July 25, 2026

How Underground Gold Deposits in the Andes Are Reshaping Latin America's Precious Metals Supply Chain

The global gold mining industry has spent the better part of two decades grappling with a structural paradox: demand for new ounces continues to grow, yet the pipeline of technically viable, commercially sound underground projects capable of replacing depleting legacy assets has remained chronically thin. Nowhere is this tension more visible than across the Andean cordillera of South America, where some of the world's most geologically prospective ground collides with complex regulatory, environmental, and logistical realities. Against this backdrop, the San Gabriel gold project in Peru has moved from exploration-stage concept to producing mine, and its trajectory over the next several years will serve as a critical case study for how mid-tier gold producers can rebuild production profiles from the inside out.

When big ASX news breaks, our subscribers know first

What Is the San Gabriel Gold Project and Where Is It Located?

Situated within the District of Ichuña, Province of General Sánchez Cerro, in the Moquegua region of southern Peru, the San Gabriel project overview covers an underground gold and silver operation owned entirely by Compañía de Minas Buenaventura S.A.A. (NYSE: BVN), Peru's largest publicly listed precious metals producer. The deposit sits within a high-altitude Andean setting, a geography that carries both geological opportunity and operational complexity in equal measure.

From a technical standpoint, San Gabriel is classified as an intermediate-sulfidation epithermal deposit, hosted within calcareous Mesozoic rocks and associated with a diatreme structure. This geological classification is significant for several reasons that are not always well understood outside the technical mining community.

Understanding Intermediate-Sulfidation Epithermal Deposits

Epithermal gold deposits form at relatively shallow crustal depths, typically less than 1.5 kilometres below the ancient surface, from hydrothermal fluids circulating through volcanic and sedimentary rock systems. The intermediate-sulfidation classification sits between the two better-known end members of this deposit family:

- Low-sulfidation epithermal deposits tend to carry coarser, more free-milling gold in quartz vein systems, which generally respond well to straightforward cyanide leach processing.

- High-sulfidation epithermal deposits contain gold locked within refractory sulfide minerals, often requiring more complex and costly metallurgical treatment.

- Intermediate-sulfidation deposits like San Gabriel occupy a middle ground, featuring fine gold and chalcopyrite hosted within pyrite-siderite gangues, with mineralisation occurring across multiple structural styles simultaneously.

At San Gabriel specifically, mineralisation presents as blanket zones, stockwork networks, vein-like structures, and disseminated occurrences. Two primary mineralised domains have been defined: San Gabriel Sur (south) and San Gabriel Norte (north). This multi-domain architecture introduces both resource growth optionality and grade control complexity during production stope sequencing, a challenge discussed further in the operational risk section below.

The association with a diatreme structure is a particularly noteworthy geological feature. Diatremes are volcanic conduits formed by explosive gas-driven eruptions through overlying rock, and their chaotic breccia pipe geometries can create highly irregular ore body shapes that complicate both resource estimation and underground mine planning. Understanding the structural controls on gold distribution within San Gabriel's diatreme-hosted system has been a core technical challenge across the project's exploration and development history.

