July 8, 2026

The Architecture of Sovereign Wealth: Why Gold Is Reshaping African Reserve Management

Across much of the twentieth century, developing nations built their foreign exchange buffers almost entirely around the US dollar and multilateral lending relationships. That model, deeply embedded in post-Bretton Woods financial architecture, created a structural dependency that left many African economies exposed whenever aid flows contracted, commodity prices collapsed, or donor priorities shifted. Today, a quietly transformative reorientation is underway. Several African central banks are deliberately reconfiguring their reserve portfolios toward physical gold, and Tanzania central bank gold reserves now stand as one of the most instructive examples of how this shift is being executed in practice.

Understanding Tanzania's approach requires more than noting a headline tonnage figure. It demands examining the regulatory mechanics, the economic logic, the domestic refining infrastructure, and the genuine trade-offs embedded in a gold-heavy reserve strategy.

When big ASX news breaks, our subscribers know first

Tanzania Central Bank Gold Reserves: How the Programme Actually Works

The Bank of Tanzania's gold accumulation effort did not emerge spontaneously. Its foundations were laid within the 2022/23 fiscal framework, and the legal basis for the programme sits within Section 51 of the Bank of Tanzania Act, which mandates that the country maintain international reserves sufficient to cover a minimum of four months of imports. That statutory floor created an institutional imperative to build reserves through means other than foreign currency holdings alone.

What makes the Tanzanian approach structurally distinctive is the September 2024 regulatory intervention by the country's mining regulator. Under that directive, all gold mining firms and traders involved in gold exports became legally obligated to channel at least 20% of their gold output directly to the central bank. This single regulatory mechanism transformed what had previously been a voluntary or market-driven accumulation process into a mandatory and predictable supply pipeline.

The 20% Mandate: Implications Across the Mining Sector

The consequences of this allocation requirement ripple across every tier of the gold production landscape:

- Large-scale miners face a direct reduction in freely exportable gold volume, affecting their foreign exchange revenue calculations

- Artisanal and small-scale miners (ASM) gain a formalised, structured offtake channel that removes reliance on volatile spot market intermediaries

- Export traders must integrate compliance monitoring into their logistics and accounting systems

- Domestic refineries benefit from guaranteed throughput volumes, supporting the economic viability of local processing infrastructure

The ASM dimension is particularly worth examining. Informal gold producers in Tanzania have historically sold through unregulated middlemen at prices significantly below international benchmarks. The mandatory allocation policy, while creating a compliance burden, also offers artisanal producers a degree of price stability and a formally documented transaction record. This has meaningful downstream effects on financial inclusion, a point discussed further below.

Which Refineries Are Processing Tanzania's Monetary Gold?

A less-discussed element of the programme is the deliberate use of domestic refining infrastructure. Rather than exporting raw or semi-processed gold for overseas refining, the Bank of Tanzania has directed purchases through three in-country facilities:

| Refinery | Volume Processed | Location |

|---|---|---|

| Mwanza Precious Metals Refinery (MPMR) | 3,181.3 kg | Tanzania |

| Eyes of Africa (EOA) | 979.5 kg | Tanzania |

| Geita Gold Refinery (GGR) | 385.6 kg | Tanzania |

| Total (early programme phase, as of June 2025) | 5,022.85 kg (~5.02 t) | Domestic |

This refinery architecture reflects a deliberate sovereign value-capture strategy. By processing monetary gold domestically, Tanzania retains refining margin value within its own economy rather than exporting it to international facilities. This is a meaningful, often overlooked dimension of the programme's economic logic.

How Much Gold Has Tanzania's Central Bank Accumulated?

