July 4, 2026

The global financial landscape stands at a critical juncture as discussions around a Trump monetary reset gain momentum, fundamentally challenging the established monetary framework that has governed international commerce for decades. The intersection of fiscal policy, military expenditure, and currency dynamics creates complex feedback loops that traditional economic models struggle to predict. Understanding these interconnected forces becomes essential for investors, policymakers, and institutions navigating an environment where established norms may no longer provide reliable guidance.

Central banks across major economies find themselves reconsidering foundational assumptions about independence, inflation targeting, and international coordination. The relationship between defense spending and currency valuation has emerged as a critical variable in global economic planning, challenging conventional wisdom about how military expenditure affects national competitiveness. These dynamics suggest that monetary policy discussions must expand beyond traditional interest rate mechanisms to encompass broader questions of imperial finance and international power projection.

Understanding the Trump Administration's Monetary Strategy

What Does "Monetary Reset" Actually Mean in Trump's Context?

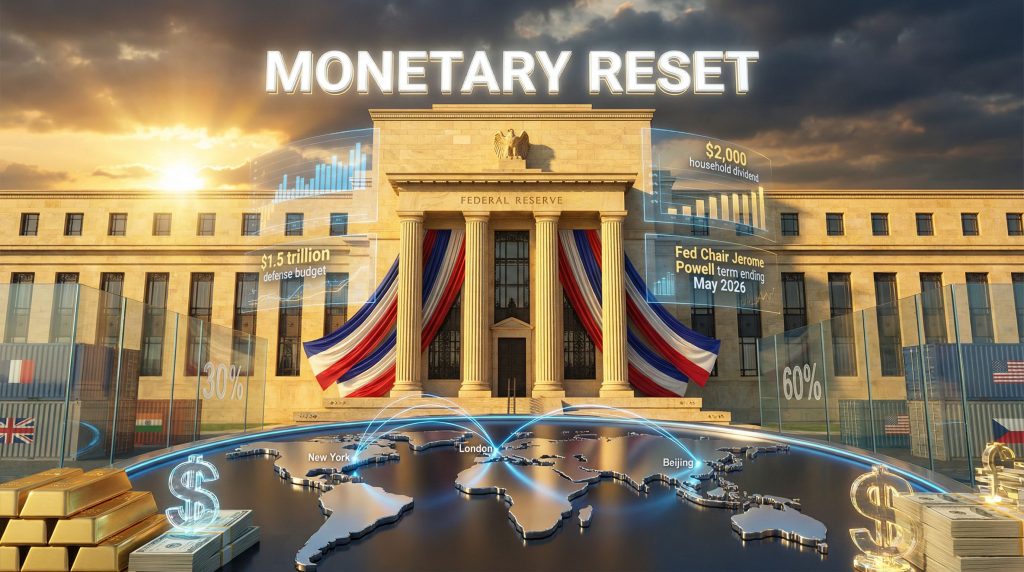

The term "monetary reset" encompasses a range of policy proposals designed to address structural imbalances in the global trading system. The administration's economic team, including Treasury Secretary Scott Bessent, trade official Peter Navarro, and senior economic adviser Stephen Miran, has articulated concerns about substantial current account and trade deficits that they attribute partially to dollar strengthening driven by military expenditures. These officials share what observers describe as visceral anger about America's perceived victimisation within the existing monetary framework.

The scope of proposed changes extends beyond traditional Federal Reserve pressure tactics toward systematic currency policy overhaul. Policy instruments under consideration include tariff-funded initiatives, interest rate manipulation through central bank pressure, and fiscal redistribution mechanisms designed to extract payments from dollar-holding nations. These proposals represent a departure from post-World War II monetary cooperation frameworks that have governed international finance.

Distinguishing documented policies from online speculation requires careful analysis of official statements and published frameworks. Stephen Miran's November 2024 essay, "A User's Guide to Restructuring the Global Trading System," provides concrete evidence of strategic thinking within the administration. This document envisions converting what Miran characterises as "Pax Americana into Tax Americana," whereby holders and users of US dollars would be persuaded to convert their holdings into long-term securities as payment for continued military protection.

Why Traditional Monetary Policy May Be Inadequate for Trump's Goals

Current account deficit pressures drive policy innovation beyond conventional central banking tools. The United States maintains substantial trade deficits that administration officials view as symptomatic of an unfair international system where trading partners benefit from currency devaluation whilst America bears the costs of global military presence. This creates what economists term the "dollar strength paradox," wherein military spending generates currency appreciation that undermines manufacturing competitiveness.

