike activity has been a persistent feature of Chile's mining industry. Labour disputes at major operations have interrupted production schedules across both state-owned and privately operated mines. Chile's mining workforce is highly unionised, and negotiations over wages, conditions, and profit-sharing arrangements frequently reach impasse. When production halts at an operation processing tens of thousands of tonnes of ore per day, the cumulative impact on annual output is measurable.

Infrastructure Constraints and Waste Management

Several flagship operations face physical limitations related to tailings storage. Tailings are the fine-grained waste material remaining after copper has been extracted from ore. As mines age and process larger volumes of lower-grade rock, the accumulation of tailings accelerates. Storage capacity constraints directly limit how much material a processing plant can handle, creating a physical ceiling on throughput.

Regulatory requirements around tailings storage facility construction and safety certification have also become more stringent, adding both capital cost and timeline uncertainty to expansion plans.

Energy Costs as a Structural Competitive Disadvantage

Chile's electricity costs for mining operations have historically ranked among the highest in Latin America. The country's reliance on imported energy sources and the significant transmission infrastructure required to supply remote Atacama desert operations have both contributed to elevated power costs.

For context, energy typically accounts for 20 to 30% of total mining operating costs. When those energy costs are structurally elevated relative to competing jurisdictions, the margin impact compounds the pressure already created by declining ore grades. The combination of lower grades and higher energy costs means more money spent to produce less copper.

Water Scarcity in the Atacama Region

The world's driest non-polar desert hosts some of its richest copper deposits. The Atacama's aridity creates a fundamental tension between mining operations that require substantial water for ore processing and communities and ecosystems that depend on already scarce groundwater resources.

Regulatory frameworks governing water use in the region have tightened progressively, and permitting for new or expanded water extraction has become more complex and time-consuming. Some operations have invested in seawater desalination and pipeline infrastructure to reduce dependence on Atacama groundwater, but this adds capital cost and energy consumption.

The next major ASX story will hit our subscribers first

The Investment Threshold Problem

Perhaps the most consequential long-term question facing the sector is whether current copper prices are actually high enough to justify the capital required to develop Chile's next generation of deposits.

Industry analysis suggests that bringing genuinely difficult, lower-grade, and deeper Chilean copper deposits into economic production may require sustained prices approaching $15,000 per tonne, a level meaningfully above where the market has been trading even during the 2026 price surge.

This creates a significant dilemma. The deposits that remain undeveloped in Chile tend to be the harder ones: deeper, lower-grade, more water-constrained, and more capital-intensive. The easier, higher-grade, surface-accessible deposits are largely already in production or depleted.

| Dimension | Short-Term Outlook | Long-Term Risk |

|---|---|---|

| Export revenue | Elevated due to price surge | Vulnerable if prices correct |

| Production volume | Declining | Requires major capital injection |

| New project development | Limited pipeline activity | Dependent on sustained high prices |

| Fiscal receipts | Temporarily improved | Structurally exposed to output decline |

| Global supply contribution | Shrinking share | Risk of market share loss to rivals |

Exploration Activity and the Reserve Replacement Gap

A mine produces copper by consuming its ore reserve. That reserve is not replenished by production — it is only replenished by exploration success that identifies and delineates new economic ore bodies. The critical question for Chile's long-term position is whether exploration activity is keeping pace with the rate at which existing reserves are being depleted.

The evidence suggests it is not. Exploration investment across Chile's mining sector has not matched the scale of reserve consumption. The combination of falling ore grades, rising development costs, regulatory complexity, and extended permitting timelines for new projects has deterred the level of capital deployment needed to build a robust pipeline of future production. The copper exploration importance cannot be overstated in this context, as reserve replacement is the only credible long-term solution to declining output.

The exploration-to-development timeline also creates a compounding lag. Even if a major new copper discovery were made in Chile today, the time required to complete feasibility studies, secure environmental permits, obtain community consent, arrange financing, and complete construction typically spans ten to fifteen years. There is no short-term fix to a long-term reserve depletion problem.

What Chile's Output Decline Means for Global Supply Chains

The implications of a sustained production decline at the world's largest copper-producing nation extend well beyond Chilean fiscal policy. Copper is the foundational metal of electrification. Every electric vehicle contains roughly three to four times more copper than a conventional internal combustion vehicle. Grid-scale energy storage systems, wind turbines, solar installations, and the transmission infrastructure required to connect them all depend on copper in substantial quantities.

The Codelco production outlook is one of the most closely watched indicators of whether Chile can arrest its decline. Furthermore, the International Energy Agency and multiple independent research bodies have projected that copper demand will grow significantly over the coming decade as energy transition investment accelerates. If that demand trajectory materialises against a backdrop of constrained Chilean supply and insufficient development of alternative sources, the global copper market faces a structural deficit that current price signals may not yet fully reflect.

If Chilean production were to contract by a further 10% from current levels, the resulting reduction in global refined copper supply would likely sustain prices well above historical averages and potentially accelerate capital deployment into previously marginal deposits across Australia, Canada, and parts of Africa.

This is the broader strategic significance of the record copper price in Chile's mining sector. It is not just a story about commodity markets or Chilean fiscal dynamics. It is a leading indicator for whether the global energy transition has access to the materials it fundamentally requires.

A Sector at a Genuine Strategic Inflection Point

The convergence of record copper prices with declining Chilean production forces a more honest assessment of where the sector stands. Revenue metrics look favourable. Productive capacity does not. The gap between what market prices suggest about copper's value and what operational realities are delivering in terms of Chilean output is widening in ways that demand serious attention from policymakers, investors, and industrial consumers alike.

The path forward for Chile's copper sector requires not just higher prices but sustained, credible policy frameworks that support long-term capital deployment; exploration incentives that encourage companies to fund the expensive, uncertain work of finding tomorrow's deposits; energy infrastructure investment that reduces the structural electricity cost disadvantage; and water solutions that make operations viable in arid regions without compromising ecosystems.

None of these challenges are insurmountable. However, none of them resolve themselves through price appreciation alone. That is the fundamental lesson the record copper price in Chile's mining sector is delivering to those paying close attention.

This article contains forward-looking statements and scenario analysis based on publicly available market data and industry frameworks. It does not constitute financial or investment advice. Readers should conduct independent research before making any investment decisions related to copper markets or mining sector equities.

Want to Capitalise on the Next Major Copper Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements to identify significant mineral discoveries — including copper — translating complex data into clear, actionable opportunities for investors at every experience level. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.