June 2, 2026

The Brownfield Advantage: Why Underground Gold Expansion Is Reshaping Capital Allocation in Mining

The economics of gold mining have never been straightforward, but one principle has endured across commodity cycles: it almost always costs less to grow what you already have than to build something new. Brownfield expansion, the practice of extending production from existing underground infrastructure, has quietly become one of the most capital-efficient strategies available to mid-tier precious metals producers. When a processing plant sits partially underutilised, when shaft infrastructure is already sunk, and when regulatory relationships are already established, the incremental cost of adding ore tonnes to the feed can be a fraction of what a greenfield development would demand. This structural logic sits at the heart of the Pan American Silver Timmins expansion drive currently unfolding in northern Ontario.

When big ASX news breaks, our subscribers know first

Understanding the Timmins Gold Belt and Why Its Depth Matters

The Timmins district in Ontario is not a newcomer to gold mining. The region has produced gold continuously for over a century, making it one of the most historically significant gold-producing corridors in the western hemisphere. What is less commonly understood by observers outside the sector is that the Timmins camp's geological prospectivity extends to considerable depth along structural corridors that remain incompletely tested by historical drilling.

Underground gold systems in this part of the Canadian Shield are typically hosted in shear zone networks associated with Archean-age greenstone belts. These geological settings are known for their persistence at depth, meaning that mineralisation does not simply terminate at the limits of existing workings. This geological characteristic is precisely what underpins the rationale for vertical shaft development programs: the ore system continues downward, and the capital question becomes one of access cost versus in-situ value.

The Timmins operation currently comprises two underground gold mines, Timmins West and Bell Creek, positioned approximately 34 kilometres apart and feeding a single centralised processing facility at Bell Creek. This configuration is itself an underappreciated structural advantage. Operating two geologically distinct ore sources through shared surface infrastructure distributes fixed overhead costs across a larger ore base, improving unit economics even before any expansion capital is deployed.

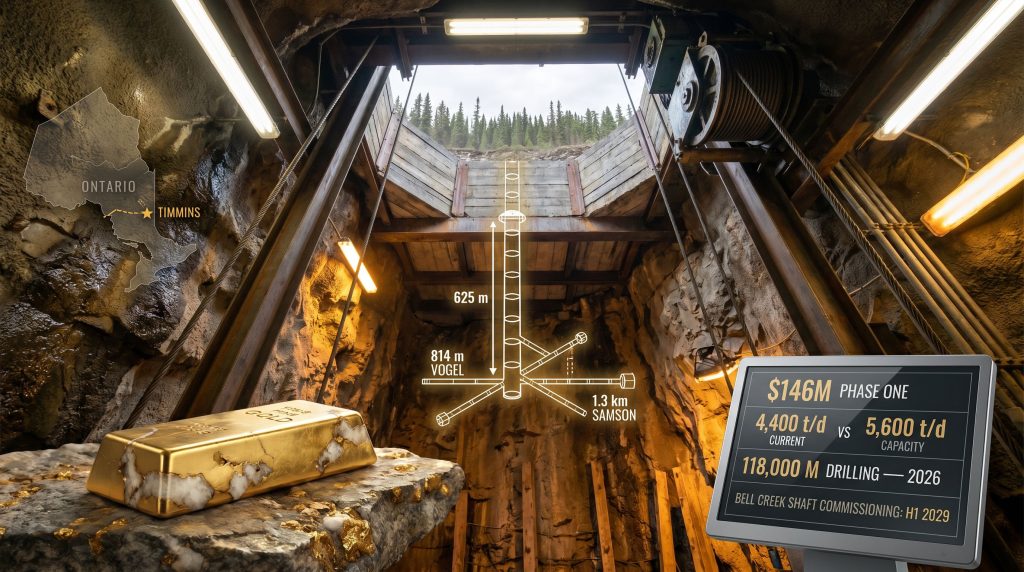

Breaking Down the $146 Million Phase One Investment

The approved Phase One capital program totals $146 million and encompasses three distinct underground development components, each designed to open access to resources that cannot currently be economically extracted. Furthermore, this underground mine study framework closely mirrors approaches used in comparable brownfield programs elsewhere in the sector.

| Project Component | Scope | Construction Start | Target Commissioning |

|---|---|---|---|

| Bell Creek Shaft Extension | 625 m vertical development | July 2026 | H1 2029 |

| Vogel Access Drift | 814 m lateral development | In progress | TBC |

| Samson Exploration Drift | 1.3 km lateral development | In progress | TBC |

The Bell Creek shaft extension of 625 metres represents the most capital-intensive single element, enabling access to deeper mineralisation below the existing workings. Shaft sinking in Canadian underground hard-rock environments is among the most technically demanding and cost-sensitive activities in the sector, subject to geotechnical risk from varying rock mass conditions, groundwater inflows, and the precision requirements of blast-hole development at depth.

