July 15, 2026

The Hidden Fault Line in Western Battery Metal Supply Chains

When geopolitical pressure intersects with critical mineral supply chains, the consequences rarely stay contained to the companies directly involved. The global pivot toward electrification has created an uncomfortable dependency on a handful of refining nodes outside Chinese control, and the number of those nodes is now shrinking. Understanding why requires examining not just policy in isolation, but the physical geography of nickel and cobalt processing, and what happens when the politics surrounding those assets turn adversarial. Sherritt Cuba sanctions nickel cobalt dynamics sit at the very centre of this unfolding story.

Cuba's Moa Bay deposit sits at precisely this intersection. It is one of a small number of laterite nickel deposits in the Western Hemisphere capable of co-producing battery-grade cobalt at commercial scale. For decades, its output has flowed into a Canadian refinery that represents a genuinely rare asset: a North American nickel processing facility with no Chinese ownership stake. The chain of events now threatening that arrangement has been building for years, but 2026 brought it to a breaking point.

When big ASX news breaks, our subscribers know first

Why Cuban Nickel and Cobalt Carry Outsized Strategic Weight

Not all nickel is equal in the context of the energy transition. The industry draws a sharp distinction between Class 1 nickel (high-purity, battery-grade) and Class 2 nickel (lower-purity, primarily used in stainless steel and industrial alloys). Moa's laterite ore, processed through the pressure acid leach (PAL) method, yields Class 1 nickel sulphate and cobalt sulphate. Both are direct inputs into NMC (nickel manganese cobalt) and NCA (nickel cobalt aluminium) cathode chemistries used in EV batteries and grid storage systems.

This distinction matters enormously. While the industry has pursued cobalt-free battery architectures such as lithium iron phosphate (LFP), the highest energy-density applications — including long-range EVs and aerospace — continue to rely on cobalt-containing cathodes. Cobalt sourced as a co-product of nickel laterite processing at Moa is considered particularly valuable because it arrives in sulphate form, already suited for direct battery precursor manufacturing without additional conversion steps.

Cuba holds an estimated 5.5 million tonnes of nickel reserves, placing it among the top ten globally. Those reserves are concentrated in laterite deposits in the eastern Holguín province, where the Moa district is located. Furthermore, Moa's ore profile is more comparable to Indonesian or Filipino nickel laterites than to traditional Western sulphide mines, yet its processing destination — Alberta's Fort Saskatchewan refinery — anchors its output firmly within the Western supply chain. Understanding how this fits into the broader battery metals investment landscape helps clarify just how consequential any disruption would be.

"The Fort Saskatchewan facility processes Cuban laterite concentrate into refined nickel and cobalt products sold into European, Asian, and Canadian markets, entirely outside U.S. jurisdiction. This geographic arbitrage has historically been Sherritt's commercial lifeline and its central geopolitical vulnerability simultaneously."

What the 2026 U.S. Sanctions Actually Changed

The expansion of U.S. embargo measures in May 2026 introduced a qualitative shift in how sanctions pressure operates against Cuba's mining sector. Previous enforcement cycles targeted broad categories of Cuban state entities or imposed travel restrictions on company executives. The 2026 measures went further by specifically designating Moa Nickel S.A., the joint venture entity itself, alongside GAESA, Cuba's military-linked economic conglomerate.

This is a structurally different form of pressure. When a joint venture entity is directly sanctioned rather than simply its state-owned partner, the legal insulation that foreign operators have historically relied upon collapses. Any transaction touching Moa Nickel S.A. now carries U.S. person blocking requirements and secondary sanctions exposure for third-party financial institutions.

The practical cascade effects include:

- Banking access disruption: Correspondent banking relationships become untenable when transactions are linked to a designated entity, cutting off payment flows for operational expenses, contractor payments, and metal sales proceeds

- Insurance and shipping complications: Lloyd's-affiliated insurers and major shipping operators face their own sanctions compliance obligations, making cargo movement and coverage procurement difficult

- Offtake agreement enforcement risk: Long-term sales contracts become legally uncertain if counterparties or their financial institutions face secondary sanctions exposure for continuing the relationship

- Auditor and director risk tolerance: Professional services firms and board members face personal liability exposure for continued association with sanctioned operations, explaining the departures of Sherritt's CFO and auditor

This cascading effect is what distinguishes the 2026 escalation from prior Helms-Burton-era pressures. The Helms-Burton Act of 1996, which originally sanctioned Sherritt International — making it the first company designated under that legislation — operated primarily through Title III property claims and travel restrictions. The newer executive-order-based architecture works through the international financial system, making it far harder to route around through non-U.S. banking channels.