Manufacturing competitiveness concerns reflect broader anxieties about American economic position in a multipolar world. Traditional monetary policy operates through interest rate adjustments that affect borrowing costs and investment decisions. However, these mechanisms may prove insufficient for addressing structural trade imbalances that result from currency dynamics driven by geopolitical rather than purely economic factors.

The administration's approach reflects scepticism about whether existing Federal Reserve tools can adequately address what they perceive as fundamental flaws in the international monetary system. Furthermore, military expenditure creates demand for dollars in foreign exchange markets, contributing to appreciation pressure that benefits consumers purchasing imported goods but disadvantages domestic manufacturers competing globally or against imports in domestic markets.

When big ASX news breaks, our subscribers know first

Federal Reserve Independence Under Pressure

How Trump Plans to Influence Interest Rate Policy

Legal challenges targeting Fed Chair Jerome Powell centre on allegations of "gross incompetence" in monetary policy management. These potential lawsuits would need to overcome substantial jurisprudential hurdles, as courts have generally interpreted "for cause" removal provisions narrowly to preserve institutional independence. Federal Reserve Board governors, including the Chair, serve fixed terms and can be removed only for demonstrated malfeasance, neglect of duty, or violation of law.

Timeline constraints create definitive parameters for potential succession planning, with Powell's term scheduled to conclude on May 15, 2026. This provides a clear window for policy transitions and strategic positioning. The Federal Open Market Committee's structure, consisting of seven Board of Governors members and five rotating Federal Reserve Bank presidents, disperses decision-making authority across multiple individuals with fixed, staggered terms.

Market implications of reduced central bank independence could trigger significant financial disruptions. The term structure of interest rates incorporates market expectations about future monetary policy, inflation prospects, and economic growth. If market participants believe Federal Reserve decisions will be subordinated to short-term political considerations rather than long-term price stability objectives, long-term interest rates could rise substantially to compensate investors for increased inflation risk.

What Aggressive Rate Cuts Could Mean for Markets

Inflation risk scenarios under politically-driven monetary policy draw lessons from historical episodes of compromised central bank independence. The Arthur Burns Federal Reserve during the early 1970s, operating under Nixon administration pressure to maintain accommodative policy despite emerging inflation pressures, contributed to the "Great Inflation" that ultimately required painful contractionary measures under Paul Volcker's chairmanship to reverse.

Currency devaluation strategies and international competitive responses create complex feedback loops throughout the global financial system. If aggressive rate cuts are perceived as politically motivated rather than economically justified, inflation expectations could become unanchored, leading to higher long-term interest rates even as short-term rates decline. This phenomenon would steepen the yield curve in economically counterproductive ways.

Asset bubble formation in equity and real estate markets represents a significant risk under scenarios where interest rates are pushed below economically justified levels through political pressure. The transmission mechanism of monetary policy operates through multiple channels, including effects on borrowing costs, exchange rates, asset prices, and credit availability. Disrupting these mechanisms through non-economic interference could create unintended consequences that reduce policy effectiveness.

The Tariff-Funded Economic Model

Can Tariffs Really Fund a $2,000 Household Dividend?

Revenue mathematics reveal substantial challenges in funding proposed expenditures through tariff income alone. A $2,000 household dividend would require approximately $660 billion annually based on current household counts, whilst realistic tariff revenue projections range from $80-120 billion under aggressive implementation scenarios. This creates a funding gap of $540-580 billion that would require alternative financing mechanisms or significant reduction in promised benefits.

| Policy Promise | Estimated Annual Cost | Available Tariff Revenue | Funding Gap |

|---|---|---|---|

| $2,000 household dividend | $660 billion | $80-120 billion | $540-580 billion |

| Defence spending increase | $500 billion | Shared revenue pool | Substantial shortfall |

| Infrastructure projects | $200 billion | Shared revenue pool | Major deficit |

| Tax reduction extensions | $400 billion | Shared revenue pool | Critical shortage |

Historical precedent analysis from the 1930s provides cautionary lessons about tariff-based revenue systems. The Smoot-Hawley Tariff Act raised average tariff rates to approximately 20 percent on dutiable imports, though actual revenue generated fell short of projections due to contraction in international trade volumes following implementation. Economic efficiency concerns arise because tariffs function as regressive taxation that disproportionately affects lower-income households through higher consumer prices.

