July 31, 2026

Why Silver's Structural Crisis Is Unlike Any Commodity Shortage Before It

Most commodity shortfalls are cyclical. Prices rise, capital flows in, supply responds, and the market rebalances within a few years. Silver is breaking that model entirely. What makes the current situation so unusual is not simply that supply is lagging demand, but that the mechanisms which normally correct such imbalances have become structurally impaired. New mines take longer to develop than most market participants assume, the majority of silver production cannot be directed by silver price signals alone, and the industrial applications consuming silver at record rates are permanently embedded in the global energy transition economy.

Understanding this requires moving beyond the standard commodity framework and into a deeper examination of how the silver supply deficit and price suppression dynamic has evolved across six consecutive years of structural imbalance. Furthermore, silver's dual role as both a precious metal and an industrial input makes it uniquely exposed to compounding demand pressures that few commodities face simultaneously.

When big ASX news breaks, our subscribers know first

Six Years of Deficit and Why the Gap Is Not Closing

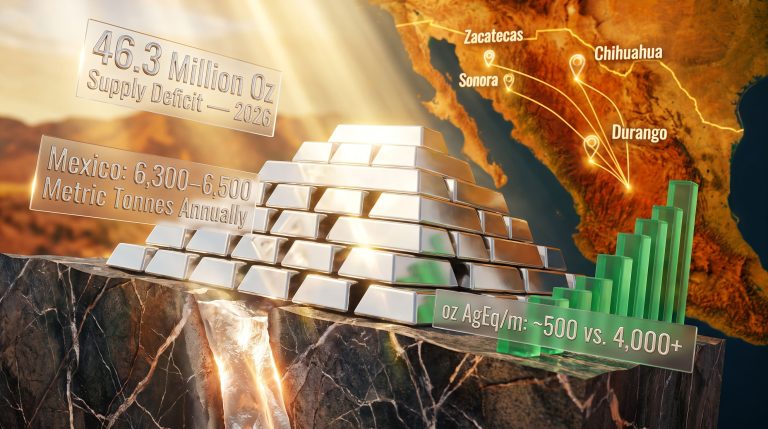

The silver market has recorded a supply deficit every year since 2021, with the cumulative shortfall across that period approaching an estimated 800 million ounces. The 2024 annual deficit alone was recorded at approximately 182 million ounces, representing one of the largest single-year shortfalls in modern market history. For 2026, the projected deficit stands at around 46.3 million ounces, roughly 15% higher than 2025 estimates, signalling that the imbalance is not narrowing but widening on a structural trajectory.

Global mine production in 2024 grew by just 0.9% year-on-year to approximately 819.7 million ounces. That marginal increase is categorically insufficient to close a demand gap measured in the hundreds of millions of ounces. What makes this more significant is the reason why production cannot simply accelerate: more than 70% of all silver produced globally is extracted as a byproduct of base metal mining operations, primarily copper, lead, and zinc. This means that silver output is governed not by the silver price, but by the production cycles of other industrial metals.

When a commodity's supply is structurally decoupled from its own price signals, conventional market correction mechanisms fail. Silver's byproduct nature is arguably its most underappreciated supply constraint.

Pure-play primary silver mines are rare across the global mining landscape, and bringing a new one into production from initial discovery requires a development timeline that regularly exceeds ten years. This encompasses exploration drilling, resource definition, prefeasibility and feasibility studies, environmental permitting, financing, construction, and commissioning. The financial and regulatory runway required means that even a prolonged and significant price rally cannot produce new mine supply within the timeframe investors typically expect.

Exploration budgets declined in 2024 despite silver prices appreciating dramatically in the preceding period, which compounds the long-term supply problem further. Consequently, ongoing silver supply deficits are likely to deepen before any meaningful supply response materialises from the development pipeline.

Geographic concentration adds another layer of vulnerability. Mexico contributes approximately 200 million ounces annually to global silver output, making it the world's largest silver-producing nation. Any trade disruption, policy shift, or geopolitical development affecting Mexican mining operations creates immediate and difficult-to-replace supply pressure in Western markets.