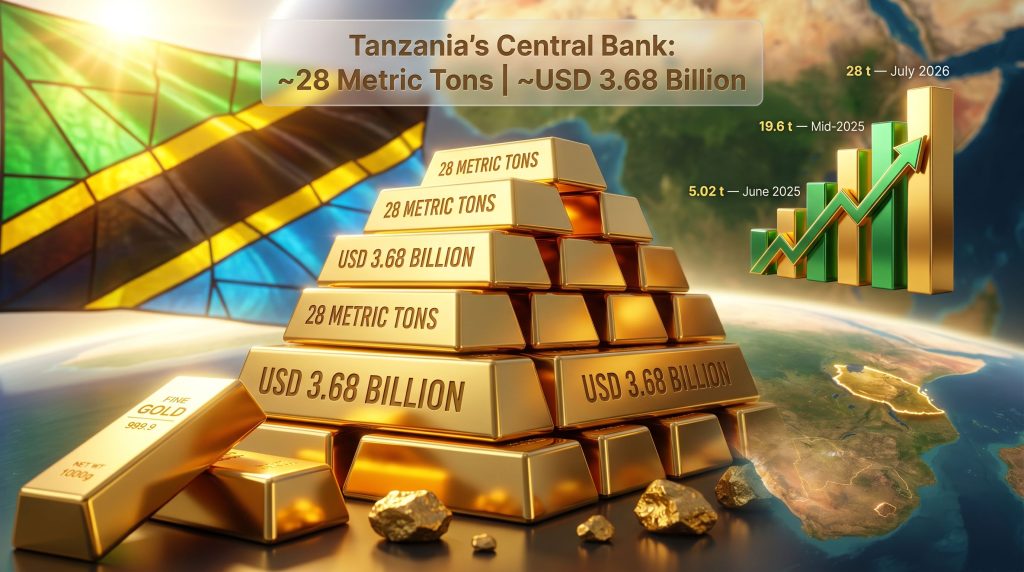

The scale of accumulation over a relatively compressed timeframe is striking. Bank of Tanzania Governor Emmanuel Tutuba, speaking at an IMF-World Bank meeting in Gambia in July 2026, confirmed that the central bank had purchased approximately 28 metric tons of gold over the preceding 18 months. At prevailing market prices, that volume carried a value of approximately USD 3.68 billion.

The accumulation timeline places this achievement in sharper relief:

| Milestone | Volume | Approximate Value | Period |

|---|---|---|---|

| Early domestic refinery throughput | ~5.02 metric tons | Partial programme value | To June 2025 |

| Monetary gold classification | ~19.6 metric tons | Undisclosed at time | Mid-2025 |

| Total confirmed purchases | ~28 metric tons | ~USD 3.68 billion | To July 2026 |

| Total reserves (gold + forex combined) | N/A | ~USD 6 to 6.5 billion | Dec 2025 to July 2026 |

What Does 28 Metric Tons Over 18 Months Actually Represent?

Translating that raw figure into an annualised rate produces approximately 18.7 metric tons per year, which places Tanzania among the most aggressive reserve accumulators in sub-Saharan Africa on a per-year basis. Critically, the programme reportedly surpassed its original 20-ton three-year target approximately 18 months ahead of schedule, a fact that signals either that the 20% mandatory allocation is producing higher throughput than anticipated, or that gold price appreciation has accelerated the reserve value build faster than volume alone would suggest.

Furthermore, according to Tanzania's total reserves data, at Governor Tutuba's last interest rate announcement prior to the July 2026 disclosure, Tanzania's total reserves, encompassing both gold and conventional foreign exchange, stood at approximately USD 6 billion, equivalent to roughly 4.3 months of import cover, placing the country above the IMF's recommended three-month minimum threshold.

The Strategic Logic: Why Tanzania Is Buying Gold

Currency Stabilisation and Shilling Credibility

The Tanzanian shilling has faced periodic depreciation pressure consistent with broader emerging market currency dynamics. Gold-backed reserve positions carry signalling value to international currency markets: they communicate that a sovereign's reserve buffer contains assets whose value is not correlated with USD monetary policy decisions or geopolitical donor sentiment. For a currency without a deep derivatives market or significant foreign investor participation in domestic debt, this kind of reserve quality matters disproportionately.

Several Sub-Saharan currencies that have experienced sharp depreciations in recent years shared a common characteristic: their reserve buffers were heavily weighted toward foreign currency positions and multilateral credit lines rather than non-correlated hard assets. Indeed, gold as a safe haven continues to attract increasing sovereign attention precisely for this reason.

Reducing Structural Aid Dependency

Tanzania, like many African economies, has historically relied to varying degrees on concessional financing and donor flows as components of its external balance management. The strategic logic of replacing this dependency with commodity-backed reserve assets rests on a simple insight: gold cannot be withheld by a foreign government or multilateral institution for political reasons. Its value is determined by global markets rather than bilateral relationships.

As global aid architectures face increasing strain from donor country fiscal pressures and shifting geopolitical priorities, this consideration has moved from theoretical to operationally relevant. A central bank holding substantial physical gold has optionality that a central bank dependent on credit lines does not. This aligns with gold's strategic role in buffering against precisely these kinds of geopolitical and inflationary pressures.