Legal constraints under the International Emergency Economic Powers Act (IEEPA) and constitutional provisions governing congressional authority over international commerce create potential obstacles to executive tariff implementation. Supreme Court challenges to IEEPA-based tariffs could establish precedents limiting presidential authority to impose trade restrictions without congressional approval, particularly for revenue generation rather than national security purposes.

Why Multiple Tariff-Funded Promises Create Fiscal Contradictions

The double-counting problem emerges when the same revenue stream funds multiple policy priorities simultaneously. Administration proposals for tariff-funded household dividends, defence spending increases, infrastructure projects, and tax reduction extensions collectively exceed realistic tariff revenue by several trillion dollars over a ten-year period. This mathematical impossibility requires either substantial modification of proposed spending or alternative funding sources.

International retaliation risks escalate as trading partners implement responsive measures to protect their economic interests. Trade war dynamics create negative-sum outcomes where all participating nations experience reduced economic welfare, potentially destroying more value than tariffs affecting investment markets generate in revenue. Historical episodes of trade conflict demonstrate how quickly protective measures can spiral into comprehensive commercial warfare.

Economic efficiency concerns extend beyond revenue adequacy to fundamental questions about optimal taxation systems. Modern economies typically rely on diversified revenue sources including income taxes, corporate taxes, and consumption taxes rather than trade barriers, which economists generally view as distortionary mechanisms that reduce overall economic welfare by protecting inefficient domestic industries from international competition.

Defence Spending and Fiscal Reality

The $1.5 Trillion Defence Budget Proposal

Comparison to current spending levels reveals the magnitude of proposed increases relative to existing baselines. The FY 2025 defence budget baseline of approximately $886 billion would need to expand by roughly 70 percent to reach $1.5 trillion annually. This represents the largest peacetime military spending increase in American history, exceeding even Cold War peaks when adjusted for inflation and economic size.

Strategic justification for these expenditures centres on military modernisation requirements and global presence expansion to counter emerging threats from peer competitors. Defence officials argue that technological advances in hypersonic weapons, artificial intelligence, cyber warfare, and space-based systems require substantial investment to maintain American military superiority. Additionally, alliance relationships demand increased American presence in multiple theatres simultaneously.

Debt implications prove severe under scenarios where defence spending increases proceed without corresponding revenue increases or spending reductions elsewhere. Adding $614 billion annually to federal expenditures would contribute approximately $6.1 trillion to national debt over ten years, assuming standard interest costs and debt service requirements. This would push federal debt-to-GDP ratios toward levels historically associated with wartime emergencies.

How Defence Spending Connects to Monetary Strategy

Dollar demand creation through military expenditure cycles operates through balance of payments mechanisms that affect currency valuation. Government spending on overseas military installations and operations creates demand for dollars in foreign exchange markets, contributing to appreciation pressure on the currency. This relationship forms a core component of the administration's analysis regarding how military commitments affect trade competitiveness.

Alliance cost-sharing mechanisms represent potential revenue streams to offset domestic military investment. NATO partnership contributions and Pacific security arrangements could generate substantial foreign payments if restructured according to administration proposals. The concept involves transforming military protection from a public good provided freely by the United States into a subscription service requiring payment from beneficiaries.

Weapons export revenue offers another avenue for offsetting military expenditure through commercial sales to allied nations. Historical precedents demonstrate how major powers have used arms sales to recoup development costs whilst maintaining technological superiority through controlled proliferation. However, export revenue typically represents a small fraction of total development and procurement costs for major weapons systems.

International Implications and Currency Competition

How Other Nations Might Respond to US Monetary Pressure

European Central Bank policy adjustments would likely prioritise maintaining competitiveness against aggressive American monetary expansion. If Federal Reserve policy becomes subordinated to political pressure for sustained accommodation, European policymakers face difficult choices between matching American policies and risking currency appreciation that damages export competitiveness, or maintaining independent policies and accepting potential trade disadvantages.

Chinese yuan strategy under increased tariff pressure involves complex calculations about currency positioning, trade relationships, and financial system stability. Beijing's response options include allowing yuan depreciation to offset tariff impacts, accelerating domestic consumption transition to reduce export dependence, or developing alternative trade settlement mechanisms that bypass dollar-denominated transactions.