The Vogel deposit access drift at 814 metres and the Samson exploration drift at 1.3 kilometres are lateral development headings, meaning they advance horizontally from existing infrastructure to intersect satellite ore bodies. This approach is more cost-efficient per metre advanced than vertical shaft sinking, but the return on investment depends entirely on whether resource conversion drilling confirms sufficient grade and tonnage to justify bulk mining.

A key aspect of capital discipline in this program is that the 2026 spending component is already embedded within Pan American Silver's existing project capital guidance range of $40 million to $43 million, meaning no revision to current financial guidance is required.

This pre-absorption of capital into guidance is not a trivial detail. It signals that management has sequenced the investment program with balance sheet stability in mind, reducing the risk of capital surprises for investors monitoring the company's broader portfolio allocation. In addition, a definitive feasibility study process will ultimately be required before Phase Two capital commitments can be confirmed.

The Processing Plant Gap: 1,200 Tonnes Per Day of Untapped Value

One of the least-discussed aspects of the Timmins expansion story is the throughput gap at the Bell Creek processing facility. The plant carries a design capacity of approximately 5,600 tonnes per day, yet current operations are feeding it roughly 4,400 tonnes per day. That difference of approximately 1,200 tonnes per day represents installed infrastructure that is effectively idle.

In mill economics, processing plants carry substantial fixed cost structures covering power, reagents, maintenance, and labour that are largely invariant to throughput volume within a broad operating range. When a plant runs below design capacity, those fixed costs are spread over fewer recovered ounces, increasing the cost per ounce of production. Conversely, as incremental ore tonnes are added to the feed from new sources like Vogel and Samson, the fixed cost burden per ounce progressively declines.

This dynamic creates what mine economists sometimes call the throughput leverage effect: the marginal economics of additional ore tonnes processed through an underutilised plant are substantially more attractive than the average economics of the existing operation, because the new tonnes carry only marginal processing costs rather than a full share of fixed overheads.

Why Spare Capacity Changes the Expansion Economics

- Additional ore from satellite deposits is processed at marginal cost, not full capital replacement cost.

- Fixed infrastructure including haulage systems, ventilation, power reticulation, and surface facilities is already in place and paid for.

- The incremental capital required to fill spare capacity is the underground development cost only, a fraction of what a standalone processing plant would require.

- Closing the 1,200 t/d throughput gap would represent a production uplift of approximately 27% relative to current operating rates, without any processing plant expansion capital.

Vogel and Samson: The Satellite Deposit Strategy Explained

The integration of satellite deposits into a centralised processing hub is a well-established strategy in Canadian underground gold mining, but its execution carries meaningful geological risk. The 814-metre Vogel drift and the 1.3-kilometre Samson drift are development headings designed to establish physical access and enable drill platforms from which resource conversion drilling can be conducted underground.

Resource conversion is a critical concept for investors to understand. Inferred mineral resources, the lowest confidence category in the international resource classification framework, cannot be counted in mine plans or used for feasibility-level economic assessments. To progress toward production, inferred resources must be upgraded to indicated or measured status through systematic infill drilling that reduces geological uncertainty to acceptable levels. The 118,000 metres of drilling planned at Timmins during 2026 is specifically targeted at this conversion process.

Correctly interpreting drill results from this program will be essential for investors assessing whether resource conversion is tracking at the grade and continuity needed to support Phase Two decisions. This scale of drilling — approximately 118,000 metres — is substantial for a single operating camp and reflects the company's commitment to generating the resource confidence needed to justify further capital allocation. To contextualise this figure, 118,000 metres represents roughly 118 kilometres of drill hole, a volume that, if successful, could materially redefine the resource inventory underpinning the mine's long-term production schedule.

The Phased Development Timeline: From Access to Production

Stage 1: Infrastructure Development (2026 to 2029)

- Bell Creek shaft extension construction commences on-site in July 2026.

- Vogel and Samson access drifts advance concurrently from existing underground workings.

- The 118,000-metre drilling program generates resource conversion data through 2026.

- Updated mineral reserve and resource estimates for Timmins, Vogel, and Gold River are anticipated around June 30, 2026, with a broader corporate-level update expected in Q3 2026.

Stage 2: Resource Conversion and Mine Planning (2027 to 2028)

- Continued infill drilling upgrades inferred resources toward indicated and measured classification.

- Metallurgical test work evaluates ore blending ratios and recoveries from new ore sources.

- Engineering studies advance toward feasibility-level assessment for satellite deposit integration.