San Gabriel Gold Reserves, Mine Life, and Resource Base

The SK-1300 Reserve Estimate: What the Numbers Mean

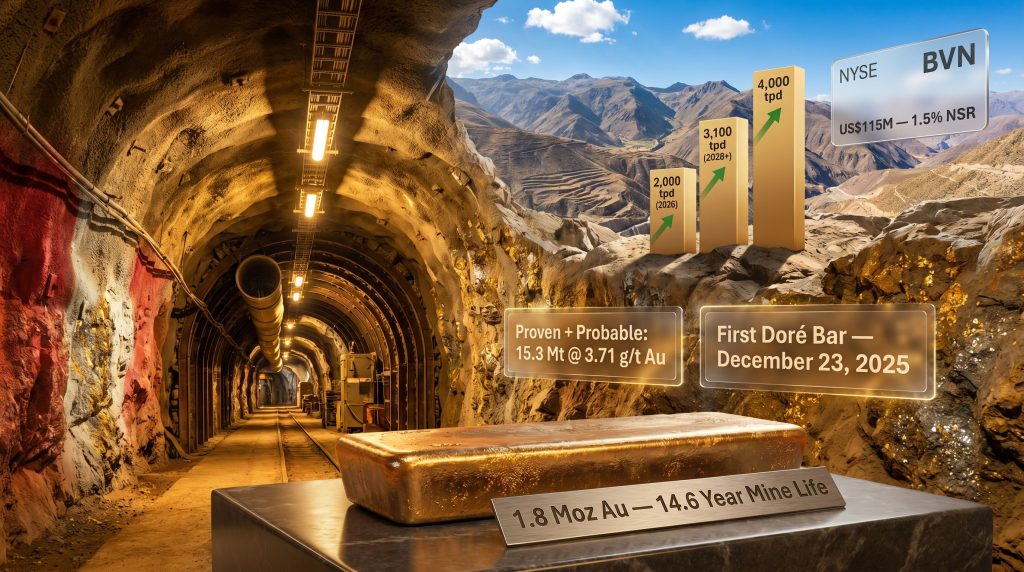

As of the April 2025 SK-1300 compliant reserve estimate, San Gabriel holds the following Proven and Probable reserves:

| Category | Tonnes (Mt) | Gold Grade (g/t Au) | Silver Grade (g/t Ag) | Contained Gold (Moz) | Contained Silver (Moz) |

|---|---|---|---|---|---|

| Proven + Probable | 15.3 | 3.71 | 6.32 | 1.8 | 3.1 |

The SK-1300 designation refers to the United States Securities and Exchange Commission's modernised mineral disclosure standard, which replaced the older Industry Guide 7 framework and requires mines to demonstrate economic viability under current market conditions before classifying material as reserves. This distinction matters to investors because SK-1300 compliant reserves carry stronger regulatory credibility than estimates prepared under older, less rigorous standards.

An average gold grade of 3.71 g/t Au across a reserve base of this scale is considered genuinely high-grade for an underground operation of San Gabriel's planned throughput. For context, the global average reserve grade across producing underground gold mines has declined steadily over the past three decades, with many operations now mining below 2.5 g/t. San Gabriel's grade profile, furthermore, meaningfully improves its unit economics relative to industry averages.

At current planned mining rates, the reserve base supports an estimated mine life of approximately 14.6 years, providing a long capital recovery runway and multi-decade production visibility. Importantly, the historical resource estimates from 2016 identified Measured and Indicated resources of 7.7 Mt at 5.7 g/t Au (1.4 Moz) and Inferred resources of 5.3 Mt at 4.6 g/t Au (0.8 Moz), suggesting the project has undergone substantial resource conversion and reserve growth through continued drilling over the intervening years.

Annual Production Targets Across the Expansion Roadmap

San Gabriel's production ramp is structured across three distinct throughput phases:

| Phase | Processing Throughput (tpd) | Targeted Gold Output | Target Timeline |

|---|---|---|---|

| Initial ramp-up | 2,000 | 70,000–80,000 oz Au | 2026 |

| Mid-term expansion | 3,100 | ~100,000–120,000 oz Au | 2028+ |

| Full-scale operation | 4,000 | Up to 150,000 oz Au | Post-2028 |

The silver by-product stream adds meaningful economic depth to the project. With 3.1 Moz of contained silver in the reserve base at 6.32 g/t Ag, silver credits will partially offset operating costs across the mine's life, improving all-in sustaining cost metrics in ways that pure gold reserve figures alone do not capture.

Capital Expenditure, Construction History, and the Budget Escalation Story

From US$430M to US$750M: Understanding Cost Escalation in Andean Mining

San Gabriel's construction cost trajectory is one of the more instructive capital discipline stories in recent Latin American mining history. The project was originally sanctioned with a capital budget of US$400–430 million. By the time construction reached completion, total capital expenditure had climbed to approximately US$750 million, representing a near-doubling of the original estimate.

The US$320+ million cost overrun at San Gabriel reflects a pattern observed broadly across Latin American underground mining projects commissioned between 2020 and 2024, where pandemic-era supply chain disruptions and global materials cost inflation inflated construction budgets by 40–80% across comparable developments in the Andean region.

The drivers of San Gabriel's cost escalation include:

- Pandemic-related construction delays that extended the project timeline and disrupted labour availability across multiple construction seasons.

- Global materials cost inflation, particularly for steel, cement, and specialised mining equipment, which saw dramatic price increases between 2021 and 2023.

- Extended permitting timelines that added carrying costs and required scope adjustments over the multi-year construction period.

