June 3, 2026

Supply Chain Vulnerabilities in Global Energy Technology Markets

Modern energy infrastructure faces unprecedented challenges as the transition toward electrification accelerates across multiple sectors simultaneously. Traditional risk management frameworks, originally designed for relatively stable fossil fuel supply chains, prove inadequate when applied to the complex, multi-stage manufacturing networks required for batteries, solar panels, wind turbines, and electric vehicle components. The fundamental shift from commodity-based energy systems to technology-intensive infrastructure creates entirely new categories of systemic vulnerabilities that demand comprehensive strategic analysis.

The emergence of what industry analysts term the "Age of Electricity" represents more than technological evolution; it constitutes a complete restructuring of global economic dependencies and geopolitical relationships. Unlike conventional energy commodities that can be substituted relatively easily between suppliers, advanced energy technologies require specialised manufacturing capabilities, precise quality control, and sustained investment in research and development. This transformation creates supply chain resilience in energy technologies challenges that extend far beyond traditional concepts of critical minerals and energy security.

When big ASX news breaks, our subscribers know first

What Defines Supply Chain Resilience in Modern Energy Infrastructure?

Core Components of Resilient Energy Networks

Supply chain resilience in energy technologies encompasses multiple interconnected elements that function as integrated systems rather than isolated components. The framework requires comprehensive identification of critical chokepoints across multi-stage supply chains, systematic assessment of alternative sourcing capacity outside dominant supplier nations, and quantitative analysis of production redundancy at each manufacturing stage.

| Resilience Framework Elements | Key Requirements | Assessment Metrics |

|---|---|---|

| Risk Identification Protocols | Multi-stage vulnerability mapping | N-1 analysis for critical suppliers |

| Redundancy Systems | Alternative sourcing capacity | Production capacity outside dominant suppliers |

| Recovery Objectives | Time-to-restoration targets | Economic impact quantification |

| Stakeholder Coordination | Cross-sector collaboration mechanisms | Information sharing protocols |

The International Energy Agency's analysis reveals that the global market for key energy technologies may expand from approximately $1.2 trillion in 2026 to around $2 trillion by 2035, representing growth equivalent to the entire global oil market. Under stated policy scenarios, this market could reach nearly $3 trillion by 2035, fundamentally altering the scale and complexity of supply chain management requirements.

Digital Infrastructure as the Foundation Layer

Advanced monitoring systems form the technological backbone of resilient energy supply chains, enabling real-time visibility across geographically distributed manufacturing networks. Internet of Things (IoT) integration provides equipment tracking and performance optimisation capabilities that allow operators to identify potential disruptions before they cascade through downstream production stages.

Automated response systems incorporate machine learning algorithms that analyse historical disruption patterns and current operational data to generate predictive alerts. These systems enable proactive decision-making protocols that can redirect supply flows, adjust production schedules, or activate backup suppliers based on predetermined risk thresholds.

Key technological capabilities include:

-

Predictive analytics for demand forecasting and resource optimisation

-

Anomaly detection systems for early warning of potential disruptions

-

Integrated communication platforms for coordinated emergency response

-

Blockchain-based tracking for supply chain transparency and verification

Furthermore, data-driven mining insights enable operators to optimise extraction and processing operations while maintaining visibility across complex supply networks.

Material Flow Security and Critical Resource Management

Strategic stockpiling represents a fundamental component of resilience planning, though the approach must be adapted for energy technology components that may become obsolete due to rapid innovation cycles. Quality assurance systems ensure that stored materials maintain performance specifications over extended periods, while traceability protocols enable rapid identification of component origins during quality issues or recalls.

Supplier diversification strategies require careful balance between cost optimisation and risk mitigation, particularly given the significant economies of scale in energy technology manufacturing. Qualification processes for alternative suppliers must account for technical capability, financial stability, and geopolitical risk factors that could affect long-term reliability.

How Do Geographic Concentrations Create Systemic Vulnerabilities?