Industrial Demand That Cannot Be Reversed

Total global silver demand reached approximately 1.16 billion ounces in 2024. While the aggregate figure showed a modest 3% year-on-year decline, the composition of that demand tells a far more significant story. Industrial consumption reached a record high, driven by photovoltaic solar panel manufacturing, electric vehicle production, artificial intelligence infrastructure buildout, and advanced electronics.

| Demand Category | 2024 Volume (Moz) | Year-on-Year Change |

|---|---|---|

| Total Global Demand | ~1,160 | -3% overall |

| Industrial (Electronics, PV, EV, AI) | Record high | Positive |

| Jewellery | ~208.7 | +3% |

| Silverware | ~54.2 | -2% |

| ETF Investment | Rising | Positive |

Silver's role in photovoltaic manufacturing is particularly significant because each solar panel requires silver paste for electrical conductivity in the cell. As panel installations accelerate globally, total silver consumption in this segment continues to grow despite efficiency improvements in per-unit silver usage. The volume growth from expanding solar deployment consistently outpaces the per-unit reductions from technological thrifting.

The electric vehicle sector represents another permanent demand pool. Each EV contains meaningful quantities of silver in its electrical systems, battery management systems, and conductive components. As EV penetration rates rise across major automotive markets in China, Europe, and North America, the aggregate demand from this sector alone represents a structurally growing claim on available silver supply.

Is AI Infrastructure an Underestimated Demand Driver?

One dimension that receives insufficient analytical attention is the AI infrastructure buildout. Data centres, advanced semiconductors, and high-frequency electronic systems require silver in quantities that are not yet well-modelled in consensus demand forecasts. This emerging category could represent a material upside surprise to demand projections through the end of the decade.

A speaker at the Vancouver Resource Investment Conference, drawing on an interview with industry analyst Eric Young, highlighted that China has achieved near self-sufficiency in electricity generation through aggressive investment in EV adoption, wind power, and alternative energy infrastructure. All of these systems require significant quantities of silver. The same observation applies to energy diversification programmes accelerating across Southeast Asia, South Asia, and parts of the Middle East in response to geopolitical energy market instability. The framing of silver as the new oil reflects the commodity's increasingly indispensable role in the global energy economy.

Critically, silver consumed in industrial applications is largely non-recoverable. Once embedded in a solar panel, circuit board, or vehicle electrical system, it exits the available supply chain permanently. This differentiates silver's demand destruction profile from that of gold, where recycling and above-ground stock circulation play a more significant role in supply balancing.

The Paper Market and Physical Market Divide

The silver supply deficit and price suppression debate is most acute when examining the relationship between paper derivative markets and physical delivery markets. These two pricing mechanisms are increasingly diverging under structural supply stress, and the implications for price discovery are significant. In addition, the silver market backwardation signal that has emerged in futures curves points to acute near-term physical tightness that paper pricing has not yet fully reflected.

COMEX silver futures, the dominant Western price-setting mechanism, are estimated to operate at leverage ratios of approximately 400 to 1, meaning the volume of paper silver contracts outstanding is vastly larger than the physical silver available for actual delivery. This is not unusual for futures markets, which are designed for price discovery and hedging rather than physical settlement. However, when delivery demands stress registered inventories, the structural fragility of this arrangement becomes visible.

During March 2026, COMEX delivery demands placed significant pressure on registered silver inventories, with reports suggesting that over 60% of registered stock was called for physical delivery during that period. This represents an extreme stress test of the paper-to-physical relationship and is consistent with a market where buyers of last resort are prioritising the physical metal over paper exposure.

Falling open interest in a rising or elevated price environment typically signals one of two conditions: commercial short-sellers are reducing exposure due to delivery risk, or the paper market is progressively losing its function as the primary price discovery mechanism.

Open interest in silver futures has dropped below 100,000 contracts, a level that is structurally notable. Conventional market dynamics would suggest that elevated prices attract speculative interest and push open interest higher. The opposite pattern — rising or sustained prices alongside declining open interest — suggests that major participants are unwinding short positions rather than adding new directional bets.