- High-altitude logistical complexity inherent to Andean underground developments, where every tonne of equipment, reagent, and consumable must traverse challenging mountain road infrastructure.

Despite the cost overrun, a capital intensity analysis reveals the expenditure remains defensible. At 1.8 Moz of proven and probable gold reserves, the construction cost equates to approximately US$417 per reserve ounce. This figure sits within the range typically observed for comparable underground epithermal gold developments in Latin America, and compares favourably when measured against the all-in discovery and development cost cycles of greenfield projects brought into production during the same period.

Key Construction and Production Milestones

San Gabriel's development timeline charts a decade-long journey from regulatory approval to first metal:

- March 2017 – Environmental Impact Assessment (EIA) receives approval from Peruvian authorities.

- March 30, 2022 – Full government permits received, enabling formal construction commencement.

- Mid-2025 – Project reaches approximately 80% construction completion; plant startup testing scheduled.

- November 2025 – Initial gold production commences, as announced by Buenaventura.

- December 23, 2025 – First doré bar successfully produced, marking the definitive transition from construction to operational status.

- 2026 – Commercial production phase begins, targeting 2,000 tpd throughput and 70,000–80,000 oz Au output.

- 2028+ – Planned expansion to 3,100 tpd, with a longer-term pathway to 4,000 tpd.

The doré bar milestone on December 23, 2025 warrants specific attention. Doré is an unrefined gold-silver alloy poured directly from the smelting circuit at the mine site, prior to further refining at an off-site facility. Producing the first doré bar represents the culmination of the entire upstream development process and confirms that the full mining, processing, and smelting circuit is functioning as designed.

Why San Gabriel Is Strategically Central to Buenaventura's Future

Production Profile Transformation in the Mid-Tier Gold Sector

Buenaventura's 2024 total gold production reached approximately 109,300 oz, reflecting a 12.6% year-on-year decline consistent with the natural depletion trajectory affecting its existing portfolio of mature underground assets. This decline is not unique to Buenaventura. Across the global mid-tier gold producer segment, replacing depleting ounces through organic development rather than acquisition is among the most capital-intensive and operationally demanding challenges a mining company can undertake.

San Gabriel addresses this challenge directly. At full steady-state capacity, the project is projected to contribute 100,000–150,000 oz Au per annum, a volume that could nearly double Buenaventura's consolidated gold output relative to its 2024 baseline. Achieving this transformation through a single, wholly-owned underground project, rather than through dilutive mergers or expensive streaming arrangements that surrender future upside, represents a genuinely rare outcome in the mid-tier precious metals space.

The OR Royalties Transaction: Reading Third-Party Validation

In January 2026, OR Royalties completed the acquisition of a 1.5% Net Smelter Return (NSR) royalty on San Gabriel as part of a broader US$115 million portfolio transaction. For investors who may be unfamiliar with royalty mechanics, this transaction type deserves some unpacking. Understanding how mining royalty companies operate is, consequently, essential context here.

An NSR royalty entitles the holder to a fixed percentage of the gross revenue generated from metal sales at the mine, net of smelting and refining charges, for the life of the asset. Royalty companies do not bear any operating or capital costs; they simply receive their percentage of revenue from every ounce sold. This structure makes royalty valuations highly sensitive to production continuity and reserves confidence.

Royalty and streaming companies are widely regarded as the most rigorous independent technical validators in the mining finance ecosystem. Before committing capital to acquire a royalty on a producing or near-producing asset, these firms conduct exhaustive due diligence covering geology, metallurgy, permitting, infrastructure, and management capability. The OR Royalties transaction on San Gabriel, structured to deliver immediate Gold Equivalent Ounce (GEO) deliveries during 2026, signals a high degree of institutional confidence in the project's near-term production continuity and reserve quality.

Peru's Gold Sector: The Competitive and Macroeconomic Context

Where Peru Stands in Global Gold Supply

Peru currently ranks among the world's top ten gold-producing nations, holding approximately the ninth position globally as of recent production data. However, this ranking faces structural pressure. Several of Peru's largest and longest-operating gold mines are in advanced depletion phases, and the replacement pipeline of construction-ready projects has historically been thin relative to the output gap created by declining legacy assets.