The N-1 Analysis Framework for Risk Assessment

The N-1 supply chain security analysis methodology evaluates what occurs when the single largest supplier of any technology component is removed from global markets. This analytical approach reveals critical vulnerabilities that traditional risk assessment methods often overlook, particularly in highly concentrated manufacturing sectors.

Critical Vulnerability Definition: When less than 25% of global demand can be satisfied without the largest single supplier, the entire supply chain faces existential risk from any disruption to that dominant source. This threshold indicates insufficient alternative capacity to maintain global operations during extended disruptions.

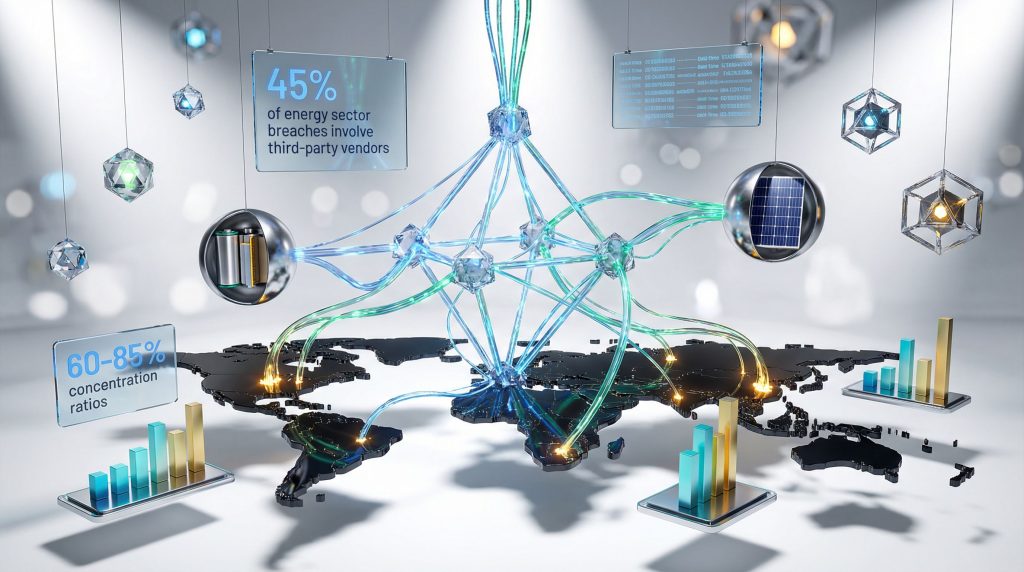

Research indicates that China holds 60-85% of global production capacity across multiple supply chain steps for key energy technologies. The geographical manufacturing landscape appears unlikely to change significantly before 2030, based on committed manufacturing and mining projects and current market trajectories.

Manufacturing Hub Dependencies and Single Points of Failure

Every major supply chain analysed contains at least one step where production outside the largest exporting country could theoretically meet demand outside that country at final manufacturing stages. However, intermediate manufacturing steps demonstrate severe concentration levels that create cascading vulnerability throughout the entire production network.

| Technology Category | Concentration Level | Primary Vulnerability Points |

|---|---|---|

| Battery Technology | 60-85% single-country dominance | Cathode materials, cell manufacturing |

| Solar PV Components | 65% cost gap in upstream stages | Polysilicon production, wafer manufacturing |

| Wind Turbine Manufacturing | 75% energy/labour cost advantage | Blade production, generator systems |

The analysis reveals that alternative production capacity exists outside dominant suppliers at final assembly stages, but critical intermediate components remain highly concentrated. This creates a paradox where finished product assembly could theoretically be diversified while remaining dependent on concentrated upstream suppliers.

Consequently, the development of an European CRM facility represents a strategic response to these vulnerabilities, though implementation timelines may limit near-term impact.

Economic Impact Modelling for Disruption Scenarios

Quantitative analysis of supply chain disruption impacts demonstrates the substantial economic consequences of concentration-related vulnerabilities. A one-month halt in Chinese battery supply chain exports would reduce electric vehicle factory output elsewhere by an estimated $17 billion, with more than 50% of losses occurring in the European Union.

