June 23, 2026

When Deposit Geometry Becomes a Business Model

The critical minerals industry has spent the better part of a decade debating which commodities matter most for the energy transition and Western supply chain security. Less attention has been paid to a more fundamental question: among the projects capable of supplying those commodities, which ones are structurally built to survive across the full range of price cycles, financing conditions, and geopolitical disruptions?

The answer rarely lies in commodity selection alone. It lies in deposit architecture. A project whose cost structure is embedded in its geology, rather than engineered around it, carries a durable advantage that no competitor can replicate through capital efficiency or management execution alone. That distinction sits at the centre of what makes the Sovereign Metals (ASX: SVM | AIM: SVML | OTCQX: SVMLF) Kasiya project competitive advantage genuinely unusual among critical minerals developments at the definitive feasibility study stage.

When big ASX news breaks, our subscribers know first

The Three-Layer Cost Problem Most Projects Cannot Escape

Why Most Critical Minerals Operations Carry Structural Inefficiency

Every critical minerals project inherits a cost structure from three compounding sources: the complexity of extracting ore from the ground, the intensity of processing that ore into a saleable product, and the logistical burden of delivering that product to market. Most projects carry at least two of these cost layers simultaneously. Hard-rock graphite operations carry all three, requiring drilling and blasting to access ore, energy-intensive flotation and thermal purification to reach battery-grade carbon purity, and often remote locations that inflate export costs.

The rare project eliminates all three layers at once. When that occurs, the cost advantage is not marginal; it is architectural. The operating cost floor drops to a level that cannot be matched by competitors whose deposits impose cost layers as a geological given. Furthermore, critical minerals demand continues to grow in ways that reward structurally low-cost producers above all others.

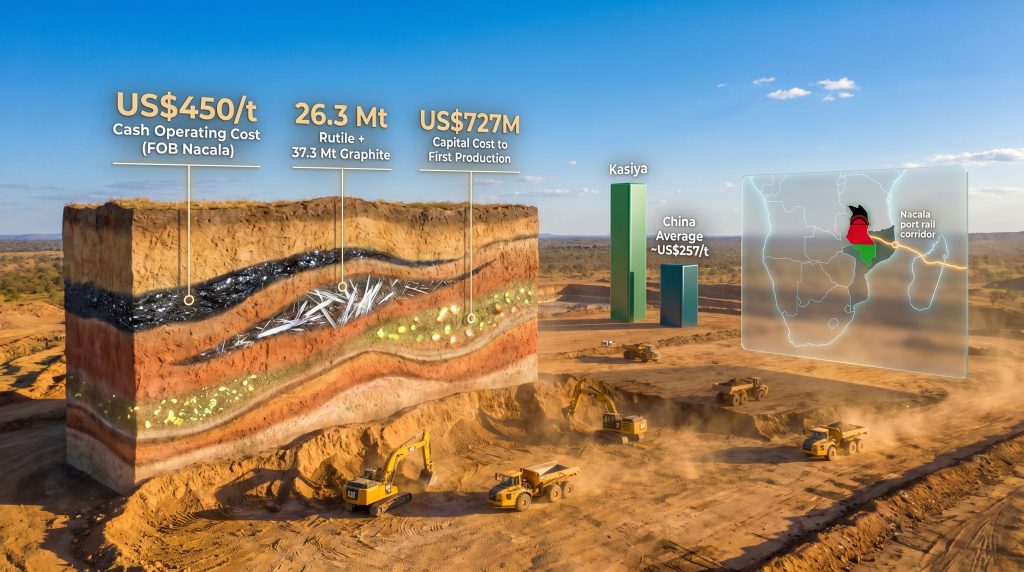

Kasiya eliminates all three. The deposit occupies a laterally extensive, flat-lying laterite plain west of Lilongwe, Malawi, where rutile, graphite, and monazite are hosted within a deeply weathered saprolite blanket sitting above the saprock boundary. Ore is physically accessible without mechanical intervention. There is no hard rock, no requirement to drill or blast, and no pre-strip phase. Standard mobile excavators and haul trucks replace the capital-intensive comminution infrastructure that defines conventional hard-rock critical minerals operations.