Emerging market currency hedging against dollar volatility becomes increasingly critical as monetary policy uncertainty increases. Developing nations typically face greater vulnerability to currency crises during periods of dollar strength or weakness, requiring sophisticated risk management strategies including foreign exchange reserves diversification and alternative payment system development.

Historical Parallels: Imperial Finance Models

Roman conquest-based funding provides instructive parallels to contemporary extraction-based economic policy proposals. The Roman Empire sustained itself through military campaigns that generated revenue via appropriation of precious metals, agricultural production, and tax collection from conquered territories. This system proved effective during expansion periods but created fiscal pressures when territorial growth ceased or maintenance costs exceeded acquisition benefits.

The British consol system offers a more sophisticated model of imperial finance through market mechanisms rather than direct extraction. Consols, or consolidated annuities, were perpetual bonds that paid fixed interest rates indefinitely without principal repayment obligations. This allowed Britain to maintain substantial debt levels whilst financing military operations and colonial administration across multiple continents through willing investor participation.

Isaac Newton's 1717 mint ratio decision demonstrates how seemingly technical monetary adjustments can reshape international economic relationships. As master of the mint, Newton established currency ratios that reduced silver circulation relative to gold, inadvertently setting Britain on a trajectory toward the world's first formal gold specie standard. This decision had profound implications for British monetary policy and international trade throughout the subsequent century.

What Countries Can Do to Reduce Dollar Dependency

Bilateral trade settlement mechanisms bypass American currency through direct exchange rate arrangements between trading partners. Countries including Russia, China, Iran, and India have developed systems for conducting commerce in local currencies or alternative units of account, reducing exposure to dollar-based payment systems and potential American sanctions enforcement.

Central bank digital currencies (CBDCs) represent technological alternatives to dollar-dominated international payments. Multiple nations including China, the European Union, and numerous emerging economies are developing sovereign digital currencies designed to facilitate cross-border transactions without relying on American-controlled financial infrastructure. These systems could potentially enable large-scale trade finance operations independent of dollar clearing systems.

Commodity-backed currency experiments explore alternative stores of value and exchange media based on physical assets rather than fiat currency systems. Proposals for gold-backed payment systems, oil-denominated trade currencies, and basket currencies incorporating multiple commodities aim to provide stability and independence from any single national currency, though practical implementation faces substantial technical and coordination challenges.

Market Scenarios and Investment Implications

Scenario 1: Successful Fed Pressure Campaign

Interest rate trajectory under successful political pressure would likely involve aggressive cuts despite inflation concerns, potentially driving federal funds rates below neutral levels for extended periods. This scenario assumes political pressure succeeds in overcoming Federal Reserve independence, leading to accommodation beyond what economic fundamentals would justify. Market participants would face challenges distinguishing between legitimate economic policy and political manipulation.

Equity market response would likely involve significant sector rotation as different industries benefit or suffer from sustained low interest rates and accompanying currency effects. Growth stocks typically outperform value stocks during low rate environments, whilst financial sector profitability faces pressure from compressed net interest margins. Real estate investment trusts and utilities often benefit from lower discount rates applied to their cash flows.

Bond market dynamics would reflect complex interactions between artificial rate suppression and market perceptions of inflation risk and policy credibility. Whilst short-term Treasury yields might decline due to Federal Reserve actions, longer-term yields could rise if investors demand compensation for expected inflation acceleration or reduced confidence in monetary policy effectiveness.

Scenario 2: Tariff Revenue Falls Short of Promises

Fiscal crisis management becomes necessary when tariff income proves insufficient to fund promised expenditures, forcing choices between emergency spending cuts, debt expansion, or alternative revenue sources. Historical precedents suggest that politically popular spending programmes prove difficult to reduce once established, creating pressure for debt financing or tax increases that could undermine the original policy objectives.

Political backlash scenarios develop when promised benefits fail to materialise due to inadequate funding, potentially affecting midterm elections and subsequent policy directions. Voter expectations established during campaign periods create accountability pressures that may force policy modifications or abandonment if economic reality contradicts political promises.

Market confidence erosion emerges when fiscal sustainability questions affect government borrowing costs and credit ratings. International investors holding substantial Treasury securities may demand higher yields if debt dynamics deteriorate significantly, creating feedback effects where increased borrowing costs exacerbate fiscal challenges and reduce policy flexibility.

Scenario 3: International Currency Coalition Formation

Alternative payment systems development accelerates when multiple nations coordinate responses to American monetary pressure. SWIFT bypass mechanisms already under development by various countries could achieve critical mass if geopolitical tensions drive broader adoption. These systems would enable large-scale international transactions without exposure to American sanctions or dollar-based clearing requirements.