How Institutional Short Positioning Suppresses Silver

Commentary from market observers, including analysis shared at the Vancouver Resource Investment Conference, indicates that major financial institutions are actively reducing short exposure on silver futures. They are aware of the extreme leverage embedded in the system and the delivery risk that comes with it. This behaviour is structurally bullish for physical silver pricing because it represents a reduction in artificial downward price pressure from derivative short positions. According to research on how silver price suppression works, this mechanism has operated for years through concentrated short positions in futures markets.

The East-West price divergence reinforces this picture. Shanghai silver markets have been trading at persistent premiums to Western spot prices, reflecting genuine physical demand that exceeds what paper-priced Western supply can satisfy. Physical silver is flowing from London and New York vaults toward Asian buyers in China and India at an accelerating pace. Silver lease rates, the cost of borrowing physical silver for short-term delivery, reached their highest levels since 2002 during recent periods of acute physical tightness — a signal that is difficult to reconcile with a commodity experiencing only modest price pressure.

Price Forecasts, Institutional Bias, and the Magnitude Problem

Silver reached a peak of $121.62 per ounce in January 2026 before undergoing a correction driven by US dollar strength and COMEX margin requirement increases. The recovery has brought prices back into a range of mid-to-upper $80s per ounce, with structural deficit dynamics reasserting themselves as the primary price driver. However, the broader context of trade war impact on gold and silver prices has added further complexity to price forecasting during this period.

| Period | Approximate Price (USD/oz) | Key Driver |

|---|---|---|

| 2024 Pre-Surge | $28–$32 | Accumulation phase |

| Early 2025 | $58+ | Deficit recognition breakout |

| January 2026 | $121.62 (peak) | Physical delivery stress |

| Post-Correction 2026 | $64–$80s | USD strength, margin hikes |

| Recovery 2026 | Mid-to-upper $80s | Structural deficit reassertion |

Bank of America has published a silver price target range of $135 to $309 per ounce for 2026, citing supply constraints and gold-silver ratio analysis. The gold-silver ratio remains historically elevated, suggesting that silver is undervalued relative to gold when measured against long-term ratio norms.

However, institutional price forecasts carry a well-documented bias that investors should understand. A speaker at the Vancouver Resource Investment Conference, drawing on more than two decades of tracking bullion bank forecasts dating back to 2002, observed that investment banks have a consistent pattern of overestimating equity index targets while simultaneously underestimating the upside potential of gold and silver. When a major institution like Bank of America publishes a target approaching $300 per ounce for silver, the directional call is likely correct — but historical precedent suggests the magnitude of the actual move may substantially exceed even that elevated target.

This is not simply analytical conservatism. Bullion banks hold significant short-side exposure in precious metals derivatives as part of their market-making and hedging operations. Conservative price forecasts serve multiple institutional functions simultaneously, managing client expectations, limiting liability, and maintaining orderly positioning in markets where the institution itself holds material exposure.

The practical implication for investors: institutional targets provide directional guidance but should not be treated as ceilings.

Monetary Expansion as a Structural Amplifier

The silver supply deficit and price suppression dynamic does not exist in isolation from the broader monetary environment. US M2 money supply broke above $22 trillion in the period following COVID-19 monetary expansion and is now approaching $23 trillion. Global M2, aggregating major economies, is estimated to be growing at a rate of approximately 12 to 15% on an annualised basis, according to analysis shared at the Vancouver Resource Investment Conference.

The Federal Reserve's balance sheet has expanded by over $150 billion since December of the reference period, a de facto resumption of quantitative easing irrespective of the official terminology used. Furthermore, the Silver Institute's latest outlook confirms that global silver investment is expected to remain strong in 2026 against the backdrop of a sixth consecutive annual market deficit, reinforcing the case for sustained price support.

The conventional focus on CPI as an inflation metric significantly understates the real rate of monetary debasement. M2 growth rate is the more accurate measure of purchasing power erosion, and at 12–15% annually, it represents a structurally hostile environment for fiat currency holders.

The distinction matters for silver investors because it changes the analytical framework. When real monetary expansion runs at double-digit annual rates, hard assets with structural supply deficits serve a dual function simultaneously: they are both industrial commodities with genuine scarcity value and monetary hedges against currency debasement. This compression of roles accelerates price appreciation potential beyond what either function would generate independently.