Monthly Disruption Cost Analysis:

-

Electric vehicle production losses: $17 billion potential impact

-

Solar module manufacturing: $1 billion monthly exposure

-

European Union exposure: >50% of battery disruption costs

-

Southeast Asia and India: >40% of solar PV disruption impact

Similar disruption scenarios in solar photovoltaic supply chains would reduce monthly output from solar PV module factories outside China by approximately $1 billion, with Southeast Asia and India accounting for over 40% of affected output. These figures illustrate how geographic concentration translates directly into measurable economic vulnerability.

However, US-China trade war impacts demonstrate how geopolitical tensions can exacerbate these vulnerabilities, creating additional pressure for supply chain diversification.

Which Cybersecurity Threats Pose the Greatest Risk to Energy Supply Chains?

Third-Party Vendor Vulnerabilities in Energy Networks

Energy sector organisations face disproportionate cybersecurity risks compared to other industries, with research indicating that 45% of energy sector breaches involve third-party vendors compared to a 29% global average across all industries. The interconnected nature of energy infrastructure amplifies the impact of vendor-related security incidents, as compromised third-party systems can provide attackers with access to critical operational technology networks.

Third-party risk management requires comprehensive assessment of vendor security capabilities, contractual obligations for incident reporting, and regular security auditing protocols. The complexity increases significantly in energy technology supply chains, where multiple vendors may contribute components to single systems, creating interdependent vulnerability surfaces.

| Cybersecurity Risk Metrics | Energy Sector | Industry Average |

|---|---|---|

| Third-party vendor breach involvement | 45% | 29% |

| Successful attacks via third-party access | 90% | 67% |

| Average recovery time from incidents | 287 days | 197 days |

| Financial impact per incident | $4.88 million | $3.86 million |

Infrastructure Interdependency and Cascade Effects

Modern energy infrastructure demonstrates high levels of interdependency, where disruption to one system component can trigger cascade failures across multiple connected systems. Cybersecurity incidents that compromise industrial control systems can affect not only the directly targeted facility but also downstream users and interconnected networks.

Critical system interconnections create multiple pathways for attack propagation, requiring security architectures that can isolate compromised segments while maintaining operational continuity. Recovery time analysis indicates that energy sector incidents typically require longer resolution periods due to the complexity of operational technology systems and safety requirements for restoration procedures.

Zero-Trust Security Models for Energy Infrastructure

Zero-trust security architectures assume that no system component should be automatically trusted, requiring continuous verification of user identity, device integrity, and network traffic patterns. Implementation in energy infrastructure requires careful balance between security requirements and operational efficiency, particularly for systems that require real-time response capabilities.

Key implementation components include:

-

Multi-factor authentication for all system access points

-

Network microsegmentation to limit attack propagation

-

Continuous monitoring of user behaviour and system activities

-

Automated threat detection and response capabilities

What Technologies Are Transforming Supply Chain Monitoring and Response?

Artificial Intelligence and Machine Learning Applications

Investment trends in emerging energy technologies provide insight into the technological transformation of supply chain monitoring systems. Investment in low-emissions hydrogen production projects increased by 80% year-on-year in 2025, with capital increasingly shifting toward projects with established policy backing and commercial structures.

Machine learning algorithms analyse vast quantities of operational data to identify patterns that indicate potential equipment failures, supply disruptions, or quality issues. Predictive maintenance applications can reduce unexpected downtime by 20-25% while optimising maintenance schedules to minimise operational disruption.

Demand forecasting systems utilise artificial intelligence to analyse market signals, weather patterns, and economic indicators to predict energy technology requirements across different geographic regions and time horizons. These capabilities enable proactive supply chain adjustments that can prevent shortages or overproduction scenarios.

Blockchain and Distributed Ledger Solutions

Blockchain technology provides immutable records of supply chain transactions, enabling complete traceability from raw material extraction through final product delivery. Smart contract automation can execute supplier payments, quality verification, and logistics coordination without manual intervention, reducing administrative overhead while improving accuracy.