Complicating matters further, Peru's artisanal and small-scale mining (ASGM) sector contributes a meaningful but highly volatile share of national gold output. The broader Peru mining political risk landscape makes large-scale, formally permitted operations like San Gabriel disproportionately important as stabilising anchors for national production accounting.

Comparative Positioning Among Major Peruvian Gold Operations

| Project / Mine | Operator | Annual Gold Output (Approx.) | Mine Type | Operational Status (2026) |

|---|---|---|---|---|

| San Gabriel | Buenaventura (BVN) | 70,000–120,000 oz (ramp-up) | Underground | Commercial ramp-up |

| Yanacocha | Newmont / Buenaventura JV | Declining; sulphides transition underway | Open pit / Underground | Transition phase |

| Lagunas Norte | Hochschild / Pan American | Reduced output | Open pit | Reduced operations |

| Shahuindo | Pan American Silver | ~100,000+ oz | Open pit | Operating |

Note: Output figures are approximate and derived from publicly available company disclosures. This table is presented for comparative context only and does not constitute investment advice.

The next major ASX story will hit our subscribers first

Operational and Technical Risks: What Could Slow the Ramp?

Underground Complexity and Grade Control Challenges

Intermediate-sulfidation epithermal deposits present specific operational challenges during production ramp-up that are worth understanding in detail. Unlike simple vein deposits where ore and waste contacts are visually obvious, multi-style mineralisation systems like San Gabriel's — featuring simultaneous blanket zones, stockworks, and disseminated occurrences within diatreme-influenced geometry — require precise geological modelling and rigorous grade control practices to avoid unplanned dilution.

Dilution occurs when waste rock or sub-economic material is inadvertently included with ore during mining. In high-grade underground operations, even modest dilution percentages can disproportionately reduce mill feed grades and processed metal recovery, compressing margins during the critical ramp-up window. Achieving consistent 2,000 tpd throughput at design grades during 2026 will depend heavily on:

- Stable ground conditions across active development headings.

- Reliable ore feed management from multiple stoping areas across both San Gabriel Sur and Norte domains.

- Optimised processing plant performance, particularly in the flotation and cyanide leach circuits responsible for gold recovery from fine-grained, sulfide-hosted mineralisation.

Regulatory and Social Licence Considerations

Peru's mining regulatory framework involves multiple agencies with overlapping jurisdictions, including the Ministry of Energy and Mines (MINEM), the Environmental Assessment and Enforcement Agency (OEFA), and regional and local government bodies with consultation rights under national and international frameworks protecting indigenous and community interests.

For San Gabriel, situated in the Ichuña district of Moquegua, maintaining community relations with local stakeholders is an ongoing operational obligation rather than a one-time approval process. Water management in high-altitude Andean environments carries particular sensitivity, as local communities depend on highland water sources for agriculture and pastoral activities. Mining-related hydrological changes can, furthermore, generate social friction even when operations remain technically compliant with environmental permit conditions.

The project's demonstrated track record — EIA approval in 2017 and full permit receipt in 2022 — provides a solid regulatory foundation. Active community engagement programmes, equitable local procurement, and transparent environmental monitoring remain essential to sustaining the social licence necessary for long-term operation.

Financial Implications: From Construction Burn to Cash Generation

Revenue Potential at Steady-State Production

Using a conservative gold price assumption of US$2,500 per ounce (below prevailing 2025–2026 spot prices), San Gabriel's projected steady-state output of 100,000 oz Au per annum implies approximately US$250 million in annual gross gold revenue. At expanded throughput targeting 120,000–150,000 oz, gross revenue potential at the same price assumption rises to US$300–375 million annually.

The silver by-product stream adds further revenue diversification. With 3.1 Moz of contained silver distributed across a 14.6-year mine life, annual silver production will contribute meaningful by-product credits that reduce net operating costs on a per-gold-ounce basis, improving all-in sustaining cost (AISC) competitiveness relative to gold-only peers.

Capital Efficiency Across the Mine Life

For resource sector analysts evaluating capital deployment efficiency, San Gabriel's metrics compare favourably to recent Latin American underground development benchmarks:

- Construction cost per reserve ounce: ~US$417/oz (US$750M total CAPEX / 1.8 Moz P+P reserves).

- Industry benchmark range for comparable underground epithermal projects in the Andean region: approximately US$350–600/oz.