The absence of a comminution circuit eliminates one of the largest single capital and energy cost centres in conventional mineral processing. For projects that require crushing and grinding, this circuit alone can account for 30% to 40% of total processing plant capital expenditure and represents a disproportionate share of ongoing operating energy demand.

What Free-Dig Geology Actually Means in Practice

The term free-dig describes ore bodies where excavation can proceed using earthmoving equipment without any prior rock fragmentation. In a saprolite-hosted deposit like Kasiya, the weathering process that created the mineral concentration also disaggregated the host material over geological time, leaving a loose, clay-rich matrix that mobile equipment can directly load and transport.

The practical consequences are significant, and the processing simplicity advantage this geology provides is difficult to overstate:

- No blasting means no explosives supply chain, no vibration management programme, and no regulatory complexity associated with energetic materials

- No crushing or grinding circuit means capital expenditure for the processing plant is concentrated in wet gravity separation and electrostatic separation equipment, both of which are lower-cost and lower-maintenance than comminution infrastructure

- No conventional tailings storage facility is required, removing one of the most complex and environmentally sensitive engineering elements in conventional mineral processing

- Power demand of approximately 30 megawatts at initial throughput and 60 megawatts at full dual-plant capacity falls within the supply capacity of the existing Malawi national grid, removing the captive power infrastructure risk that inflates financing costs at comparable off-grid operations

The April 2026 DFS: Translating Geology Into Financials

The April 2026 definitive feasibility study converts Kasiya's geological simplicity into a specific set of economic outcomes. The headline capital figure of US$727 million to first production is notable not just in absolute terms but in relative terms. Comparable-scale critical minerals projects at the DFS stage routinely exceed US$1 billion in pre-production capital, with many hard-rock graphite and mineral sands developments carrying capital intensities 40% to 60% higher per unit of annual production capacity.

The operating cost of US$450 per tonne of product (FOB Nacala) positions Kasiya as the lowest-cost producer of both rutile and graphite globally, including Chinese operations. The graphite-specific cost of approximately US$241 per tonne FOB sits below China's average of roughly US$257 per tonne, a comparison that carries significant strategic weight given China's dominance of approximately 75% of global graphite production.

| Metric | Kasiya DFS (April 2026) | Peer / Benchmark Context |

|---|---|---|

| Capital cost to first production | US$727 million | Comparable projects typically exceed US$1 billion |

| Cash operating cost (FOB Nacala) | US$450/tonne | Lowest-cost globally, including China |

| Graphite operating cost | ~US$241/tonne FOB | Below China average of ~US$257/tonne |

| Rutile DFS base-case price | ~US$1,670/tonne | Toho Titanium confirmed on-specification approval |

| Graphite jumbo flake DFS price | ~US$1,288/tonne | US market: ~US$2,000-US$2,200/tonne for comparable grades |

| Initial throughput | 12 Mtpa (south plant) | Scaling to 24 Mtpa with north plant by end of Year 5 |

| Mine life | 25+ years | Supported by 26.3 Mt rutile + 37.3 Mt graphite resource |

| Power demand (initial / full capacity) | 30 MW / 60 MW | Serviceable by existing Malawi national grid |

A detail that investors often overlook is that the DFS base-case commodity prices are set conservatively relative to prevailing market conditions. The rutile price of US$1,670 per tonne reflects a production-period forecast rather than current spot levels, and the graphite jumbo flake price of US$1,288 per tonne sits well below the approximately US$2,000 to US$2,200 per tonne currently quoted in the US market for equivalent material. Consequently, the published economics are structurally conservative, and any normalisation of commodity pricing directly expands the project's financial profile without any operational change.