Distributed ledger systems enable secure information sharing between supply chain participants while maintaining confidentiality of proprietary data. This capability proves particularly valuable in energy technology supply chains where multiple organisations must coordinate complex manufacturing and assembly processes.

Advanced Simulation and Digital Twin Technologies

Digital twin technologies create virtual representations of physical supply chain assets, enabling real-time optimisation and predictive analysis without disrupting actual operations. Virtual testing capabilities allow organisations to evaluate the impact of different disruption scenarios and response strategies before implementing changes to actual systems.

Deployment of carbon capture, utilisation, and storage (CCUS) technology demonstrates how advanced simulation supports technology scaling, though many announced projects have yet to reach final investment decisions. Digital twin applications can accelerate project development by identifying optimal configurations and operating parameters through simulation rather than physical prototyping.

How Can Organisations Build Multi-Layered Resilience Strategies?

Risk Assessment and Quantification Methodologies

Comprehensive resilience strategies require systematic evaluation of vulnerabilities across multiple dimensions, incorporating both quantitative analysis and qualitative assessment of emerging threats. The strategic risk framework must address different categories of potential disruptions while maintaining focus on the most likely and impactful scenarios.

Strategic Risk Framework Components:

-

Comprehensive threat landscape mapping including geopolitical, natural disaster, and technological failure scenarios

-

Value-at-risk calculations that quantify potential financial impact across different disruption timeframes

-

Probability assessment and scenario development based on historical data and expert analysis

-

Mitigation strategy cost-benefit analysis comparing investment requirements with risk reduction benefits

Vendor Risk Management and Supply Chain Governance

Analysis of manufacturing cost structures reveals significant variation in competitive factors across different energy technologies. For battery manufacturing, manufacturing efficiency and automation account for over 40% of China's cost advantage over Europe. In wind blade production, energy and labour costs represent 75% of the production cost gap, while solar PV wafer and polysilicon manufacturing show 65% cost gap attribution to energy and labour factors.

Due diligence protocols must evaluate not only current supplier capability but also long-term viability under different market and regulatory scenarios. Performance monitoring systems should track both operational metrics and early warning indicators that might signal potential supplier difficulties before they affect delivery capability.

In addition, the establishment of a battery-grade lithium refinery in regional markets can provide strategic alternatives to concentrated supply sources.

Infrastructure Diversification and Redundancy Planning

Geographic distribution strategies must balance risk mitigation benefits against the economic advantages of concentrated production. In energy-intensive upstream industries such as steel and aluminium, energy costs can represent more than two-thirds of total production costs, making access to low-cost renewable electricity a critical competitive factor.

Research indicates that hydrogen-based steelmaking could compete with conventional production in major steel-producing countries including the United States, China, and India under certain conditions, particularly where producers can access competitively-priced renewable electricity. This demonstrates how technology diversification can enhance supply chain resilience in energy technologies while maintaining economic competitiveness.

The next major ASX story will hit our subscribers first

What Role Does Manufacturing Localisation Play in Energy Security?

Reshoring Strategies and Regional Production Hubs

Manufacturing localisation requires careful analysis of cost factors that determine competitive positioning across different geographic regions. Energy and labour costs vary significantly in their importance depending on the specific technology and production stage involved.

| Manufacturing Location Factors | Battery Production | Wind Blade Production | Solar PV Manufacturing |

|---|---|---|---|

| Manufacturing efficiency/automation | 40%+ of cost advantage | 25% of cost factors | 35% of cost factors |

| Energy costs | 25% of cost factors | 75% of production gap | 65% of production gap |

| Labour costs | 35% of cost factors | Included in 75% figure | Included in 65% figure |

| Transportation and logistics | 10-15% impact | 20% impact | 15% impact |

Regional production hubs can achieve economies of scale while reducing transportation costs and supply chain complexity. However, establishing competitive manufacturing capability requires sustained investment in both physical infrastructure and workforce development over multi-year timeframes.