- Mine life capital recovery runway: 14.6 years at current reserve base, with meaningful expansion potential as the 4,000 tpd throughput scenario unlocks incremental reserve conversion from the existing resource inventory.

The transition from the construction phase — which consumed substantial capital across a multi-year build — into operating cash generation represents a fundamental inflection point in Buenaventura's financial profile. Reduced leverage and improving free cash flow capacity are the natural financial consequences of a major project moving from development to production, and San Gabriel's ramp trajectory will be a key variable in Buenaventura's valuation across the 2026–2028 period.

Frequently Asked Questions: San Gabriel Gold Project in Peru

What type of deposit is San Gabriel?

San Gabriel is an intermediate-sulfidation epithermal deposit hosted within calcareous Mesozoic rocks and structurally associated with a diatreme. Gold mineralisation occurs across blanket zones, stockwork networks, vein-like structures, and disseminated occurrences, with fine gold and chalcopyrite present within pyrite-siderite gangue assemblages.

Who owns San Gabriel?

The project is 100% wholly owned by Compañía de Minas Buenaventura S.A.A. (NYSE: BVN), Peru's largest publicly listed precious metals mining company.

When was the first gold produced at San Gabriel?

The first doré bar was produced on December 23, 2025, marking the project's operational transition from commissioning into active gold production.

How much gold does San Gabriel produce annually?

The 2026 ramp-up phase targets 70,000–80,000 oz Au at initial throughput of 2,000 tpd. At full steady-state capacity, annual output is projected at 100,000–120,000 oz Au, with expanded throughput scenarios potentially reaching 150,000 oz per year.

What are San Gabriel's total gold reserves?

The April 2025 SK-1300 compliant estimate confirms 15.3 Mt of Proven and Probable reserves grading 3.71 g/t Au and 6.32 g/t Ag, containing approximately 1.8 Moz of gold and 3.1 Moz of silver.

How long is San Gabriel's mine life?

Based on current Proven and Probable reserves, the project carries an estimated mine life of approximately 14.6 years.

What did it cost to build San Gabriel?

Total capital expenditure reached approximately US$750 million, compared to an original project sanction estimate of US$400–430 million. The cost increase was driven by pandemic-related delays and global construction input inflation.

San Gabriel's Role in Peru's Long-Term Gold Production Outlook

The San Gabriel gold project in Peru is not simply another mine entering production in a country with a long mining history. It represents a structural inflection point for Buenaventura's production economics, a meaningful counterweight to the declining output trajectory of Peru's legacy gold asset base, and a benchmark development case for the broader challenge of building large-scale underground gold mines in the Andean region under modern regulatory, environmental, and community engagement standards.

Several dimensions of the project's significance deserve emphasis for those tracking the Peru gold industry outlook:

- The reserve grade of 3.71 g/t Au positions San Gabriel well above the global underground average, providing a cost-competitive foundation that should sustain margins across a wide range of gold price scenarios.

- The 14.6-year mine life at current reserves, combined with incremental resource conversion potential through ongoing exploration of the San Gabriel Norte and Sur domains, offers multi-decade production visibility that is increasingly rare in the mid-tier gold producer universe.

- The throughput expansion roadmap from 2,000 to 4,000 tpd provides a sequence of identifiable production growth catalysts across the 2026–2030+ window, each stage supported by incremental capital allocation rather than requiring a single large step-change commitment.

- Third-party validation through the OR Royalties NSR acquisition adds an independent layer of confidence that goes beyond the operator's own disclosures, reflecting the assessment of a specialised royalty institution with direct financial exposure to the project's output.

For resource sector participants and Peru mining watchers alike, San Gabriel's emerging gold role within Buenaventura's portfolio — and its performance through the 2026 ramp-up and into the first expansion phase — will establish whether Andean underground epithermal development at this scale can deliver on its technical and economic promise. The operational data generated over the next two to three years will be closely studied as a reference point for future project feasibility work across the region.

Disclaimer: This article is intended for informational and educational purposes only. It does not constitute financial or investment advice. Statements regarding production targets, reserve estimates, capital costs, and financial projections are based on publicly available company disclosures and industry sources. Actual outcomes may differ materially from projections due to operational, geological, regulatory, and market risks. Readers should conduct their own due diligence before making any investment decisions.

Want to Catch the Next Major Precious Metals Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including gold and silver opportunities — instantly translating complex geological and market data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the market.