Tanzania's Position as a Leading Gold Producer

Tanzania ranks among Africa's top ten gold producers, and that fact creates a structural advantage that most gold-accumulating central banks do not enjoy. When a country can source reserve gold domestically, through a mandatory allocation from its own licensed mining sector, the acquisition does not drain foreign exchange to pay for imports. The closed-loop economic effect means mining revenue that might otherwise leave the country as repatriated profits or royalty flows is partially captured on the sovereign balance sheet.

This dynamic is conceptually comparable to Ghana's gold-for-oil programme, in which Ghana sought to use domestically produced gold to pay for oil imports rather than spending US dollars. Tanzania's approach differs in targeting reserve accumulation rather than trade settlement, but both programmes reflect the same underlying logic: using commodity production capacity to reduce external financing vulnerability.

Financial Inclusion as an Unexpected Dividend

One of the more surprising outcomes of the programme, confirmed by Governor Tutuba, is the opening of more than 4,000 new accounts at formal financial institutions by mineral traders and small-scale miners. This figure deserves more analytical attention than it typically receives.

Tanzania's artisanal mining sector has long operated largely outside formal banking. Transactions between ASM operators and intermediary buyers were commonly conducted in cash, creating AML/KYC blind spots and depriving miners of access to credit, savings products, and electronic payment infrastructure. The mandatory allocation to the central bank requires documented, traceable transactions, which in turn requires bank accounts.

The formalisation dynamic creates a compounding effect:

- Miners open accounts to participate in the programme

- Account ownership creates a transaction history

- Transaction history enables credit assessment

- Credit access enables investment in better equipment and safer operations

- Improved productivity generates more taxable revenue for the state

This sequence represents a meaningful, if underappreciated, contribution of the reserve programme to Tanzania's broader financial development agenda.

The Infrastructure Financing Debate: Should Tanzania Sell Its Gold?

The Tanzanian government has publicly examined the possibility of liquidating a portion of accumulated gold to fund infrastructure priorities including roads and power generation. This debate surfaces a genuine tension in reserve management strategy.

| Factor | Case for Retention | Case for Partial Sale |

|---|---|---|

| Gold price trajectory | Rising prices favour holding | A price plateau or correction favours selling |

| Fiscal urgency | Low urgency supports patience | High infrastructure deficit demands capital |

| Reserve adequacy | Above 4-month floor: buffer exists | Below minimum: sale may be necessary |

| Infrastructure ROI | Lower than gold appreciation rate | Higher than gold appreciation rate |

| Sovereign credit impact | Positive: stronger balance sheet | Neutral to mildly negative |

| External perception | Signals monetary discipline | May signal fiscal pressure if poorly communicated |

The Bank of Tanzania Act's Section 51 requirement sets a statutory floor on reserve holdings, meaning any liquidation decision must be calibrated against the four-month import cover minimum. This legislative constraint functions as a built-in discipline mechanism against politically motivated asset sales.

Historical precedent from IMF member states that have sold gold reserves to fund fiscal deficits suggests outcomes are highly context-dependent. Sales executed during rising price environments have often been viewed retrospectively as mistimed. The UK's gold sales between 1999 and 2002, conducted near multi-decade price lows, remain a widely cited cautionary example in central bank reserve management literature.

The next major ASX story will hit our subscribers first

How Tanzania's Reserves Compare Regionally

Tanzania's accumulation rate positions it as a notable outlier in East African monetary management. A regional and continental comparison contextualises the scale of its ambition. The World Gold Council's data on gold reserves by country further illustrates how Tanzania's trajectory compares to broader global trends:

| Country | Approximate Gold Reserves | Context |

|---|---|---|

| Algeria | ~174 metric tons | North Africa's largest holder |

| South Africa | ~125 metric tons | Historic gold production dominance |

| Egypt | ~126 metric tons | Actively expanding |

| Tanzania | ~28 metric tons (as of July 2026) | Fastest recent accumulation rate in East Africa |

| Ghana | ~8.7 metric tons | Pursuing gold-for-oil programme |

Tanzania's absolute tonnage remains modest relative to North African holders, but its annualised acquisition rate of approximately 18.7 metric tons per year exceeds most peers in sub-Saharan Africa and reflects a deliberate policy posture rather than passive reserve management. In addition, central banks influencing gold prices globally are increasingly scrutinising such programmes as models for their own accumulation strategies.