The bond market reinforces this picture. A secular bear market in bonds, with yields rising from their 2020 cycle peak, creates sustained pressure on government finances and limits the Federal Reserve's genuine room for monetary tightening. Efforts to suppress the 10-year Treasury yield below 4.5% and the 30-year below 5% reflect a structural tension between fiscal sustainability and market price discovery that cannot be maintained indefinitely without explicit intervention.

If yield curve control or explicit quantitative easing is announced to defend bond markets during an economic slowdown, the monetary expansion required would be powerfully bullish for silver given its dual industrial-monetary character. Suppressing the 10-year yield back toward 3% is theoretically possible, but achieving it in a structural bond bear market requires massive monetary creation. A currency being devalued at 12% to 15% annually renders the nominal yield figure largely irrelevant as a measure of real returns.

Historically, central bank independence has eroded during financial crises across multiple countries and policy regimes. Fiscal and monetary policy converge under crisis conditions because the alternative — allowing a debt deflation of historic severity — is politically and economically untenable. This historical pattern creates a near-inevitable trajectory toward sustained monetary expansion, which is structurally supportive of silver as both an industrial input and a store of value.

The next major ASX story will hit our subscribers first

The Supply Pipeline Cannot Be Fixed Quickly

Looking toward the end of the decade, the supply picture for silver offers little prospect of relief. Demand projections from photovoltaic installations, EV production, AI infrastructure, and electrification programmes continue to rise across every major region. Deutsche Bank has forecast record ETF silver holdings as institutional investors respond to rate reduction cycles and physical tightness signals. Consensus analysis projects deficits persisting through at least 2030 in the absence of a step-change in primary mine development investment.

That step-change is not currently visible in exploration budget data. The refining capacity and geographic alignment between production and consumption centres also remains mismatched, adding further friction to physical supply chains. Silver produced in Mexico or Peru must navigate logistics chains to reach refining facilities and then physical delivery destinations in Asia or Europe, and capacity constraints along that chain amplify tightness during periods of elevated demand.

The byproduct dependency problem is ultimately the most intractable constraint. Even a significant increase in global copper mining, driven by electrification demand, produces only marginal incremental silver output relative to the deficit scale. Without a sustained and dramatic expansion of primary silver mine development, the structural imbalance between supply and demand is likely to persist and deepen.

Key Takeaways for Investors Navigating the Silver Market

Synthesising the structural, monetary, and market dynamics examined above produces a framework with several actionable implications:

- Six consecutive years of supply deficit have created a cumulative shortfall approaching 800 million ounces with no credible near-term resolution pathway

- Industrial demand from solar, EVs, AI, and electrification is permanent, growing, and largely irreversible once silver enters the industrial consumption cycle

- COMEX paper market structural stress, including declining open interest at elevated prices, record delivery demands, and institutional short unwinding, points to a potential inflection in price discovery mechanisms

- East-West price divergence and physical silver flows toward Asia reflect genuine physical scarcity beyond what paper markets are currently pricing

- Monetary expansion at 12–15% annually creates a powerful backdrop for hard assets with supply constraints, amplifying silver's appreciation potential beyond what industrial demand alone would generate

- Institutional price forecasts, while directionally useful, have a documented history of underestimating the magnitude of precious metal bull market moves

- New mine supply cannot be accelerated on any timeline relevant to the current deficit cycle; the imbalance is likely structural through at least 2030

This article is for informational and educational purposes only and does not constitute financial advice. Forecasts, price targets, and projections referenced reflect third-party analysis and historical patterns and are not guarantees of future performance. Precious metals markets carry significant volatility and investment risk. Readers should conduct their own due diligence and consult qualified financial advisors before making investment decisions.

Want To Stay Ahead of the Next Major Silver Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data across 30+ commodities into actionable insights — so investors can act before the broader market catches on. Start your 14-day free trial at Discovery Alert today, or explore how historic mineral discoveries have generated extraordinary returns for early-positioned investors.