Sherritt's Strategic Risk Autopsy: How a Century-Old Miner Became Hostage to Geopolitics

Understanding the current crisis requires tracing a series of strategic decisions that, individually, appeared rational but cumulatively created catastrophic concentration risk.

Sherritt was founded in 1927 and named after Carl Sherritt, a trapper who identified copper deposits in Manitoba, Canada. The company's entry into Cuba was engineered by Ian Delaney following a corporate proxy contest in 1990, with an agreement signed with the Cuban government in 1991. At the time, the post-Soviet collapse had left Cuba's state-owned mining infrastructure severely underfunded, and Sherritt's offer to purchase unrefined nickel from the nationalised Moa mine filled a critical commercial gap.

The joint venture formalised in 1994 created an integrated supply chain: Moa mined the ore, Sherritt's Fort Saskatchewan refinery in Alberta processed it, and the refined products were sold into markets that had no U.S. jurisdiction concerns. For over a decade, this model generated exceptional returns.

The inflection point came with an ambitious expansion into Madagascar. The Ambatovy nickel project, a massive laterite development in which Sherritt held a significant stake, became one of the most capital-intensive mining ventures of its era. By 2013, the debt burden associated with this expansion had reached nearly CAD $2.5 billion, coinciding with a post-2014 collapse in nickel prices that made servicing that debt structurally impossible without Cuban cash flows.

The result was a forced asset sale programme that stripped Sherritt of its Canadian coal business and other diversifying assets, leaving Cuba as the overwhelmingly dominant revenue source precisely when that concentration became most dangerous.

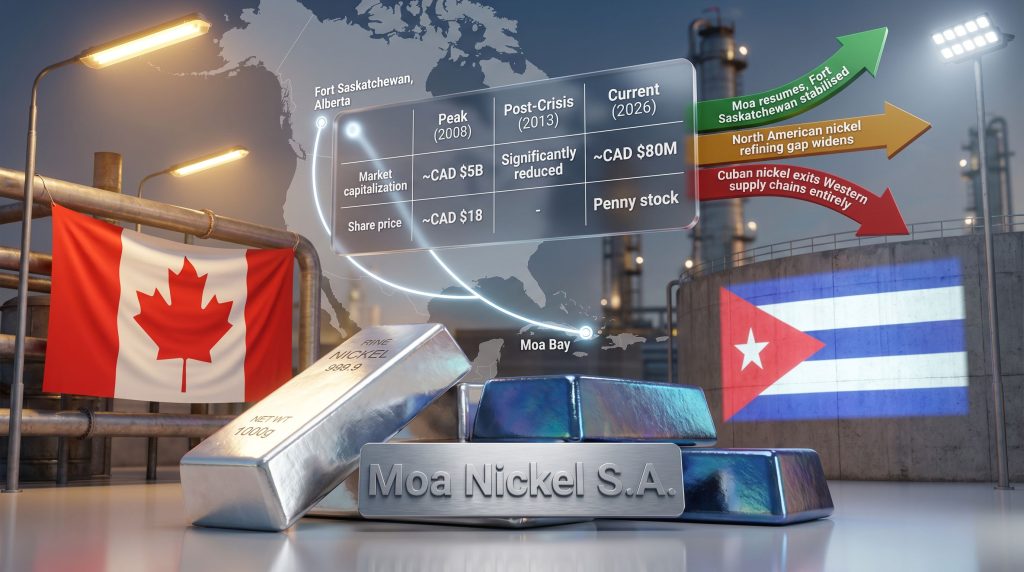

| Metric | Peak (2008) | Post-Crisis (2013) | Current (2026) |

|---|---|---|---|

| Market Capitalisation | ~CAD $5 billion | Significantly reduced | ~CAD $80 million |

| Share Price | ~CAD $18 | Sustained decline | Penny stock territory |

| Debt Load | Moderate | ~CAD $2.5 billion | Restructured |

| Cuba Asset Concentration | High | Very high | Over 70% of asset base |

By 2026, Sherritt was operating with only two directors following board departures, its CFO had resigned, and its auditor had stepped back. These governance indicators are not merely corporate housekeeping details; they are forward-looking signals about a company's capacity to navigate complex negotiations or execute a structured wind-down.

The Venezuelan Fuel Cascade and Fort Saskatchewan's Countdown

The immediate operational crisis at Moa did not originate directly from the 2026 sanctions announcement. It began earlier, as U.S. sanctions targeting Venezuelan oil exports created secondary disruptions to Cuba's fuel supply infrastructure. Venezuela has historically been Cuba's primary petroleum supplier, and when that supply chain was constrained, Moa's energy-intensive hydrometallurgical operations became untenable.