The Dual-Commodity Model as a Natural Hedge

Rutile and graphite serve structurally different end markets. Rutile feeds the titanium feedstock supply chain, supplying manufacturers of titanium metal, titanium dioxide pigment, and specialty welding consumables. Graphite serves the battery anode material market, the electric vehicle supply chain, and refractory applications. Price cycles in these markets are driven by different demand variables and do not historically correlate.

Kasiya would be the only large-scale primary natural rutile producer globally, entering a market where Japan accounts for more than 15% of global titanium metal capacity and more than 60% of non-sanctioned aerospace and defence-grade titanium supply. Toho Titanium, one of Japan's leading titanium producers, has confirmed that Kasiya's rutile meets specification across its entire product range, providing early-stage commercial validation for the project's primary revenue stream.

The graphite by-product carries its own premium characteristics. Approximately 68% of Kasiya's graphite output falls in the medium, large, and jumbo flake categories, which command significant price premiums over the small-flake material that dominates output from most competing operations. Carbon purity reaches 96% to 98%, compared to the industry-typical 94% to 95%, a specification gap that is particularly relevant to battery-grade downstream processors.

The environmental profile compounds the commercial differentiation. Kasiya's rutile production carries an emissions intensity up to 97% lower than conventional titanium feedstock alternatives, while its graphite production generates up to 83% fewer greenhouse gas emissions than hard-rock processing peers. For European and Japanese industrial buyers operating under Scope 3 reporting obligations, this distinction is moving from a preferential characteristic to a procurement requirement.

The Hidden Revenue Layer: Monazite in the Tailings Stream

How the Non-Conductor Tailings Stream Works

The electrostatic separation circuit that processes Kasiya's mineral concentrate separates particles by their electrical conductivity. Rutile and graphite are conductors; monazite is not. In a conventional operation, this separation is an unwanted complication. At Kasiya, however, it creates a precisely characterised by-product stream that already exits the existing DFS flowsheet as a discrete concentrate, potentially requiring no additional mining campaign, no separate processing circuit, and no additional reagents.

Monazite was confirmed across four DFS mine plan pits: Babbler, Kingfisher, Sparrow, and Mousebird, including pits scheduled for Year 1 production. The implication is that the monazite stream is available from the first day of operations, not from a later expansion phase. You can explore the full details of the Kasiya project overview on the Sovereign Metals website.

The Heavy Rare Earth Composition Gap

The strategic value of Kasiya's monazite stream does not lie in its volume. It lies in the composition of its total rare earth oxide basket. The 4-pit weighted average shows a heavy rare earth profile that is fundamentally different from the basket produced by the world's dominant rare earth operations:

| Rare Earth Component | Kasiya 4-Pit Weighted Average | World's 5 Largest REE Producers (Average) |

|---|---|---|

| Dysprosium + Terbium (% of TREO) | 2.5% | ~0.4% |

| Yttrium (% of TREO) | 11.8% | ~1.7% |

| Heavy REE basket vs. peers | ~7x higher | Baseline |

| Dysprosium/Terbium at MP Materials | Not measurable | N/A |

Dysprosium, terbium, and yttrium are not interchangeable with light rare earths. They are the specific elements required for high-performance permanent magnets used in electric vehicle drivetrains, wind turbine generators, and defence electronics systems including guidance systems and radar. The supply of these elements outside China is structurally limited. In addition, concerns about rare earth supply chains continue to intensify, reinforcing Kasiya's strategic relevance to Western industrial buyers.

The pricing differential between standard monazite and a heavy rare earth-enriched equivalent is substantial. Project Blue Group Limited's independent 2026 forecast places the base-case price for Kasiya's 60% TREO monazite concentrate at US$16,000 per tonne, compared to the April 2026 Shanghai Metals Market benchmark of US$6,142 per tonne for standard monazite concentrate at 54% to 55% TREO grade.

That premium, reflecting the heavy rare earth basket composition, is currently assigned zero economic contribution in the DFS base case, leaving an estimated potential contribution of approximately US$60 million per year in additional EBITDA as an unrecognised value layer pending a dedicated economic uplift study.