Technology Transfer and Capability Development

Knowledge sharing and skills development programmes form essential components of successful manufacturing localisation strategies. The complexity of energy technology manufacturing requires specialised expertise that may not exist in all geographic regions, necessitating structured technology transfer and training initiatives.

Research and development infrastructure represents a critical long-term factor in maintaining manufacturing competitiveness. Regions that invest only in assembly operations without supporting R&D capability may find themselves vulnerable to technological obsolescence as product designs evolve.

Economic Competitiveness and Industrial Policy

Government incentives and support mechanisms can influence manufacturing location decisions, though their effectiveness varies significantly depending on the underlying cost structure and competitive dynamics. Investment attraction strategies must consider not only initial capital costs but also ongoing operational competitiveness over the entire technology lifecycle.

Trade policy implications affect both import costs for components and export market access for finished products. Market access considerations become particularly important for technologies where global scale is required to achieve cost competitiveness.

How Are Emerging Technologies Reshaping Energy Supply Chain Dynamics?

Energy Storage Integration and Grid Modernisation

Battery technology advancement and deployment trends indicate accelerating integration between energy storage systems and grid infrastructure. Grid-scale storage deployment requires coordination between battery manufacturers, power electronics suppliers, and grid operators, creating new interdependencies in supply chain management.

Distributed energy resources introduce additional complexity as storage systems become distributed across multiple locations rather than concentrated in centralised facilities. This distribution pattern requires supply chain capabilities that can support maintenance and replacement operations across geographically dispersed installations.

Hydrogen Economy Development and Infrastructure Needs

The 80% year-on-year increase in low-emissions hydrogen production project investment during 2025 demonstrates accelerating commercial interest in hydrogen technologies. However, capital allocation patterns show increased selectivity, with investors focusing on projects that demonstrate clear policy backing and established commercial structures.

Transportation and storage infrastructure requirements create new supply chain categories that did not exist in conventional energy systems. Hydrogen pipeline systems, compression equipment, and specialised storage vessels require manufacturing capabilities and maintenance expertise that represent emerging market segments.

Industrial application development drives demand for hydrogen production equipment, storage systems, and distribution infrastructure. Market development requires coordination between hydrogen producers, equipment manufacturers, and end-use industries to ensure supply chain alignment across the entire value chain.

Carbon Capture and Utilisation Technology Scaling

Deployment of carbon capture, utilisation, and storage (CCUS) technology advances steadily, though many announced projects have not yet reached final investment decisions. Technical readiness assessment indicates that while core technologies have been demonstrated, commercial viability depends on policy support mechanisms and carbon pricing frameworks.

Integration with existing energy infrastructure requires specialised engineering and project management capabilities. Supply chain development for CCUS technologies must address both new equipment categories and modification of existing facilities to accommodate carbon capture systems.

What Metrics Should Organisations Use to Measure Supply Chain Resilience?

Key Performance Indicators and Benchmarking

Effective measurement of supply chain resilience in energy technologies requires metrics that capture both operational performance and vulnerability assessment across multiple dimensions. Recovery time objectives provide baseline expectations for restoration capability following different types of disruptions.

| Resilience Measurement Framework | Target Metrics | Benchmark Standards |

|---|---|---|

| Recovery Time Objectives | 24-72 hours for critical systems | Industry-specific requirements |

| Supplier Diversity Indices | Maximum 50% single-supplier dependency | Risk tolerance thresholds |

| Cost Impact Metrics | <5% of annual revenue at risk | Financial resilience standards |

| System Availability | 99.5%+ uptime for critical components | Operational excellence targets |

Supplier diversity indices measure the degree of concentration across different supplier categories and geographic regions. These metrics should account for both direct suppliers and critical sub-tier vendors that provide essential components or services to primary suppliers.

Cost impact metrics quantify the financial exposure from different disruption scenarios, enabling organisations to prioritise resilience investments based on potential economic consequences. System availability statistics track actual performance against target uptime requirements for critical infrastructure components.