In February 2026, Sherritt halted its plan to dissolve the Cuba nickel venture and announced a suspension of Moa operations due to the inability to fulfil scheduled fuel delivery commitments. This is a technically significant detail: pressure acid leach processing requires sustained high-temperature, high-pressure operations. Fuel interruptions cannot be compensated for with partial supply, as the chemistry demands consistent thermal conditions.

The downstream consequence was clear and time-bound. Fort Saskatchewan's refinery inventory of nickel and cobalt feed material was projected to be exhausted by June 2026 based on Sherritt's own reporting. After that point, without fresh feed from Moa, the refinery would have no material to process.

The strategic significance of Fort Saskatchewan cannot be overstated in this context:

- It is one of only a small number of nickel refining facilities operating in North America outside Chinese corporate control

- It produces battery-grade nickel sulphate and cobalt sulphate suitable for direct cathode precursor manufacturing

- Its processing capacity cannot be quickly substituted by other facilities given the capital intensity and permitting timelines for new hydrometallurgical plants

- Its idling would represent a concrete reduction in Western refining capacity at precisely the moment that governments are investing in supply chain diversification away from Chinese processing dominance

"According to analysis from Northstream Capital, Fort Saskatchewan's strategic importance within critical mineral supply chain architecture has grown substantially in recent years, precisely because alternatives outside Chinese ownership are so scarce."

Gillon Capital and the Sanctions Arbitrage Calculation

The emergence of Gillon Capital LLC as a prospective acquirer introduces a dimension that transcends conventional corporate finance. Gillon is a Dallas-based family office associated with Ray Washburne, a real estate executive appointed by Donald Trump in 2017 to lead the Overseas Private Investment Corporation (now rebranded as the U.S. International Development Finance Corporation, or DFC).

The non-binding preliminary agreement, signed in May 2026, would grant Gillon a controlling interest in Sherritt. The mechanism through which this creates value is not operational synergies or balance sheet restructuring — it is political connectivity. The core thesis is that a U.S.-linked controlling shareholder could engage the State Department in ways that a Canadian company operationally isolated from Washington cannot.

This model can be understood as sanctions arbitrage through ownership structure, a novel mechanism by which the nationality of a controlling shareholder becomes the primary variable in determining whether an asset is operable. It raises significant questions about precedent:

- If ownership by a politically-connected U.S. entity can unlock State Department licences for sanctioned operations, what does that mean for other companies with assets in Cuba or other sanctioned jurisdictions?

- Does this create a template for politically-connected capital to extract value from distressed companies rendered worthless by U.S. sanctions?

- How does this interact with Canada's 2024 critical minerals protection framework, which was specifically designed to prevent foreign investors from acquiring control over strategic mineral assets?

The Canadian regulatory dimension creates a genuine collision course. The Investment Canada Act review process for critical minerals acquisitions introduced in 2024 empowers the Canadian government to block or impose conditions on foreign takeovers of companies controlling critical mineral assets. A U.S. family office linked to Trump-era political networks seeking to acquire a Canadian company's Cuban nickel operations, during a period of heightened Canada-U.S. trade tension, presents an almost uniquely complex regulatory scenario.

"The irony is acute: the very political connections that might enable a State Department licence for Moa could simultaneously trigger a Canadian national security review that blocks the acquisition from proceeding."

The next major ASX story will hit our subscribers first

Three Scenarios for Cuban Nickel's Future in Western Supply Chains

The range of outcomes from the current situation is wide, and the probability weighting of each scenario carries significant implications for battery metal supply chains, energy transition timelines, and China's growing influence over critical mineral processing.

| Scenario | Key Conditions Required | Supply Chain Impact |

|---|---|---|

| Gillon acquires Sherritt, obtains State Dept. licence | U.S. political will, Canadian regulatory clearance, Cuban cooperation | Moa resumes operations, Fort Saskatchewan stabilised, Western supply chain preserved |

| Sherritt dissolves Cuba JV, refinery idles | Sanctions enforcement without relief, deal failure | North American nickel refining gap widens, Western battery supply chain weakened |

| Cuba pivots to Chinese partnership for Moa | Western exit accelerates Chinese capital entry | Cuban nickel exits Western supply chains entirely, deepening Chinese processing dominance |

The third scenario deserves particular attention. China's state-linked mining and processing entities have demonstrated consistent willingness to enter jurisdictions that Western capital finds politically untenable. Indeed, China's cobalt stockpiling behaviour already signals Beijing's strategic intent to secure battery metal supply wherever possible. If Western operators exit Moa entirely, Cuban nickel — one of the few significant non-Chinese laterite production sources feeding into Western refining infrastructure — would be redirected into Chinese-controlled processing networks.