The monazite stream's exclusion from the DFS base case is arguably the most consequential piece of conservative accounting in the project's published economics. It means that the NPV figures investors currently use to value Kasiya structurally understate the project's revenue potential by at least one full commodity stream before any exploration upside is considered.

How Flowsheet Simplicity Directly Reduces the Cost of Capital

The IFC Engagement and What It Signals

The International Finance Corporation of the World Bank Group is engaged as a potential co-lead arranger for Kasiya's project financing, having confirmed that the DFS meets IFC Performance Standards. This confirmation matters beyond its symbolic significance. IFC Performance Standards represent the baseline environmental, social, and governance framework required by most commercial lenders, development finance institutions, and export credit agencies before committing to project debt due diligence.

The deeper connection runs from deposit characteristics to debt pricing. Lenders at the DFS-to-construction transition apply a technical risk premium to projects that carry unresolved engineering complexity. Every eliminated risk category — whether blasting management, hard-rock processing, conventional tailings storage, or captive power infrastructure — reduces the premium that lenders price into project debt. Kasiya's flowsheet eliminates all four simultaneously, which is why the financing concept targets approximately 60% debt against 40% equity, prepayments, and offtake finance.

The US Listing Consideration

A US listing is under active discussion as Sovereign Metals broadens its investor base ahead of the construction financing phase. The strategic logic reflects a specific institutional market dynamic: US-listed critical minerals companies supplying Western defence and industrial supply chains access a significantly larger pool of institutional capital, including funds with mandates to hold domestically accessible critical materials exposure.

Furthermore, Australia's critical minerals strategy increasingly aligns with allied nation procurement priorities, strengthening the commercial case for projects like Kasiya that can supply three confirmed critical materials from a single, simple flowsheet.

Structural Comparison: Where Kasiya Sits Among Global Peers

| Dimension | Kasiya (Malawi) | Typical Hard-Rock Graphite Project | Typical Mineral Sands Project |

|---|---|---|---|

| Mining method | Free-dig, no blast | Drill and blast | Dredge or dry mining |

| Processing complexity | Wet gravity + electrostatic | Flotation + thermal purification | Wet gravity + electrostatic |

| Comminution circuit | None | Required | Minimal |

| Tailings storage facility | None required | Conventional TSF | Conventional TSF |

| By-product revenue streams | Graphite + monazite (HREEs) | Typically single commodity | Typically zircon + ilmenite |

| Grid power access | Existing national grid | Often off-grid | Variable |

| GHG emissions intensity | Up to 97% lower (rutile); 83% lower (graphite) | High (thermal purification required) | Moderate |

The logistics dimension compounds the operating cost advantage. Proximity to Nacala port via existing rail infrastructure reduces export costs versus landlocked competing projects, and the FOB Nacala delivered cost benchmark is directly relevant to Asian and European buyers whose procurement decisions are made on a landed-cost basis.

The next major ASX story will hit our subscribers first

Key Catalysts That Could Re-Rate the Project's Market Value

The published DFS economics are conservative in multiple respects simultaneously: base-case commodity prices set below current market levels, a fourth revenue stream carrying zero value, and a modular expansion pathway that doubles production capacity without greenfield engineering complexity. The catalysts that close the gap between published and potential economics are sequenced and identifiable:

- Monazite economic uplift study — Formal quantification of the heavy rare earth tailings stream contribution within the existing flowsheet, establishing the incremental capital and operating cost additions required to capture the US$16,000 per tonne concentrate value

- Project financing advancement — Progress on the IFC co-lead arranger mandate and engagement with commercial lenders and development finance institutions toward a financing commitment

- Offtake agreement formalisation — Supply agreements with titanium producers, battery material processors, and rare earth separation facilities that validate the project's commercial position with binding contractual terms

- US listing — Broadening institutional access ahead of the construction financing phase

- Commodity price recovery — Any movement of rutile or graphite prices toward current spot levels directly expands the project's published economics without operational change

- North plant expansion — Addition of the second identical 12 Mtpa plant targeting 24 Mtpa total throughput by end of Year 5, via a modular approach that avoids the execution complexity of new greenfield construction

Frequently Asked Questions: Kasiya Project Competitive Advantage

Why Does Free-Dig Geology Create a Lasting Cost Advantage Rather Than a Temporary One?