Regional currency blocs may emerge as Asia-Pacific and European responses to dollar weaponisation. Historical precedents including the European Monetary System demonstrate how regional cooperation can create alternatives to dominant international currencies, though coordination challenges and varying national interests complicate implementation of comprehensive alternatives.

Furthermore, commodity trading shifts toward alternative settlement currencies could fundamentally alter global commerce patterns. Oil, gold, and agricultural products represent enormous markets currently dominated by dollar-denominated transactions. Shifts toward euro, yuan, or basket currency pricing could reduce global dollar demand and affect American monetary policy transmission mechanisms.

The next major ASX story will hit our subscribers first

What This Means for Different Asset Classes

Equity Markets Under Monetary Reset Conditions

Sector winners in a monetary reset environment likely include defence contractors benefiting from increased military spending, domestic manufacturers gaining from tariff protection, and infrastructure companies receiving government investment. These sectors would benefit from policy tailwinds but face risks from potential retaliation, inflation pressures, and debt sustainability concerns affecting overall economic growth.

Sector losers would include import-dependent industries facing higher input costs, multinational corporations dealing with trade disruption, and financial services companies operating internationally. Technology companies with global supply chains and manufacturing operations could face particular challenges from tariff escalation and potential technology transfer restrictions.

Volatility expectations increase significantly during periods of monetary policy uncertainty and international trade conflict. Historical analysis suggests that policy uncertainty creates elevated market volatility as investors struggle to price assets without clear understanding of future regulatory and economic environments. This creates both risks and opportunities for active investment strategies.

Fixed Income Strategy Adjustments

Treasury yield predictions under Federal Reserve pressure scenarios become extremely complex due to competing forces affecting different yield curve segments. Short-term yields may decline due to political pressure for accommodation, whilst long-term yields could rise due to inflation concerns and reduced policy credibility. This potential yield curve steepening creates challenges for traditional fixed income strategies.

Corporate credit implications arise from tariff cost pass-through effects that could pressure profit margins across multiple industries. Companies unable to pass higher input costs to consumers may face earnings pressure affecting credit quality, whilst those with pricing power may benefit. Credit analysis must incorporate potential trade policy impacts alongside traditional financial metrics.

Municipal bond considerations include potential federal spending redirection that could affect state and local government finances. Infrastructure spending priorities may shift toward federal programmes, reducing local investment capacity. Additionally, economic disruption from trade policies could affect local tax bases supporting municipal bond payments.

Commodities and Alternative Assets

Gold price dynamics reflect competing forces between safe haven demand during periods of monetary uncertainty and potential dollar strength from military spending and geopolitical tension. Historical precedents suggest gold often benefits during currency crises and inflation acceleration, though performance varies depending on real interest rate movements and opportunity costs relative to other assets.

Energy market shifts toward domestic production incentives and import tariffs could create significant price distortions affecting both producers and consumers. American oil and gas companies might benefit from protection against foreign competition, whilst refiners and chemical companies using imported feedstocks could face cost pressures. These dynamics would affect energy sector investment attractiveness and broader economic competitiveness.

Real estate implications vary significantly by location and property type due to interest rate sensitivity and regional economic effects. Industrial real estate could benefit from manufacturing reshoring incentives, whilst retail properties might suffer from reduced consumer spending power due to tariff-induced price increases. Regional variations would reflect local exposure to international trade and military spending.

Risk Management for Investors and Institutions

Portfolio Diversification Strategies

Geographic allocation adjustments become essential for reducing concentration risk in dollar-denominated assets during periods of monetary uncertainty. International diversification provides potential hedges against American policy mistakes whilst creating exposure to economies that might benefit from shifts away from dollar dependence. However, global economic integration means few assets provide complete insulation from American monetary policy changes.

Currency hedging techniques using forward contracts and options strategies offer protection against exchange rate volatility during Trump monetary reset periods. Sophisticated institutional investors can implement dynamic hedging programmes that adjust exposure based on evolving policy developments and market conditions. However, hedging costs may increase during volatile periods when protection becomes most valuable.

Alternative investment vehicles including REITs, commodities, and international exposure provide potential diversification benefits during periods of conventional market stress. Real estate investment trusts offer inflation protection and alternative income streams, whilst commodity exposure provides hedges against currency debasement. International investments enable participation in economies potentially benefiting from shifts away from American economic dominance.