Risks and Limitations of a Gold-Concentrated Reserve Strategy

No reserve strategy is without cost, and Tanzania's approach carries identifiable risks that merit transparent analysis:

Gold price volatility: Central bank balance sheets carry mark-to-market exposure. A significant downward price movement would reduce the stated value of Tanzania's reserves without any change in physical holdings, potentially creating political pressure to liquidate at unfavourable prices.

Liquidity constraints: Gold is materially less liquid than USD or EUR holdings in acute crisis scenarios. Converting physical gold to usable foreign exchange requires either market sales, which can be price-moving at scale, or repo arrangements with counterparty banks, which carry their own structural conditions.

Concentration risk: Over-weighting a single commodity class, regardless of its historical store-of-value credentials, creates exposure that diversification across SDRs, multilateral development bank instruments, and currency baskets would reduce.

Governance and transparency: International standards, including the IMF's Special Data Dissemination Standard (SDDS) and BIS reporting guidelines, set expectations for central bank gold disclosure. Tanzania's ongoing alignment with these frameworks will be an important credibility signal to international counterparties.

Short-term forex earnings reduction: Redirecting 20% of gold exports to domestic reserves reduces the foreign exchange earnings that mining companies repatriate or that flow through export channels. The long-term offset — a stronger sovereign reserve position that reduces borrowing costs and exchange rate risk premiums — is real but operates on a longer time horizon than the immediate earnings reduction.

Frequently Asked Questions: Tanzania Central Bank Gold Reserves

How much gold does the Bank of Tanzania hold?

As of July 2026, the Bank of Tanzania had purchased approximately 28 metric tons of gold over the preceding 18-month period, with a total value of around USD 3.68 billion at prevailing market prices. Earlier 2025 data indicated that approximately 19.6 metric tons had been formally classified as monetary gold within the reserve framework.

Why is Tanzania buying gold for its reserves?

The Bank of Tanzania is accumulating gold to strengthen its international reserve position, support Tanzanian shilling stability, and reduce structural reliance on foreign aid flows and concessional lending as reserve buffer components. Moreover, global gold reserve trends in 2025 have reinforced the case for sovereign gold accumulation across emerging markets.

What is the 20% gold allocation requirement?

Since September 2024, Tanzania's mining regulator has required all gold mining companies and export traders to direct at least 20% of their gold production to the central bank, creating a mandatory domestic supply pipeline for reserve accumulation.

Is Tanzania planning to sell its gold reserves?

The Tanzanian government has publicly discussed partial liquidation to fund infrastructure development. The Bank of Tanzania has confirmed that selective sales remain consistent with its reserve management mandate under Section 51 of the Bank of Tanzania Act, provided minimum import cover thresholds are maintained.

What are Tanzania's total foreign exchange reserves?

As of late 2025 through mid-2026, Tanzania's combined reserves — encompassing both gold and conventional foreign exchange — stood at approximately USD 6 to 6.5 billion, representing roughly 4.3 to 5 months of import cover.

What Tanzania's Programme Signals for East African Monetary Policy

Tanzania central bank gold reserves are best understood not as a financial curiosity but as an early-mover template within a broader structural shift in how resource-rich African nations are approaching sovereign balance sheet management. The combination of a mandatory domestic allocation mechanism, sovereign refining infrastructure, and a statutory reserve floor creates a replicable framework that other East African gold producers could adapt to their own contexts. Consequently, the gold market surge of 2025 has only amplified interest in programmes of this kind.

For other nations considering similar approaches, Tanzania's experience suggests several transferable lessons: the importance of legislative foundations rather than voluntary frameworks, the value of domestic processing capacity in capturing refining margin, and the underestimated financial inclusion dividend that formalised commodity transactions can generate at scale.

Whether Tanzania ultimately chooses to hold its accumulated gold through a full commodity cycle or selectively monetise portions for infrastructure investment, the programme has already demonstrated that a developing economy with significant domestic gold production can meaningfully reshape its reserve quality profile within a compressed timeframe. That outcome will not go unnoticed by central bank policymakers across the region.

This article is intended for informational purposes only and does not constitute financial or investment advice. Reserve valuation figures are based on reported prices at the time of disclosure and are subject to change with gold market movements. Readers should consult qualified financial professionals before making investment decisions.

Want to Profit From the Next Major Gold Discovery Before the Broader Market Notices?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX gold and mineral discoveries, transforming complex geological data into actionable investment insights the moment they are announced. Start your 14-day free trial today, or explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns for well-positioned investors.