Stress Testing and Scenario Planning Methodologies

Regular assessment protocols should evaluate supply chain performance under controlled stress conditions that simulate different types of potential disruptions. Testing schedules must balance the need for comprehensive evaluation against operational disruption from testing activities.

Scenario development incorporates both historical disruption patterns and emerging threat categories that may not have precedent in past experience. Impact modelling should consider not only direct effects but also indirect consequences that may emerge as disruptions propagate through interconnected systems.

Performance gap analysis compares actual system response during stress tests against predetermined resilience objectives. This analysis identifies specific areas where additional investment or process improvement could enhance overall system resilience.

Continuous Improvement and Adaptive Management

Feedback loops enable organisations to incorporate lessons learned from both actual disruptions and stress testing exercises into updated resilience planning. Learning integration requires systematic documentation of incidents and analysis of response effectiveness.

Technology upgrade and modernisation planning must consider how emerging technologies can enhance resilience capabilities while maintaining compatibility with existing systems. Investment prioritisation should balance resilience improvements against other operational requirements and budget constraints.

Stakeholder engagement ensures that supply chain resilience in energy technologies planning incorporates perspectives from all critical participants, including suppliers, customers, regulators, and community organisations. Collaboration enhancement initiatives can improve information sharing and coordinated response capabilities across the extended supply chain network.

Frequently Asked Questions About Energy Supply Chain Resilience

What Are the Most Critical Vulnerabilities in Current Energy Supply Chains?

The most significant vulnerabilities arise from geographic concentration in manufacturing capacity, particularly in intermediate production stages where alternative suppliers may not exist. Every major energy technology supply chain contains at least one step where less than 25% of global demand could be satisfied without the largest single manufacturer. For battery supply chains, this vulnerability exists in cathode material production, electrolyte manufacturing, and cell assembly. Solar PV supply chains show similar concentration in polysilicon production and wafer manufacturing stages.

How Long Does It Typically Take to Recover from Major Supply Chain Disruptions?

Recovery times vary significantly depending on the type and scope of disruption. Minor supplier issues may be resolved within days or weeks through alternative sourcing arrangements. Major disruptions affecting primary manufacturing facilities typically require 3-6 months for full restoration, assuming no permanent damage to production equipment. Geopolitical disruptions or trade restrictions may create longer-term adjustments requiring 12-24 months to establish alternative supply arrangements and qualify new suppliers.

What Investment Levels Are Required for Meaningful Resilience Improvements?

Meaningful resilience improvements typically require investment equivalent to 3-5% of annual supply chain costs, though this varies significantly based on current vulnerability levels and target resilience objectives. Organisations with highly concentrated supplier bases may need initial investments of 5-10% of annual procurement costs to establish adequate diversification. Ongoing resilience maintenance requires approximately 1-2% of annual supply chain costs for monitoring systems, supplier qualification, and emergency response capabilities.

How Do Regulatory Requirements Impact Supply Chain Resilience Planning?

Regulatory requirements increasingly emphasise supply chain transparency, cybersecurity standards, and domestic content requirements that directly affect resilience planning. Environmental regulations may limit supplier options to those meeting specific sustainability standards. National security regulations in various countries require assessment of foreign dependency levels and may mandate domestic sourcing for critical components. Organisations must integrate regulatory compliance requirements with resilience objectives to ensure that risk mitigation strategies also satisfy applicable legal and regulatory frameworks.

The analysis presented reflects current market conditions and emerging trends in energy technology supply chains. Investment decisions should consider multiple risk factors and seek appropriate professional guidance. Supply chain disruption scenarios represent potential impacts based on current concentration levels and may not account for all possible mitigation measures or market adaptations.

Ready to capitalise on the next major mineral discovery driving energy transition technologies?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in critical minerals and energy technologies ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring Discovery Alert's dedicated discoveries page, then begin your 14-day free trial today to position yourself at the forefront of the energy transition investment opportunity.