Institutional Response Planning

Central bank reserve management strategies increasingly focus on diversification away from American Treasury securities toward alternative stores of value. Foreign central banks holding substantial dollar reserves face complex decisions about optimal portfolio composition during periods when American monetary policy may become less predictable. Alternative reserve assets including gold, other national currencies, and International Monetary Fund Special Drawing Rights provide diversification options.

Corporate treasury strategies must adapt to multi-currency cash management requirements as international trade patterns potentially shift. Companies with significant international operations need sophisticated currency risk management systems capable of handling multiple settlement currencies and payment mechanisms. This includes developing relationships with banks and payment systems outside traditional American-dominated networks.

Pension fund adjustments for long-term liability matching under new monetary conditions require careful analysis of inflation protection and currency risk. In addition, pension funds with multi-decade payout obligations must consider how monetary reset scenarios might affect purchasing power and real returns. This may require increased allocation to inflation-protected securities and real assets providing protection against currency debasement.

Long-Term Systemic Implications

What Happens If the Dollar Loses Reserve Currency Status?

Transition timeline estimates based on historical precedents suggest reserve currency changes typically occur over decades rather than years due to enormous infrastructure and institutional requirements. The British pound's displacement by the dollar required multiple crisis periods spanning from World War I through the 1970s. However, modern financial systems' speed and interconnectedness might accelerate transition timelines if confidence deteriorates rapidly.

Economic adjustment costs would include substantial disruption to trade finance systems, international business operations, and financial market infrastructure. American economic benefits from reserve currency status include reduced borrowing costs, enhanced monetary policy transmission, and substantial seigniorage revenues. Losing these advantages would require fundamental adjustments to fiscal policy and international economic relationships.

Geopolitical consequences extend beyond economics to military projection capabilities and alliance structures. Reserve currency status enables the United States to finance military operations globally without immediate balance of payments constraints. Alternative arrangements would require either reduced international military presence or substantially different financing mechanisms potentially affecting alliance relationships and global security arrangements.

Building Financial System Resilience

Regulatory framework adaptations for banking supervision under new monetary conditions require updated stress testing scenarios and capital requirements reflecting potential policy regime changes. Traditional banking regulation assumes relatively stable monetary policy frameworks and international trade relationships. For instance, Trump monetary reset scenarios create new risk categories requiring regulatory response and supervisory preparation.

International cooperation mechanisms through G7 and G20 coordination face substantial challenges when major economies pursue conflicting monetary policies. Historical precedents from the 1930s demonstrate how quickly international economic cooperation can deteriorate during crisis periods. Maintaining coordination mechanisms becomes essential for preventing competitive currency devaluations and trade conflicts from spiralling into broader economic warfare.

Technology infrastructure development for digital payment systems and blockchain alternatives provides potential foundations for more resilient international finance. Distributed ledger technologies enable payment systems less dependent on centralised institutions or national governments, though technical challenges and energy requirements limit near-term scalability. Central bank digital currencies represent more immediate alternatives to traditional payment infrastructure.

Consequently, the implications of US tariffs, inflation & debt under a restructured monetary system demand careful consideration from all market participants. The potential for US-China trade war effects to accelerate monetary system changes adds urgency to these preparations. However, global market recession insights suggest that economic disruption from monetary reform could exceed current projections.

Furthermore, understanding the broader context of these monetary changes becomes crucial for institutional planning. Additionally, exploring potential alternatives to traditional monetary systems provides insight into the scope of proposed changes.

Disclaimer: This analysis contains speculative elements regarding potential policy changes and their economic impacts. Monetary policy scenarios involve significant uncertainty, and actual outcomes may differ substantially from projected scenarios. Investors should conduct thorough due diligence and consider consulting financial advisors before making investment decisions based on political or policy speculation. Market predictions and economic projections represent analytical scenarios rather than guaranteed outcomes. Past performance of monetary policy regimes does not guarantee future results under different economic conditions.

Looking to Position Your Portfolio for Potential Monetary Policy Shifts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, providing investors with immediate insights into actionable opportunities that could prove particularly valuable during periods of monetary uncertainty and currency volatility. With historic discoveries demonstrating exceptional returns potential, explore Discovery Alert's dedicated discoveries page to understand how major mineral finds have delivered substantial market gains, and begin your 30-day free trial today to position yourself ahead of evolving market conditions.