Battery Chemistry, Demand Growth, and Why This Matters Beyond One Company

The Sherritt Cuba sanctions situation is often framed as a corporate governance or geopolitical story. Its deeper significance is as a case study in critical mineral supply chain fragility. Concerns around critical minerals energy security have never been more acute, and this situation illustrates precisely why policymakers and investors must pay close attention.

Global cobalt production remains highly concentrated, and losing a Western-aligned laterite source only tightens that picture further. China controls over 70% of global nickel refining capacity, a figure that has grown substantially as Chinese investment in Indonesian nickel processing, through rotary kiln-electric furnace (RKEF) technology, has expanded laterite refining capacity at scale. Against this backdrop, Fort Saskatchewan's role as a non-Chinese Class 1 nickel refinery becomes structurally important in ways that go far beyond Sherritt's market capitalisation of approximately CAD $80 million.

Complicating the supply picture further is the growth of nickel demand from data centre infrastructure, where stainless steel construction and cooling system components consume substantial quantities of refined nickel. This demand stream exists alongside, not instead of, EV battery demand, meaning that supply disruptions become more consequential as the demand base diversifies. Furthermore, efforts around critical minerals recycling are progressing but cannot yet compensate for the loss of primary production nodes like Moa.

What Investors and Supply Chain Strategists Should Monitor

For market participants tracking the intersection of Sherritt Cuba sanctions nickel cobalt dynamics, several indicators will be pivotal in determining how this situation resolves:

- State Department licence activity: Whether a specific licence or carve-out is issued for Moa operations under a new ownership structure will be the single most important near-term signal

- Investment Canada Act review timeline: The pace and outcome of any national security review of the Gillon Capital acquisition will determine whether the U.S. political angle can actually be executed

- Fort Saskatchewan inventory status: Once Cuban feed material inventory is exhausted, the operational clock shifts to facility preservation and restart costs, which escalate significantly the longer the plant remains idle

- Chinese engagement signals: Any reported discussions between Cuban state entities and Chinese mining or processing companies would confirm the third scenario trajectory

- Nickel sulphate spot pricing: Sustained tightness in Western battery-grade nickel supply would appear first in sulphate price premiums over LME nickel, a technically specific market signal worth tracking

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. The scenarios and analyses presented involve significant uncertainty and are subject to rapid change based on geopolitical, regulatory, and operational developments. Readers should conduct independent due diligence before making any investment decisions.

FAQ: Sherritt, Cuba Sanctions, Nickel, and Cobalt

What specifically did the 2026 U.S. sanctions target in Cuba's nickel sector?

The sanctions expansion designated GAESA, Cuba's military-linked economic conglomerate, and critically, Moa Nickel S.A. itself — the joint venture entity responsible for nickel and cobalt production at Moa. This created blocking requirements for U.S. persons and secondary sanctions risk for international financial institutions maintaining business relationships with these entities.

Why did Sherritt halt Moa operations before the sanctions announcement?

The fuel supply disruption originated from U.S. sanctions on Venezuelan oil exports, which cascaded into Cuba's energy infrastructure. Moa's pressure acid leach processing requires consistent high-energy inputs, and when scheduled fuel deliveries could not be fulfilled, operations became non-viable. The suspension was announced in February 2026.

What is the strategic significance of Fort Saskatchewan?

The Alberta refinery is one of very few Class 1 nickel processing facilities in North America outside Chinese corporate control. It converts Cuban laterite concentrate into battery-grade nickel sulphate and cobalt sulphate. Its potential idling would remove a genuinely scarce Western processing node from the supply chain at a critical moment.

What is the Gillon Capital deal and how would it work?

Gillon Capital LLC, a Dallas-based family office with political connections to Trump-era policy networks, signed a non-binding preliminary agreement for a controlling interest in Sherritt. The commercial logic is that U.S.-connected ownership could facilitate State Department engagement to obtain a sanctions licence enabling Moa to resume operations.

Could Canada block the Gillon acquisition?

Yes. Canada's 2024 critical minerals protection policy under the Investment Canada Act empowers the government to block or condition foreign acquisitions of companies controlling critical mineral assets. Any Gillon acquisition would likely trigger a national security review, creating a significant regulatory obstacle regardless of U.S. political positioning.

What happens to Cuban nickel if Western operators exit permanently?

Cuba would most likely seek Chinese state-linked capital and technical partnerships to maintain Moa operations. This would effectively redirect Cuban nickel and cobalt output into Chinese-controlled processing networks, consequently further concentrating critical mineral supply chains outside the Western sphere.

Want to Stay Ahead of the Next Major Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through the complexity of over 30 commodities to surface actionable opportunities the moment they are announced. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the broader market.