Stage 3: Production Ramp-Up and Throughput Optimisation (2029 onwards)

- Bell Creek shaft extension commissioned, targeting H1 2029.

- Satellite deposit ore begins contributing to Bell Creek mill feed.

- Throughput progressively approaches the 5,600 t/d design ceiling.

- Extended mine life materialises as newly defined reserves enter the production schedule.

The next major ASX story will hit our subscribers first

Brownfield vs. Greenfield: A Structural Comparison

| Factor | Brownfield Expansion at Timmins | Typical Greenfield Development |

|---|---|---|

| Processing Infrastructure | Already installed and operating | Full capital outlay required |

| Permitting Complexity | Lower (existing site approvals) | Higher (new environmental assessments) |

| Community Relationships | Established over decades | Must be built from scratch |

| Capital Efficiency | Higher (incremental investment only) | Lower (full build-out required) |

| Time to First Ore | Shorter (infrastructure already in place) | Longer (multi-year surface construction) |

| Geological Risk Profile | Partially derisked by existing mine data | Higher uncertainty in new terrains |

The Timmins brownfield model benefits from something greenfield projects almost never have: decades of geological data from adjacent and overlying mine workings. Underground drilling from existing drifts, combined with historical production records and geophysical surveys, provides a geological context for new resource targeting that simply cannot be replicated at a brand new site. According to Pan American Silver's Timmins operations page, the combined asset base has been developed over many decades of continuous operation, reinforcing the depth of institutional knowledge underpinning this expansion.

Key Risk Factors Investors Should Monitor

The Pan American Silver Timmins expansion drive carries genuine execution risks that deserve transparent assessment alongside the strategic opportunity.

- Shaft development geotechnical risk: The 625-metre Bell Creek shaft extension will pass through rock mass conditions that may not be fully characterised prior to sinking. Unexpected ground conditions, water inflows, or fault intersections can extend timelines and escalate costs.

- Resource conversion uncertainty: The 118,000-metre drilling program must deliver resource upgrades of sufficient grade and tonnage to justify Phase Two capital commitment. Lower-than-anticipated results at Vogel or Samson would reduce the economic case for further development.

- Capital cost inflation: Three-year underground construction programs in northern Ontario are exposed to Canadian labour market pressures, materials cost escalation, and energy price volatility, all of which have been meaningful factors in mining project cost overruns in recent years.

- Processing performance from new ore sources: Integrating ore from geologically distinct satellite deposits into an existing processing circuit introduces blending and metallurgical variables. Recovery rates and reagent consumption for new ore types may differ from the existing Bell Creek ore profile.

- Gold price dependency: The economic returns from this investment are inherently sensitive to the gold price outlook prevailing during the production ramp-up phase from 2029 onwards. Current elevated gold prices improve project economics but cannot be assumed to persist over the development horizon.

Disclaimer: This article contains forward-looking analysis and speculative projections based on publicly available information. It does not constitute financial or investment advice. Readers should conduct their own due diligence before making any investment decisions.

Near-Term Catalysts Worth Watching

For investors and analysts tracking the progression of this program, several near-term data points will be particularly informative about whether the expansion is tracking toward its stated objectives. Furthermore, drill results interpretation from the 2026 campaign will play a central role in shaping how the market values the program's progress.

- The June 30, 2026 mineral resource update for Timmins, Vogel, and Gold River will be the first major test of whether drilling is delivering the resource conversion outcomes needed to support Phase Two planning.

- The Q3 2026 corporate-level resource update will provide a broader portfolio context for the Timmins program within Pan American Silver's overall asset base.

- Progress reporting on the Bell Creek shaft extension through the second half of 2026 will indicate whether construction is meeting the three-year timeline to H1 2029 commissioning.

- Any announcements related to metallurgical test work outcomes for the Vogel and Samson ore types will provide early insight into processing recovery expectations for new ore sources.

The convergence of a partially utilised processing plant, an established underground mining complex in a historically productive Canadian gold belt, and a disciplined phased capital allocation framework creates a relatively uncommon set of conditions in the mid-tier gold sector. As reported by Mining.com, the approval of this $146 million program underscores the confidence Pan American Silver's board has placed in the Timmins asset. Whether the Pan American Silver Timmins expansion drive delivers on its promise of transforming the operation into a long-life Canadian production platform will ultimately be determined by the geological outcomes of its 2026 drilling program and the engineering execution of its three-year shaft development timeline.

Want To Stay Ahead Of The Next Major Underground Gold Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across gold and 30+ other commodities — turning complex geological data into actionable investment insights before the broader market reacts. Explore how historic mineral discoveries have generated extraordinary returns and begin a 14-day free trial at Discovery Alert to position yourself ahead of the next major find.