The cost advantage is physically embedded in the ore body characteristics, not in market timing or management decisions. Weathered saprolite does not harden as mining progresses. The geological setting that eliminates blasting, pre-strip, and comminution persists across the full mine life, locking in the operating cost structure for the entire duration of production.

How Does the Dual-Commodity Model Protect Against Single-Commodity Price Risk?

Rutile and graphite serve structurally different end markets with uncorrelated demand cycles. A downturn in titanium feedstock pricing does not necessarily coincide with weakness in battery-grade graphite demand. The monazite stream adds a third revenue source tied to rare earth magnet demand, driven by electric vehicle and defence electronics dynamics that are further decoupled from both rutile and graphite cycles. An independent analysis of the DFS results provides additional context on this multi-commodity structure.

What Is the Significance of 96% to 98% Carbon Purity in Kasiya's Graphite Output?

Most competing graphite concentrates reach 94% to 95% carbon, a purity level that requires thermal purification to upgrade to battery-grade specification. Thermal purification is an energy-intensive, high-temperature process that adds cost and emissions intensity. Kasiya's 96% to 98% purity reduces or eliminates this step for downstream processors, representing a direct cost saving and emissions reduction for buyers operating under Scope 3 reporting requirements.

Why Is the Monazite Stream's Absence From the DFS Base Case Strategically Important for Investors?

It means the published project economics are structurally conservative before any upward commodity price movement is considered. An estimated US$60 million per year in potential additional EBITDA from the monazite stream sits outside the current valuation framework entirely, implying that investors pricing Kasiya against its DFS NPV are not capturing the full economic potential of the asset.

What Would Inclusion of the Monazite Stream Require?

A dedicated economic uplift study is required to quantify the revenue contribution, define the incremental processing steps to upgrade the existing non-conductor tailings concentrate, and establish the associated capital and operating cost additions. Given that the stream already reports from the existing electrostatic separation circuit, incremental capital requirements are expected to be low relative to the value potential.

Simplicity as the Rarest Quality in Critical Minerals Development

The Sovereign Metals Kasiya project competitive advantage does not rest on a single metric. It rests on the compounding interaction of a free-dig ore body that eliminates the three primary layers of mining cost, a dual-commodity structure that provides natural revenue diversification across uncorrelated markets, an embedded heavy rare earth tailings stream that requires no additional mining capital to access, and a processing flowsheet simple enough to meet IFC financing standards and attract debt at commercially viable leverage ratios.

Each of these characteristics reinforces the others. The geological simplicity that keeps operating costs below Chinese levels also keeps the flowsheet simple enough to reduce lender risk premiums. The same electrostatic separation that produces clean rutile and graphite concentrates also isolates a monazite stream whose heavy rare earth composition represents the highest-value per-tonne output at the project, currently unrecognised in any published economic model.

For investors and industrial buyers assessing the critical minerals development landscape, the relevant question is not merely which projects supply the right commodities. It is which projects are architecturally positioned to supply those commodities profitably across the full range of conditions that the next 25 years will inevitably present. That is the question that geological simplicity answers most durably, and it is precisely why the Sovereign Metals Kasiya project competitive advantage merits careful consideration within any serious critical minerals portfolio framework.

This article is intended for informational purposes only and does not constitute financial advice. Forecasts, projections, and price estimates referenced herein involve assumptions and uncertainties that may not be realised. Readers should conduct their own due diligence before making any investment decisions. Further institutional-grade analysis on Kasiya and comparable critical minerals development projects is available at Crux Investor.

Want to Be First When the Next Major Mineral Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex mineral data into actionable insights for both short-term traders and long-term investors. Explore why historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.